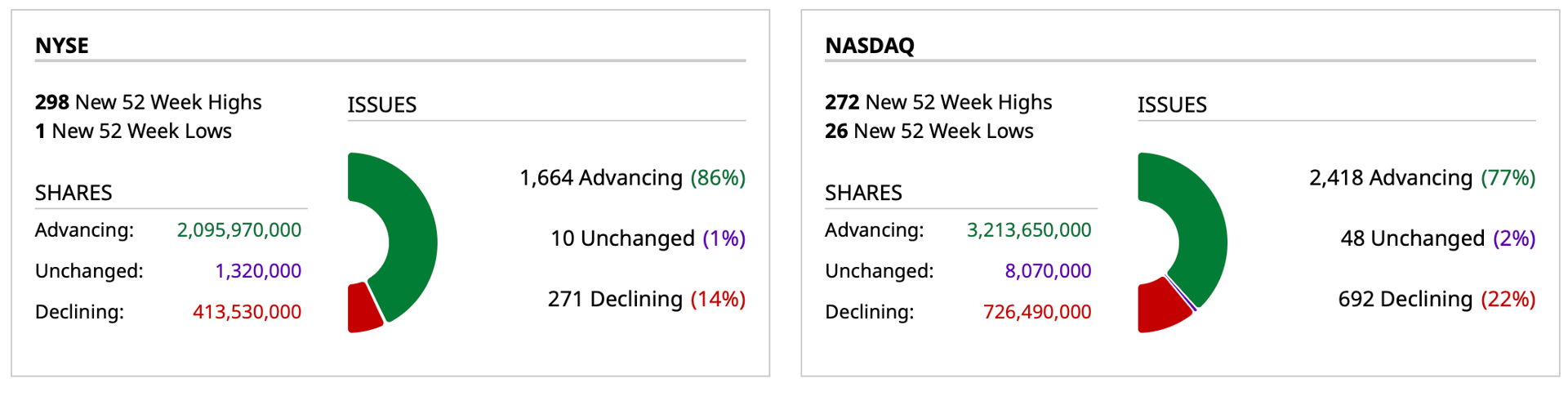

Closing Market Internals

Closing Volume

- NYSE volume 416M shares, 10% above its one-month average;

