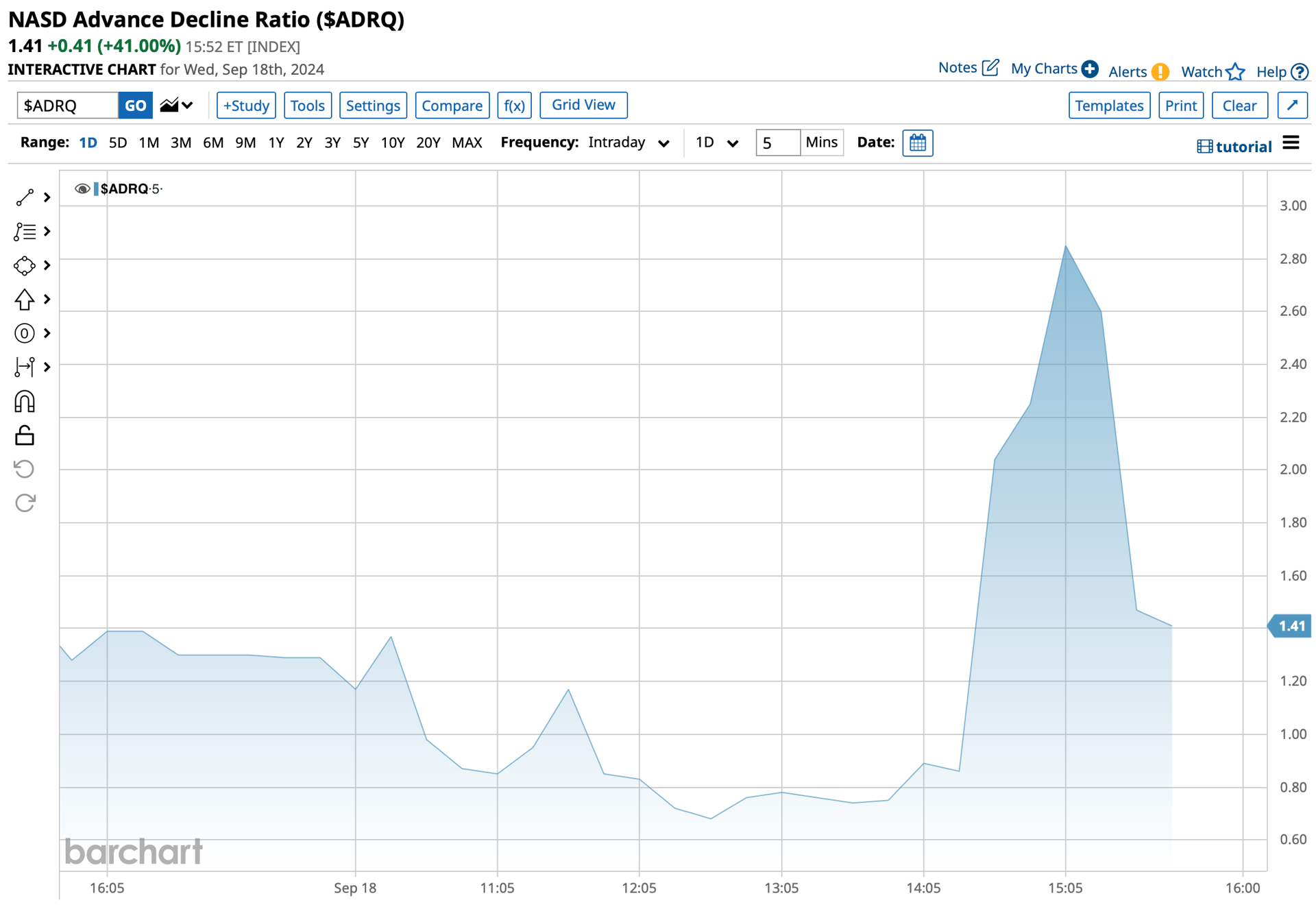

A Dose of Reality

Let's end the day with

.

BY Doug Kass · Sep 18, 2024, 5:00 PM EDT

Let's end the day with

BY Doug Kass · Sep 18, 2024, 5:00 PM EDT

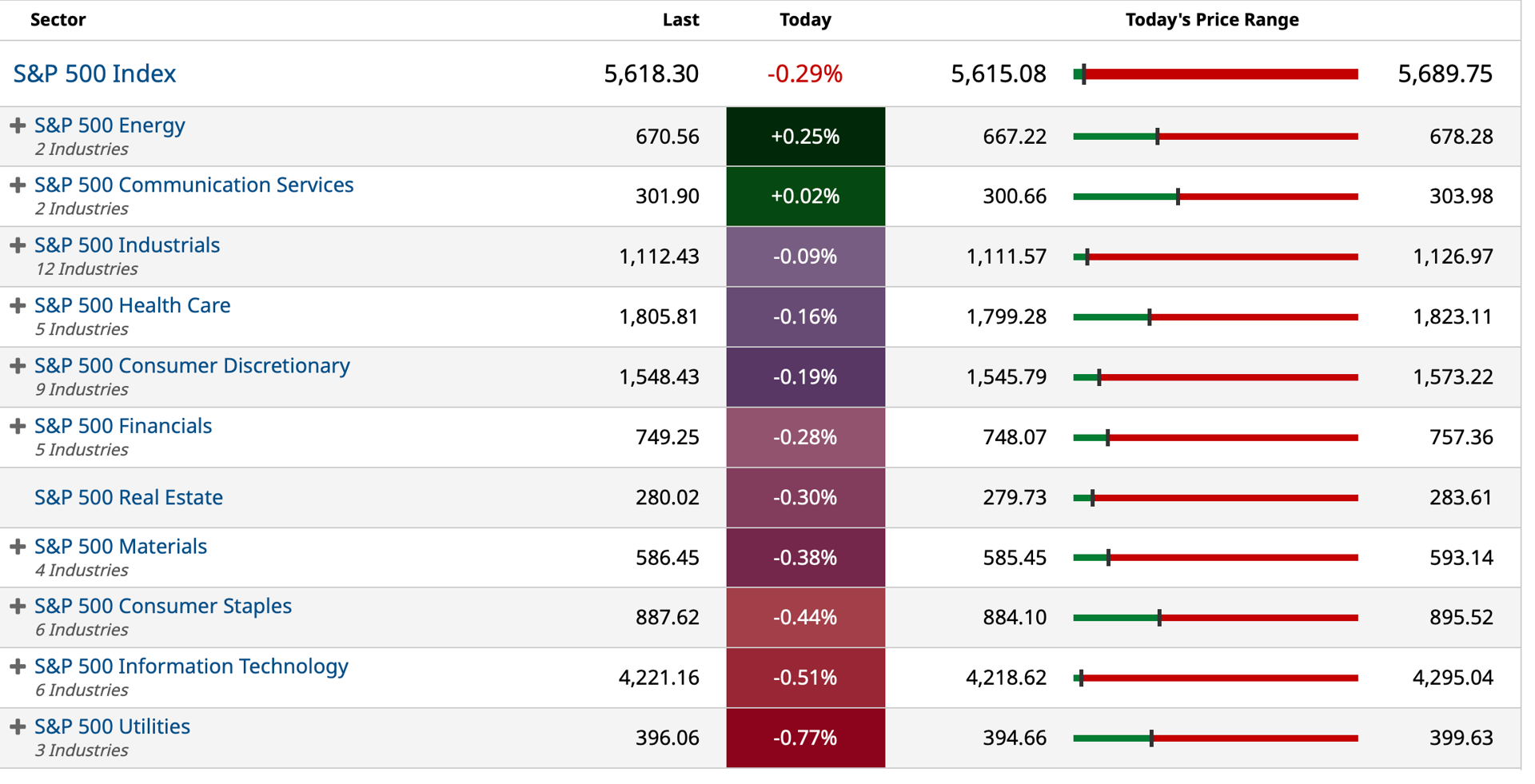

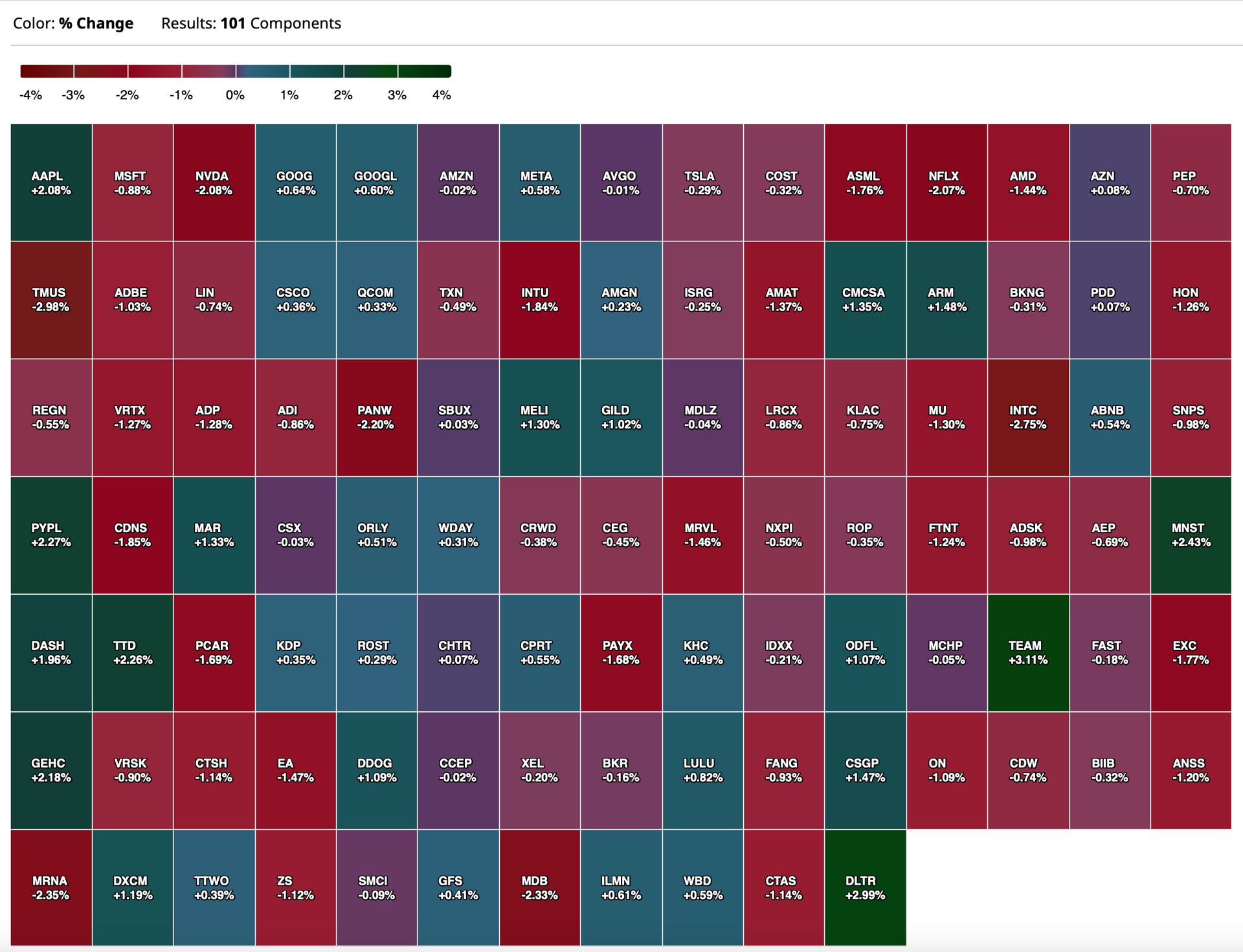

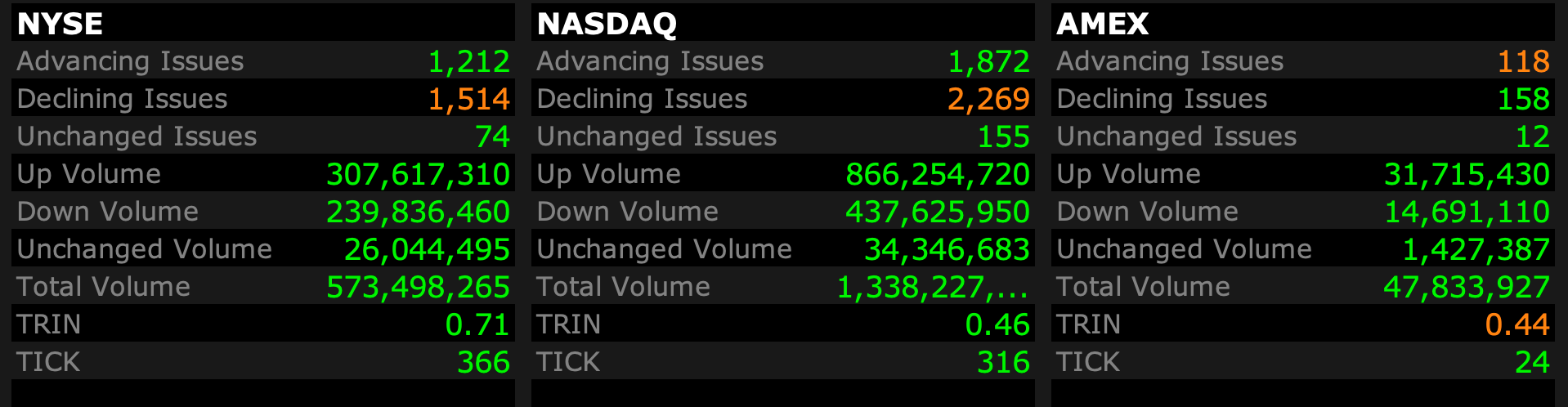

As of 4:17 p.m.:

BY Doug Kass · Sep 18, 2024, 4:50 PM EDT

BY Doug Kass · Sep 18, 2024, 4:40 PM EDT

Wolf Street howls about the Fed's cut.

