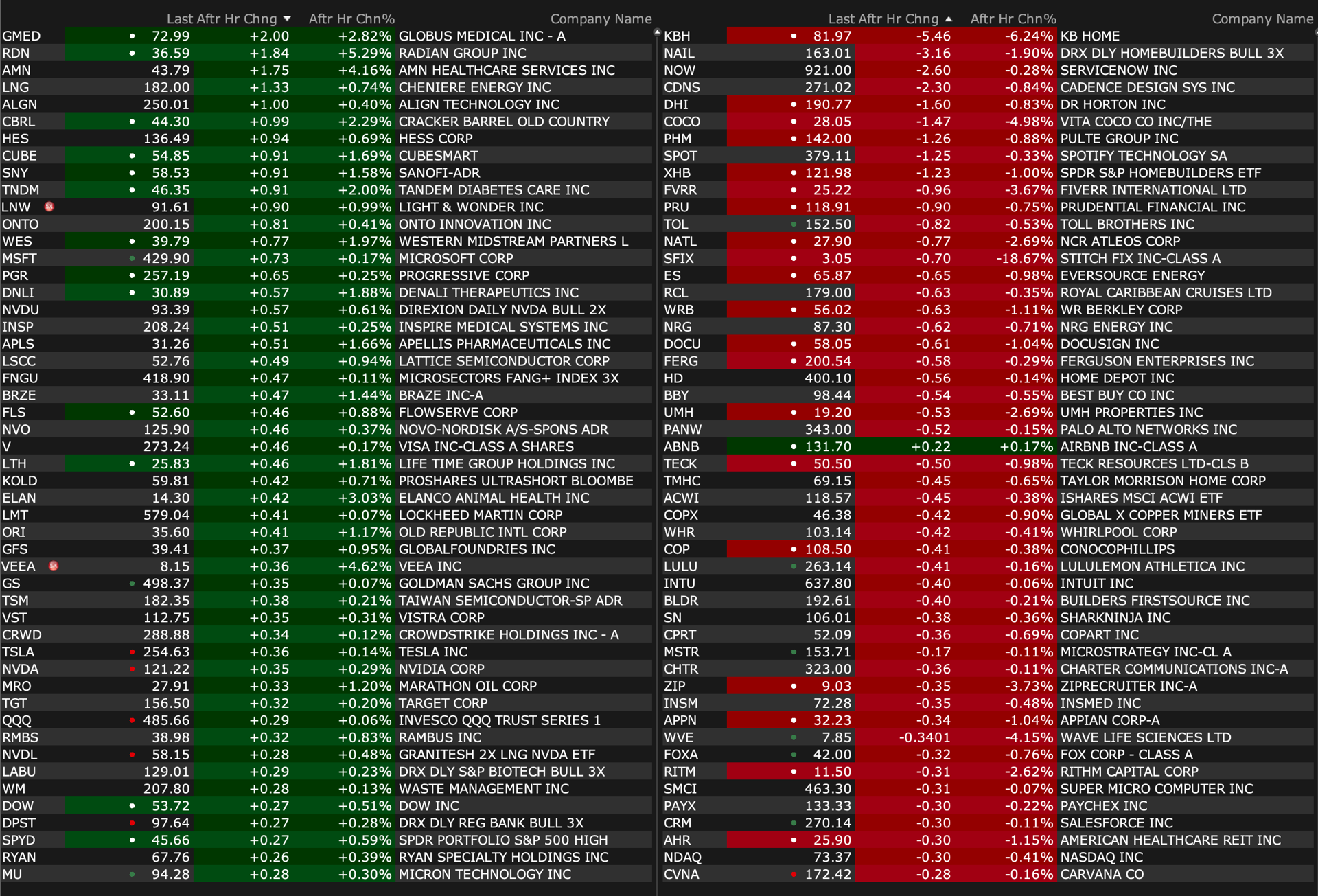

Tuesday's After-Hours Movers

As of 4:21 p.m.:

BY Doug Kass · Sep 24, 2024, 4:52 PM EDT

As of 4:21 p.m.:

BY Doug Kass · Sep 24, 2024, 4:52 PM EDT

BY Doug Kass · Sep 24, 2024, 4:47 PM EDT

New short:

Dougie Kass

Short KBH - my fourth homebuilder. KB Home - KB Home Reports 2024 Third Quarter Results

BY Doug Kass · Sep 24, 2024, 4:40 PM EDT

Wolf Street howls about tech layoffs.

BY Doug Kass · Sep 24, 2024, 4:24 PM EDT

As of 3:00 p.m. the market has, for the second day in a row, been relatively range bound'

Today's "things":

* In premarket I added to SPY short $571.12 and QQQ short at $484.99. In the regular session, a few hours later, I covered my Index shorts: SPY $567.99 and QQQ $481.10 and during the afternoon I reshorted SPY $570.82 and QQQ $486.05.

* I bought one SPY 0DTE $571 put at $0.68.

* Added to MSOS at $6.88

* Added to homebuilder shorts — GRBK, TOL and DHI.

* I shorted MCD at $301.04.

* I re-shorted Goldman Sachs GS $496.85 and MS $102.41.

* Shorted more GM.

BY Doug Kass · Sep 24, 2024, 3:10 PM EDT

I am back short Goldman Sachs GS $496.85 and Morgan Stanley MS $102.41.

BY Doug Kass · Sep 24, 2024, 2:20 PM EDT

Ocassionally I make stupid short-term market forecasts — I call them a Ludacris Forecast.

Today's forecast is that the S&P's 6 or 7-day advance comes to an end.

If you really want to be reckless and you agree with me the September 24 0DTE $571 put is trading at $0.68.

I don't trade these speculative weapons of mass destruction but I did buy ONE put.

Because I am a put(z).

BY Doug Kass · Sep 24, 2024, 2:05 PM EDT

I am adding to my General Motors GM short.

From Sanford C. Bernstein:

Yesterday Bernstein downgraded General Motors to Market Perform from Outperform with a $53 price target.

The shares have appreciated +85% since last November but Bernstein's data now signals rising earnings headwinds.

The brokerage thinks there is a risk GM will announce additional capital requirements during its October capital markets day. As such, Bernstein wants to "wait and see" which updates GM shares with the market. A continued inventory build in the U.S. could lead to pricing headwinds next year, a delayed ramp on electric vehicles and Cruise pushes losses into next year, and headwinds in GM's international businesses are increasing.

BY Doug Kass · Sep 24, 2024, 2:00 PM EDT

* Cannabis get jiggy...

Cannabis equities remain my largest long exposure of any industry sector given the extraordinarily favorable upside reward vs. downside risk.

I have devoted my Diary in the last two months to explaining my investment rationale.

If you are looking for some good resources on cannabis on X (Twitter), here are some that I view as value-added:

Toby Channabis @mayortoby

Todd Harrison @todd_harrison

Shadd Dales @thedalesreport

Anthony Varrell @V_arrell

Jesse Redmond @jesseredmond

Brady Cobb @BCobblaw

Jason Spatafora @WolfofWeedST

Jason Wild (TerrAscend) @JasonGWild

Ben Kovler (Green Thumb Industries) @BKov9

Boris Jordan (Curaleaf) @Boris_Jordan

One thing many don't understand (and most complain about) is the lack of liquidity.

As I have mentioned in the articles below, in an upturn in a sector's stock prices, the lack of liquidity becomes a positive and so is the sour state of retail investors who have gotten schmeissed in the group and have recency bias. The fact that the five largest multi-state operators have a combined equity capitalization of about $8 billion represents an outstanding opportunity for investors,

Some recent columns (in chronological order):

* Recommended Viewing (The Dales Report) TheStreet Pro

* One Bite Everyone Knows the Rules (David Portnoy endorsement) TheStreet Pro

* From My Friend Shadd Dales on Biden and Cannabis TheStreet Pro

* Green Thumb's $50 Million Buyback TheStreet Pro

* An Important Cannabis Moment TheStreet Pro

* Breaking and a Very Important Cannabis Moment TheStreet Pro

* I Don't Think the Words Mean What You Think They Mean TheStreet Pro

* Green Thumb's EPS Report Gives Me A Green Light For More Cannabis Buys TheStreet Pro

* There Is A New Cannabis Long in the House TheStreet Pro

* Getting High With A Little Help From the Markets TheStreet Pro

* Why I am Buying Cannabis Weakness TheStreet Pro

* Trade of the Week - Buy MSOS TheStreet Pro

* Markets Incorrectly Conflate Fentanyl Crisis and Likely Trump Win With Cannabis Rescheduling TheStreet Pro

BY Doug Kass · Sep 24, 2024, 12:55 PM EDT

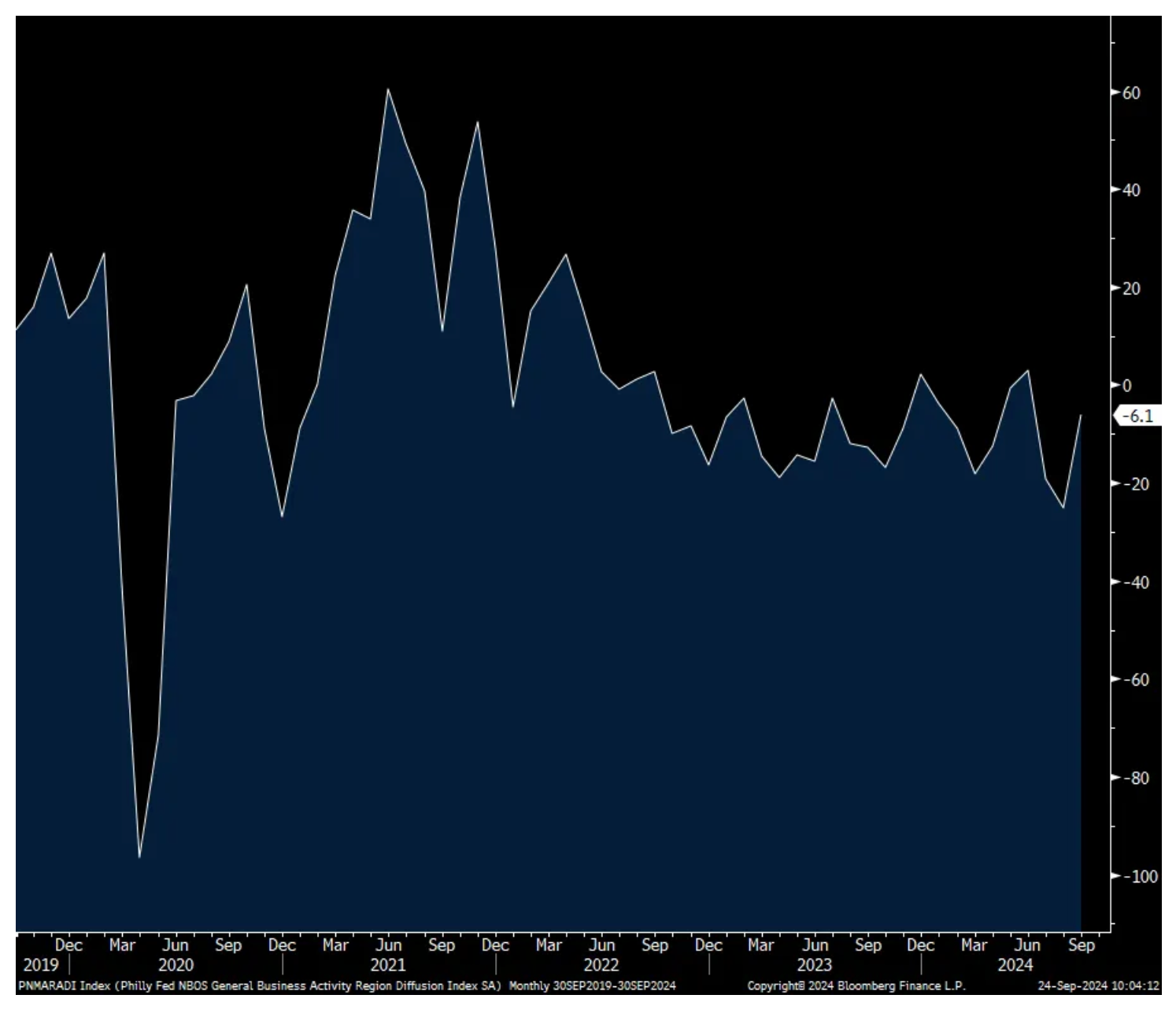

From Peter Boockvar:

A look at Philly non-mfr'g/Consumer confidence weighed down by 35-54 yr olds and lower income cohort

Out at 8:30am est was the Philly Fed non-manufacturing index which came in at -6.1, not as bad as the -25.1 seen in August but it’s only been positive twice going back to September 2022. The Philly Fed said “nonmanufacturing activity softened somewhat and remained weak.” The 6 month outlook did improve and “were more widespread for both firms and the region.” The internals are so volatile and all over the place month to month so I won’t burden you with those details but the headline number points to a continued lackluster tone in services/construction in this region.