- NASDAQ volume 4.76B shares, 7% above its one-month average

Breadth

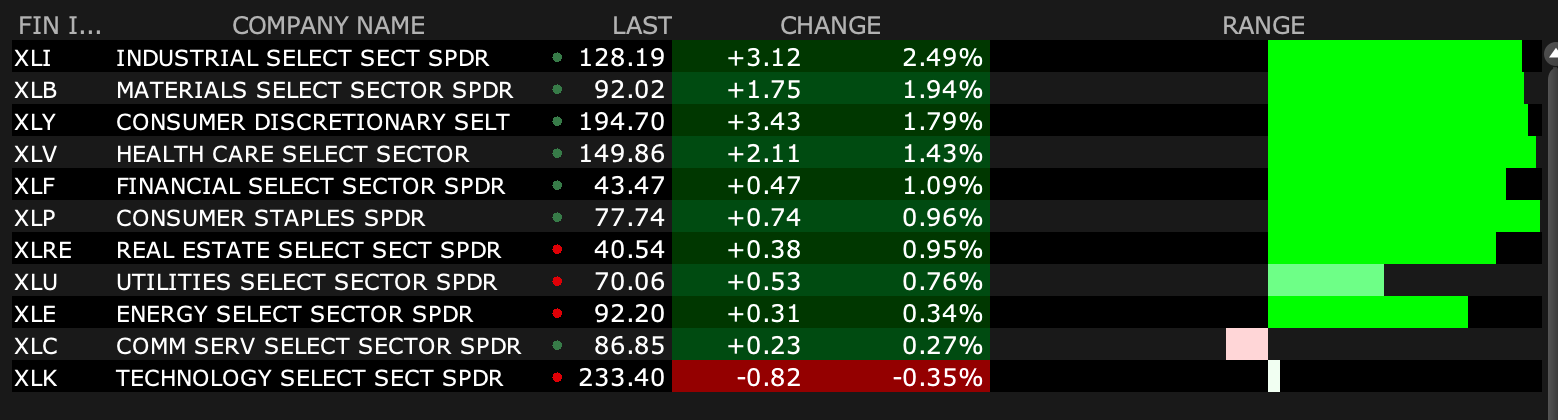

S&P 500 Sector ETFs

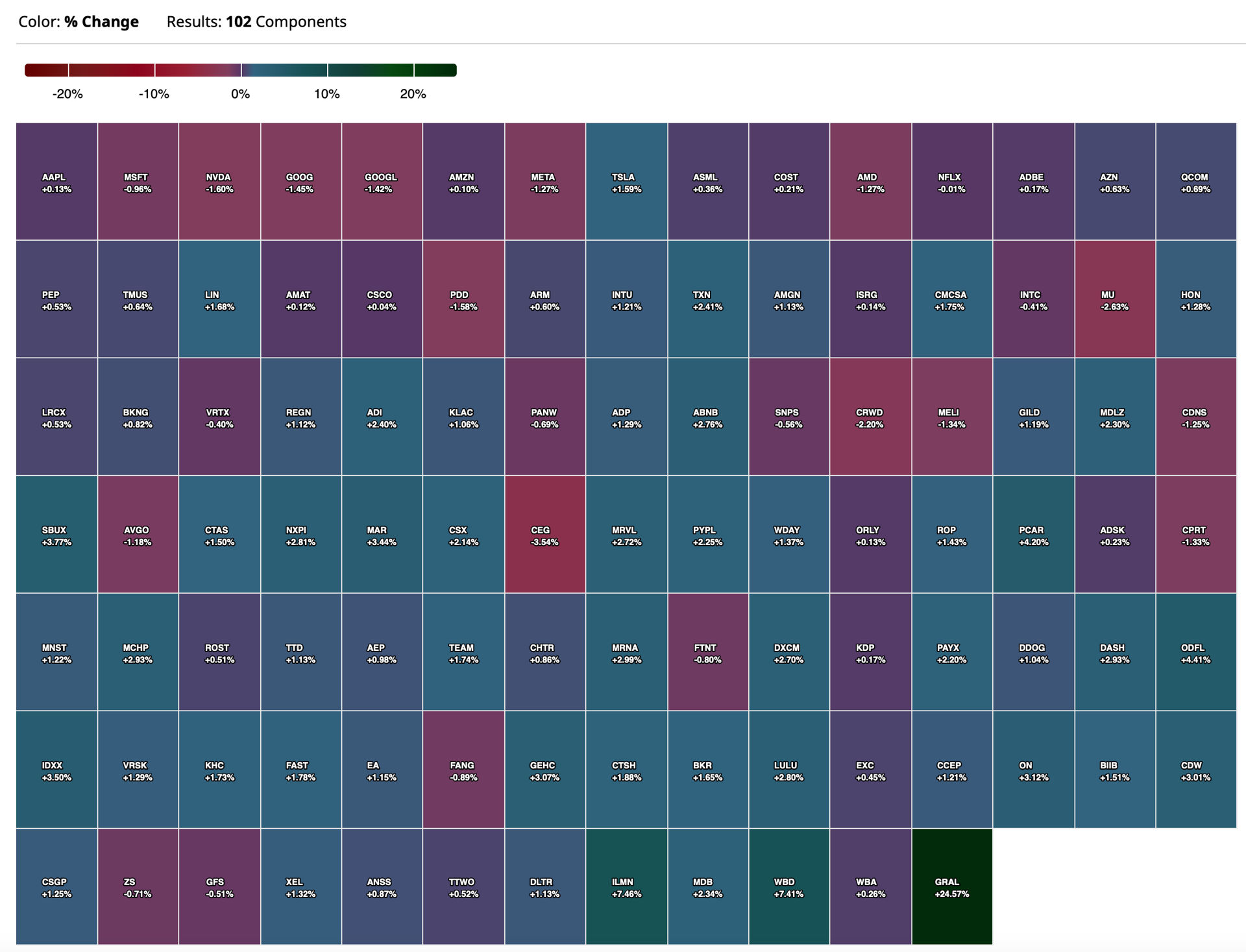

Nasdaq 100 Heat Map

BY Doug Kass · Jul 16, 2024, 4:41 PM EDT

- NYSE volume 416M shares, 10% above its one-month average;