BY Doug Kass · Sep 18, 2024, 3:51 PM EDT

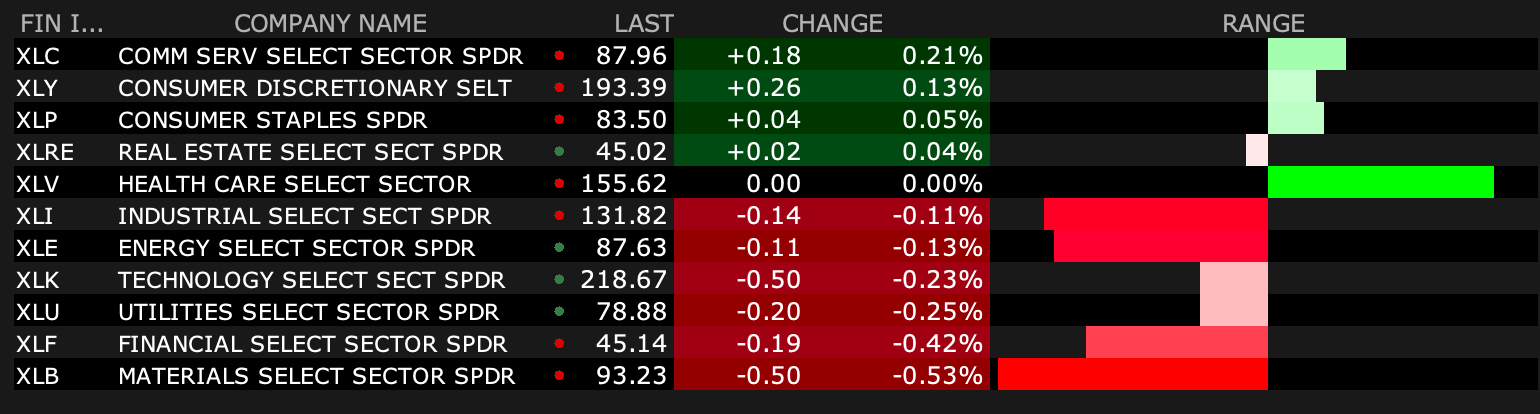

Since "Things" I have added to my Index shorts on the rally (which is now petering out)...

I also added to my XLU short

BY Doug Kass · Sep 18, 2024, 3:41 PM EDT

* Not surprisingly, I had an active day trading.

* Net/net I sold on the day.

I was active today (trading aggressively and opportunistically) — net/net I did a lot more shorting than buying.

Warning: Its 3:05 p.m. and I might not be done with the trading day!

* I traded SPY/QQQ common 4x today — buying weakness and selling strength (all profitably).

* I added to OXY common and calls... again.

* I added to private equity and homebuilding shorts, twice during the day.

* I added to MSOS at $6.83.

* I added to individual cannabis equities all day. (GTBIF, VRNOF, TSNDF and CURLF).

* I added to SLB at $41.22 and sold (moving to small sized) at around $41.70.

* I eliminated OIH at $286 — taking more than $15/share in a few days.

BY Doug Kass · Sep 18, 2024, 3:16 PM EDT

I just sold my OIH long at $286 — taking out +$15 share in a few days. Will revisit on weakness.

I reduced SLB to small at $41.66.

BY Doug Kass · Sep 18, 2024, 2:56 PM EDT

I re-shorted the Indices:

*SPY $566.84

* QQQ $477.77

BY Doug Kass · Sep 18, 2024, 2:42 PM EDT

I covered today's Index shorts just now on the whoosh lower - for a quick profit.

SPY $563.56, QQQ $474.29

BY Doug Kass · Sep 18, 2024, 2:20 PM EDT

With S&P cash +30 handles I am shorting more individual names.

BY Doug Kass · Sep 18, 2024, 2:12 PM EDT

Shorted SPY $567.98 and QQQ $478.63.

BY Doug Kass · Sep 18, 2024, 2:04 PM EDT

BY Doug Kass · Sep 18, 2024, 1:41 PM EDT

GTBIF is my largest individual cannabis equity position.

From Randorama:

Barstool Sports Expands Into Cannabis Industry, Partners With Green Thumb Industries GTBIF

BY Doug Kass · Sep 18, 2024, 1:32 PM EDT

I added to Schlumberger SLB at $41.22 this morning.

BY Doug Kass · Sep 18, 2024, 1:10 PM EDT

Coming up shortly — Danny, Guy, Carler, LY (from SoFi) at 1 p.m. on MRKT CALL.

It's the best damn daily interview in the business... and it's free!

To borrow from Warner Wolf, "Let's go to the video tape."

BY Doug Kass · Sep 18, 2024, 12:58 PM EDT

I added to MSOS $6.83, CURLF $2.91, VRNOF $3.15, GTBIF $10.38 and TSNDF $1.16 today.

BY Doug Kass · Sep 18, 2024, 12:50 PM EDT

Microsoft MSFT just traded down -$4.5 to $340.45.

The shares traded at about $352 after this buyback and dividend announcement a few trading sessions ago:

BY Doug Kass · Sep 18, 2024, 12:31 PM EDT

XLU is down for the first day since my Bar Mitzvah.

BY Doug Kass · Sep 18, 2024, 12:00 PM EDT

Brilliant in its precision and succinctness:

skeptcl

6 minutes ago

I see a little silhouetto of a man Scaramouche, Scaramouche, will you do the Fandango? JUST IN: Hedge fund manager Anthony Scaramucci says #Bitcoin could hit $100,000 by the end of the year..

BY Doug Kass · Sep 18, 2024, 11:45 AM EDT

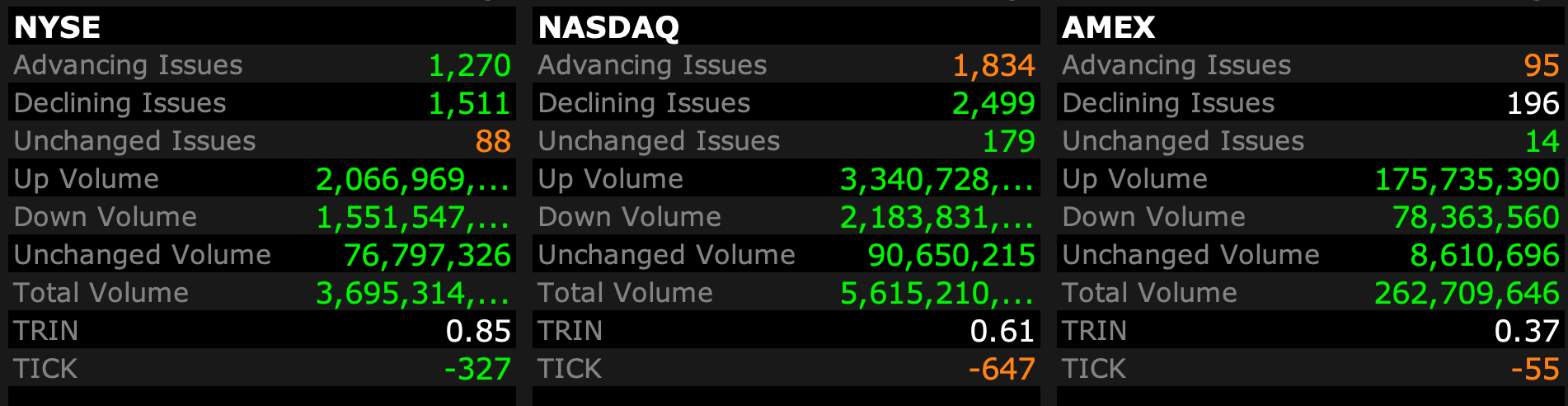

- New York Stock Exchange volume 19% below its one-month average;

- Nasdaq volume 19% below its one-month average

- VIX up 6.81% to 18.81

BY Doug Kass · Sep 18, 2024, 11:30 AM EDT

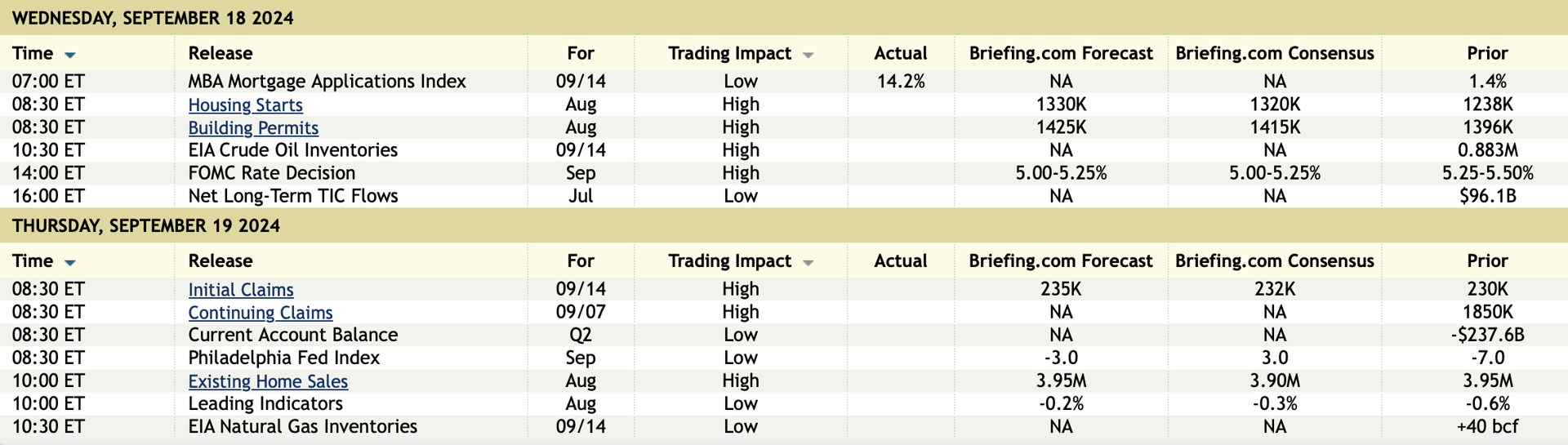

From Peter Boockvar:

