My Tweet of the Day (Part Trois)

BY Doug Kass · Sep 17, 2024, 5:05 PM EDT

BY Doug Kass · Sep 17, 2024, 5:05 PM EDT

As of 4:23 p.m.:

BY Doug Kass · Sep 17, 2024, 4:45 PM EDT

BY Doug Kass · Sep 17, 2024, 4:34 PM EDT

Adding back to MSOS at $6.89.

BY Doug Kass · Sep 17, 2024, 4:00 PM EDT

* The S&P and Nasdaq had more moves than a shortstop batting .110 today!

I was active today.

* In premarket trading: Shorted more SPY at $564.91 and QQQ at $475.96. I initiated a MSFT short on the buyback, dividend increase ramp. (Later in the day we took a profit of about $7/share in Mister Softee.)

* With S&P cash +31 handles I shorted some more Index calls. (When the S&P fell by -45 handles I covered all of my short call position)

* Also in the regular trading session:

Buying: GTBIF at $10.50, TSNDF at $1.16, VRNOF at $3.22

Shorting: MSFT at $441, SPY at $565.10, QQQ at $476.84, TOL at $151.80, DHI $195.56, KKR at $127.55, BX at $155.85, XLU at $79.22

* New short ARES (credit and private equity bubble?) at $152.67.

BY Doug Kass · Sep 17, 2024, 3:53 PM EDT

Ares Managment ARES is a global leader in the credit, private equity and real estate markets.

It is my strong view that we are in a bubble in credit and private equity.

BY Doug Kass · Sep 17, 2024, 3:33 PM EDT

Wolf Street howls about the continuing strength of the consumer.