- NASDAQ volume 4.76B shares, 7% above its one-month average

BY Doug Kass · Jul 16, 2024, 4:41 PM EDT

Thanks for reading my Diary today.

I have to prepare for three meetings with management tomorrow afternoon so I am calling it a day.

Enjoy the evening.

Be safe.

BY Doug Kass · Jul 16, 2024, 4:05 PM EDT

I have a research call between 3-3:45 p.m.

Radio silence during that timeframe.

BY Doug Kass · Jul 16, 2024, 2:58 PM EDT

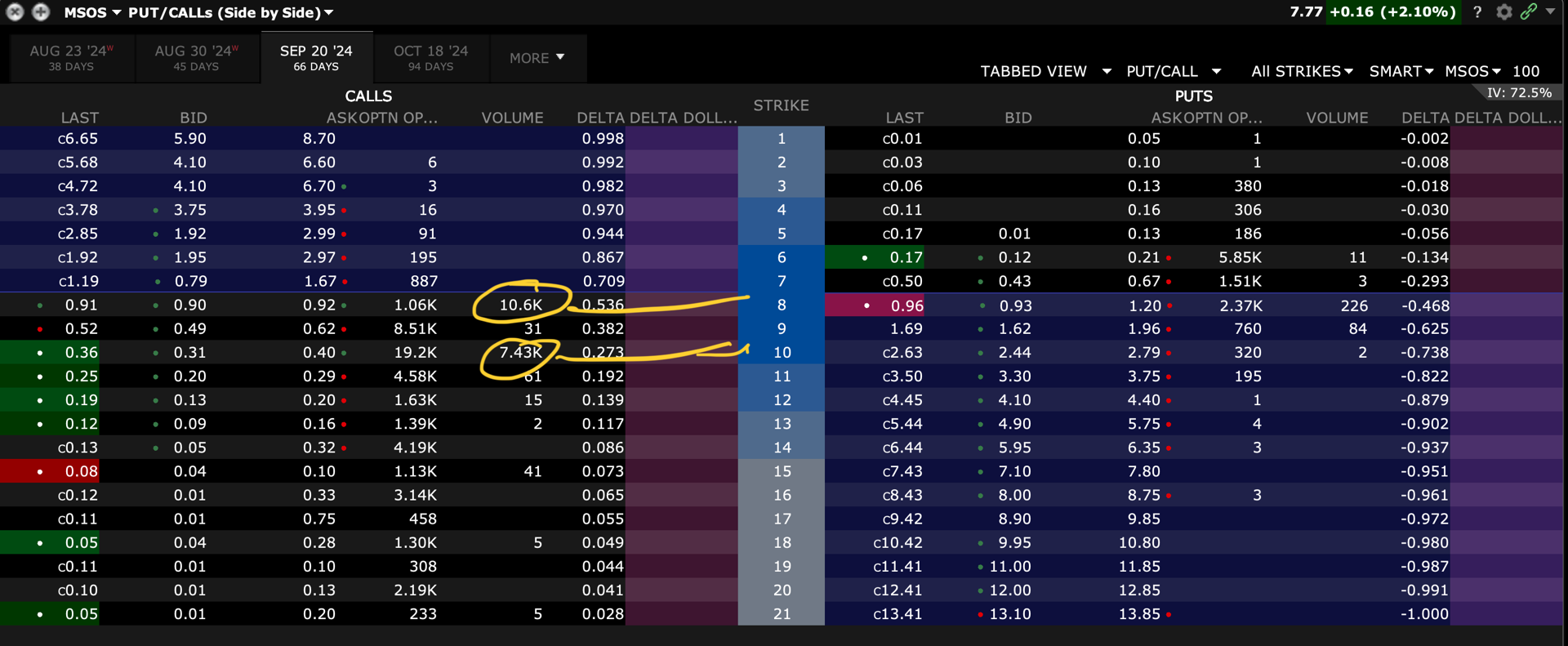

Large volume in September MSOS calls today.