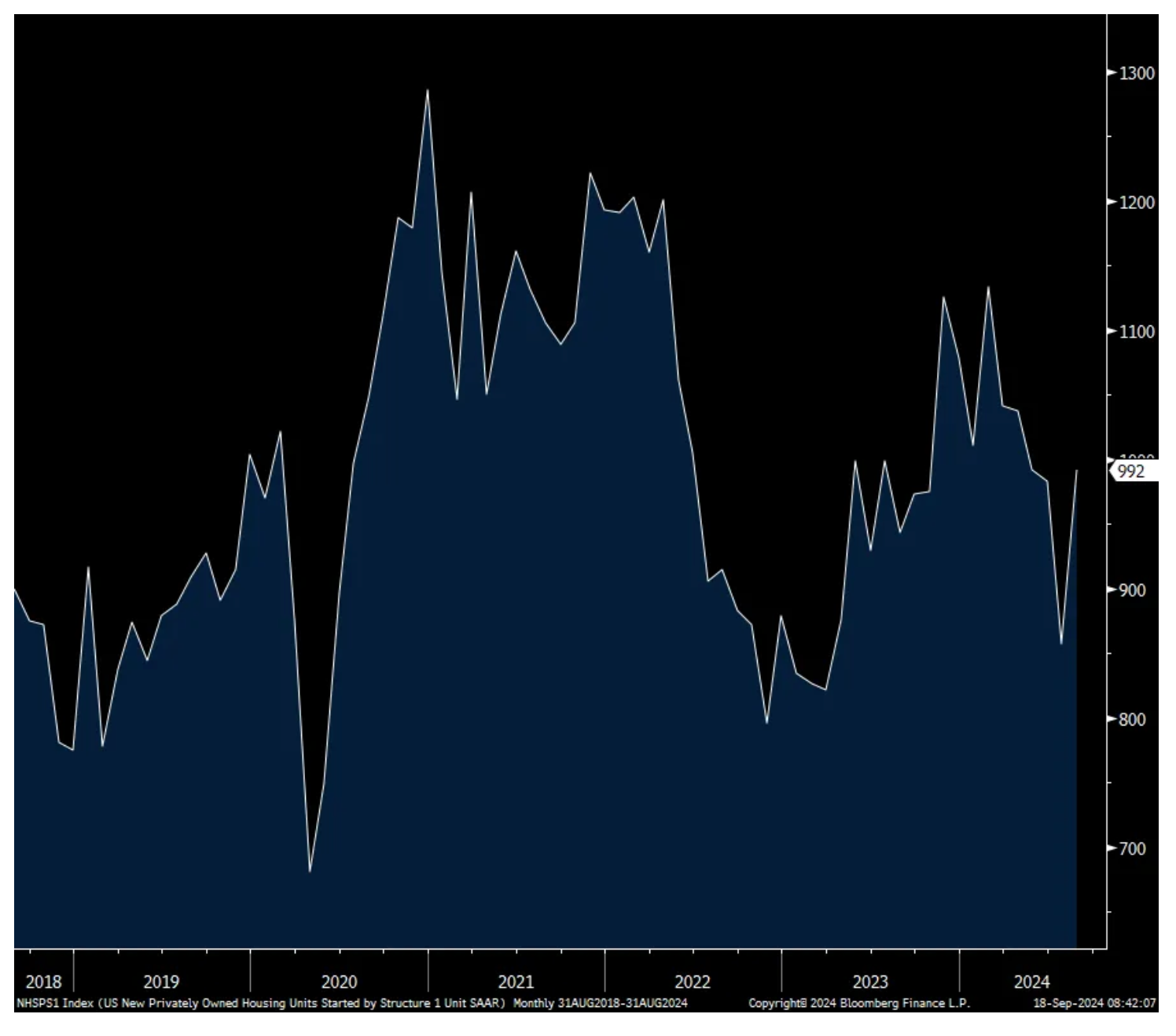

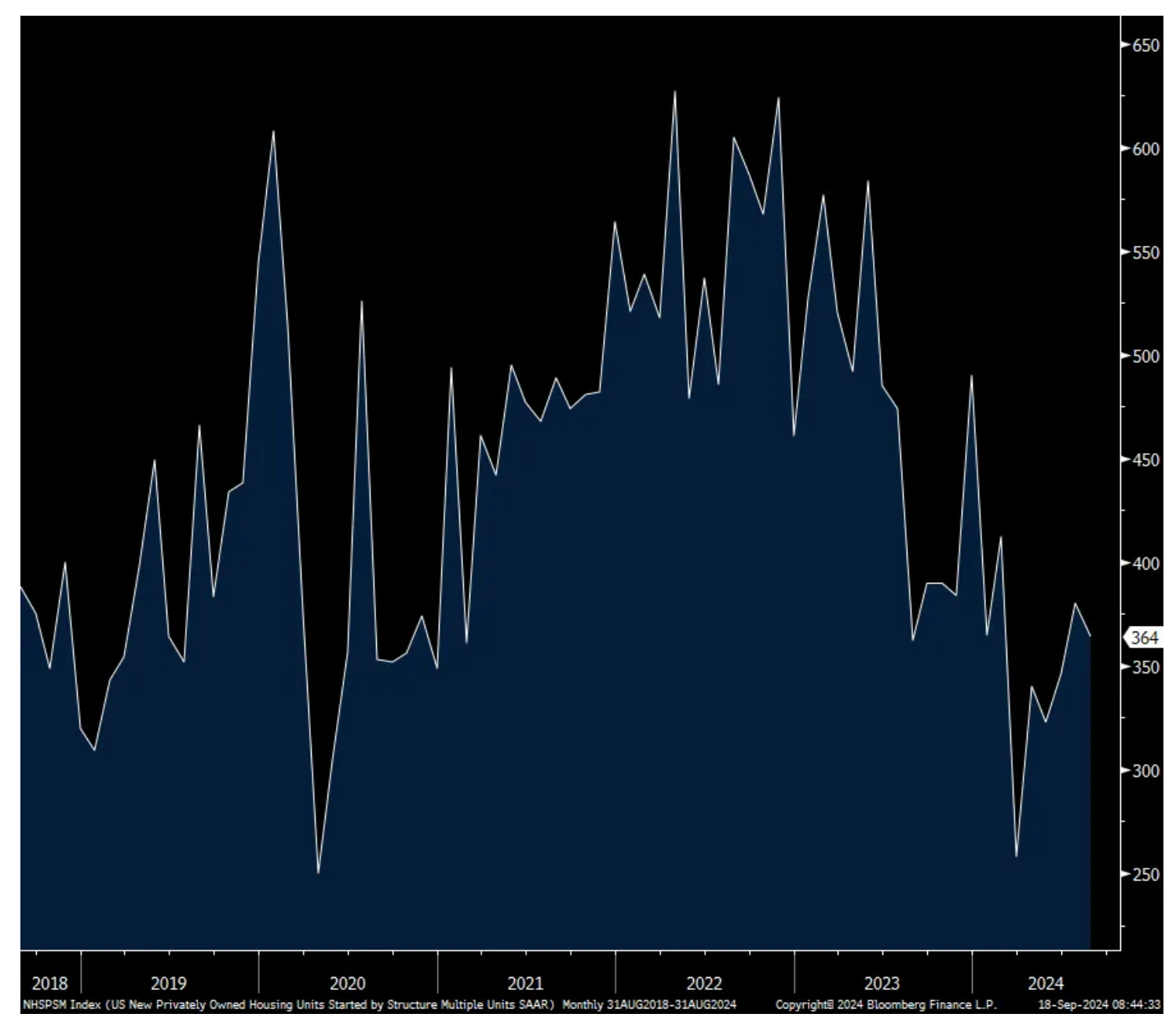

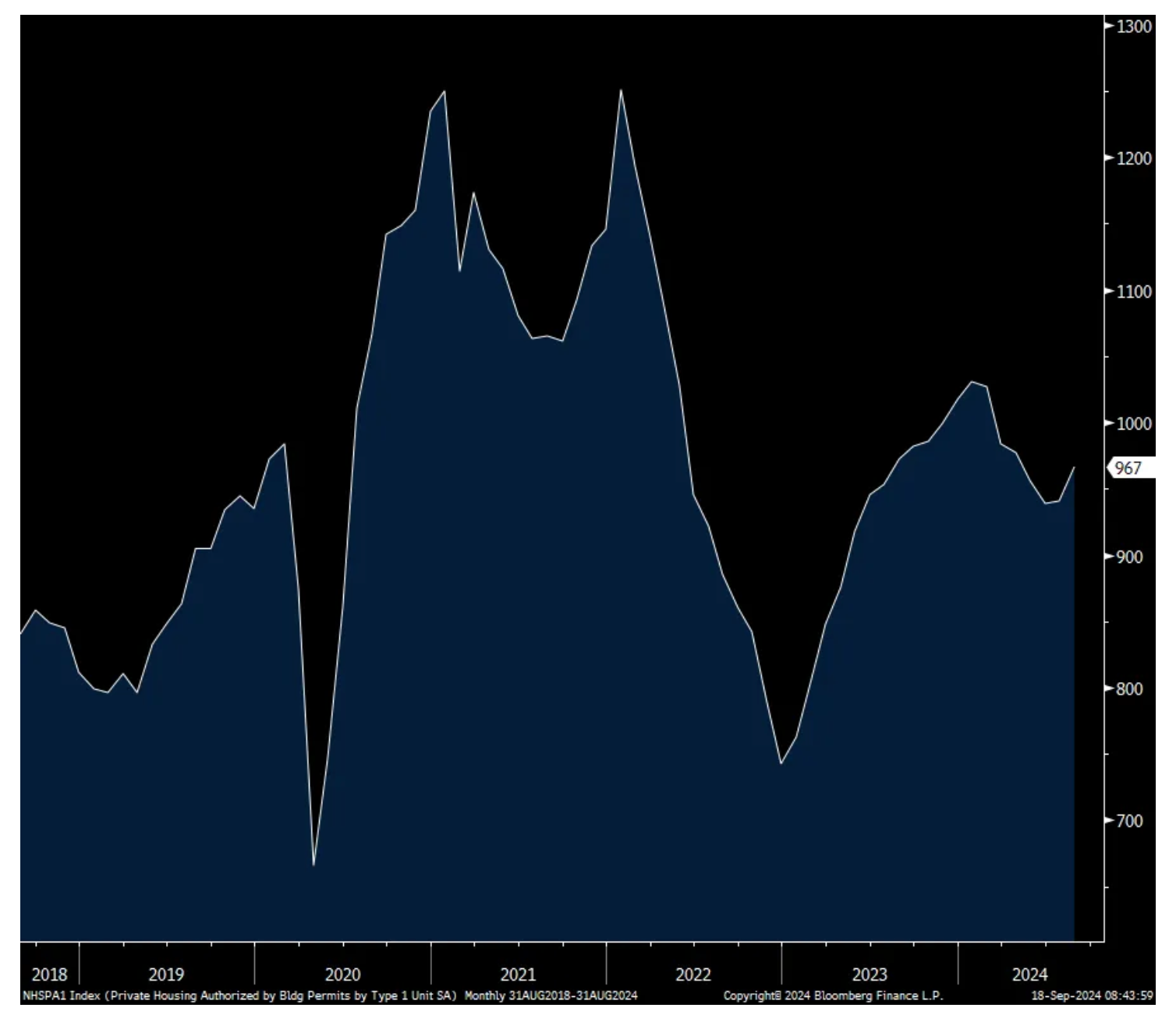

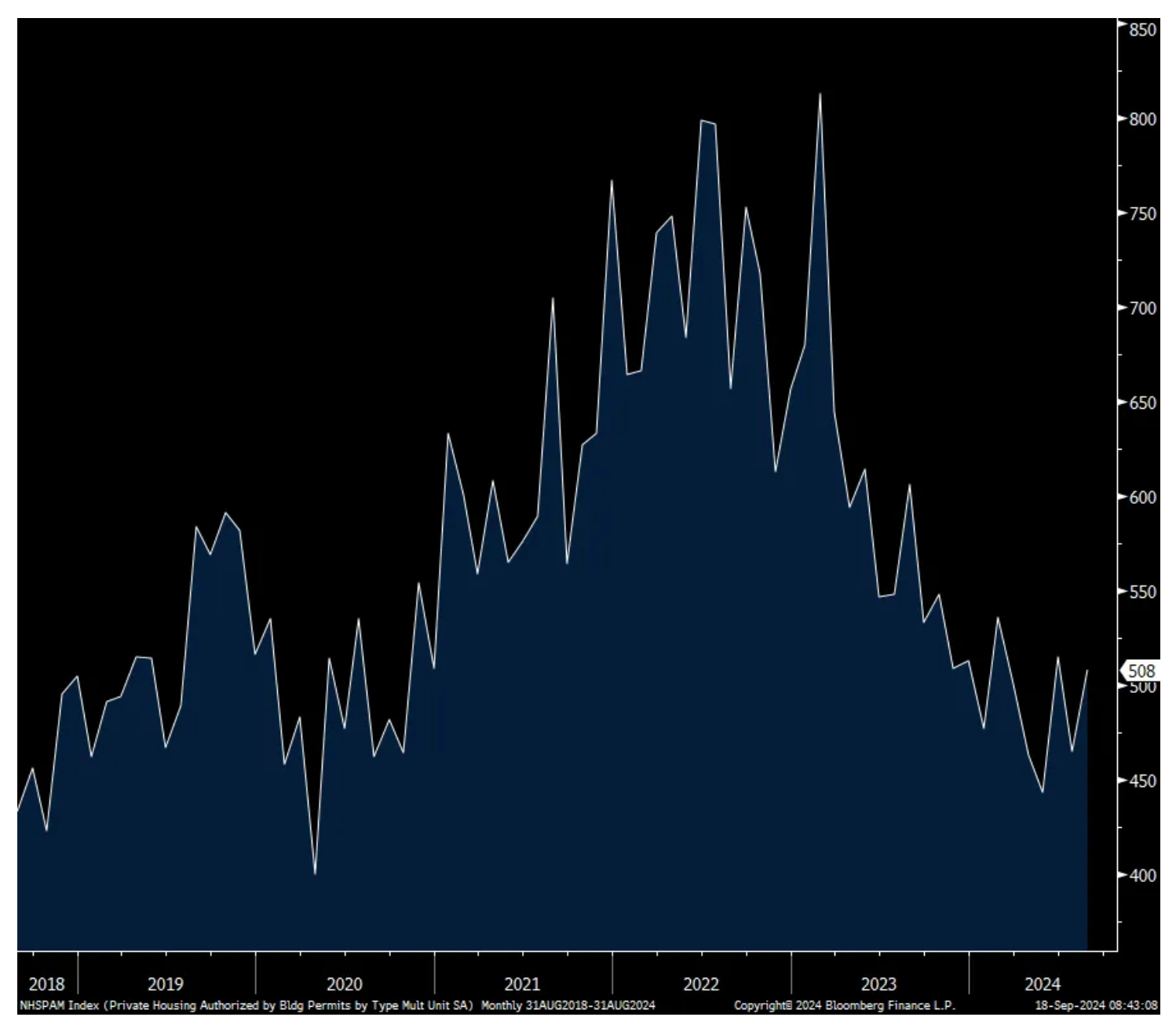

Housing starts in August totaled 1.356mm, 38k above the estimate vs 1.237mm in July and 1.329mm in June. Single family was the main swing factor over the past few months. In June they were 983k, fell to 857k in July and came in at 992k in August, the same figure seen in May. It was over 1mm in the first 4 months of the year. Hurricane Beryl was the likely factor in July, as they fell notably in the South. Multi family starts were 364k vs 380k in July and 346k in June and is well off the highs in the 600k range in 2022 as easy money and rising home prices then encouraged the construction of apartment buildings. Now, it doesn’t pencil out to the same extent.

Permits, the precursor to an eventual start, rose to a 5 month high with gains for both single and multi family, but both too well off their highs.

Bottom line, with regards to single family we have big builders that are both taking market share from smaller ones and have the ability to discount their product in order to drive sales. Multi family is absorbing a big increase in supply this year but we expect a notable drop off in supply starting in the back half of 2025 and into 2026. We’ll of course see in the coming months/quarters to what extent lower rates, though the 10 yr yield is just back to where it was last summer, has an impact.

Single Family Starts

Multi Family Starts

Single Family Permits

Multi Family Permits

BY Doug Kass · Sep 18, 2024, 11:00 AM EDT

Adding to shorts in private equity and home builders.

BY Doug Kass · Sep 18, 2024, 10:44 AM EDT

Buying more OXY (shares are modestly lower, by two bits!) calls.

BY Doug Kass · Sep 18, 2024, 10:39 AM EDT

The strongest sector this morning is energy - despite the price of crude oil being lower (now -$0.40 after being -$1.20 very early in the morning)

BY Doug Kass · Sep 18, 2024, 10:37 AM EDT

From Peter Boockvar:

To paraphrase what I said on Monday, there is high potential for market whiplash today. We'll get the initial reaction at 2pm and then see how Powell sells it at 2:30pm which I believe will offset the market impact of the cut size. If he cuts 25 bps, he'll tell us that 50 bps is possible in the coming meetings. If he cuts by 50 bps, he'll tell us not to get used to that cadence. Either way, this is all market noise as we've already priced in so many cuts through next year.

Understand that there is a huge differential between what we saw in the June dots and what the fed funds futures market is currently pricing in. That market is pricing in about a 2.90% fed funds rate by October 2025, while the Fed's median dot for year end 2025 is much higher at 4.1%, with a 3.1% rate by year end 2026. Thus, AGAIN, today's 25 or 50 bps is an irrelevant action compared to the notable cuts ALREADY priced in.