BY Doug Kass · Sep 17, 2024, 3:15 PM EDT

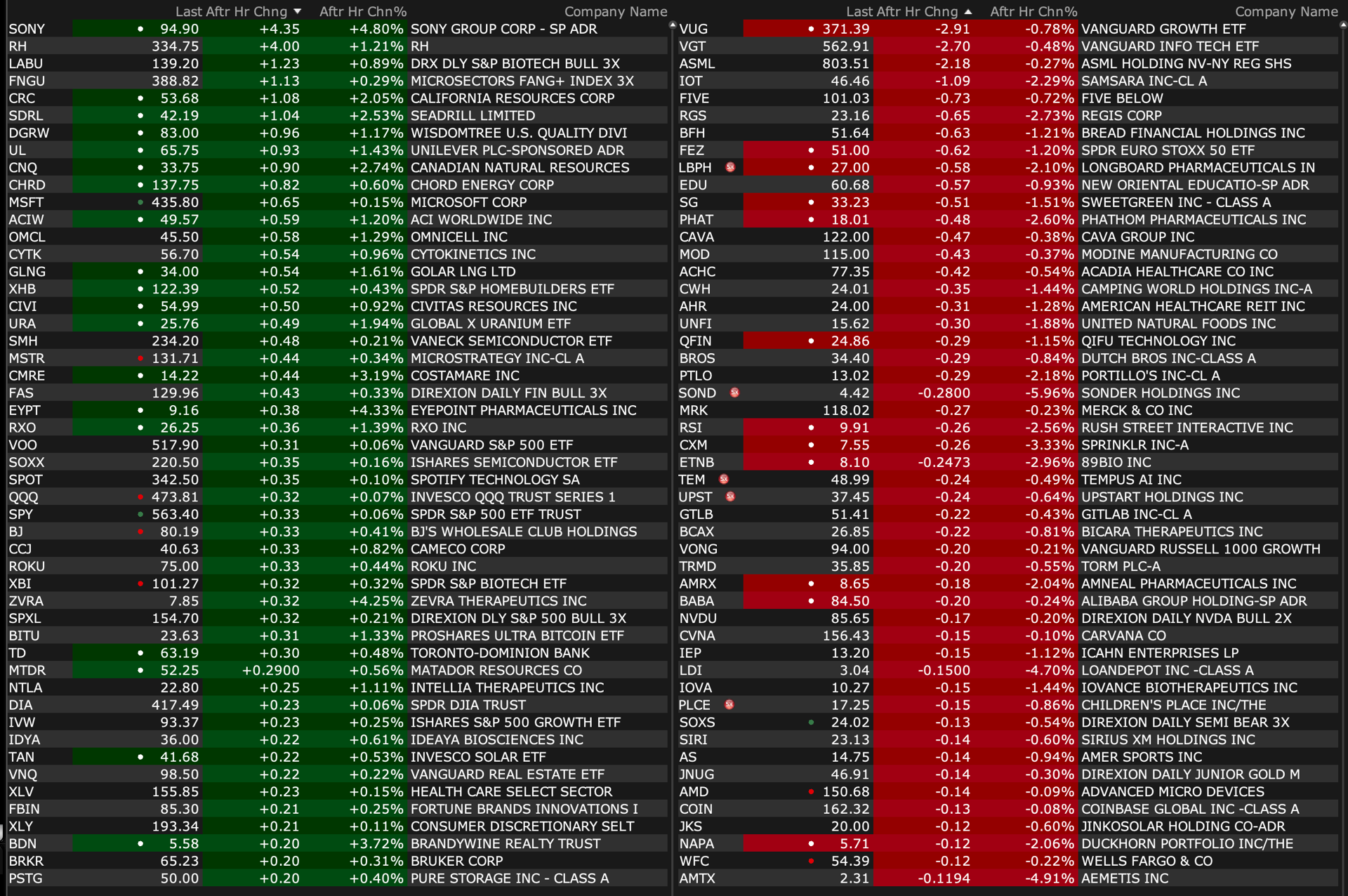

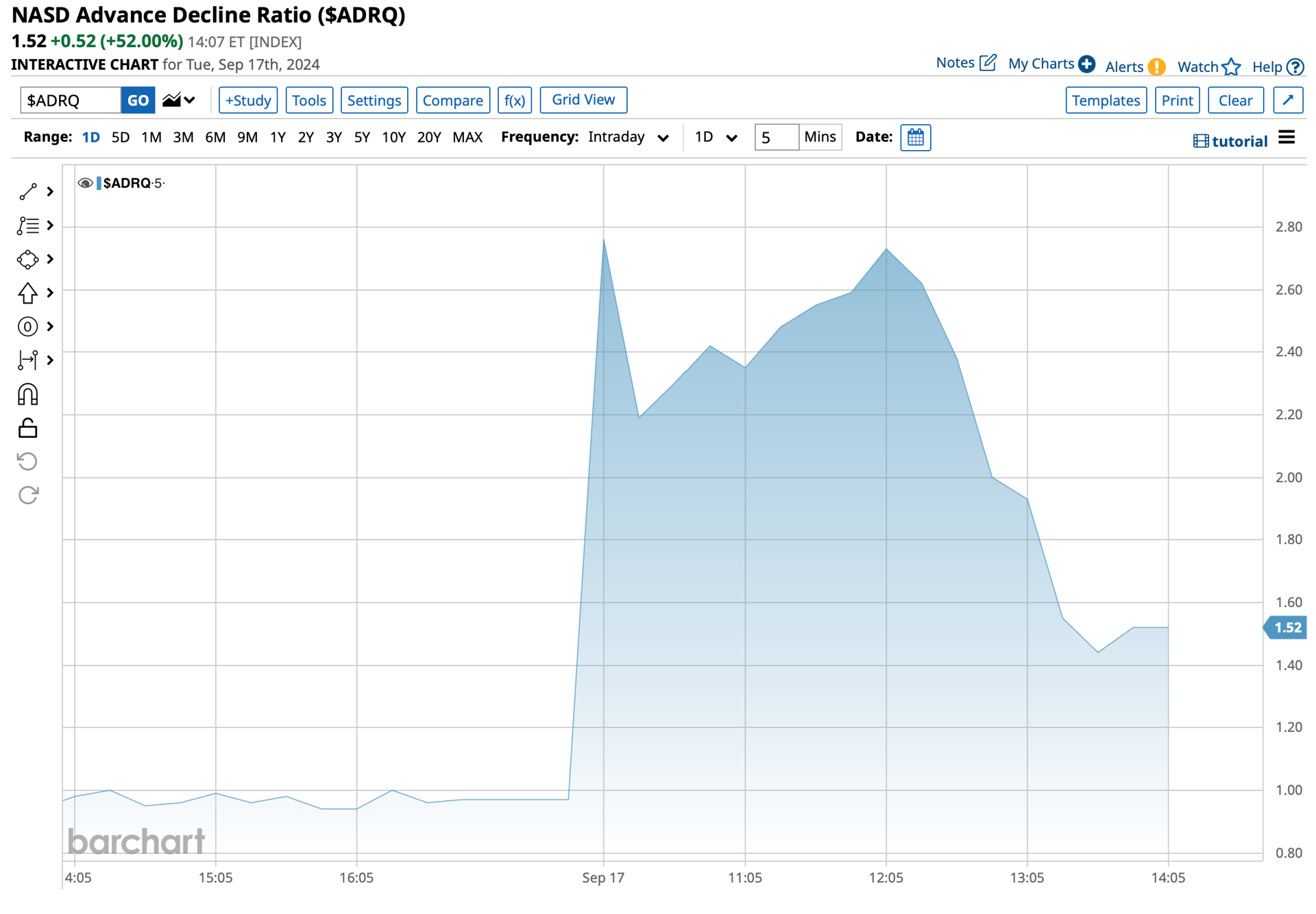

Nasdaq Advance-Decline:

BY Doug Kass · Sep 17, 2024, 2:50 PM EDT

From my friend Shadd Dales:

BY Doug Kass · Sep 17, 2024, 2:35 PM EDT

BY Doug Kass · Sep 17, 2024, 2:25 PM EDT

BY Doug Kass · Sep 17, 2024, 2:10 PM EDT

Not only is the Short Range S&P Oscillator now flashing overbought, but this from The Divine Ms M:

BY Doug Kass · Sep 17, 2024, 1:25 PM EDT

With S&P cash now -45 handles from when I put the short calls out I am taking them back in for a near $5 profit:

With S&P cash +30 handles, I am selling more Index calls short (October, in the money).

Position: Short SPY common (S) and calls (S), QQQ common (S) and calls (S)

By Doug Kass Sep 17, 2024 11:27 AM EDT

BY Doug Kass · Sep 17, 2024, 1:01 PM EDT

I have covered the balance of my MSFT short just now at $433.25.

We initially shorted in the premarket and then again during the early part of the session — with an average cost of close to $441.

BY Doug Kass · Sep 17, 2024, 12:57 PM EDT

I am still short half of my Microsoft MSFT, which is now seven dollars below my cost basis.

BY Doug Kass · Sep 17, 2024, 12:50 PM EDT

BY Doug Kass · Sep 17, 2024, 12:40 PM EDT

I neglected to mention that my CMG/SBUX pairs trade was exceptional yesterday — with CMG +$1.50 and SBUX -$2.23.

BY Doug Kass · Sep 17, 2024, 12:25 PM EDT

Shockingly, market participants are not threatened by changing tax policy — perhaps necessary as our deficit ever rises:

BY Doug Kass · Sep 17, 2024, 12:15 PM EDT

With S&P cash +30 handles, I am selling more Index calls short (October, in the money).