BY Doug Kass · Jul 16, 2024, 2:04 PM EDT

I have been accumulating a new cannabis long — Glass House Brands GLASF.

BY Doug Kass · Jul 16, 2024, 1:41 PM EDT

Jeff Bezos has now sold 35% (8.6 million) of the 25 million Amazon AMZN shares he filed to sell a while ago.

Now that we have spent two days under $200 it will be interesting to see if he is still a seller.

BY Doug Kass · Jul 16, 2024, 12:43 PM EDT

From Peter Boockvar:

Upside surprise in retail sales/Import prices do too

Core retail sales saw a big upside surprise in June with a .9% m/o/m gain vs the forecast of up .2%. That comes after a .4% rise in May that was left unrevised. They are higher by 4.1% y/o/y. Auto sales though fell 2% m/o/m and are down 4.8% y/o/y. Building materials rebounded by 1.4% after a .7% drop in May and are still down 5.6% y/o/y. Both categories we know are very interest rate sensitive. Because of lower gas prices, the sales at gasoline stations fell 3% m/o/m and by 2.1% y/o/y.

Elsewhere, sales of furniture, electronics, and clothing all rose as they did at department stores, online retailers (particularly strong with a 1.9% m/o/m and 4.8% y/o/y gain) and restaurant/bars. Sporting goods sales were little changed from the prior month but down 5.2% y/o/y. Sales for health/personal care products were up .9% m/o/m but little changed for food/beverages.

Bottom line, I’ve gone through countless consumer touching earnings conference calls over the past few months, and provided you with all that I found important, and the only portion of consumer spend that is doing well comes from the higher end. The lower to middle income consumer is stretched, extremely value conscious and focused on needs and not wants. I’m thus not reading today’s data as evidence of a strong consumer. We have some spending freely and many not.

On the upside, Treasury yields rose in response but are still down on the day.