On Monday I mentioned that my chips were on 50 bps today but I'm moving it back to 25 bps but followed with talk that 50 bps is on the table for the coming meetings. The market impact will remain the same.

As for those dots, they are irrelevant too as Powell gets what Powell wants and he'll corral the voting members around to that. Thus, his dot is the only one that matters and unfortunately he doesn't put his name on it.

With the continued drop in mortgage rates, refi's jumped by 24% w/o/w and purchases finally responded, rising by 5.4% w/o/w and are back to flattish y/o/y. Unless we get a corresponding increase in the supply of homes, stoking demand again will just see home prices continue to rise, thus offsetting the benefit of lower mortgage rates.

This is the balance the Fed has, anyone reliant on borrowing is desperate for rate cuts. That baby boomer who is clipping their Treasury coupons is hoping the Fed only cuts 25 bps, not 50.

Bank Indonesia unexpectedly cut its overnight rate to 6% from 6.25%. The Governor said "the time is right." As for what comes next, "Bank Indonesia will continue to keep an eye on the room for lowering policy rate in line with low inflation forecast, the stable and appreciating rupiah, and the need to boost economic growth higher." After a big rally, along with many Asian currencies vs the US dollar, the rupiah is flattish today in response.

Ahead of the BoJ meeting Friday, Japan's August trade data missed expectations as exports grew by 5.6%, about half the estimated increase of 10.6%. Imports were up by just 2.3%, well below the estimate of 15% growth. A typhoon in August definitely disrupted shipments but tough to say by what extent. Exports to Japan's Asian trading partners led the growth as they were little changed to the US. Product wise, machinery, semis, chemicals and electrical machinery drove the gains.

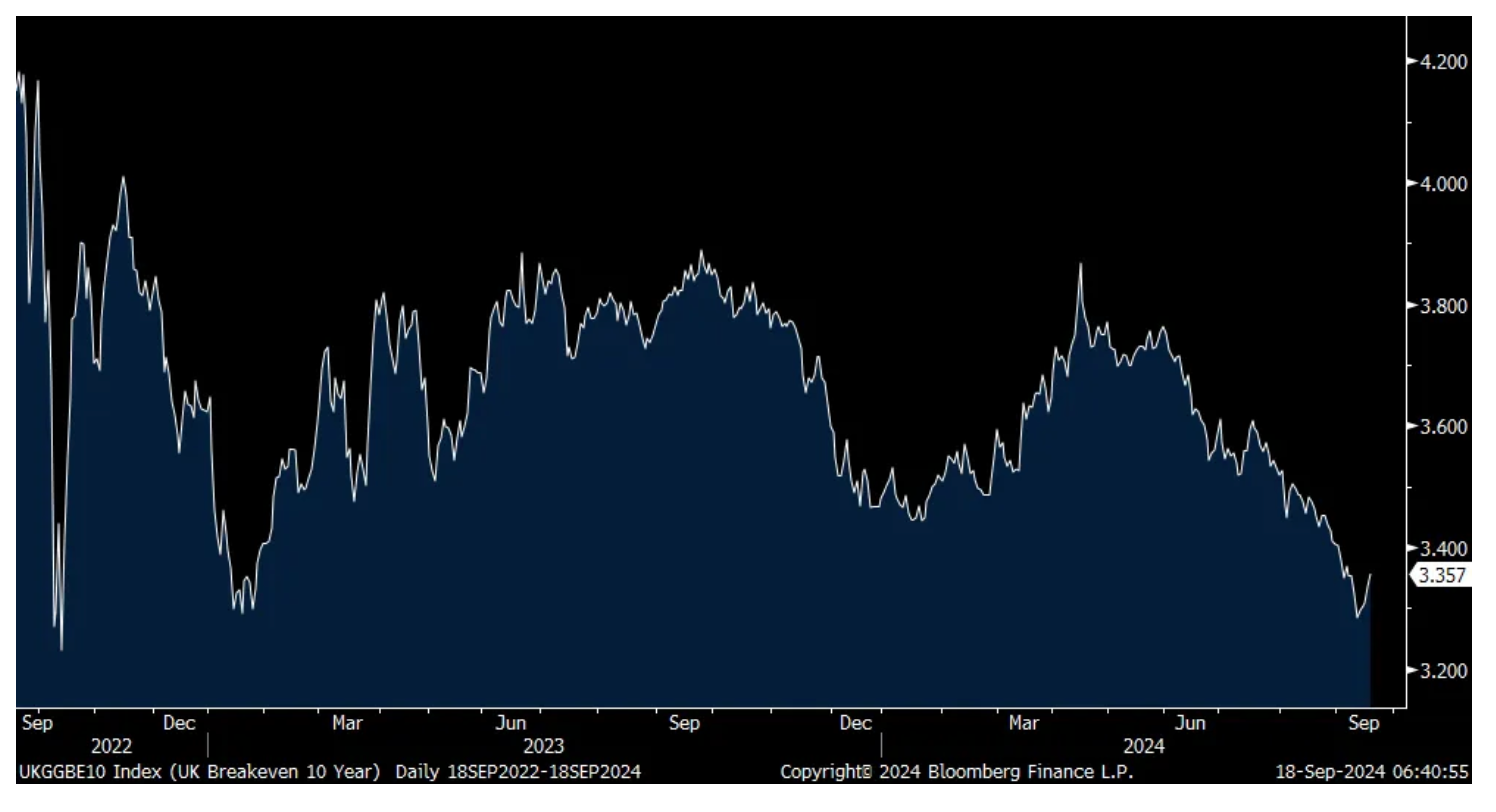

In Europe, the one thing of note was the UK inflation data the day before the Bank of England meets. Headline and core CPI rose 2.2% and 3.6% respectively and as expected. The services component remains the real sticking point, up by 5.6% y/o/y. PPI, for both input and output charges, were softer than anticipated. While CPI was in line, the persistent rise in service prices has the UK 10 yr inflation breakeven higher by 2.2 bps to 3.36% but it has fallen sharply since the recent peak in April. The Bank of England is not expected to trim its 5% bank rate after doing so at its prior meeting unexpectedly with a 5-4 vote.