BY Doug Kass · Sep 17, 2024, 11:27 AM EDT

BY Doug Kass · Sep 17, 2024, 11:16 AM EDT

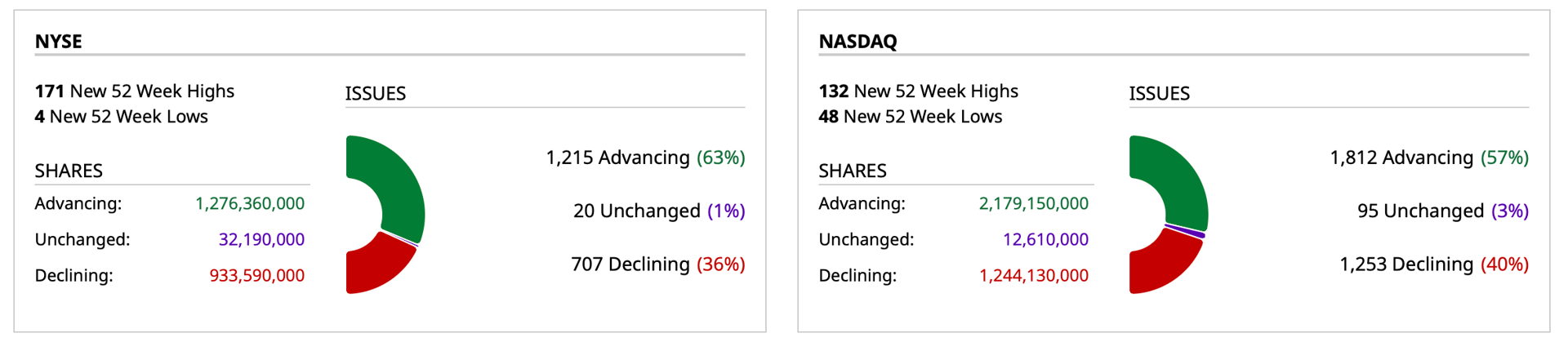

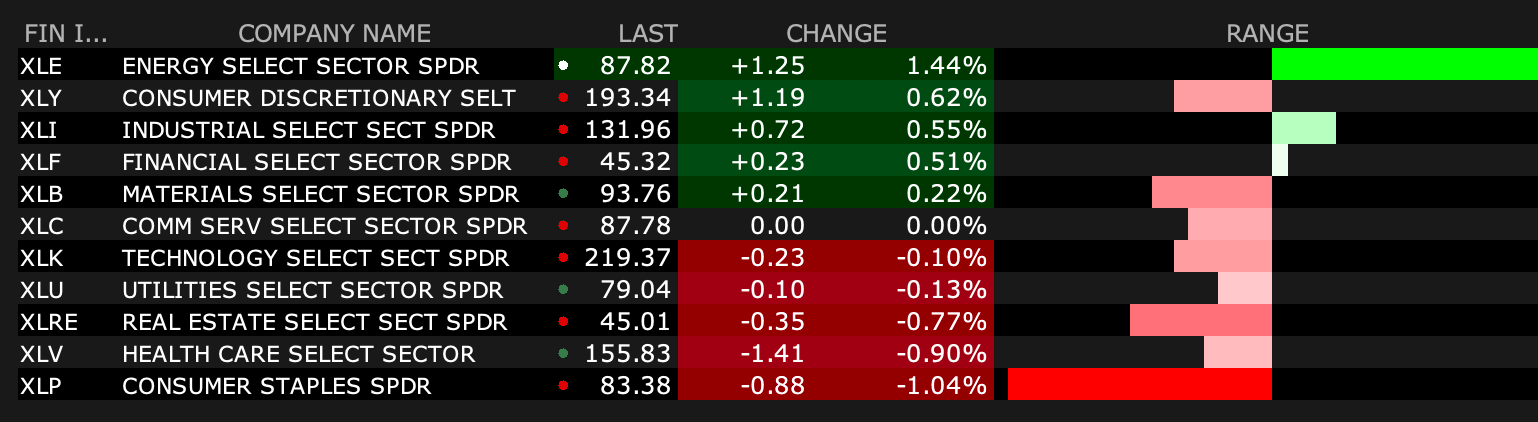

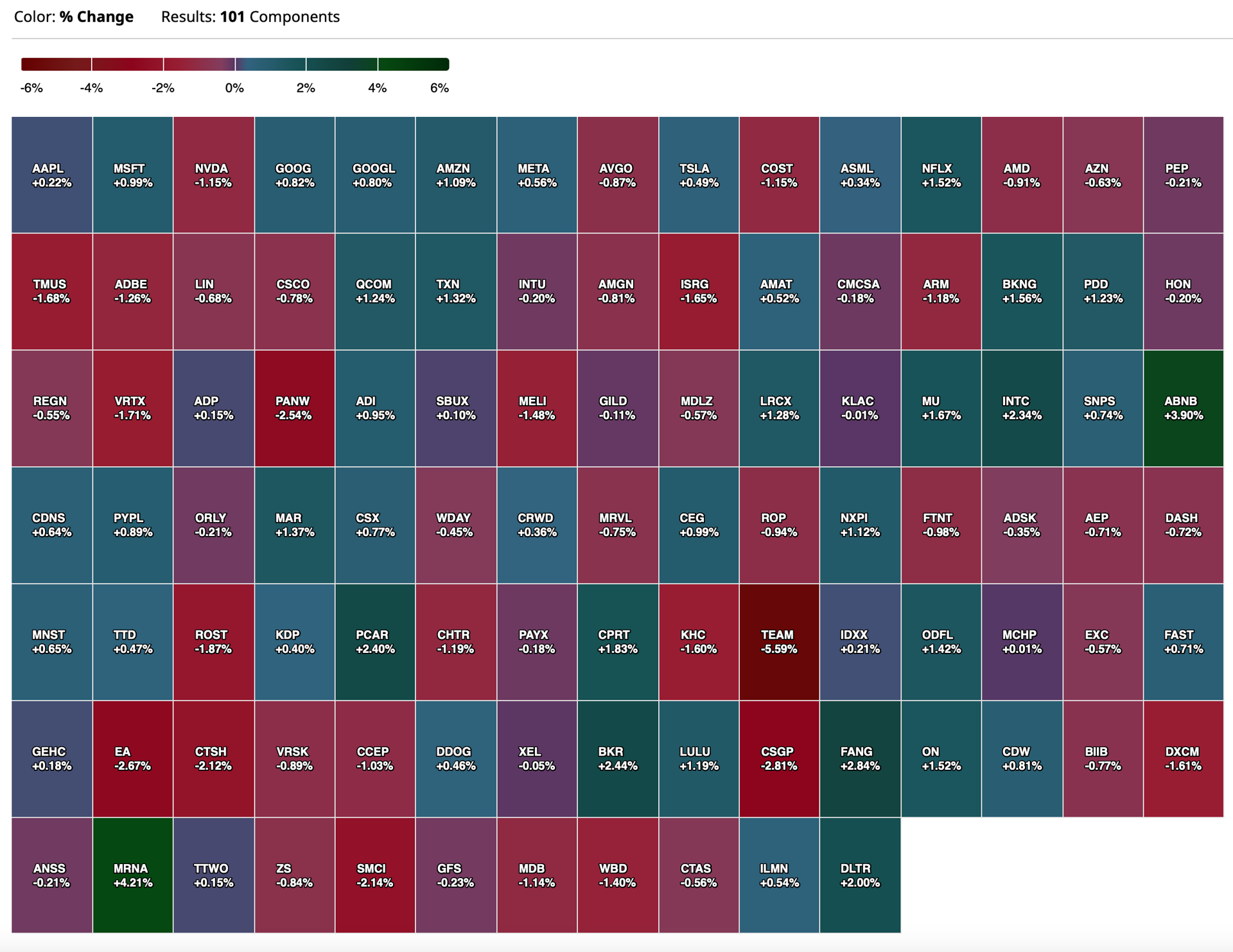

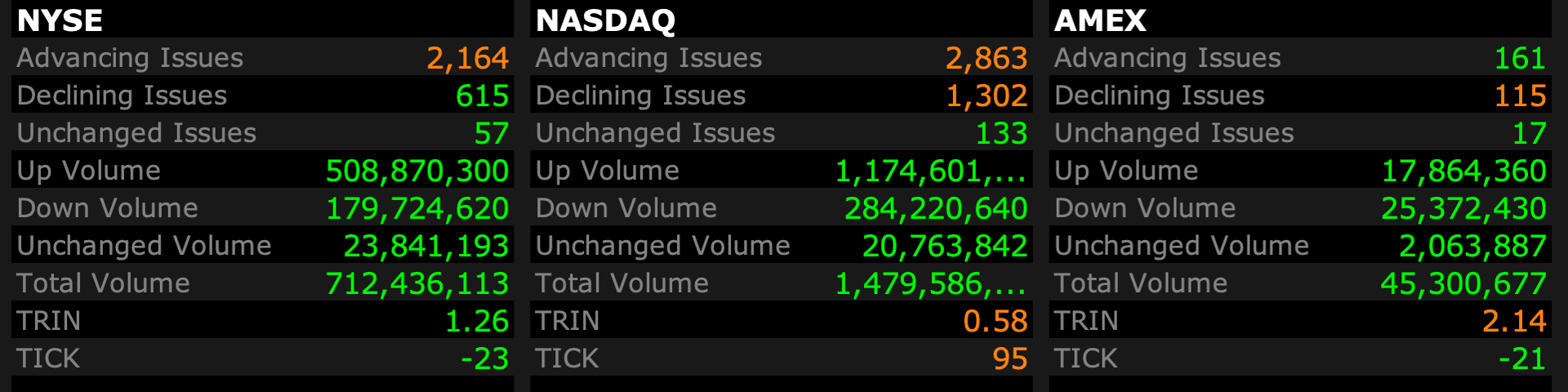

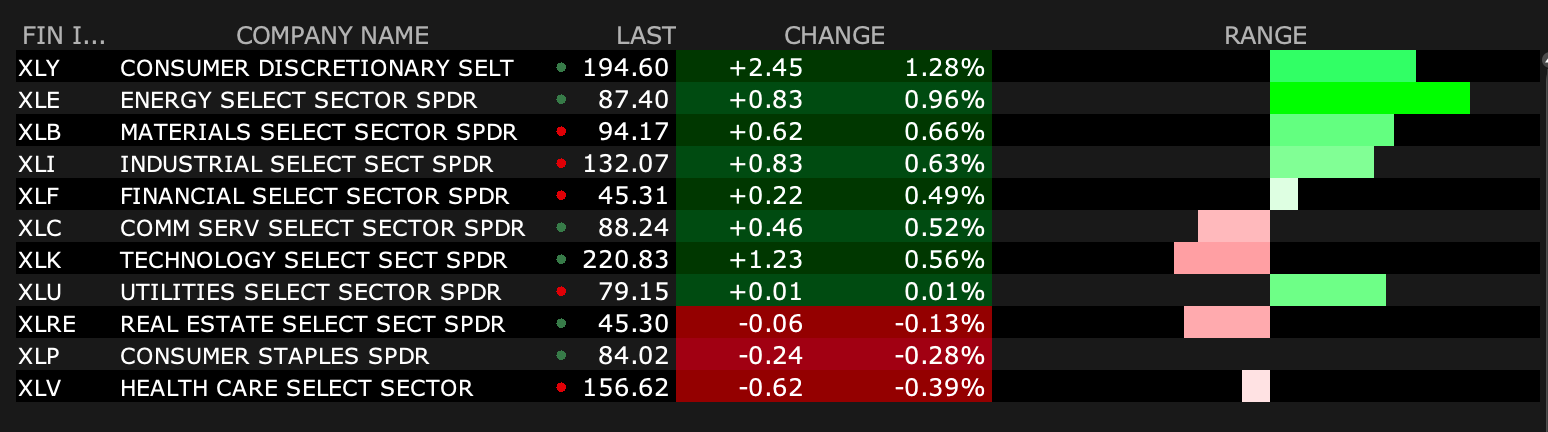

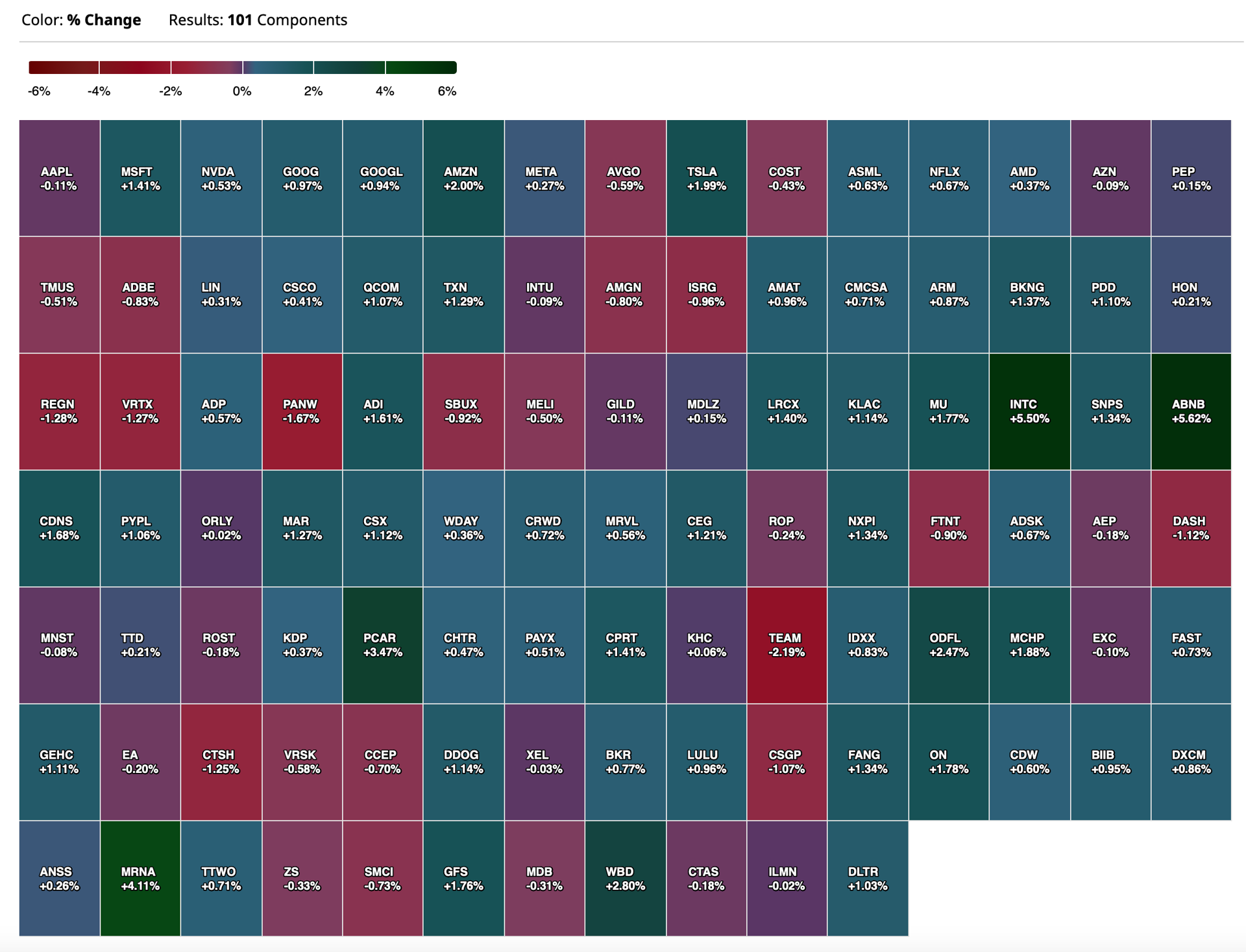