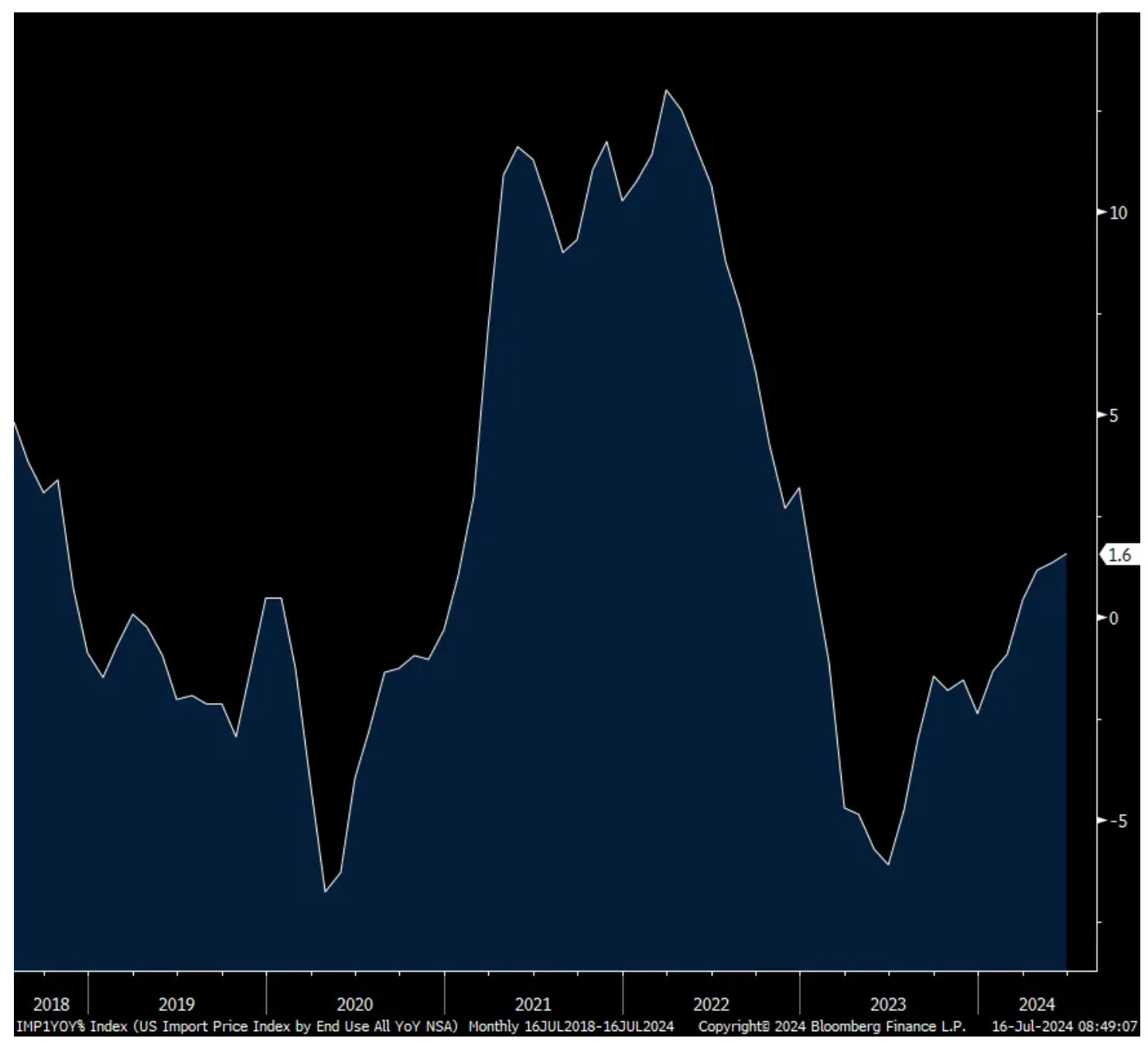

Also possibly lifting yields off their early morning lows was the higher than expected import price data for June. Headline prices were flat m/o/m, two tenths more than estimated and May was revised up by 2 tenths. They are up 1.6% y/o/y. Ex petro, import prices rose .2% m/o/m instead of falling by 2 tenths as expected. They are up 1% y/o/y. Ex food and energy prices were unchanged m/o/m and higher by just .6% y/o/y.

Bottom line, notwithstanding the upside surprise, import prices remain muted but have bottomed.

Import Prices y/o/y

BY Doug Kass · Jul 16, 2024, 11:42 AM EDT

BY Doug Kass · Jul 16, 2024, 11:07 AM EDT

With S&P cash back +20 handles I am adding another tranche of short Index calls.

BY Doug Kass · Jul 16, 2024, 10:59 AM EDT

My trade of the week is to short the QQQ at $496.85.

Rationale:

* Overall markets are overbought.

* Rotation out of tech and into Trump plays (infrastructure, healthcare, energy) is possible, given the former President's large lead in the polls.

* How much more can the Mag7 be pumped (considering the outperformance over the last year?

* Accelerated insider selling in Mag7 (see Bezos/Amazon AMZN etc.)

There is more but I wanted to get this out post haste...

BY Doug Kass · Jul 16, 2024, 10:09 AM EDT

Housekeeping items: I covered my other 60 Minute Trade, Bank of America BAC at $42.43. This was for a small profit.

BY Doug Kass · Jul 16, 2024, 9:50 AM EDT

From Peter Boockvar:

A few things

We are now wondering whether the Fed surprises us in a few weeks with a rate cut instead of waiting until September where the odds are 100% as priced by the fed funds futures and actually an additional 12% chance of 50 bps of cuts by then. Mary Daly, a voting member, though doesn't seem ready just yet for a July move. Speaking yesterday she said that while "confidence is growing that we're getting nearer to a sustainable path of getting inflation back down to 2%,...we have a lot more information to get before we can make any real determination." The next two weeks won't reveal 'a lot more information.'