Philly Non-Manufacturing index]

The September Conference Board Consumer Confidence index disappointed with a print of 98.7 from 105.6 in August and that was below the estimate of 104. That’s the 3rd weakest figure going back to July 2022. It was at 132.6 in February 2020. The Present Situation led the drop as it fell by 10.3 pts m/o/m to 124.3 and that is the lowest level since March 2021 and was last seen in 2016 pre Covid. The Expectations component fell by 4.6 pts but rose by 5.2 pts in August and is holding well above its lows. One yr inflation expectations ticked up to 5.2% from 5% and vs 5.3% in July.

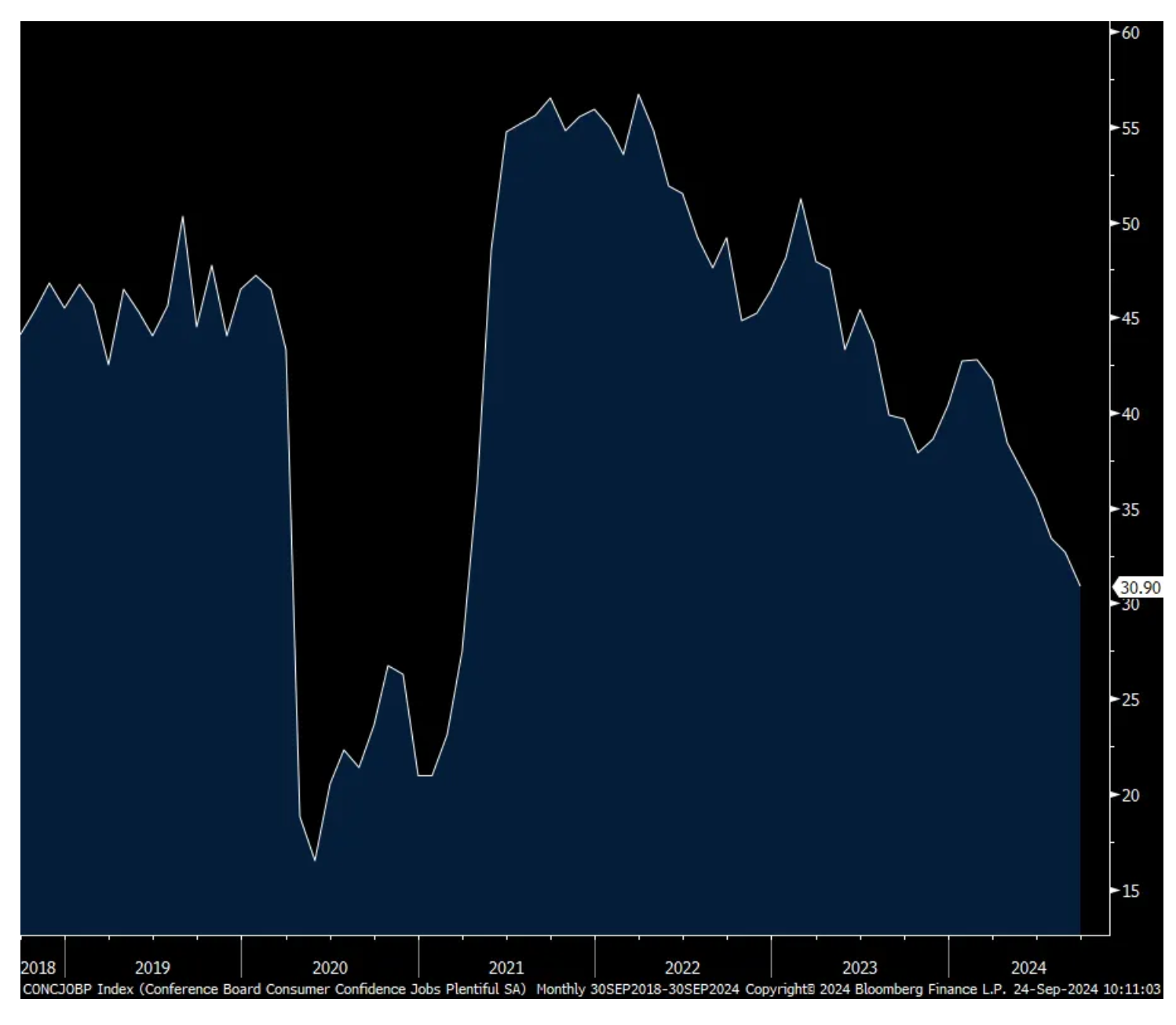

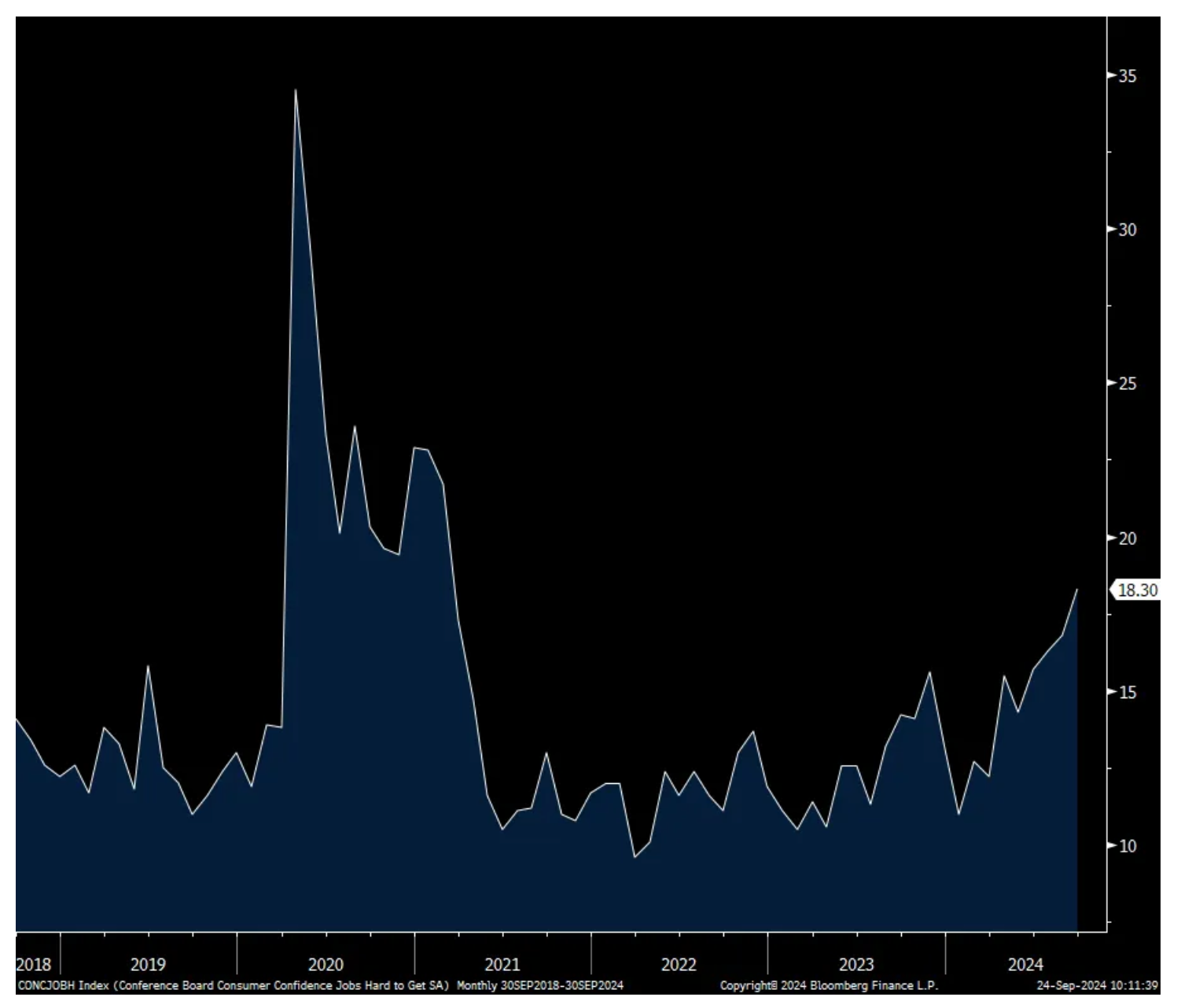

The deterioration in the Present Situation was driven by further weakness in the answers to the labor market questions. Those that said jobs were Plentiful fell to the lowest since March 2021. Jobs Hard to Get rose to the most since February 2021.

On the Expectations side, those expecting ‘more jobs’ in the coming 6 months was little changed but did rise. That was offset though by a pick up too in those expecting ‘fewer jobs’ with the balance seeing no change. Expectations softened for income growth.

With respect to spending intentions, they were little changed for vehicles and did lift for homes, likely helped by the drop in mortgage rates. They fell though for most categories of major household items.