Breadth, S&P 500 Sector exchange-traded funds, and Nasdaq 100 heat map at 10:30 a.m. ET:

BY Doug Kass · Sep 17, 2024, 10:50 AM EDT

I have taken in half of my MSFT short at $436.90 for about a $4 gain since premarket.

BY Doug Kass · Sep 17, 2024, 10:24 AM EDT

Buying: GTBIF $10.50

Shorting: MSFT $441, SPY $565.10, QQQ $476.84, TOL $151.80, DHI $195.56, KKR $127.55, BX $155.85, XLU $79.22

BY Doug Kass · Sep 17, 2024, 10:00 AM EDT

From Peter Boockvar:

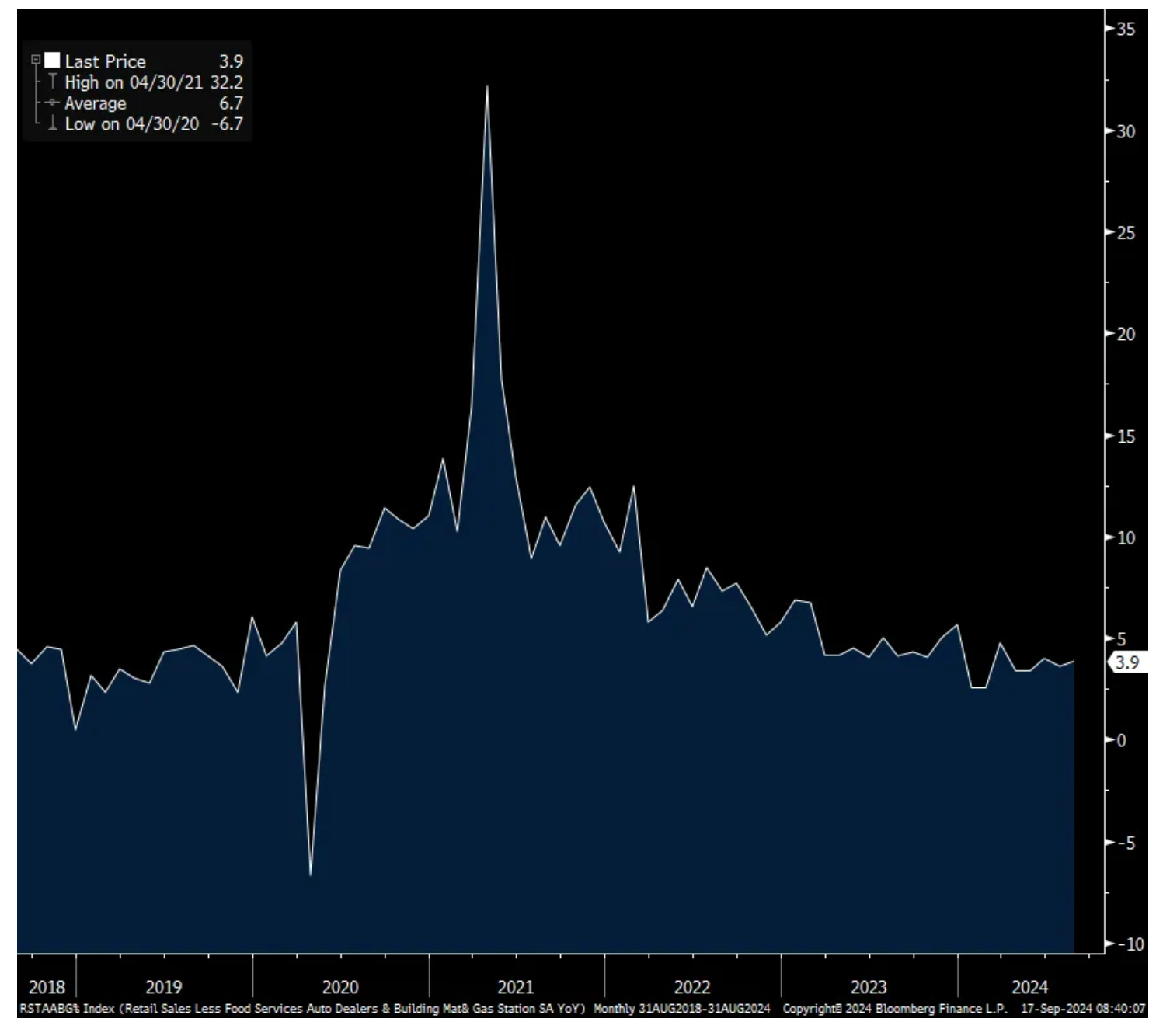

Core retail sales in August were about as expected when including a very slight upward revision to July. They rose .3% m/o/m after a .4% rise in the month before. They rose by 3.9% y/o/y in nominal terms.