Following another negative print in the July NY manufacturing survey seen yesterday, Cass Freight's June index saw a 1.8% m/o/m drop to a four year low in shipments in June and were down 6% y/o/y. They said "Amid slowing economic growth, goods demand is still broadly flattish." Combine sluggish volumes with still excess trucking capacity and the Cass Inferred Freight Rate dropped by 1.4% m/o/m in June, "giving up part of the 3.9% jump in May to a six month high."

We'll hear from JB Hunt tonight with earnings as it seems that the freight recession continues on but with hopes in the industry that we're more bouncing along the bottom rather than seeing it getting any worse. The issue too in the trucking industry is still too much capacity but that is slowing draining as firms close and/or merge.

PNC reported earnings and the problem in commercial real estate continues on as "Net loan charge-offs of $262 million increased $19 million, primarily due to higher commercial real estate net loan charge-offs."

And, "Total nonperforming loans of $2.5 billion increased $123 million, or 5%, primarily due to higher commercial nonperforming loans."

Average loans were steady q/o/q but fell y/o/y "driven by lower utilization of loan commitments."

From Bank America's earnings release:

"Net interest income decreased 3%...as higher deposit costs more than offset higher asset yields and modest loan growth."

On credit, provision for credit losses rose to $1.5b, up from $1.3b in Q1 and $1.1b in Q2 '23. Net charge-offs of $1.5b was flattish q/o/q but up from $869m in Q2 '23.

With loans, "Average loans and leases of $373b decreased $10b or 3%, reflecting lower client demand."