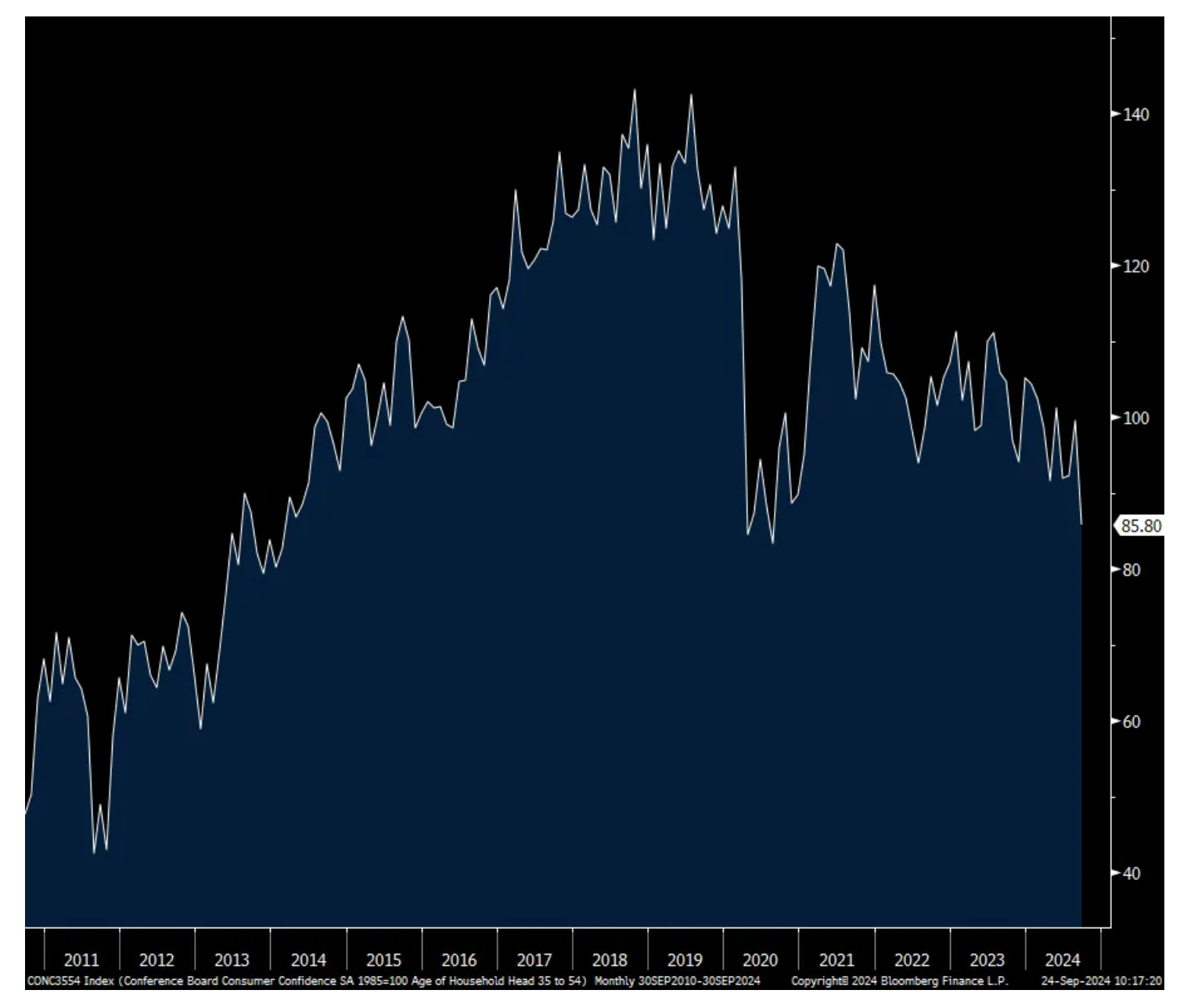

In terms of demographics, consumer confidence for the key category of 35-54 yr olds declined to a level last seen at the depths of the Covid lockdowns and back to 2014 before then. Income wise, those who make under $50,000 are stressed with confidence declines across that cohort while they were at the highest since January for those who make over $125,000.

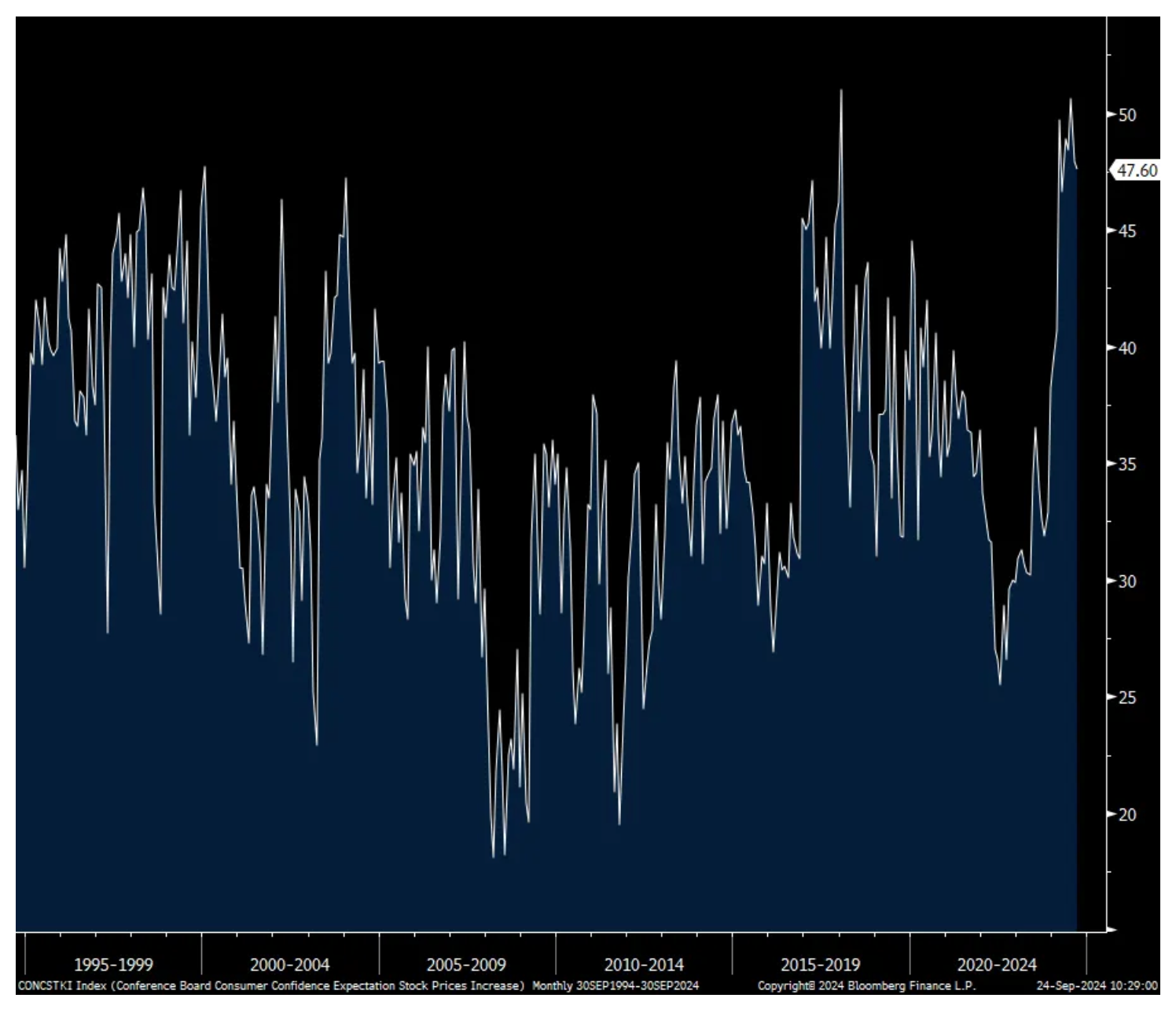

Helped by the higher confidence in that upper income category, and likely too owning stocks, they remained very bulled up with 47.6% believing in higher prices, near multi decade highs.

Bottom line, weakness being seen in the labor market was the main reason for the confidence decline and follows of course what the Fed did with a 50 bps cut instead of 25 bps. The figure also led to a bounce in the long end of the Treasury market with the 10 yr yield at 3.75% vs 3.80% earlier this morning.

Also, the Richmond manufacturing index remained very weak at -21 vs -19 in August. The estimate was -12.

Present Situation

Jobs Plentiful

Jobs Hard to Get

Consumer Confidence 35-54 yr olds

% of those who think we’ll see higher stocks

BY Doug Kass · Sep 24, 2024, 12:15 PM EDT

I re-shorted SPY at $570.82 and QQQ at $486.05.

BY Doug Kass · Sep 24, 2024, 12:07 PM EDT

Starbucks SBUX in Barron's:

Starbucks Stock Is Slipping. A New Bear Says ‘Uncertainty Is High.’ - Barron's (barrons.com)

BY Doug Kass · Sep 24, 2024, 11:50 AM EDT

BY Doug Kass · Sep 24, 2024, 11:45 AM EDT

Shorted McDonald's MCD at $301.04.

Will sell more short on a scale higher.

BY Doug Kass · Sep 24, 2024, 11:28 AM EDT

- NYSE volume 14% above its one-month average;

- NASDAQ volume 9% above its one-month average

- VIX: up 1.51% to 16.13

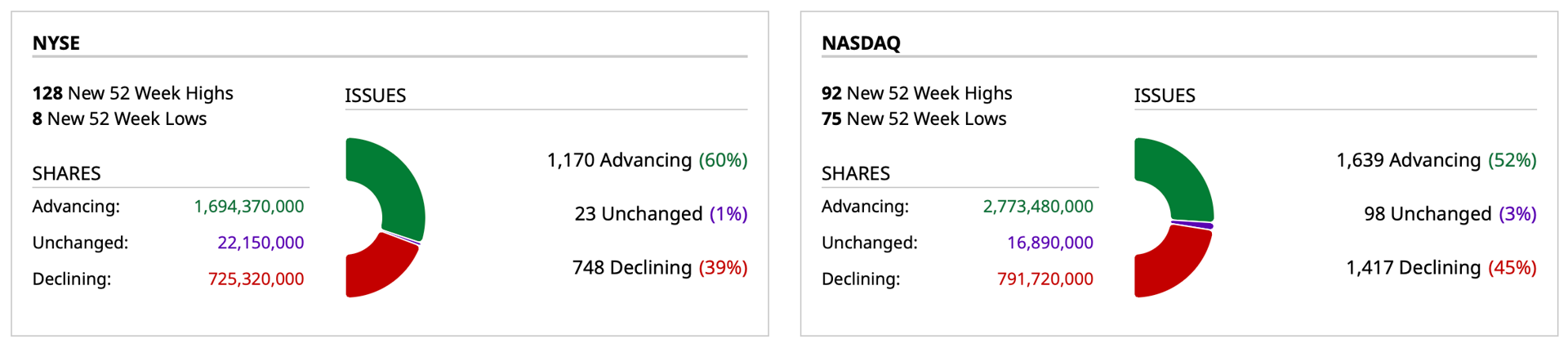

BY Doug Kass · Sep 24, 2024, 11:15 AM EDT

I'm shorting more homebuilders — Greenbrick Partners GRBK, D.R. Horton DHI and Toll Brothers TOL.

Updated short thesis delivered tomorrow.

BY Doug Kass · Sep 24, 2024, 10:50 AM EDT

I took in the day trade profitably (and in only a few hours) of my premarket Index shorts with SPY $567.99 and QQQ $481.10

From this morning:

* Added to (SPY) short at $571.12

* Added to (QQQ) short at $484.99

By Doug Kass Sep 24, 2024 6:00 AM EDT

BY Doug Kass · Sep 24, 2024, 10:30 AM EDT

From The Credit Strategist:

BY Doug Kass · Sep 24, 2024, 10:25 AM EDT

From Peter Boockvar:

China takes some bold steps, the big story of the day

The big story of the day is out of China and all the financial steps they are taking to rejuvenate their financial markets and economy and Chinese stocks spiked in response. Here is a list of things announced:

1)The PBOC cut its reserve requirement ratio to 9.5% from 10%, which is estimated to free up about 1 trillion yuan (about $140b) in fresh lending.

2)The PBOC cut the 7 day reverse repo rate to 1.50% from 1.70%.

3)There was a 50 bp drop on the average interest rate paid on existing mortgages.

4)There was a cut in the minimum downpayment to buy any home (even a 2nd one) to 15%.

5)The PBOC is creating a 500b yuan swap facility which would lend money to funds, insurers and brokerage firms to use to buy stocks.

6)There is also another re-lending facility of 300b yuan given to commercial banks that would in turn lend the money to companies and other entities for stock buybacks.