The internals though were pretty mixed. Not included in the core, vehicle sales were basically flat m/o/m, down by one tenth following the June/July CDK software outage impact. Building materials were up .1% m/o/m but are down 2.2% y/o/y with the obvious challenges in housing. Within the core, sales were led by online retailing, up by 1.4% m/o/m and miscellaneous stores like pet, dollar and convenience but not much strength elsewhere. Sales fell for furniture, electronics, clothing, and department stores. They were also down for food/beverage after a jump in July. Sales were flat for restaurants/bars and rose by .3% for sporting goods but after a drop in July. Health/personal care sales continued with its steady gains.

Bottom line, under the hood to the inline data was a very mixed picture with where people are spending their money on. I’ve highlighted countless earnings comments from so many companies that touch the consumer directly, whether via consumer products and/or retailers that reflect this. As the numbers were about as forecasted, Treasury yields and the S&P futures didn’t really move much. Q3 GDP estimates shouldn’t change either.

Core Retail Sales growth y/o/y

BY Doug Kass · Sep 17, 2024, 10:00 AM EDT

From Peter Boockvar:

The August Cass Freight index came out yesterday and it reflected a 1% m/o/m rise in shipments after a 3% increase in July. They remain though down 1.9% y/o/y after a 1.1% fall in July. Cass said with regards to the y/o/y declines "These were the smallest declines in 18 months as goods demand continues to grow slowly, and slowing capacity additions reduce the pressure on for-hire shipments." My bottom line, some of this has been front loading shipments ahead of the holidays with the Red Sea disruptions.

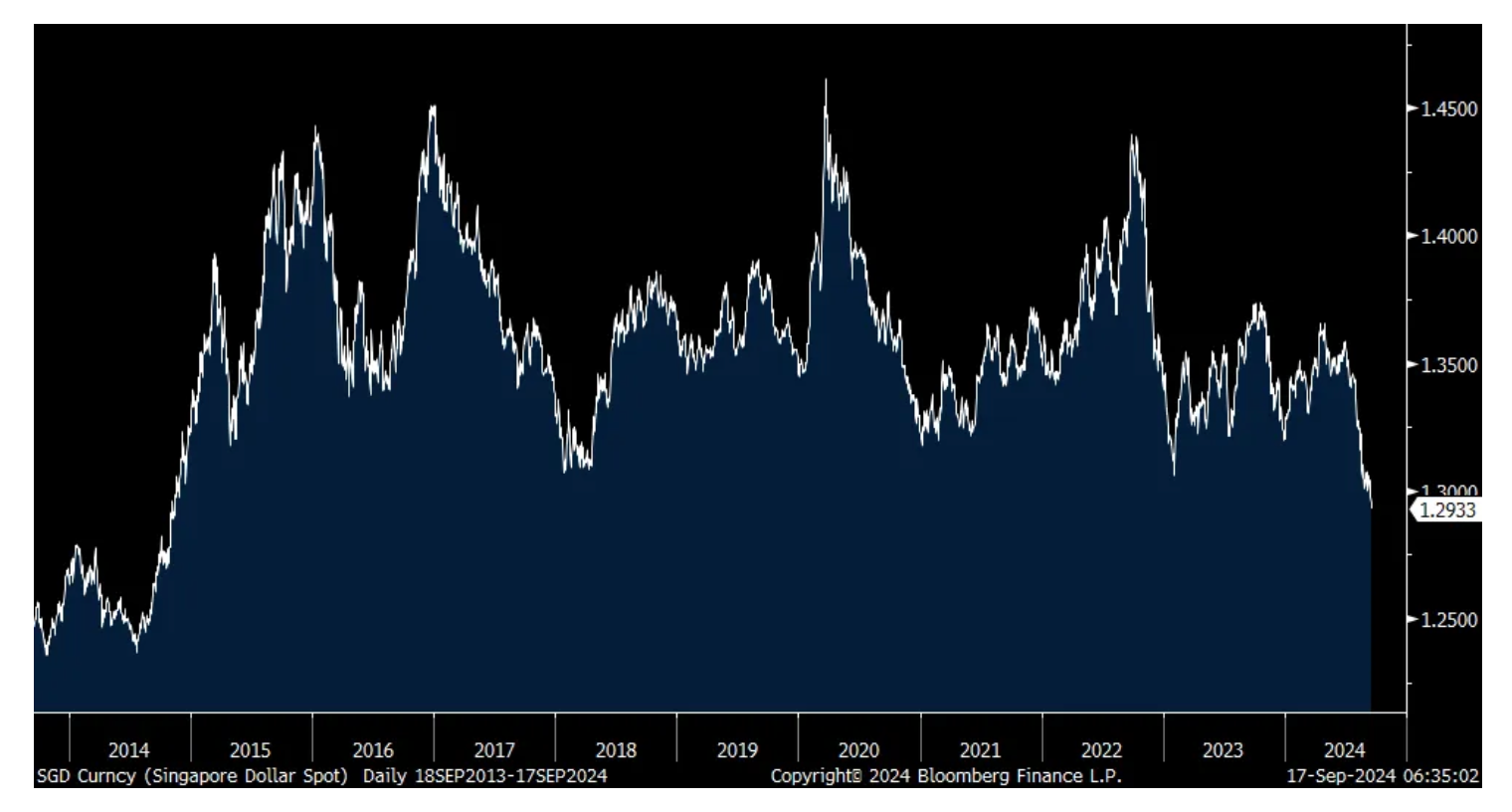

Non-oil exports from Singapore in August fell by 4.7% m/o/m after a strong 12.2% rise in July. The estimate was for a 2.7% fall. Versus last year though they are still up 10.7% with particular strength in electronic products. You may or may not know but Singapore has a big semi industry too. Taking out the influence of electronic products saw exports rise 3.7% y/o/y. Exports to China rose 19%, and were strong to other Southeast Asian countries like Indonesia and Malaysia. They were up 6.4% to the US but fell by 21% to the EU.