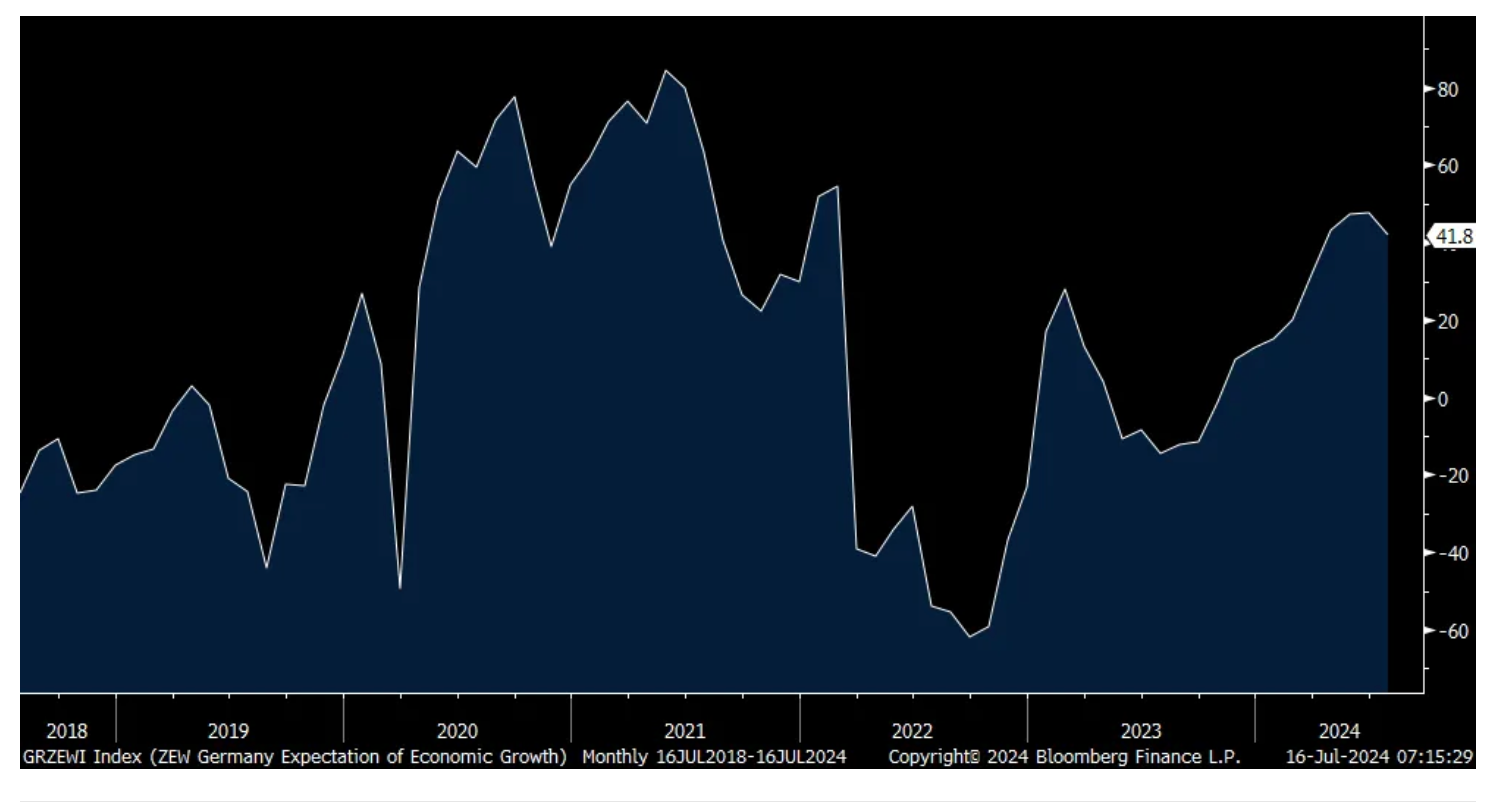

The only data point of note overseas was the July German ZEW investor expectations index on the German economy but it's never market moving. It fell to 41.8 from 47.5 but that was a bit better than the feared drop to 41. The Current Situation was less negative at -68.9 but the Expectations component softened to 43.7 from 51.3. The ZEW said "The economic outlook is worsening. For the first time in a year, economic expectations for Germany are falling. The fact that German exports decreased more than expected in May, the political uncertainty in France and the lack of clarity regarding the future monetary policy by the ECB have contributed to this development."

Bund yields are lower by about 4 bps and the euro is hovering around the highest level since mid March against the US dollar. The DAX is down for a 2nd day.

ZEW

BY Doug Kass · Jul 16, 2024, 9:30 AM EDT

Here are the premarket stock movers, percentage-wise, as of 8:36 a.m.:

BY Doug Kass · Jul 16, 2024, 9:20 AM EDT

Here are the U.S. select premarket movers as of 8:28 a.m. ET

-SILO +117% (secures Exclusive Global License for SPC-14, Alzheimer's Therapeutic)

-PAPL +24% (earnings)

-MGRX +18% (secures DEA Approval for Proprietary HIPAA-Compliant Operating System via Surescripts)

-ANGO +9.6% (earnings, guidance)

-ETON +8.4% (US FDA accepts ET-400 (Hydrocortisone Oral Solution) NDA)

-CHGG +8.2% (Morgan Stanley Raised CHGG to Equal Weight from Underweight, price target: $3.25)

-KYTX +7.5% (KYV-101 receives US FDA RMAT Designation for KYV-101 for Treatment of Patients With Refractory Stiff-Person Syndrome)

-MTCH +7.4% (Activist holder Starboard acquires >6.5% stake; Starboard to push for sale if Match doesn’t make changes)

-LSTA +7.2% (completes enrollment in Phase 2a BOLSTER Trial of Certepetide in First-Line Cholangiocarcinoma)

-UMAC +6.9% (launches NDAA Compliant, Made in the USA Flight Controller for FPV Drones)

-EGHT +6.0% (secures $200M term loan at reduced rates in debt swap paydown)

-IREN +4.4% (appoints Morgan Stanley as Financial Advisor in connection with evaluating monetization opportunities in the AI data center market)

-SHOP +4.2% (Tier1 firm Raised SHOP to Buy from Neutral, price target: $82 from $78)