UK 10 yr Inflation Breakeven

BY Doug Kass · Sep 18, 2024, 10:25 AM EDT

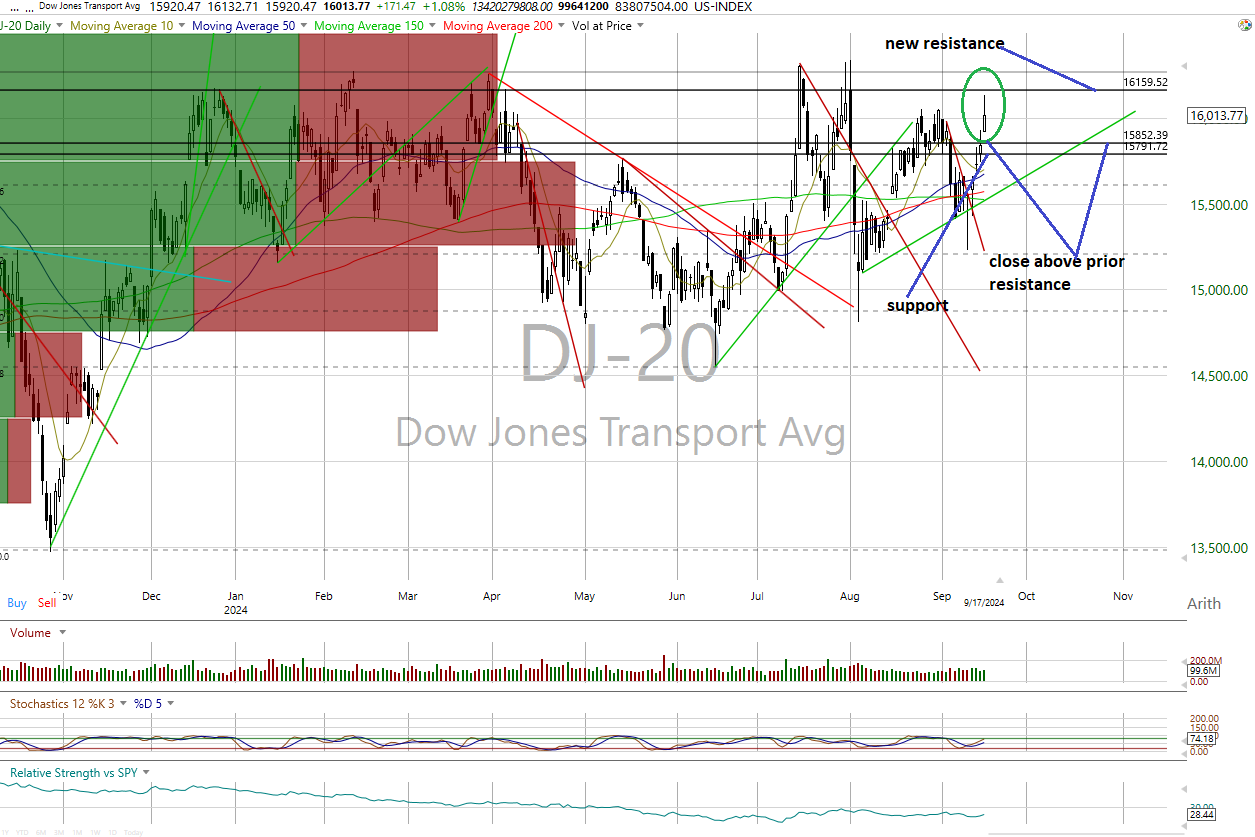

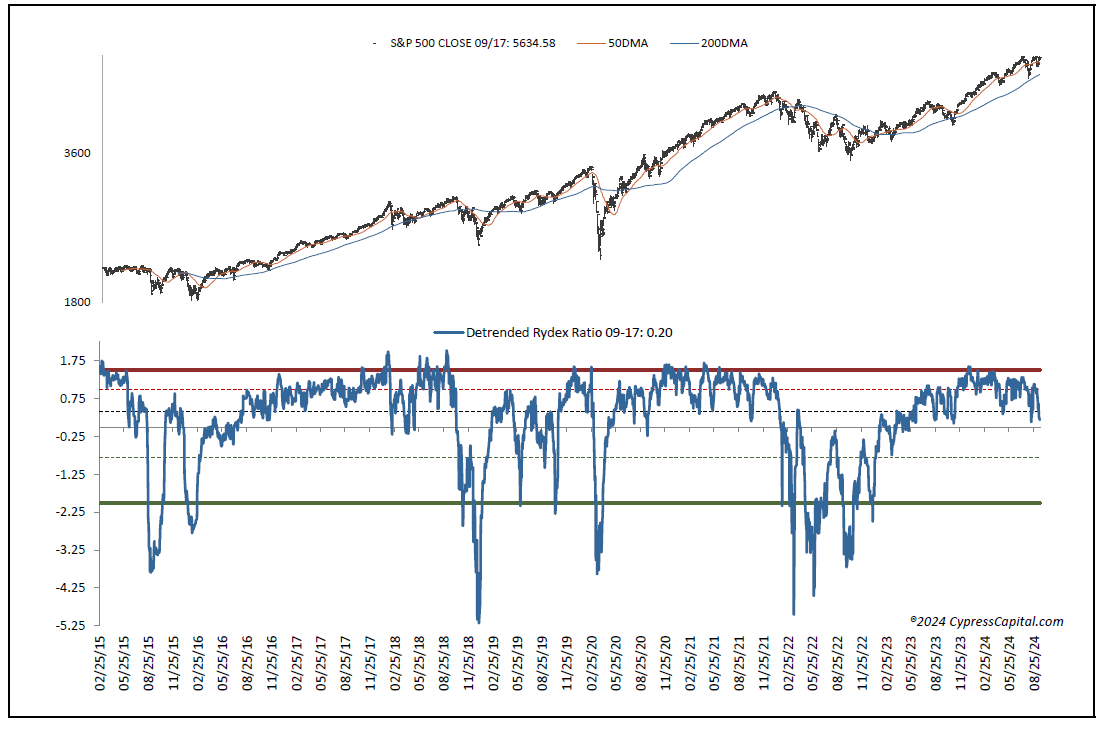

Only the Dow Jones industrial average closed lower on Tuesday as the rest of the major equity indexes posted gains. All closed near the midpoint of their intraday ranges as three of the charts closed above their resistance lines, leaving all the charts in near-term uptrends. Cumulative market breadth is also in near-term uptrends. The McClellan over-bought, over-sold oscillators are mostly overbought.

But the three contrarian sentiment indicators are at levels that suggest the “crowd” is still licking its wounds from the correction. They're non-believers of the current strength, which we view as a positive influence. Valuation does remain a concern as the forward valuation of the S&P 500, based on Bloomberg’s forward one-month earnings estimates remains well above ballpark fair value. With that said, the recent shift in the weight of the evidence still suggests buying names that fit our analysis discipline should be bought on weakness.

Aside from the Dow industrials, the indexes rose with bullish New York Stock Exchange and Nasdaq internals. The Dow Transports, mid-caps and Russell 2000 all closed above resistance that shifted the Transports into a bullish trend and joining the rest in that status. These were technically significant events.

Cumulative market breadth remains bullish as well for the All Exchange, NYSE and Nasdaq. But all the stochastic levels are overbought. They can stay overbought, however, for extended periods. Thus far, no bearish crossover signals have been generated.

The data is mixed, but the sentiment indicators are more encouraging. The neutral one-day McClellan overbought/oversold oscillators (All Exchange: +55.33 NYSE: +74.61 Nasdaq: +44.63) may present some headwinds. The percentage of S&P issues trading above their 50-day moving averages, a contrarian indicator, rose to 75% and stayed neutral.

Of note, the contrarian detrended Rydex Ratio is unchanged at a neutral 0.20. The typically wrongly leveraged exchange-traded fund traders are not believers of the rally and that's a positive by our discipline. In contrast, the Open Insider Buy/Sell Ratio dipped to 35.3%, but insiders have been increasing their buying lately as it remains neutral.

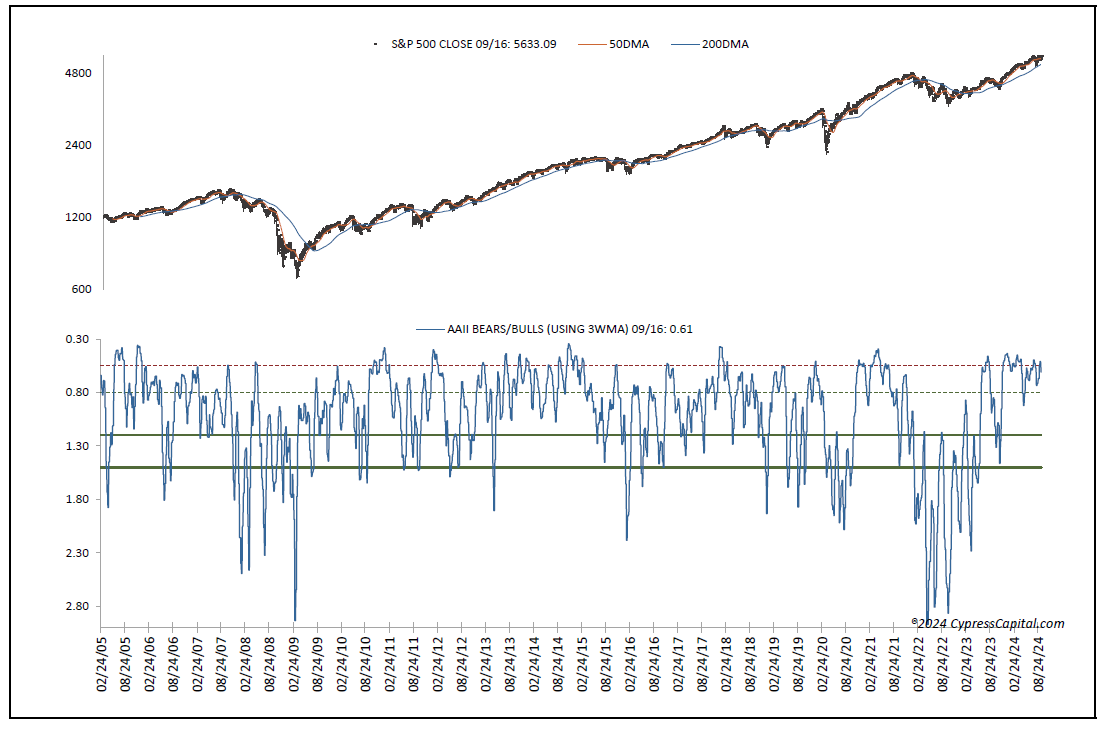

This week’s American Association of Individual Investors Bear/Bull Ratio, a contrarian indicator, rose to 0.61 as the number of bears rose, staying neutral. Also encouraging is the Investors Intelligence Bear/Bull Ratio remains neutral at 22.6/43.5 as the number of bulls declined by almost 10 points.

Finally, valuation remains a concern. The 12-month consensus earnings estimate for the S&P from Bloomberg dropped to $257.53. That leaves its forward price-to-earnings at 21.9, still well above the “rule of 20” ballpark fair value at 16.4. We believe this premium still presents some risk. Its earnings yield is unchanged at 4.57%.

The 10-year Treasury yield is unchanged at 3.62%. Support is 3.57% and resistance at 3.79%. Its near-term trend is bearish. The U.S. Dollar, via the Dollar Index Bullish Fund UUP, closed higher at $28.189. Its trend is bearish with new support at $28.06 and resistance at $28.22.

We believe you can buy individual names on weakness.

Sep 18, 2024, 10:10 AM EDT

* As data centers are what overwhelm the grid, hyperscalers should be paying for the necessary grid upgrades that need to be put in place to accommodate them.

* This is something you will not hear from Dan Ives!

This is all interesting regarding power for AI data centers.

It is one more self-own from the "hyperscalers" -- those giant cloud service providers.

Their data centers are what overwhelm the grid, therefore the hyperscalers should be paying for the necessary grid upgrades that need to be put in place to accommodate them. But this stuff is so dis-economic, they need to try things like this to stick their data center power bill on the average person -- many of whom are struggling to make ends meet, and cannot even pay their power bill and buy food at the same time.

Meanwhile, the hyperscalers and executives at these companies are all flush with cash. In addition to their data centers consuming enough power to run a small city, they use energy on yachts, private planes, and numerous giant homes while they lecture us all about the environment.

Look at this from Washington Post reporter Caroline O'Donovan:

A regulatory dispute in Ohio may help answer one of the toughest questions hanging over the nation’s power grid: Who will pay for the huge upgrades needed to meet soaring energy demand from the data centers powering the modern internet and artificial intelligence revolution? Google, Amazon, Microsoft and Meta are fighting a proposal by an Ohio power company to significantly increase the upfront energy costs they’ll pay for their data centers, a move the companies dubbed “unfair” and “discriminatory” in documents filed with Ohio’s Public Utility Commission last month.

American Electric Power Ohio said in filings that the tariff increase was needed to prevent new infrastructure costs from being passed on to other customers such as households and businesses if the tech industry should fail to follow through on its ambitious, energy-intensive plans.