On their semi prowess, an article from June, https://www.reuters.com/breakingviews/tiny-singapores-chip-hub-retains-big-punch-2024-06-21/

I mentioned the Singapore dollar weeks ago as something to watch, along with the last few years mentioning that we are long stocks in Singapore and bullish on the city/state. Their currency today is trading at a fresh 10 yr high.

Singapore Dollar (down in chart is up vs US dollar)

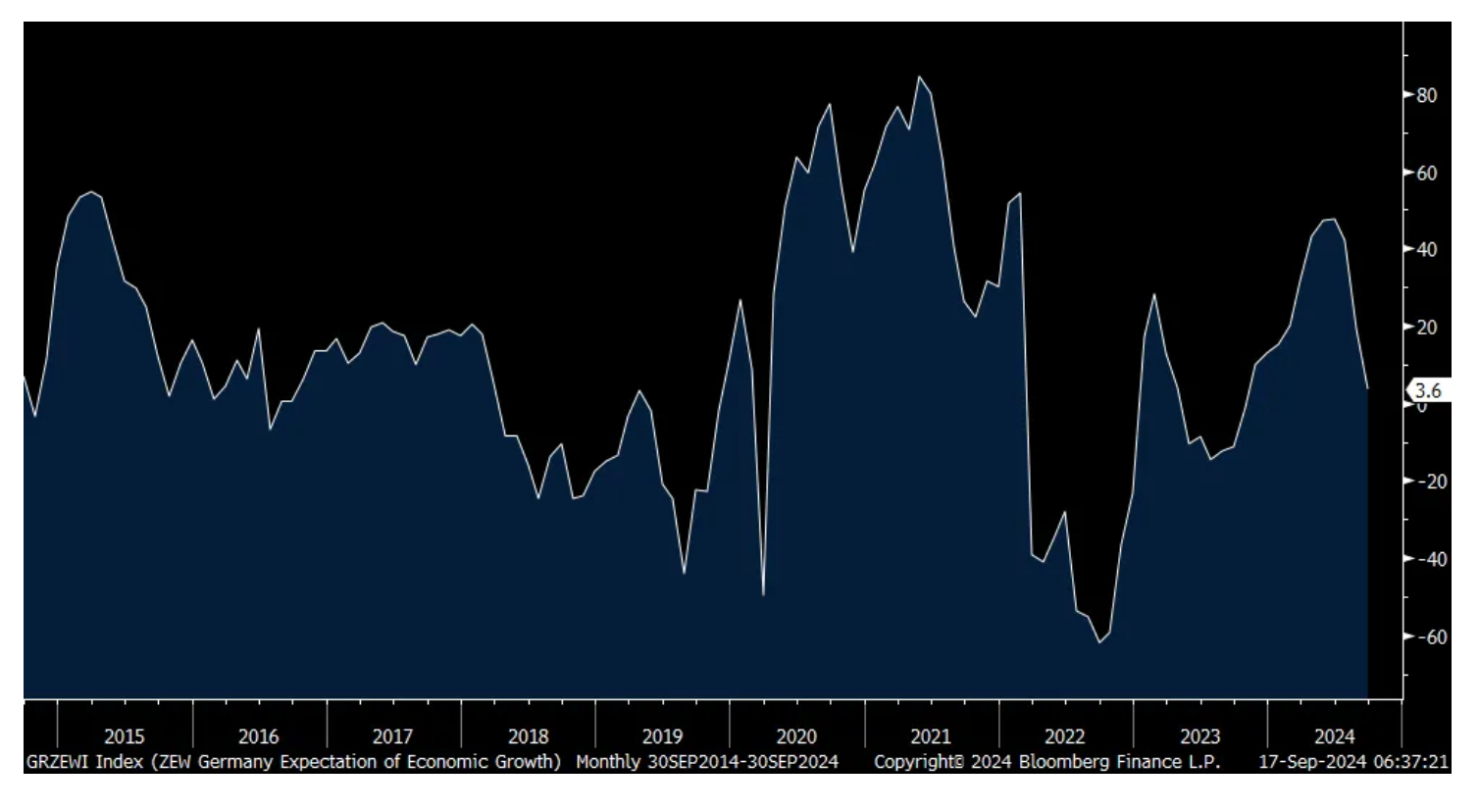

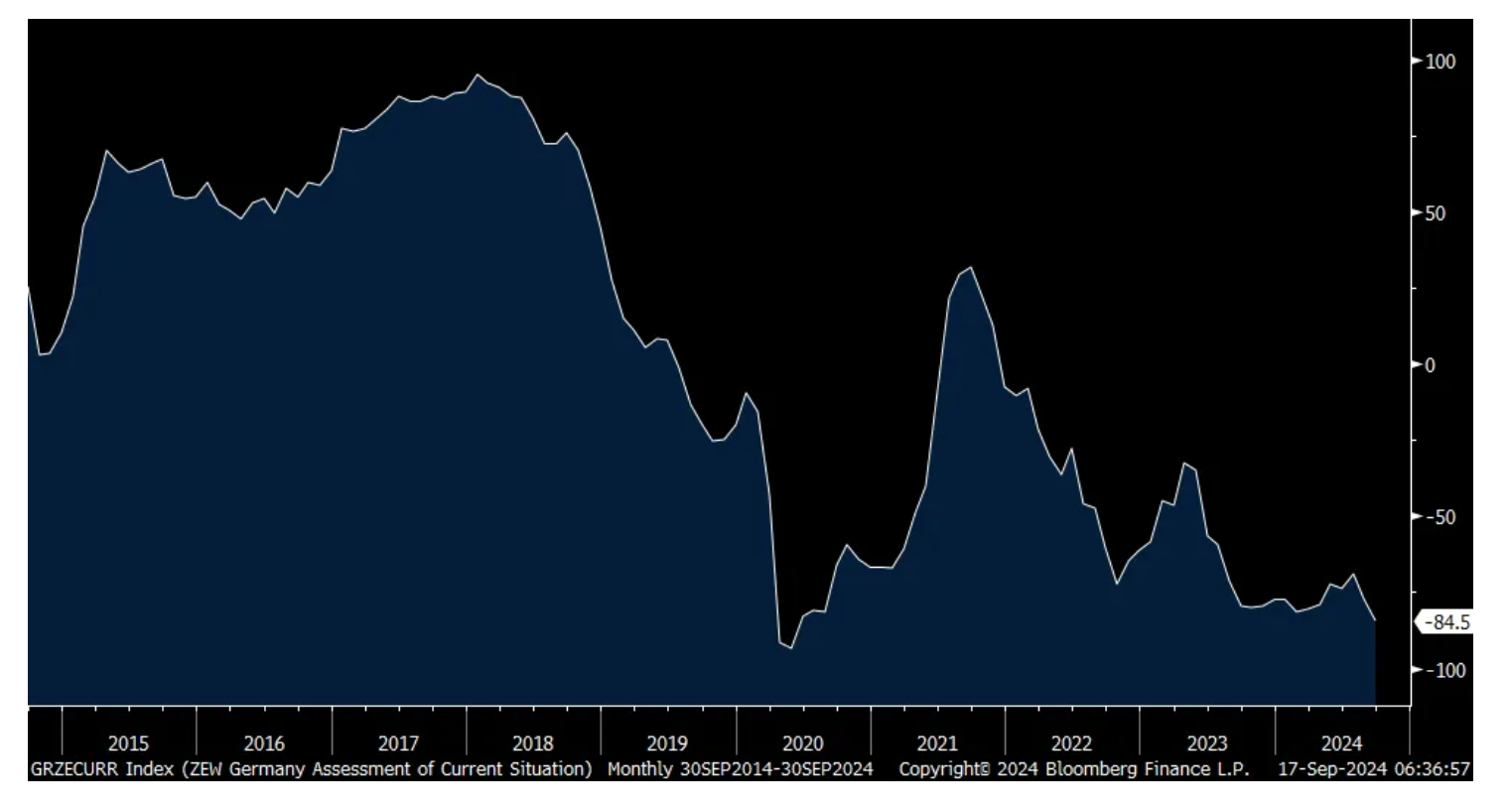

We know the economic sentiment on China is pretty dour but it is for Germany too. The September ZEW investor confidence index on the German economy fell to 3.6 from 19.2 and that was well under the estimate of 17. The Current Conditions component weakened to -84.5 from -77.3 and that is the worst since the Covid shutdowns. The ZEW said, "The optimism in economic expectations that has been evident since November 2023 has thus almost completely dwindled."

More, "The hope for a swift improvement in the economic situation is visibly fading. In the latest survey, we once again observe a noticeable decline in economic expectations for Germany." And this incorporates in investor minds the ECB rate cuts.

As the IFO is more relevant to markets, there is not much of a market response but it says a lot that the euro keeps rallying against the US dollar. It's just below the highest level since February 2022.

I'll argue again, there is something possibly else going on with this dollar weakness as other central banks, outside of the BoJ, are cutting rates too. We cannot shut out the possibility that US debts and deficits finally now matter, first reflected in the FX markets.