It's not just lighting a fire under Chinese stocks with the Shanghai comp up 4.2%, the Hang Seng higher by a similar amount and the H share index in Hong Kong jumping by 5.1% but commodities are rallying too. Crude oil is up by $2, copper by .12 per pound (2.7%), and iron ore by $6 (6.5%), to name a few.

Just imagine if this works in putting a floor under their housing market and one under the stock market just as most other central banks are cutting rates thinking the inflation war has been won. No surprise that European and US sovereign bonds are selling off in response. Maybe my January call for the Hang Seng to outperform the S&P 500 this year will finally work after being badly wrong so far. We own some stocks there benefiting from leisure and hospitality, along with a large life insurance company and remain very bullish on commodity stocks, particularly energy, uranium, precious metals and now ag.

It looks like we'll have to wait until December for another interest rate increase from the BoJ. Speaking to business people in Osaka, Governor Ueda said "In making policy decisions, the bank will need to carefully assess factors such as developments in financial and capital markets at home and abroad and the situation in overseas economies underlying these developments. We have enough time to do so." He also mentioned that the recent rally in the yen has eased import price pressures.

This is essentially taking off the table an October rate increase but leaving the door open for one in December or even January as he also said "If the outlook for economic activity and prices presented in the outlook report is realized, the bank will accordingly raise the policy interest rate."

In response to the continued patience reflected by Ueda in the face of a few years now of 2%+ inflation, JGB yields fell and the yen is dropping too.

The Reserve Bank of Australia held its benchmark rate unchanged as expected at 4.35% and the Governor, while less hawkish, is still not looking to cut anytime soon. The statement said "The board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome. Policy will need to be sufficiently restrictive until the board is confident that inflation is moving sustainably towards the target range."

Political influence on central banks is certainly global and it is in Australia too. Just a few days ago the Green party threatened to withdraw its support for some government legislation unless the RBA cut interest rates.

The Japanese September composite PMI fell a touch to 52.5 from 52.9 with strength in services (53.9) offsetting the flat lining manufacturing sector (49.6). Nothing market moving here as Ueda's comments dominated.

Germany's September IFO business confidence index softened again to 85.4 from 86.6 and below the estimate of 86. Both the Current Assessment and Expectations components were down m/o/m. As it always succinctly does, the IFO said "The German economy is coming under ever-increasing pressure." The manufacturing component fell to the weakest since June 2020 and the business climate for the services sector softened too. One positive was hospitality and tourism.

If there is an economy that can use a rebound in Chinese growth, it is Germany with its large export business with them.

German IFO

BY Doug Kass · Sep 24, 2024, 10:15 AM EDT

Dougie Kass

My clear objective in my Diary over the last 27 years is to provide hard-hitting, thought providing and contrarian views that you will not see on FINTV, will not read in the business media and certainly wont read on sell side research on Wall Street.

You don't have to agree with my views or conclusions (and I don't make recommendations), but non consensus thought is the hammer on the anvil in the search for superior investment returns.

No one has the concession on the investment truth.

No one possesses the secret sauce to investing.

Today's opener and yesterday's incorporate my above objectives.

Thanks.

BY Doug Kass · Sep 24, 2024, 9:50 AM EDT

Added to MSOS on the early dip at $6.88.

BY Doug Kass · Sep 24, 2024, 9:48 AM EDT

In light of our software publishing issue I don't think many had a chance to read yesterday's opener.

I am reposting it here:

* In the end, there is only one absolute truth about investing — Charlie Munger and Howard Marks are right, it is not easy.

* Those that think investing is easy overlook the market's nuances and complexities.

* So, I call BS to "first level thinkers" who see what is on the surface, react to it simplistically — buying or selling stocks on the basis of their reactions.

* I also call BS to the ongoing bullish and near universal narrative regarding the supposedly neat relationship of stock prices to the consensus 2025 S&P EPS forecast.

* And I continue to call BS to the poor quality of reported EPS.

The title of this morning's opening missive is taken from a wonderful quote from Charlie Munger. That quote captures today's market zeitgeist.

The investment mosaic is complex but many "talking heads" try to simplify their analysis. Indeed, today, "first level thinkers" dominate the investing landscape, but as always (as Carl Sandburg does below) should be questioned:

Two cases in point:

* The notion that equity prices neatly track S&P EPS closely.

* The quality of reported and forecast corporate profits (specifically that of the S&P Index) is suspect.

Let's start with the first misnomer — that stock prices track EPS.

This is a constant refrain I have heard in the business media (with only slightly different iterations) over the last two weeks. It is first level thinking personified (see Howard Marks' quote above), that comes off the tongue easily and is easy for the legions of investors to digest. That bullish refrain goes something like this:

"If consensus S&P EPS rise as expected next year (a projected gain of +14%), stocks have a long runway to rise higher."

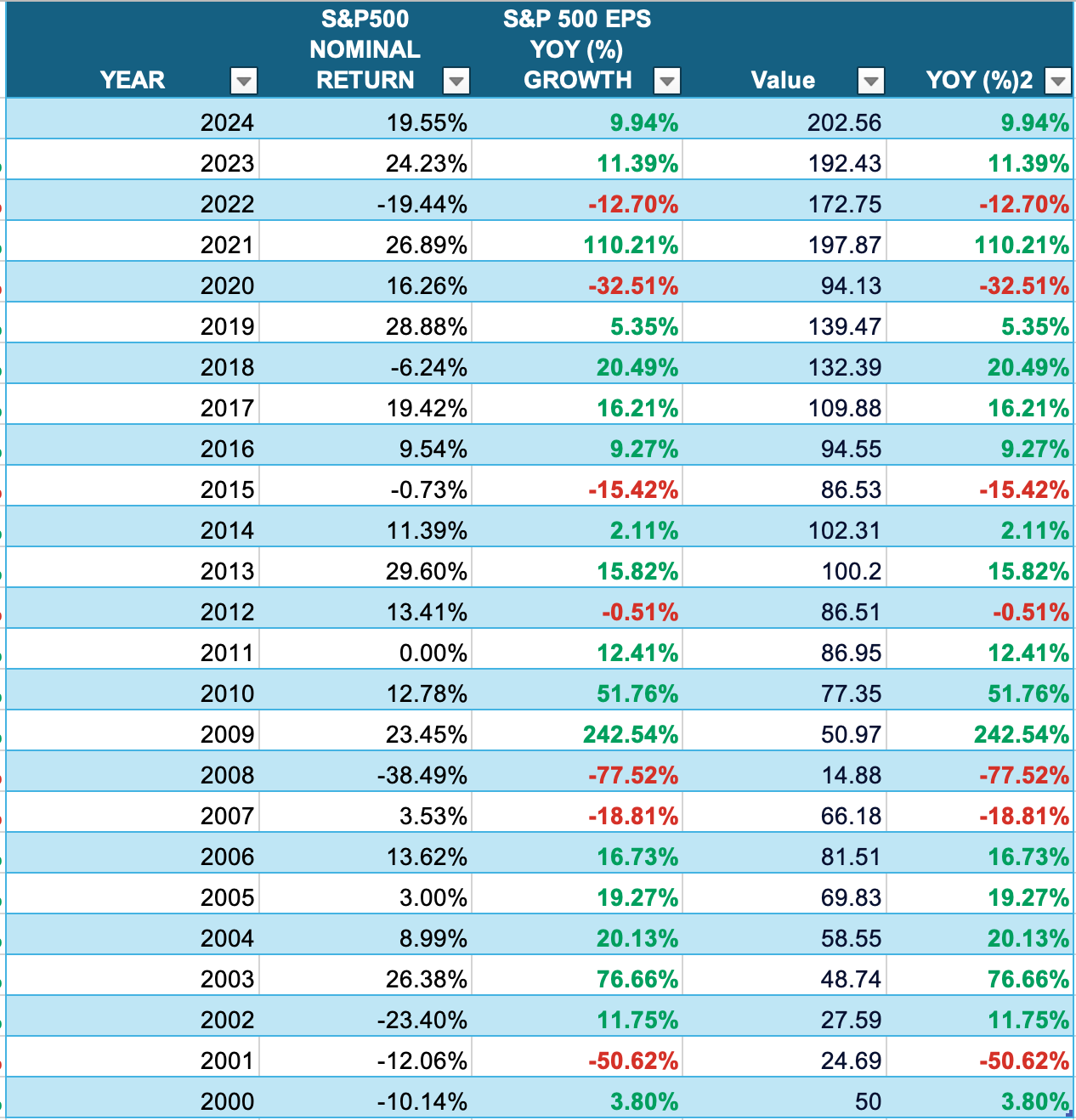

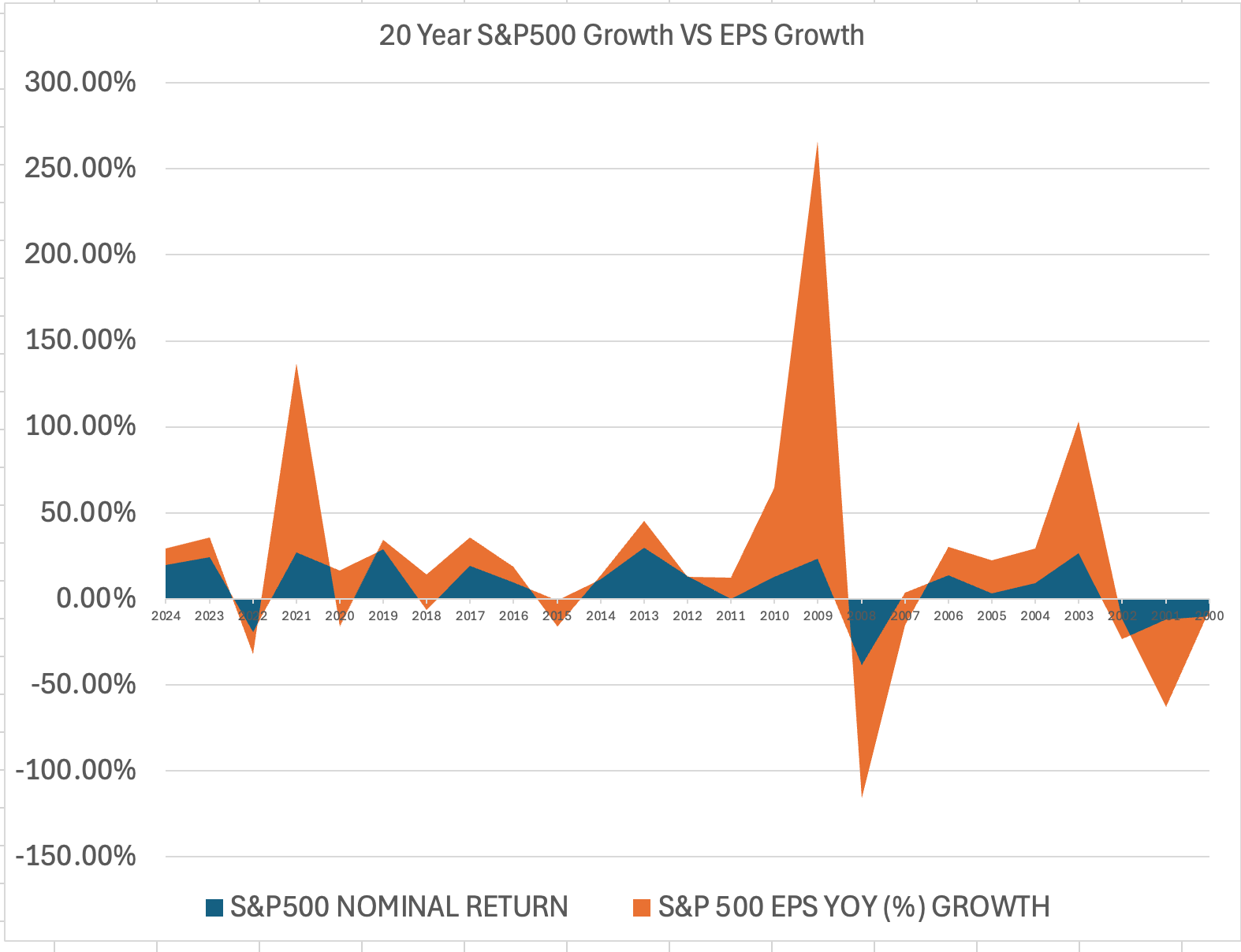

The following table is a 25-year compilation of annual change in the price of the S&P Index compared to the yearly change in S&P EPS EPS:

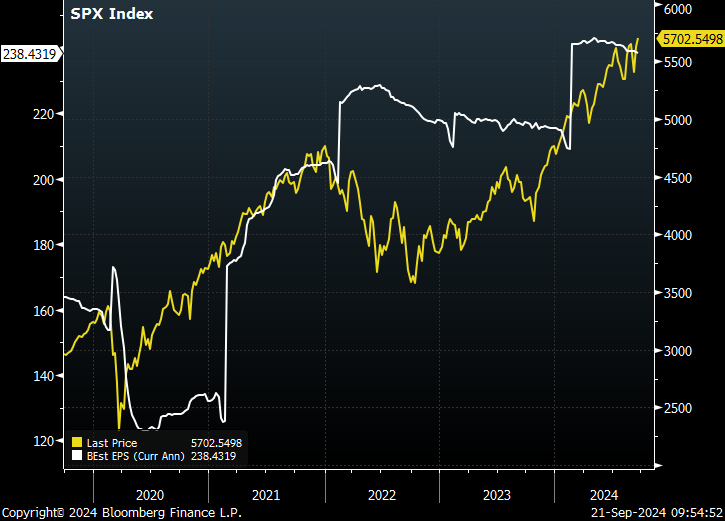

Here is a chart (prepared for us by Peter Boockvar), going back only five years measuring direction of the same two components:

These tables suggest that at times, stocks outperform the S&P Index. When this occurs, it is typically called a valuation reset in which price-earnings multiples outpace profits.

At other times stocks underperform S&P EPS. When this occurs, valuations contract.

Sometimes, as Warren Buffett reminds, our markets are a "drunken sailor."

In looking at the above charts, one can argue that the performance of equities over the last two years (and since 2019) are vulnerable as stock prices have outpaced the growth in reported EPS.

***

Let's now shift back to a column I wrote, "Is the Bull Run Based on a Bunch of Bull?" in early September that questioned the quality and level of reported S&P EPS:

Investors tend to believe what they want to believe. But fairy tales don't come true... even when it happens to you.

Investors tend to be bullish and believe the superficial BS that comes down the pike.

It is the nature of the human spirit to be upbeat — especially when it comes to our investments.

Unfortunately we can prove anything by statistics except the truth.

But tearing down "the statistics" and accepted truths can sometimes be revealing and lead to being more objective and a better investor.

As proven by the past (especially in the lead up to The Great Financial Crisis) objective analysis can also keep us from being trapped in false narratives and reduce the likelihood of losing loads of money!

Fairytales can come true, it can happen to you

If you're young at heart

For it's hard, you will find, to be narrow of mind

If you're young at heart

You can go to extremes with impossible schemes

You can laugh when your dreams fall apart at the seams

And life gets more exciting with each passing day

And love is either in your heart, or on its way

- Johnny Richards and Carolyn Leigh, Young at Heart

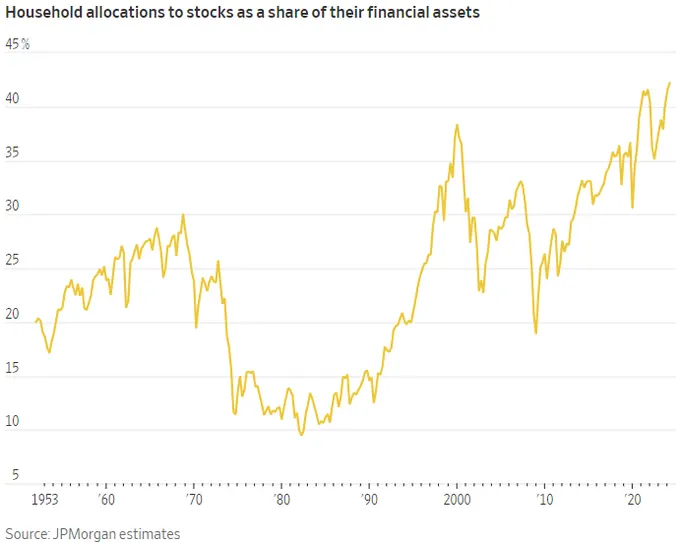

As I have noted recently, at 42%, households' allocations to equities is at the highest level in 72 years:

Household allocation to equities is at the highest level since 1952 — in part to the belief of a "Goldilocks" fairytale (an economy not too hot and not too cold).

To this observer, this allocation and the associated bullish investor sentiment may not be justified in the face of a number of headwinds including but not restricted to economic (slugflation likely lies ahead), policy (fiscal and monetary), political and geopolitical concerns, systemic stability and, the subject of today's missive — serious questions of what is the true level of S&P EPS that supports historically high (above 90%-tile) valuations.

But perhaps even more important is the lack of reliability of the economic data that forms our investment decision process.

From The Credit Strategist:

"Investors are unduly reliant on the Fed lowering interest rates and economic data whose reliability is increasingly subject to question. While they are rooting for the Fed to lower interest rates, it is unlikely that the Fed will do so aggressively. I have argued that the Fed shouldn’t do so at all until next year because it should maintain positive real (inflation-adjusted) rates at a respectable level and I don’t believe real rates are there yet. Despite government inflation statistics, real-world inflation is still pretty high (and remember, it is off a much higher base than before the pandemic). And recent events give little reason for us to trust the data supplied by the government. The recent elimination of 800,000 jobs from 2024 data by the Labor Department was an embarrassing error that shows the unreliability of government economic statistics. This was not a one-off correction. The government routinely retroactively adjusts economic statistics to a degree that shows they were highly inaccurate at the time they were released. This highlights the absurdity of the “countdowns” and other television hoopla that surrounds each Fed meeting and other economic news releases. We just have to hope that Rick Santelli doesn’t throw an embolism hyperventilating about the latest report of whether PCE comes in one-tenth-of-a-percent above or below the (totally blind) consensus. Investors treat this data like Buddhist monks interpreting koans when the information is no more meaningful than the crap printed on Page Six of The New York Post. No wonder the market behaves like a cross between a casino and a circus. The blind are leading the blind and they are all dressed up like Bozo."

Which brings us to the issue as to whether we are utilizing too-high S&P EPS numbers in justifying current valuations. (Make no mistake about it, even before my critical view of corporate profits — valuations are sky high based on historical comparisons!)

It is my conclusion that reported S&P EPS are no more accurate than government statistics. Indeed, I call BS to the level and manner in which S&P EPS are calculated in order to support bullish valuation arguments. And to government statistics that are not worth the paper they are written on.

When strategists and money managers justify their bullish market views based on unrealistic past and forward S&P EPS consider that those EPS numbers are routinely inflated by as much as 25% by non-GAAP adjustments. This serves to disguise cash flow and other key data points that are used in valuing equities.

Most investors disregard "adjustments" — certainly quants, machines and algorithms do! And, as I noted Wednesday, with so much capital flowing into passive products and strategies and with massive infusions of liquidity via central banks, there are few attempts to understand the increasingly complex, adjusted and fine-tuned.

Back to The Credit Strategist:

"The quality of reported earnings, and the quality of earnings reporting, is nothing less than appalling. This may make it challenging (and fun) for those of us trained to dissect balance sheets and financial filings, but it contributes to the false narrative that corporate earnings are robust. It also allows corporate managements to inflate their compensation by pumping up their stock prices with phony numbers. Non-GAAP adjustments contribute to the chronic overvaluation of stocks; they are no less a part of this systemic problem than profligate monetary and fiscal policy. When the book is written on the next financial crisis, bogus earnings will fill one of the chapters."

Facts are stubborn but statistics are more pliable.

Investors are basing their optimism on the fairy tales of inflated S&P EPS numbers as well as phony government statistics (see the recent revision of 818,000 jobs in the labor market!)

Believing in fairy tales is as old as the hills — and as long as equity prices keep rising (and the system stays intact) few question consensus narratives (as weak and superficial as they may be).

The lack of penetrating or even realistic analysis led up to The Great Financial Crisis, which few recognized as it unfolded.

Many similar issues — in deciphering "real EPS" and in the area of regulation — existed in 2008 that exist today.

Back then the U.S. government solved the debt crisis by creating more debt, rendering the financial system increasingly more fragile and prone to instability.

Since then, the illusion of prosperity (see our burgeoning deficit and U.S. debt) and the too liberal interpretation (at best!) of reported and projected U.S. corporates (measured as EPS) have convinced most investors that equities are inexpensive and that another financial crisis is avoidable.

These optimistic conclusions, like fairy tales, could end badly for investors.

For these reasons and others, the current level of unquestioning market optimism is a classic contrarian sign.

I prefer second level thinking over first level thinking.

Importantly, there are numerous and growing headwinds (social, political, geopolitical), off sided and undisciplined (monetary and fiscal) policy, the threat of a reacceleration of inflation, the vulnerability to profit margins (which have expanded steadily over the last five years), etc. that when combined with the recent revaluation higher in stock prices and the low quality of stated EPS suggest caution is now called for.

Not only don't stock prices neatly track reported EPS (which can also be debated in their quality) but it is likely that the aforementioned valuation reset (that has put equities in over the 90% tile in all classical measures of valuation) may have already more than discounted a gain in forecasted S&P EPS next year.

Those that think investing is easy overlook the market's nuances and complexities.