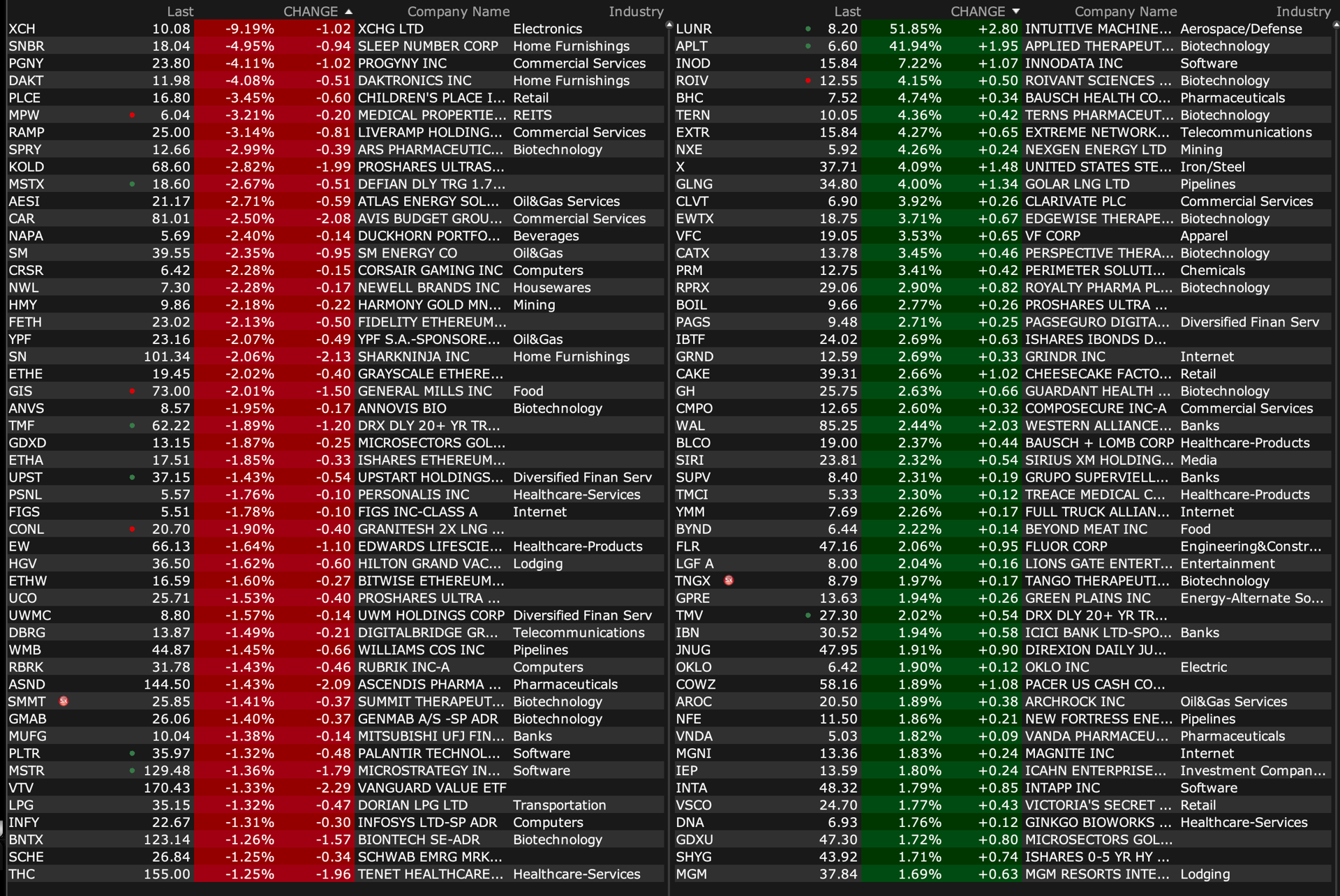

BY Doug Kass · Sep 18, 2024, 9:47 AM EDT

-LUNR +51% (NASA awards Intuitive Machines Near Space Network Contract with a max potential value of $4.8B)

-APLT +43% (update on Govorestat: FDA no longer intends to hold Advisory Committee meeting and Priority Review of NDA is continuing, with post-marketing requirements expected in Oct, PDUFA date Nov 28th)

-PSTV +20% (showcases new Interim ReSPECT-GBM Phase2 Trial Data at the 2024 Congress of Neurological Surgeons Annual Meeting)

-VVOS +19% (receives FDA 510(k) clearance to treat moderate to severe pediatric sleep apnea and snoring in children aged 6 to 17)

-BCTX +10% (US FDA authorized Expanded Access Policy for metastatic breast cancer patients)

-SWVL +10% (secures $2.6M in new annual contracts in Saudi Arabia during Q3)

-X +4.2% (Nippon Steel said to win a CFIUS extension for review of US Steel deal)

-TGTX +3.9% (new data for BRIUMVI (ublituximab-xiiy) demonstrate that 92% of patients with relapsing multiple sclerosis were free from disability progression after 5 years of treatment)

-EWTX +3.7% (to host webcast event to discuss Top-Line Data from Phase 1 trial in Healthy Subjects and Phase 2 CIRRUS-HCM Trial in Patients with Obstructive Hypertrophic Cardiomyopathy (HCM) on September 19th)

-VFC +3.2% (Barclays Raised VFC to Overweight from Equal Weight, price target: $22)

-BLCO +2.4% (reportedly Blackstone, KKR, CVC Capital and TPG Capital mull bids for Bausch & Lomb, which plans to begin exclusive talks by end of Oct)

-SIRI +2.3% (Guggenheim Securities Raised SIRI to Buy from Neutral, price target: $30)

-ROIV +2.2% (Organon to acquire unit Dermavant including its Innovative Dermatologic Therapy, VTAMA (tapinarof) Cream 1% for up to ~$1.2B)

-VSCO +1.8% (Barclays Raised VSCO to Equal Weight from Underweight, price target: $25)

-CBUS -18% (announces IPO pricing of 3M shares at $4.00/shr)

-ME -9.2% (Independent Directors resign from Board)

-CWST -4.2% (prices 4.5M share secondary at $100.00)

-MGRC -4.2% (WSC terminates merger with McGrath RentCorp due to regulatory hurdles)

-GIS -2.0% (earnings, guidance)

-EW -1.6% (Jefferies Cuts EW to Hold from Buy, price target: $70)