-ANVS +2.8% (receives FDA Approval to Transition to New Crystal Form of Buntanetap)

-DDOG +2.5% (Mizuho Securities Raised DDOG to Buy from Neutral, price target: $155)

-STT +2.5% (earnings)

-BAC +2.1% (earnings, guidance)

-LXRX +1.9% (receives December 20, 2024 PDUFA Goal Date for Sotagliflozin Type 1 Diabetes NDA Resubmission)

-CFB -9.0% (earnings, guidance)

-DJT -9.0% (Holders file to sell 37.9M shares)

-SCHW -4.1% (earnings)

-MS -2.5% (earnings)

BY Doug Kass · Jul 16, 2024, 9:10 AM EDT

From Jefferies:

BAC First Look

Focus on this new slide – which gets us to ~$14.5B 4Q exit rate NII - inclusive of 3 cuts

With that --- funding is a bit mixed; A) DDAs down $24B (-1% mix shift), B) IBD cost actually increased QoQ - from +11 to +13 bps, 3) GWIM Deposit cost jumped +25 bps QoQ

10k foot level – I don’t think anything really changes here: we know the story and we are getting some incremental detail. Bulls are long for this NIM upside (4Q25e 2.02%..) – with more debate (upside delta) around BS size than anything

That said – feedback is fine. Nothing in here that is incrementally super exciting

…..to the extent any of this may be DOL related ---- OR --- is the wealth trend (client cash trend) just tough right now regardless of DOL (answer = YES, see below)

SCHW FIRST LOOK

NII miss on

-6.5B June cash decline (-$5B sweep decline)

Exacerbated by EOP FHLB higher QoQ ($24.4B vs est $~$21B avg)

Exacerbated by EOP CDs higher MoM ($40.3B vs 36.4B)

Focus turns to out-quarter #s and balance sheet stabilization levels (presumed lower, again)

Consensus has year-end FHLB below $10B…..

Nobody had a CD increase on the radar

And this seasonal bounce in sweep cash doesn’t seem to be happening

So where does that 4Q $.90 eps exit rate fall to?

And then what’s the level that this attrition finally halts – not clear

NNA growth only $29B or +3.8% vs cons 3Q/4Q over $35B/monthly avg...

DOL? - Bank deposit rate declined 4 bps - no signs of any DOL pressures here

MS FIRST LOOK

NII miss (-30M) down ~$55M QoQ on

-$10B sweep deposit outflows

-2.5% decline in sweep/Total Deposits mix

*MS EOP deposit rate 3.11% vs avg 3.03% and 1Q EOP 2.96% ----- for all you DOL hawks out there

NNA growth 2.6%

Buyback $750M

Silver Lining? - Cap Mkts solid across Trading and IB - and WM PT margin did come thru at 27%

BY Doug Kass · Jul 16, 2024, 8:53 AM EDT

I covered my MS short at $102.75 - made four beaners, real quick.

Still short BAC.

BY Doug Kass · Jul 16, 2024, 8:15 AM EDT

Both on good profit reports (that may already have been discounted):

* Shorted BAC $42.94

* Sold balance of long and shorted MS $107.41 ("double sale")

BY Doug Kass · Jul 16, 2024, 7:41 AM EDT

Everyone is looking to bottom fish in Starbucks SBUX.

Evercore/ISI lowers the price target of Starbucks to $80.

BY Doug Kass · Jul 16, 2024, 7:36 AM EDT

Discussing J.D. Vance's position on cannabis policy.

BY Doug Kass · Jul 16, 2024, 6:55 AM EDT

Product prices and wage increases rarely retreat...

BY Doug Kass · Jul 16, 2024, 6:40 AM EDT

"Man can succeed at almost anything for which he has unlimited enthusiasm."

- Charles Schwab

Bonus — Here are some great links:

BY Doug Kass · Jul 16, 2024, 6:30 AM EDT

BY Doug Kass · Jul 16, 2024, 6:11 AM EDT

BY Doug Kass · Jul 16, 2024, 5:45 AM EDT