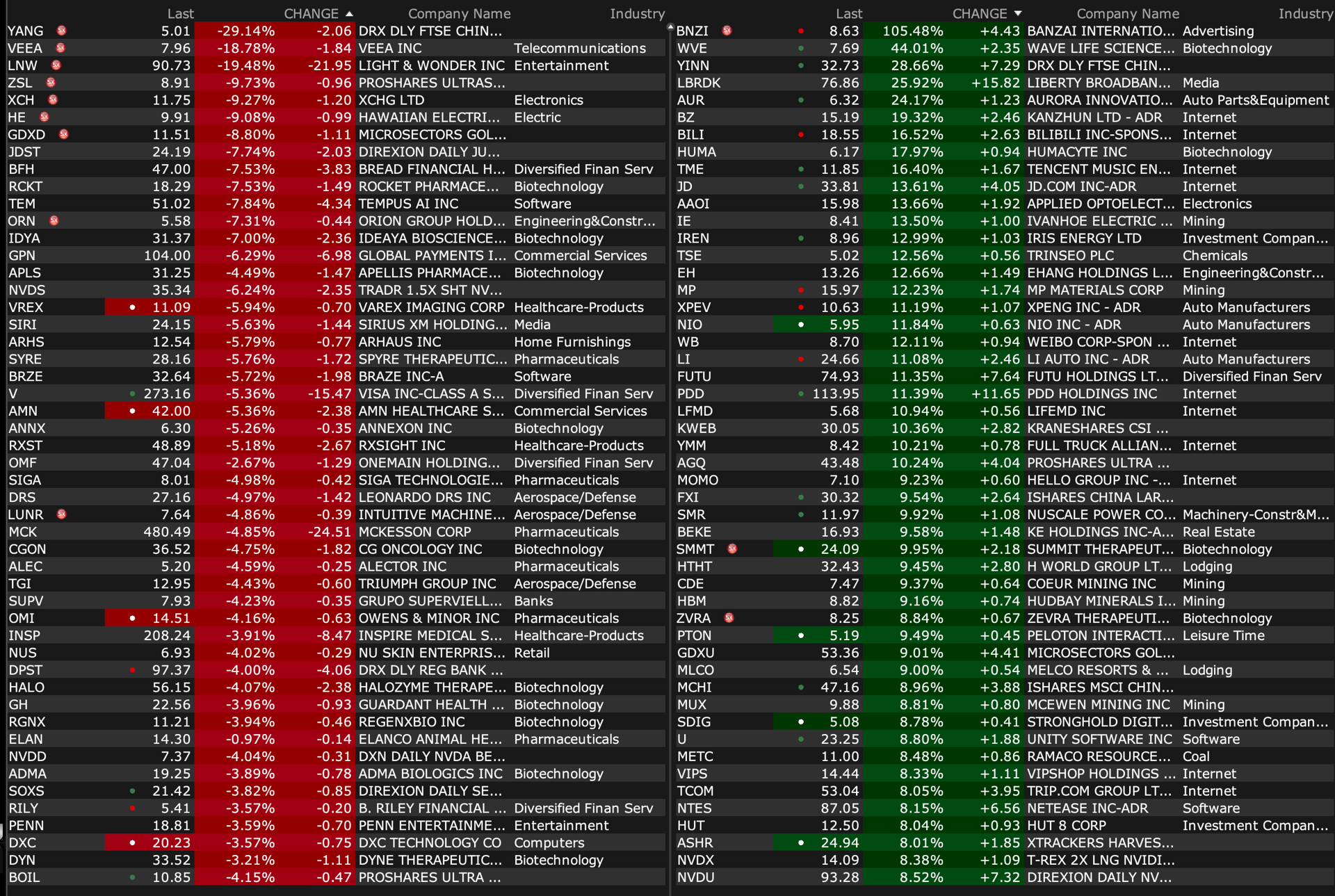

BY Doug Kass · Sep 24, 2024, 9:35 AM EDT

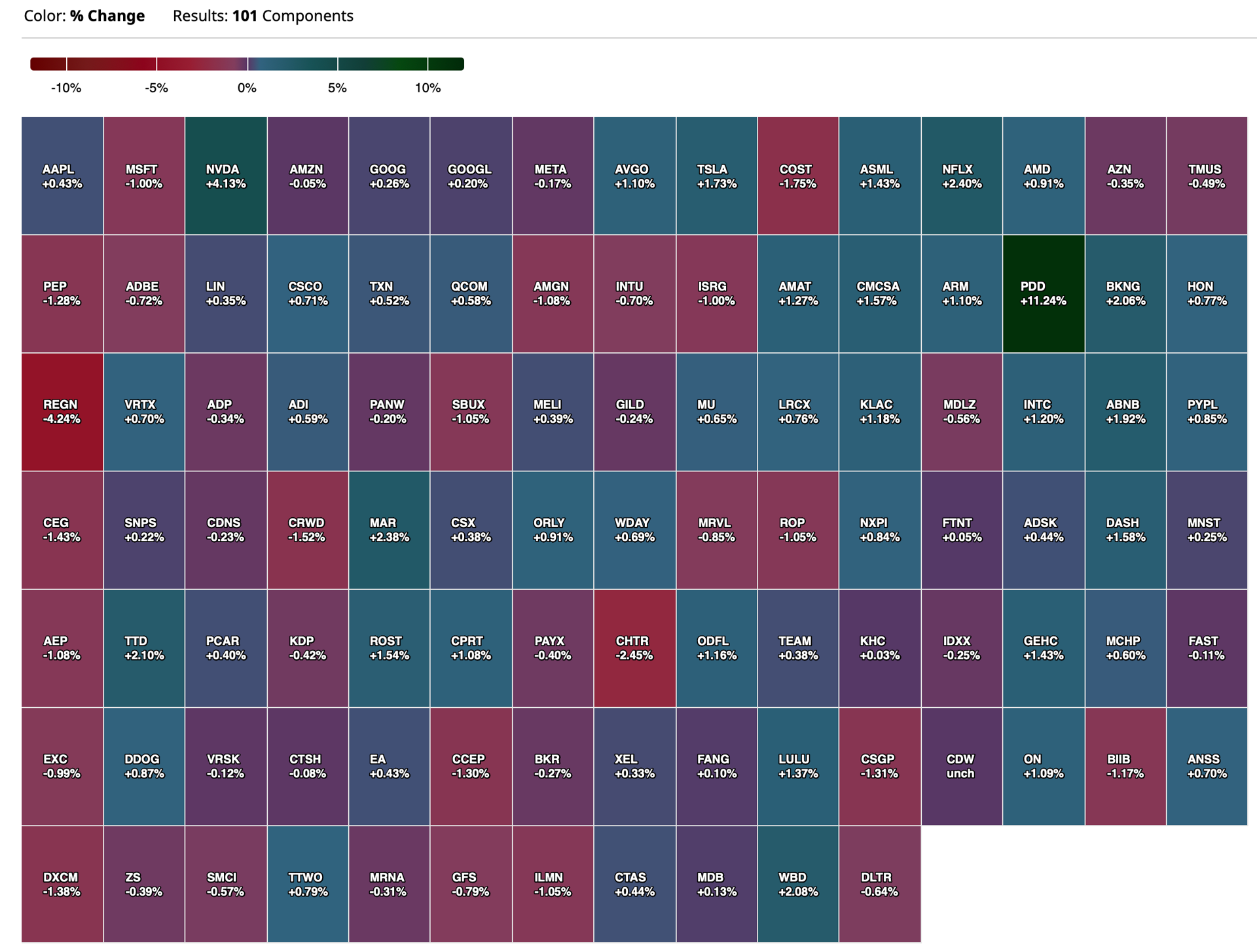

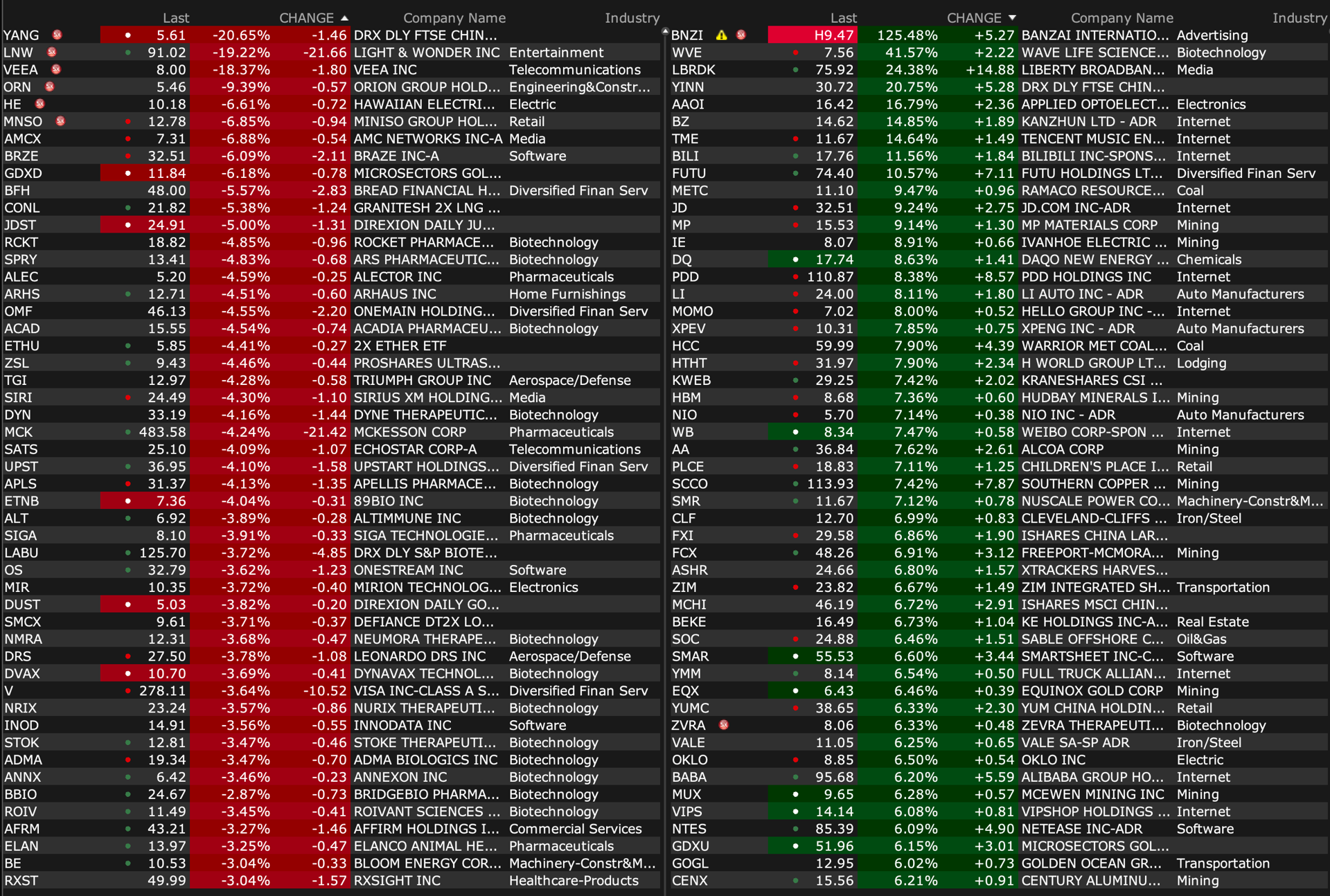

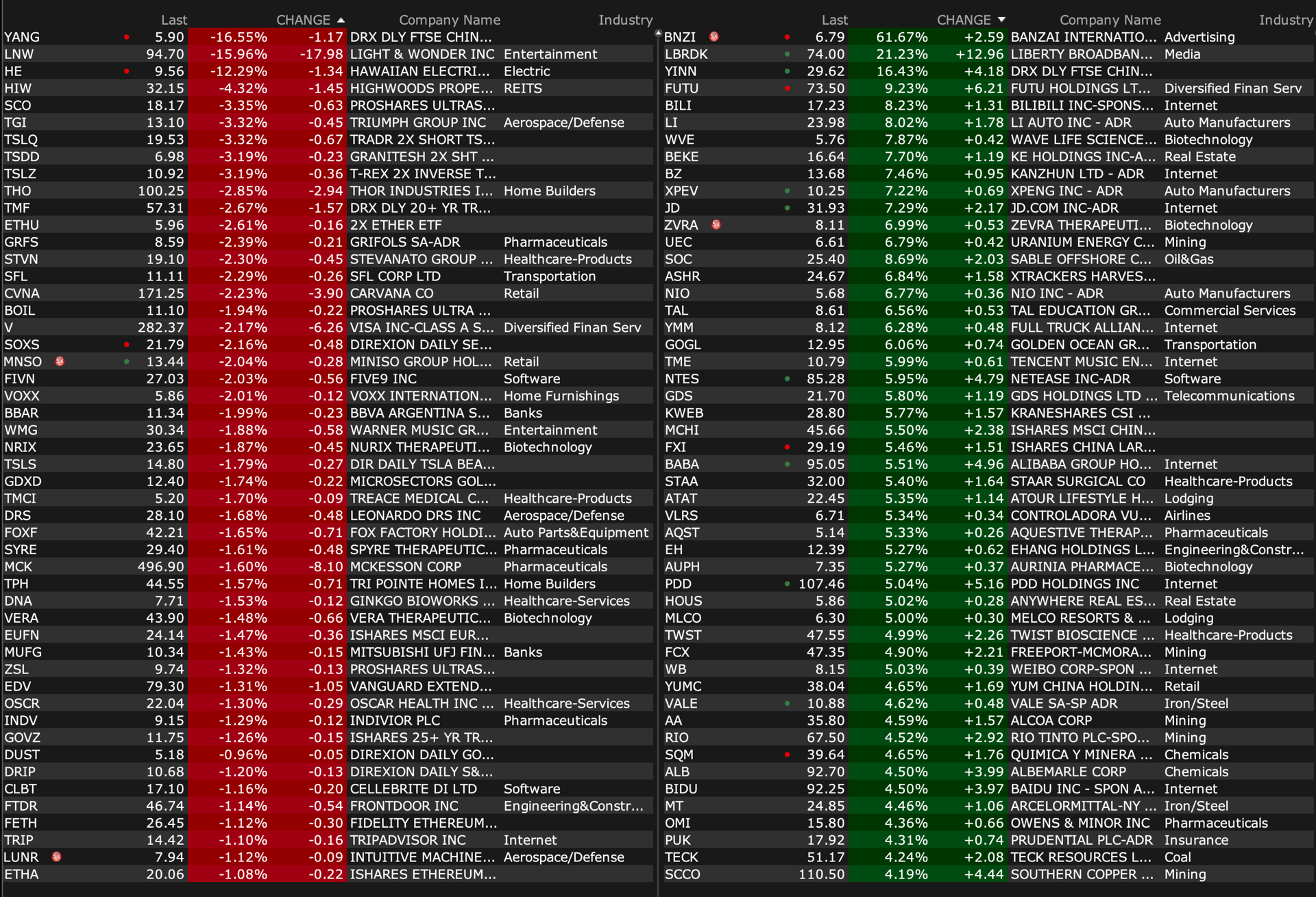

Upside:

-MSS +110% (earnings)

-SEEL +88% (announces signing of Material Transfer Agreement with US Army Medical Materiel Development Activity (USAMMDA) to evaluate SLS-002 for treatment of PTSD)

-VBFC +45% (TowneBank to buy company for $120M, or $80.25/shr cash)

-GBNY +35% (plans to dissolve)

-LBRDK +22% (submits counterproposal on all-stock merger with Charter at 0.29 Liberty shares for one Charter share)

-LWAY +17% (Danone (23.4% stakeholder) offers to buy Lifeway for $25/shr in cash)

-CAPR +8.9% (plans to file a Biologics License Application (BLA) in October 2024 for deramiocel to treat Duchenne muscular dystrophy (DMD) cardiomyopathy)

-WVE +8.6% (announces positive interim data from FORWARD-53 clinical trial evaluating WVE-N531 in Boys with Duchenne Muscular Dystrophy Amenable to Exon 53 Skipping)

-AIR +7.3% (earnings)

-GROV +6.9% (announces $15M PIPE Investment from Volition Capital)

-BABA +5.5% (China PBOC, SCRC and NFRA (China’s top 3 financial regulators) briefing: To cut its RRR by 50bps "soon" with a further RRR cut of 25-50bps possible by year-end; Plans at least CNY500B of liquidity support related to equities)

-EL +3.8% (China stimulus measures expected to help luxury names)

-WYNN +3.1% (China announces stimulus measures)

-BASE +2.9% (Director Anderson buys $300K of common shares)

-ICL +2.6% (opens new food specialty plant in China)

-BLUE +2.3% (initiates restructuring intended to optimize cost structure and enable quarterly cash flow break-even in H2 2025; To cut jobs by ~25%)

Downside:

-BIVI -54% (prices 1.96M shares at combined price of $1.53/share for gross proceeds ~$3M)

-LNW -17% (received an order from the U.S. District Court for the District of Nevada granting Aristocrat a preliminary injunction relating to L&W’s Dragon Train game)

-HE -12% (prices ~54M shares at $9.25/shr)

-RCAT -8.2% (earnings)

-AZO -3.7% (earnings, guidance)

-IVT -3.2% (prices 8M shares at $28/share [upsized from 6.5M shares])

-THO -2.8% (earnings, guidance)

-SNOW -2.2% (files $2B of Convertible Senior Notes offering)

-V -2.2% (reportedly facing DOJ antitrust case over alleged debit card market monopoly)