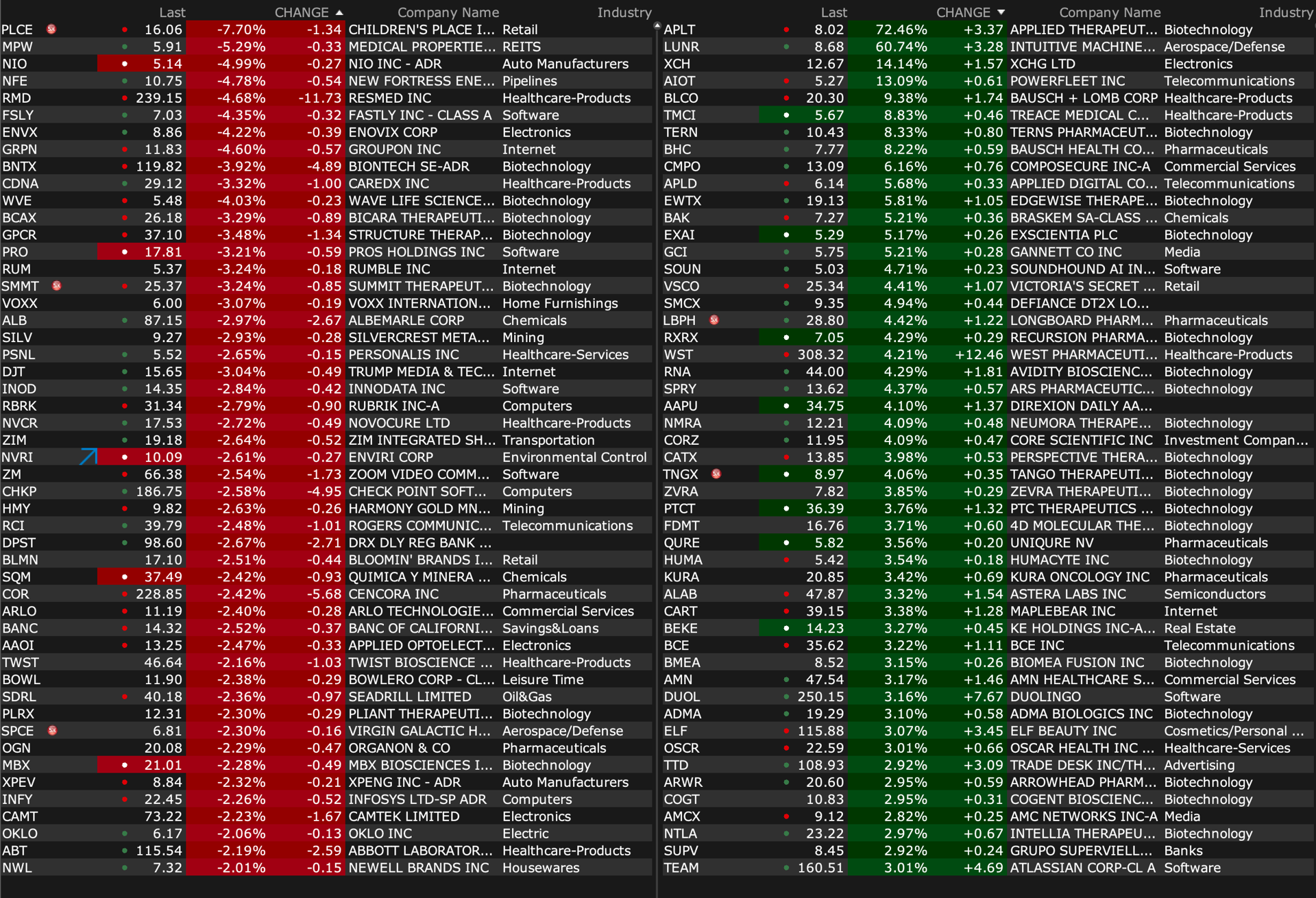

BY Doug Kass · Sep 18, 2024, 9:24 AM EDT

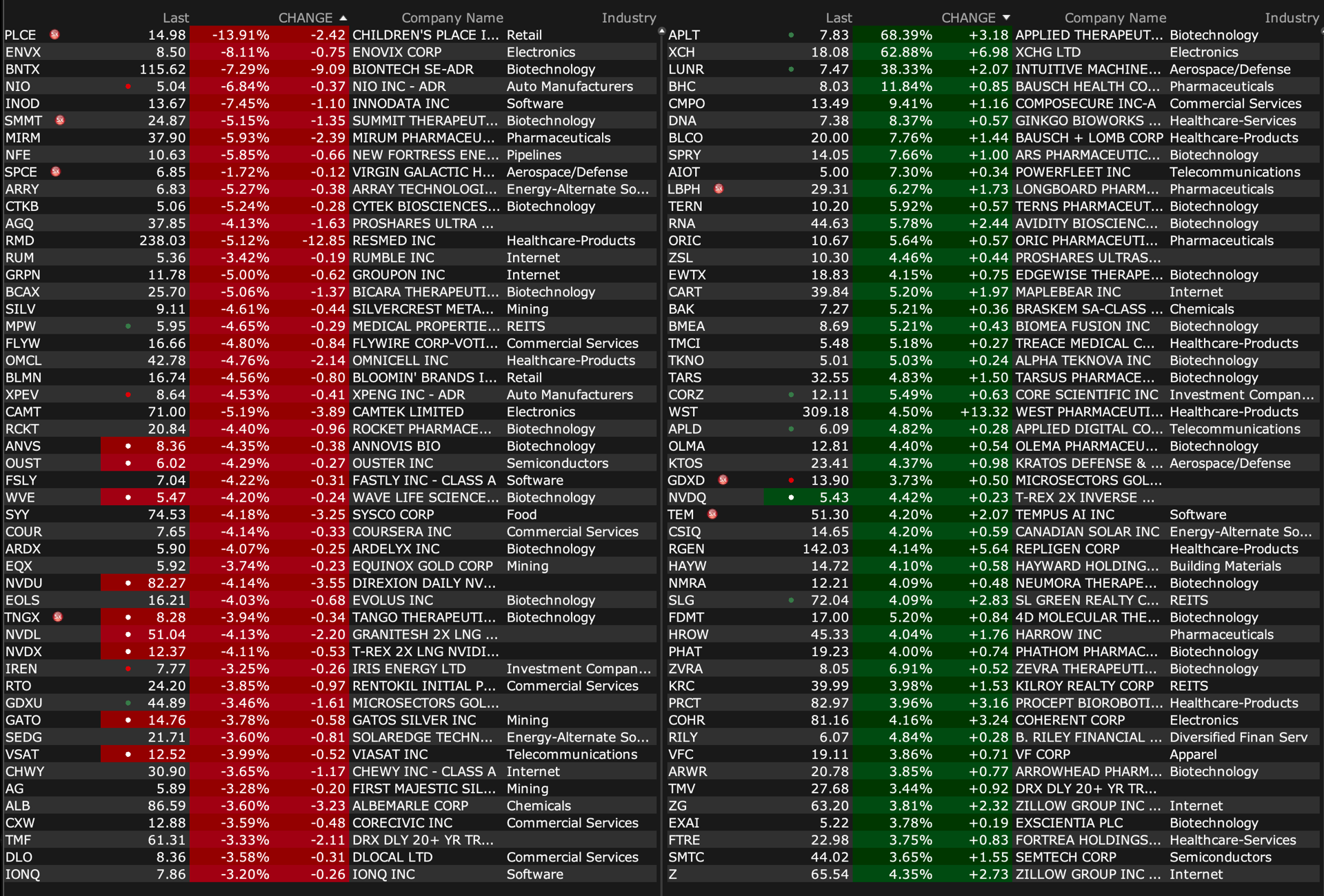

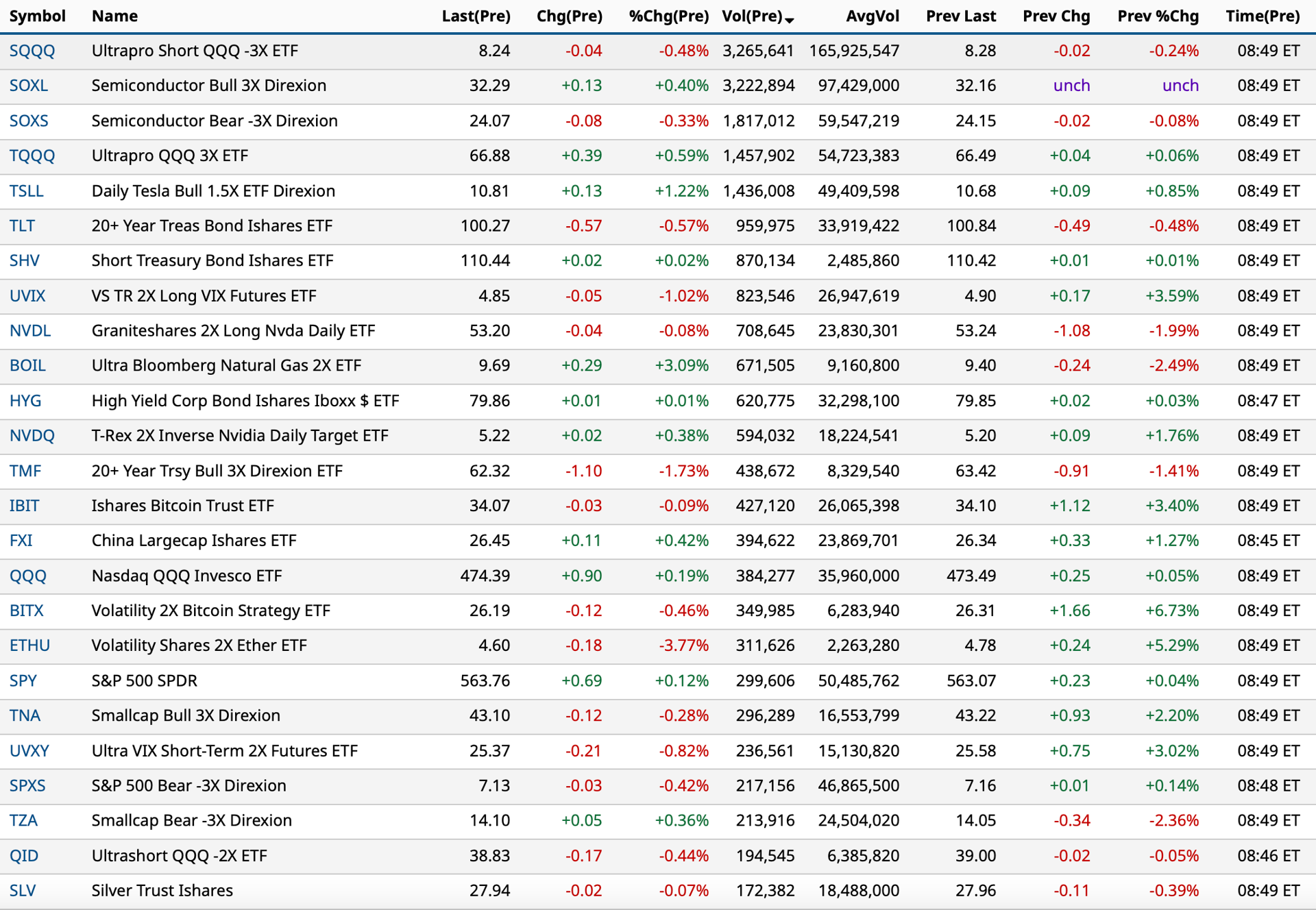

Charts from 8:49 a.m. ET:

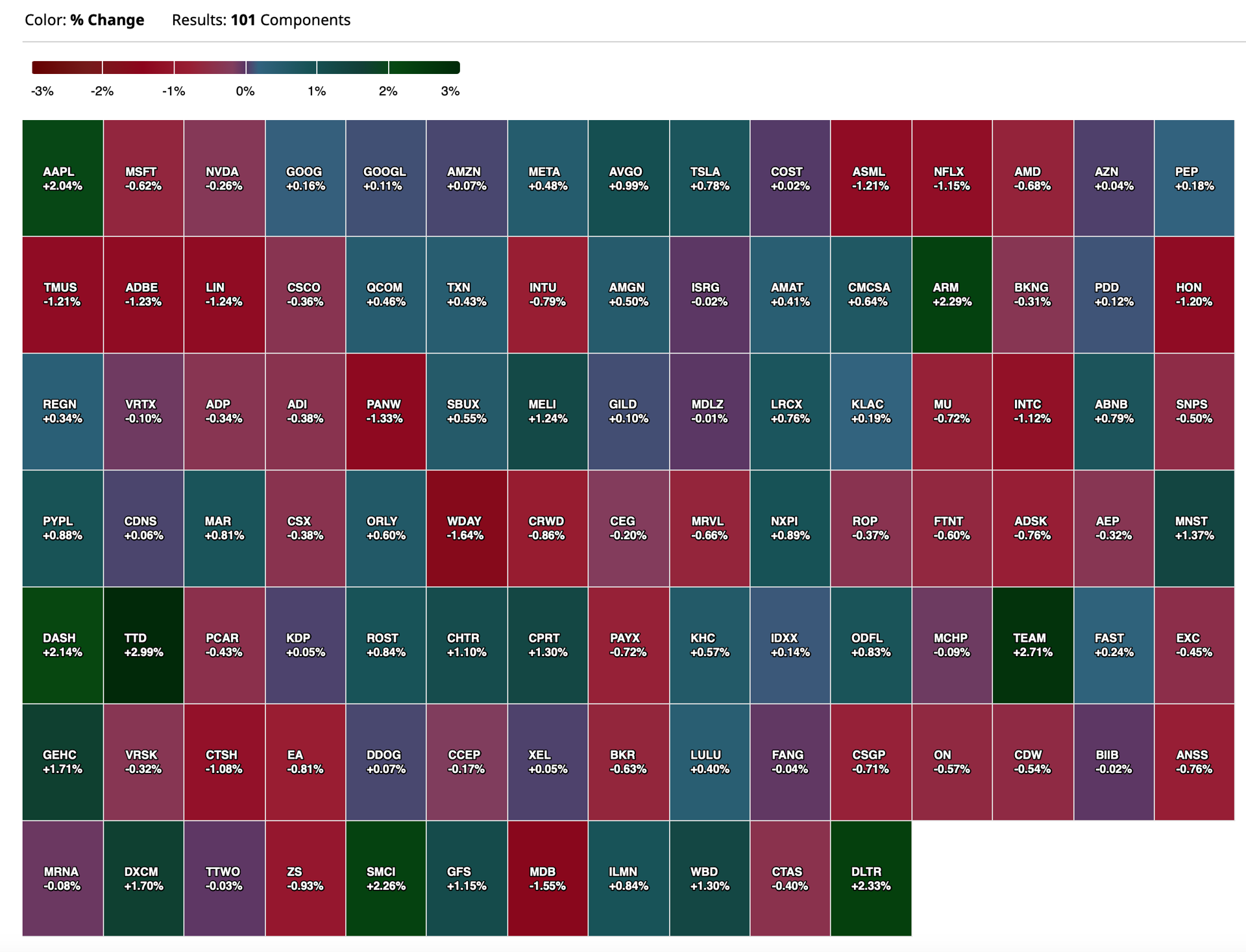

BY Doug Kass · Sep 18, 2024, 9:22 AM EDT

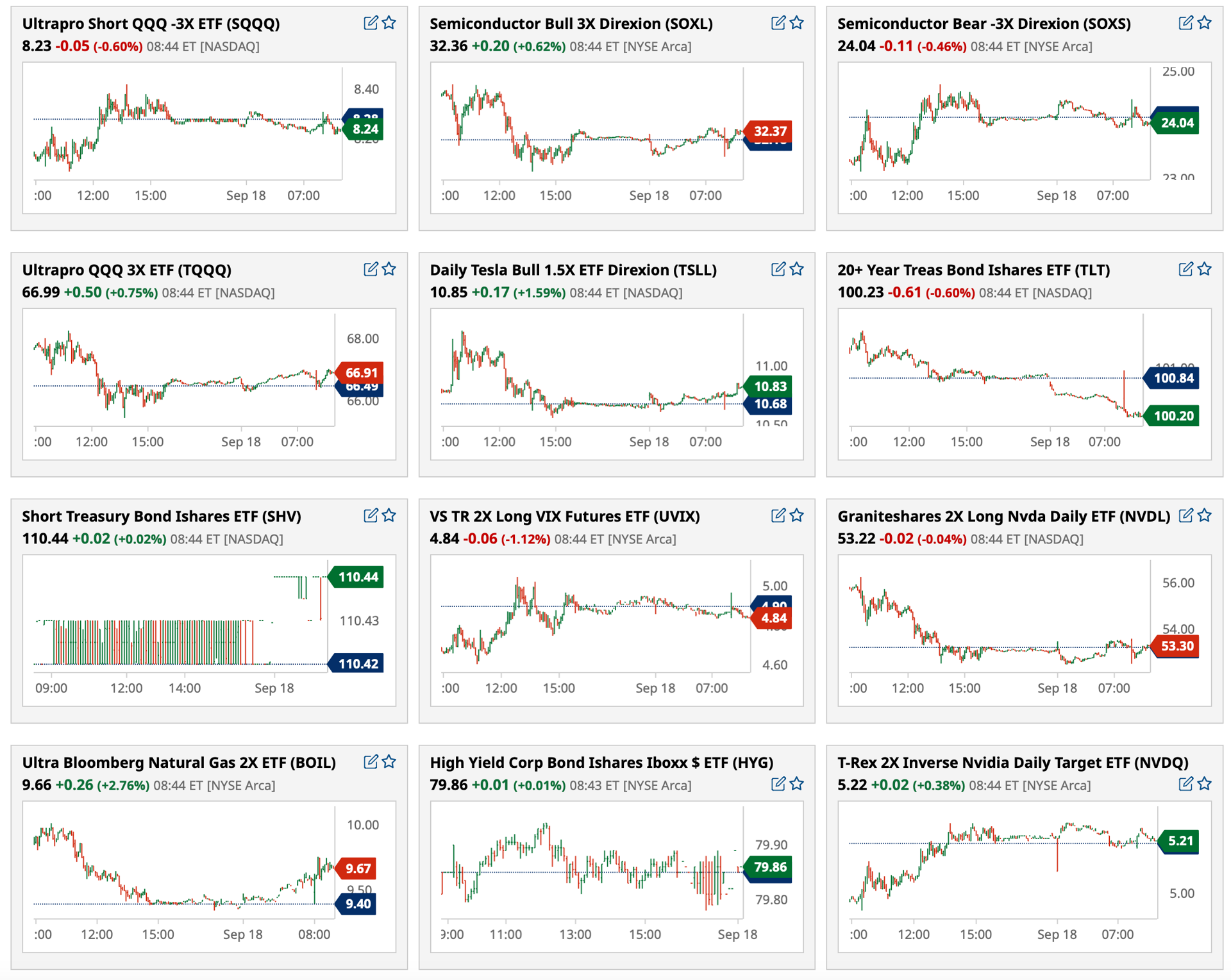

Chart from 8:30 a.m.:

BY Doug Kass · Sep 18, 2024, 8:41 AM EDT

From Charlie:

BY Doug Kass · Sep 18, 2024, 8:30 AM EDT

* Yesterday I added to my already large MSOS long.

From The Dales Report's Shadd Dales and Anthony Varrell:

With yesterday’s surprise headline that the DEA acknowledged the legitimacy of the two-step process used in the HHS’s cannabis rescheduling recommendation, it got us thinking back to the OLC memo. The memo is one of the most powerful pieces supporting rescheduling, as it legitimized this new streamlined process while taking a jab at the outdated five-step method used in the past to classify drugs.

Now, with the DEA jumping on board with the two-step approach—and let me remind you, this is the only part of the puzzle we know they agree with—the game has changed. It’s going to be entertaining to watch Smart Approaches to Marijuana (SAM), if they get their day in court, try to argue against a process that both the OLC and DEA have now deemed legitimate.

BY Doug Kass · Sep 18, 2024, 8:20 AM EDT

BY Doug Kass · Sep 18, 2024, 8:08 AM EDT

From JPMorgan:

US: FED DAY. Futs are up small with Tech in line and small-caps lagging. Pre-mkt, Mag7 is mixed, and Semis are weaker with NVDA -40bps; GOOG +70bps and MSFT +29bps. Bond yields are mixed with the curve twisting steeper; USD lower to start the day. Cmdtys are seeing weakness in Energy and Metals but strength in Ags. Today’s focus is on the Fed and the press conference, detailed views are in the body of this note.

and...

EQUITY AND MACRO NARRATIVE: Should investors brace themselves for 25bps? After yesterday’s Retail Sales and Industrial Production prints, the Atlanta Fed’s GDPNow increased from 2.5% to 3.0%.This means that Coincident Indicator Indices should also rise; that index correlates with real GDP growth which is putting upward pressure on forecasts for 24Q3. The driver of this is Retail Sales less Goods Inflation from CPI which equates to a 0.3% increase in Real Retail Sales. At this stage, it is unclear how much of the monthly declines are due to lower volumes and how much are due to lower prices. Based upon recent earnings commentary, it feels like more of the latter than the former. The message is that the US Consumer continues to outperform all expectations, dating to 23Q1.

Regarding Industrial Production, while a good monthly print, is still a weak spot of the economy but easing rates could lead to a reboot in the manufacturing sector which would also improve the unemployment rate. Further, the bull steepening of the yield curve should reduce pressure on regional banks, increasing loan supply, which is now in competition with private credit, and one can paint a picture of resurging growth in 25H1 given the increased credit impulse. If this is the Fed’s view, then 25bps with a dovish press conference seems more likely. However, with the Cleveland Fed’s real-time inflation forecast at 2.27% for September (2.07% PCE), compared to 2.5% official CPI for August, the Fed may view inflation as solved and thus Fed Funds is too high especially when compared to academic models so why not cuts rates more aggressively since both fiscal and monetary policy actions have been extraordinary in this COVID era? Feroli sticks with his 50bps cut call with a dovish press conference. The balance of this note is (i) Fed scenario analysis with breakevens from Rates Trader David Nadle; (ii) Returns charts for 1-month and 3-months after the first Fed cut; (iii) more analysis on the 25bps vs. 50bps argument; (iv) Retail Sales post-mortem; and (v) the usual assortment of levels, calendar, news links, and JPM Research.

FED SCENARIO ANALYSIS – this is not a product of Research but a Trading Desk view

US Market Intel’s Trading the Easing Cycle note is here. The note does historical comparisons to other easing cycles, gives background on the current economic environment, and has a series of charts and graphs including historical returns across various easing cycles.

RATES TRADING (David Nadle) – Over the last several sessions we have seen better selling across the LHS complex. FM has added new shorts in 3m-1y expiry 1y and 2y tails mostly in ATM straddles and low strike receivers. Skew in this sector has rotated towards the payer side of the distribution as the forwards are embedding steep inversion, and the risk to higher volatility has shifted towards puts (see below). FM has been adding long positions in 1m-1y expiry 10y and 30y straddles and payers vs LHS shorts, driving a bid to longer tail vega as forward volatility shifts away from the front end. Program selling has been running below its normal pace (closer to 250mm 1m10y/da) as the level of gamma has dropped significantly (1m10y near 93 ABPV, and has struggled to break 90 this year), while FM continues to add. At these yield levels and with a lack of supply we are near a strike concentration range to the rally (see below), which sits only 5-7bps below here in CT10. It’s worth noting that these breakevens are optically low despite the large uncertainty around fed pricing and lack of definitive communication. Gamma appears cheap in our view as a result. We remain short vega in intermediate LHS vs deeper vega.

· SFRZ4: 7.00bp

· SFRZ5: 10.25bp

· SFRZ6: 9.00bp

· FV: 9.00bp

· 5y: 8.50bp

· TY: 7.50bp

· 10y: 6.75bp

· US: 6.00bp

· 30y: 5.25bp

· *the 1d terminal breakeven (premium/dv01) for a straddle struck at 3pm today, expiring at 3pm Wednesday

BY Doug Kass · Sep 18, 2024, 6:50 AM EDT

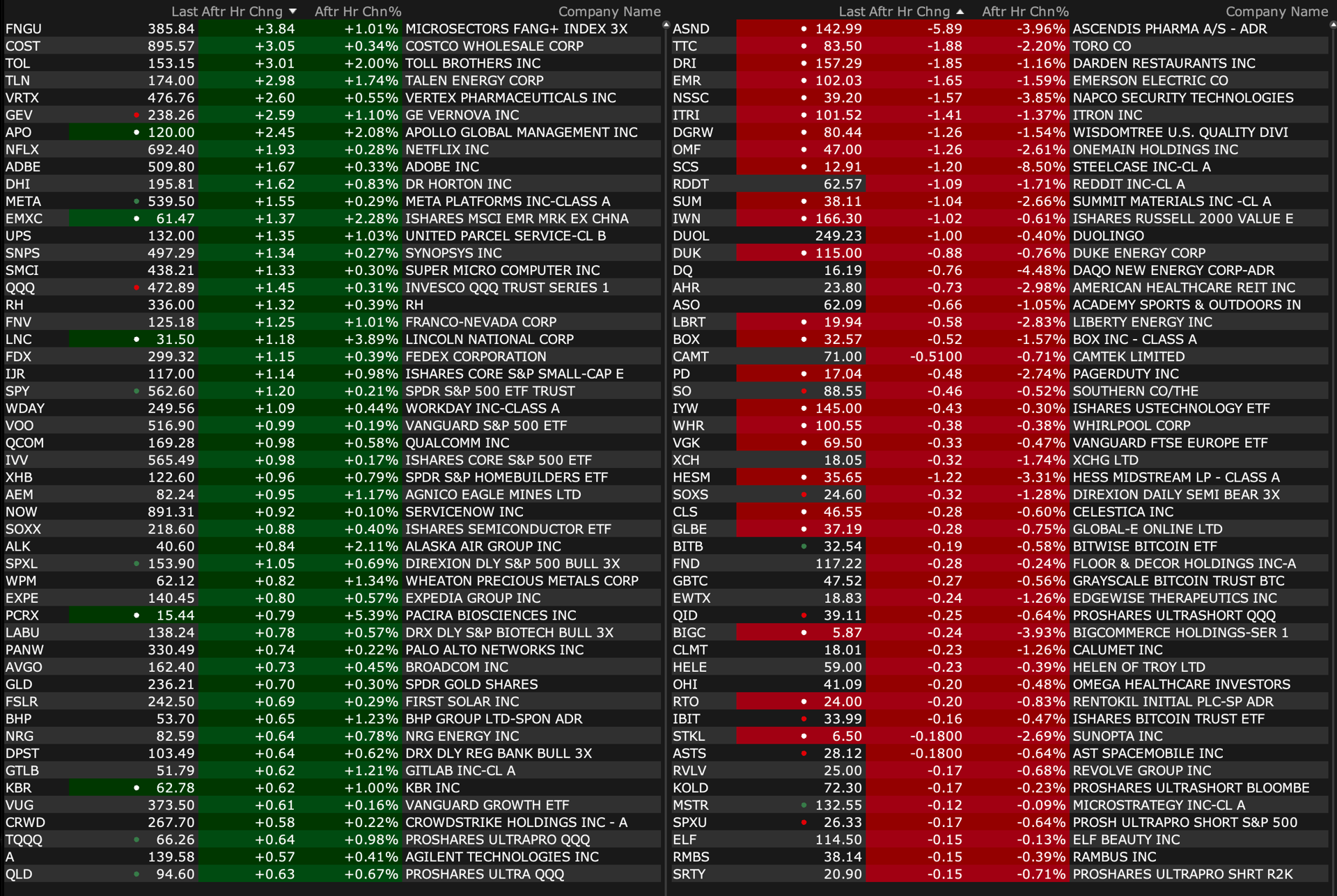

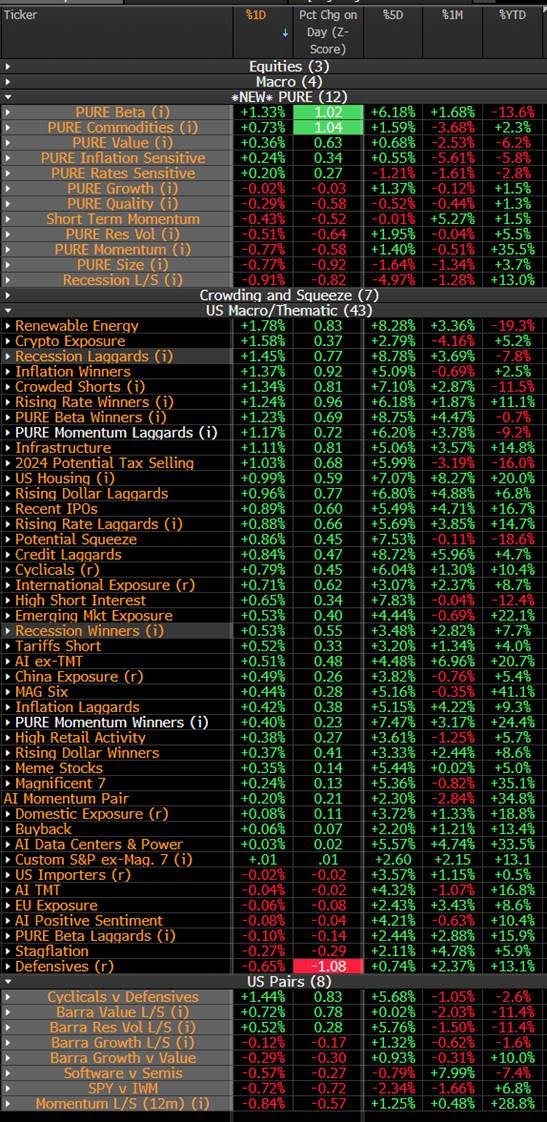

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Sep 18, 2024, 6:34 AM EDT

Bonus — Here are some great links:

Three Things to Know About Last Week

Oil Tests Support as Traders Abandon Oil ETFs

BY Doug Kass · Sep 18, 2024, 6:17 AM EDT

SEP 17, 2024 8:00 AM EDT

* Market expectations and monetary policy narratives are inconsistent.

* I call BS to more "cowbell."

Many market participants are begging for more easing tomorrow (50 basis points from a number of economists and 75 basis points from Senator Elizabeth Warren):

But some of the conditions (like elevated asset prices and others below) that exist argue for less ease:

Regardless, as noted by the GOAT (in his quote at the beginning of this column), Stan Druckenmiller, the Wall Street narratives (as they relate to anticipated/desired monetary policy) are terribly inconsistent and asymmetric.

Stop begging.

Position: None

BY Doug Kass · Sep 18, 2024, 5:55 AM EDT

"We made a good strong start at this... because we're confident in our inflation forecasts", which most recently have been dead fucking wrong #Transitory ! -Powell