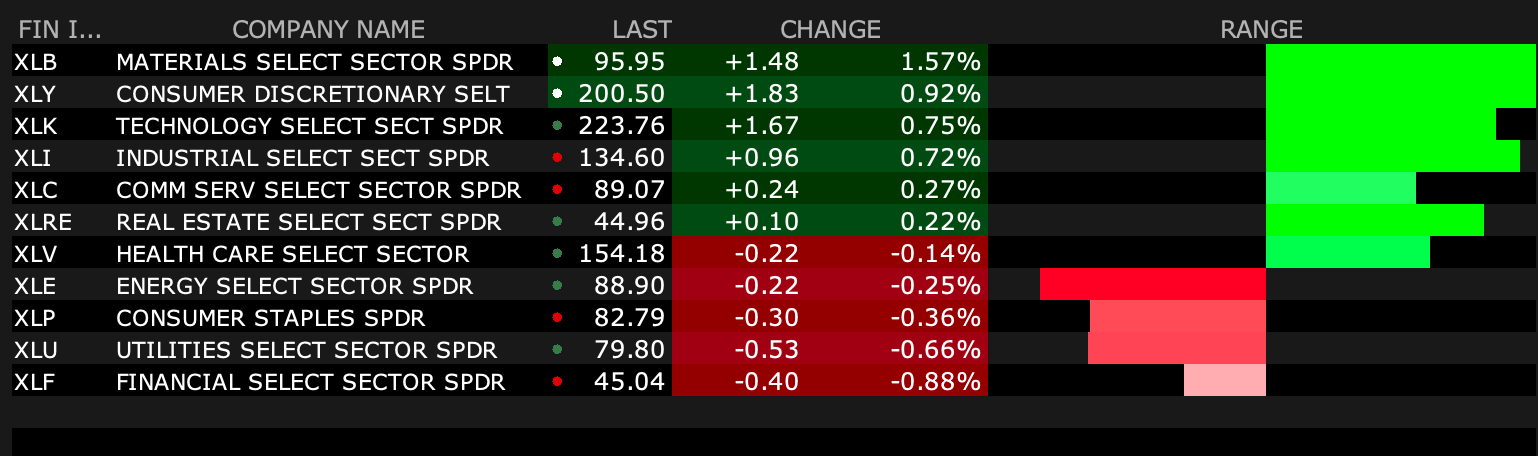

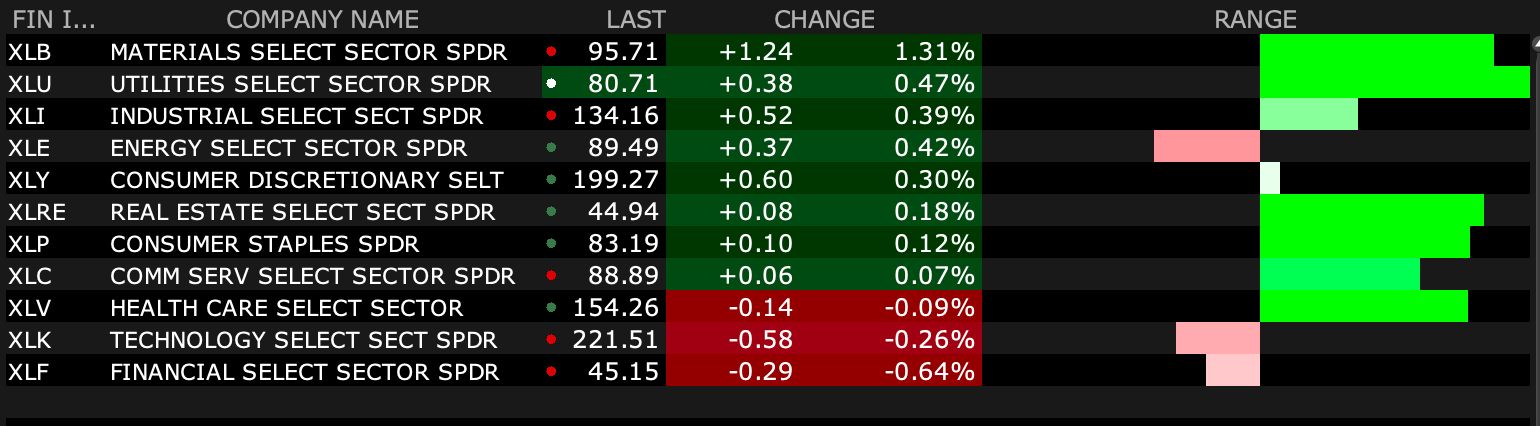

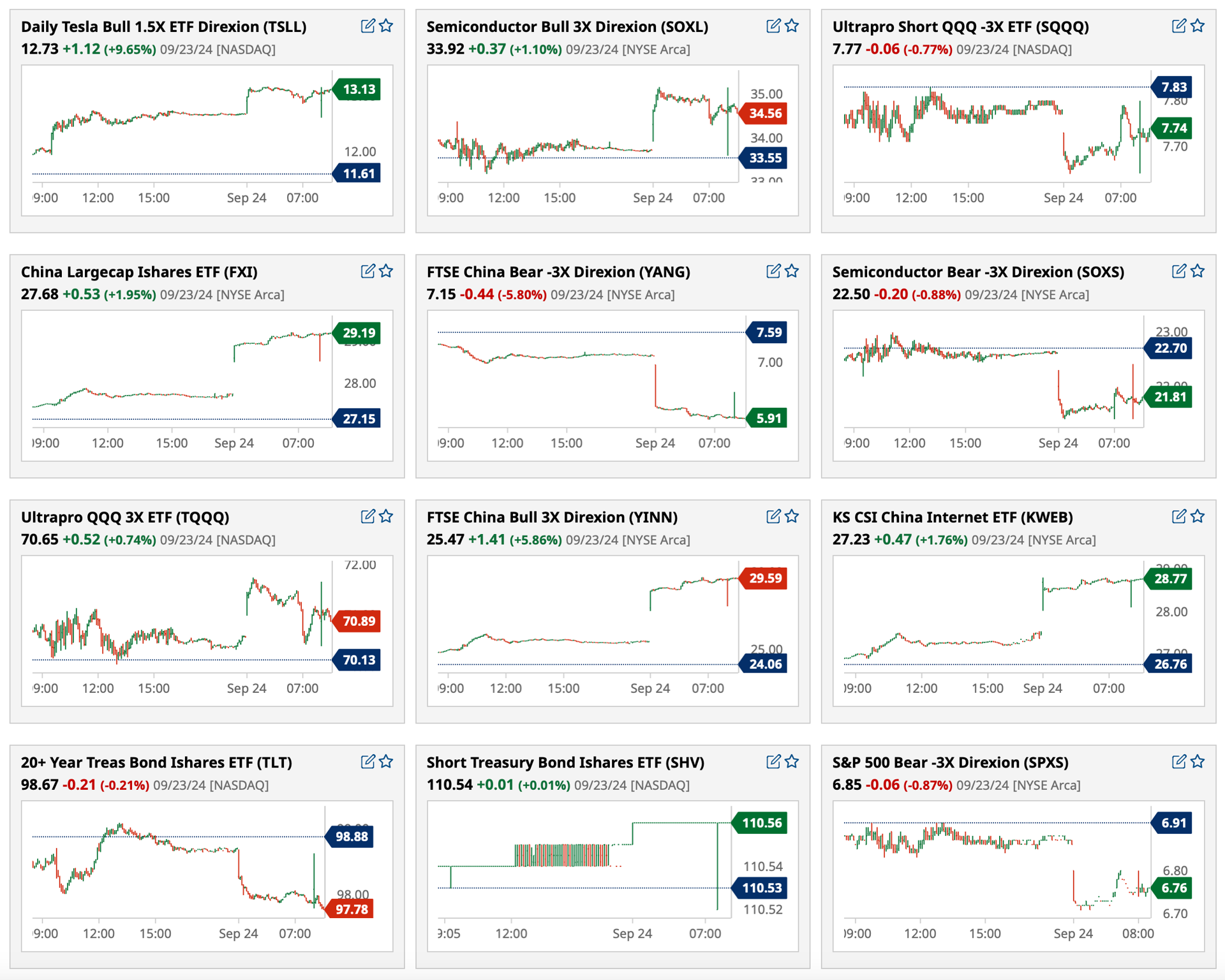

BY Doug Kass · Sep 24, 2024, 9:15 AM EDT

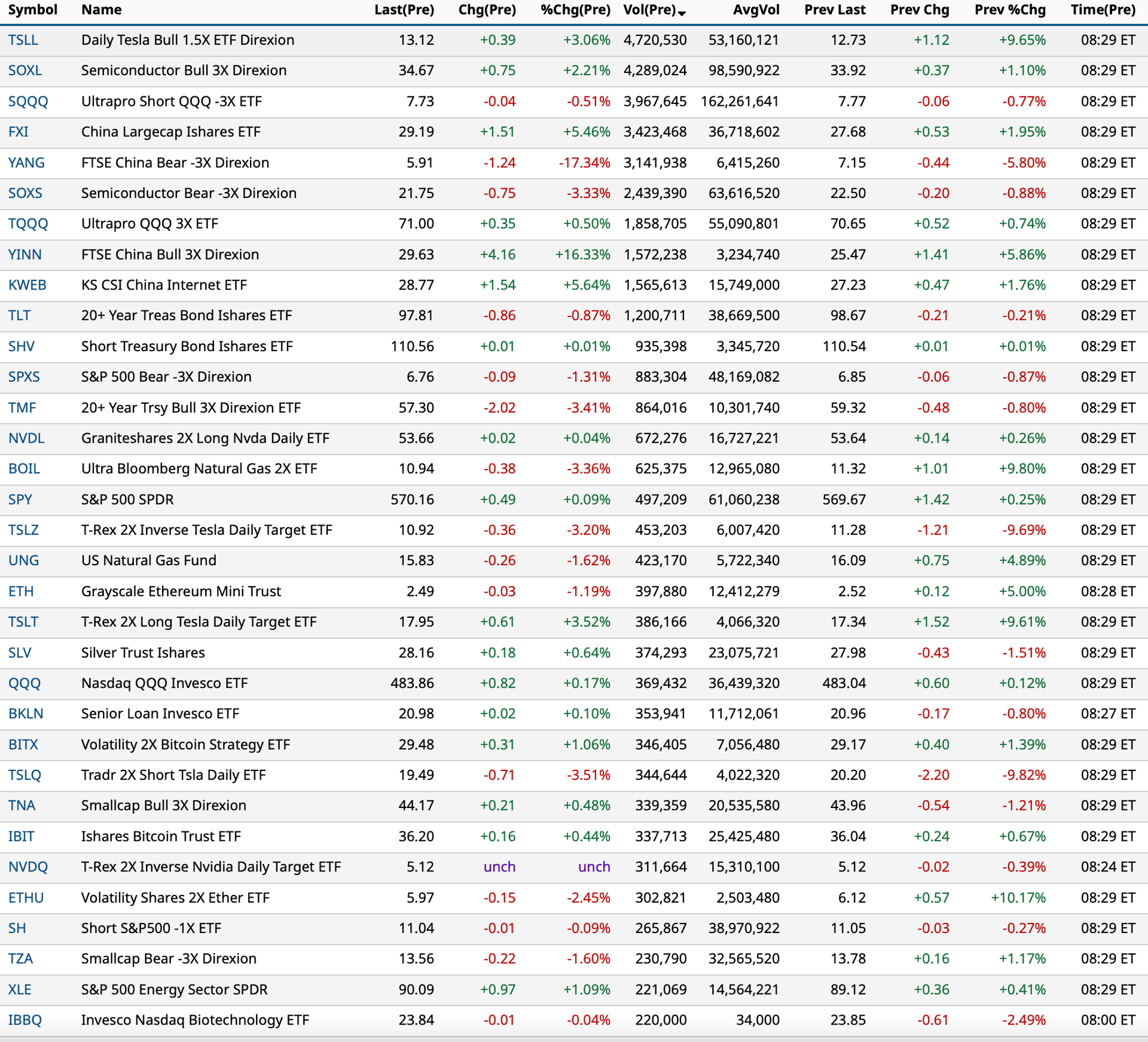

As of 8:29 a.m. and their mini-graphs:

BY Doug Kass · Sep 24, 2024, 9:10 AM EDT

As of 8:45 a.m.:

BY Doug Kass · Sep 24, 2024, 9:05 AM EDT

* The jury is still out what the dominance of passive investing means to a rational investing process, the proper allocation of capital/resources and even for our society.

* You will rarely read or hear about this concern in the business media, so read on...

The point of yesterday morning's opening missive, "It's Not Supposed to Be Easy...Anyone Who Finds It Easy Is Stupid" and the purpose of my Diary is to offer up contrarian analyses and observations that you will not regularly see from Wall Street sell-side research or in the business media.

After all, investors and traders are force fed (on a silver plater) optimism on Fin TV and from Wall Street. This makes sense as over 95% of investors are "long only."

To read my Diary, which often comprises a non-consensus view, I think has value in that it can be incorporated in your investment decision-making process.

Case in point my near 50 columns entitled "More Tales From Nvidia." These columns, especially when Nvidia NVDA and other generational compounders spurt higher, are criticized by some of our subscribers (e.g. JeffI and Masterhedge) — and this is their privilege and right as subs. But they miss the point, in my view. I serve up these columns to provide an alternative view from the spoon-fed and perma-bullish cabal on Wall Street and in the business media. I believe this is value-added.

Despite the protestations of some, I would point out since I launched this series NVDA's share price is flat against an S&P 500 Index that has risen by over +5%.

Coincidentally, I would also note a skeptical and recently published New York Times article on AI, in which a serious analyst (Jim Covello, Head of Research at Goldman Sachs) provides a downbeat outlook for AI, touching on many of the concerns I have expressed in my columns on Nvidia in my Diary.

Yesterday's opener (to be reposted after this article as many missed because of our software issues) dealt with the poor quality of reported S&P EPS: Today's opener entails a brief discussion of the threat of market structure (which is also rarely discussed in the business media).

My view is that the markets have increasingly become unhinged (both on the down and up sides). As a result, price moves are exaggerated and some very weird stock outliers have populated our markets (think: GameStop GME, AMC Entertainment AMC and most of Cathie Woods' ARKK portfolio (!)).

Importantly, for those that have a solid sense of "intrinsic values" (as I believe my hedge fund, Seabreeze Partners, has), the ramifications and inefficiencies of market structure provides an opportunity for the dispassionate investors.

Inefficiencies, sharply exaggerated stock action/movement and investing pain and gain are the byproducts of today's perilous market structure:

1. Passive Domination: As noted in my Diary for a decade, the swift transition from active money management to passive money management has been profound. According to several academic studies, passive products/strategies account for about 75% of trading volume every day.

Active managers are generally fundamentalists, passive managers generally know everything about price and nothing about value. The quantitatively based risk-parity fund knows absolutely nothing about Nvidia's fundamental outlook but everything about its price momentum (and worship at the altar of price).

Today many traders and investors (like quant funds) worship at the altar of price momentum — often forcing participation from market participants (who sometimes put themselves in an unsafe position).

And never discussed is that passive strategies are often dramatically leveraged products — holding obvious risk when momentum changes and everyone is on the same side of the (long) investing boat. Risk parity, for example, can be 5x to 10x leveraged.

2. Increased Crazy: Social media, meme stocks (read: Paramount Global PARA (which rose to over $100/share during the Bill Hwang era), GME and AMC) message boards, etc. have served up some weird/crazy price action (more often than not producing more losses than gains). So convinced are meme traders that they facilitate non understandable capital allocation (i.e. money is raised on the extraordinary moves higher). The notion that a small group of traders think they are smarter than the overall population of investors never ends well. And this sort of phenomenon (read: reckless gambling) continues to sprout up.

3. Option Speculation Has Intensified: The proliferation of 0DTE (zero days to expiration) options — which now account for the majority of options trading (and may somewhat be viewed as a product of #2 above) — is another market structure risk. To be kind, 0DTE is the manifestation of a YOLO ("you only live once") trading. To think that nearly 55% of total trading activity has a term of under one day is astonishing... and frightening.

4. Other Technological Advances Raise More Risks: The dominance of passive products (#1) has now been embraced by brokerage firms and investment advisors. Computer-generated investing strategies, intended to create a sense of safety for retail investors, have often backfired in market history.

5. Heightened Risks of Expanded Transparency: Today's transparency has an upside— it provides instantaneous information to the masses (which in the past was restricted to the privileged, wealthy, to those financial institutions that produced the most commissions and "positioned"). The problem with transparency, though, is that some of it is inaccurate, which has many investing and political ramifications.

BY Doug Kass · Sep 24, 2024, 8:15 AM EDT

BY Doug Kass · Sep 24, 2024, 6:38 AM EDT

The Short Range Oscillator prints at 6.86%. This compares to the previous day's 7.30%.

BY Doug Kass · Sep 24, 2024, 6:28 AM EDT

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Sep 24, 2024, 6:18 AM EDT

From JPMorgan:

US: Futs are higher, led by Tech with Small-caps underperforming; pre-mkt Mag7 are mostly higher led by TSLA, with Semis bid up, too. The key overnight news was China’s latest stimulus measures which aided China/HK Equities to more than 4% gains. This news is boosting the commodity complex with both Energy and Base Metals seeing gains. Bond yields are 1-4bps higher as the curve bear steepens; USD is lower pre-mkt. The US has been the anchor for global growth, but a China reboot will also benefit the globe though may create another inflation pressure, so keep an eye on cmdtys and bond yields over the coming weeks. Higher yields are not a headwind to stocks but when yields set new highs (e.g., 10Y > 5%) that is when US Equities are disrupted.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, the US session was relatively quiet despite the continuation of the global-risk on tone. Most major EU indices finished higher despite weaker than expected PMIs while the US saw a continuation of recent macro data trends, Services strong and Manufacturing weak. More color on Flash PMIs is below alongside dovish Fedspeak that indicates a still strong economy and a potentially less aggressive cutting cycle than is currently priced into bond markets, which is pricing an additional ~200bps of easing through end of October 2025. Today’s macro data focus is on Consumer Confidence, given its potential to continue to push spending and thus GDP above trend. However, do not discount the housing data as XHB has outperformed SPX over the last three months, +19.9% to 4.7%, but only 3.5% to 1.5% over the last month. As investors look to a broadening of the rally into year-end, it feel that many will target quality names within Cyclicals/Value.

BY Doug Kass · Sep 24, 2024, 6:08 AM EDT

* Added to SPY short at $571.12

* Added to QQQ short at $484.99

BY Doug Kass · Sep 24, 2024, 6:00 AM EDT