ZEW Expectations

ZEW Current Conditions

Euro

BY Doug Kass · Sep 17, 2024, 9:50 AM EDT

Energy stocks, led by OIH picking up a bid....

BY Doug Kass · Sep 17, 2024, 9:44 AM EDT

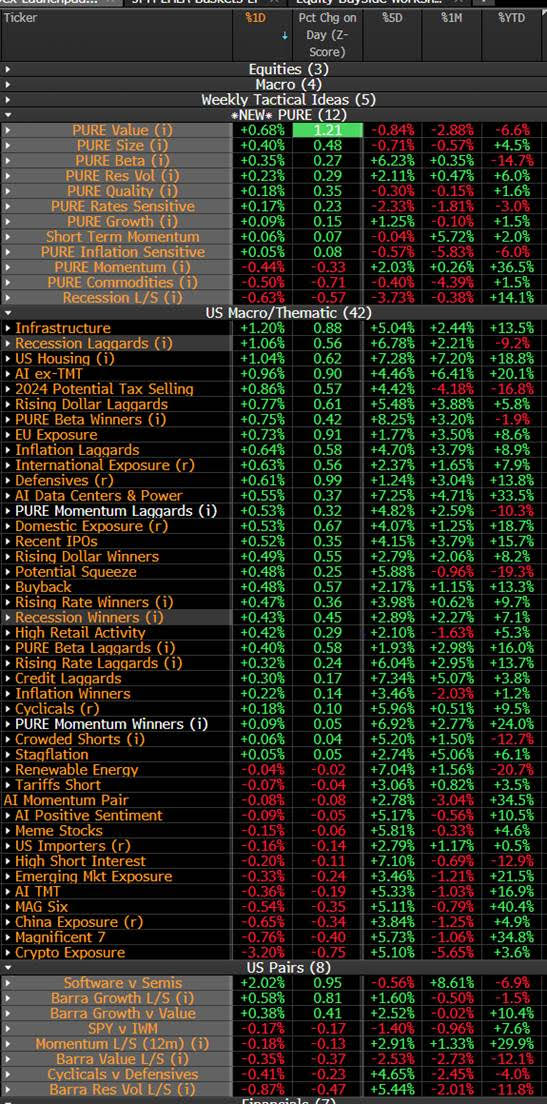

Themes and sectors table for traders:

BY Doug Kass · Sep 17, 2024, 9:35 AM EDT

From JP Morgan

· US: Futs are higher led by Tech; Mag7 and Semis are higher with INTC (+6.9%) the standout. MSFT +1.9% on dividend hike and buyback increase. Bond yields are lower 1bps from 5s – 30s ad T-Bills fall; USD remains under pressure. Cmdtys are mixed: crude down, natgas up, precious down, base up, and Ags higher. Retail Sales is the primary focus for today, but we also receive updates on Industrial Production, Inventories, and home prices.

and...

EQUITY AND MACRO NARRATIVE: Yesterday was relatively quiet as investors await the start of catalytic macro data. We saw a resumption of some trends from last week, including (i) broadening of the rally ex-TMT with ~76% of SPX higher on the day; (ii) rotation within TMT from Semis into Software; (iii) a broadening of the AI theme beyond TMT as our AI ex-TMT basket outperformed our AT TMT basket by 132bps; and (iv) early session selling reversing higher after the EU close. Separately, disappointment of AAPL’s new iPhone release weighed on the Mag7.

BY Doug Kass · Sep 17, 2024, 9:25 AM EDT

-VVPR +55% (announces strategic merger heads of agreement with FAST at a pro-forma combined equity value of $1.13B)

-SES +33% (collaborates with NVIDIA, Crusoe, and Supermicro on AI for science initiative to accelerate material discovery in Electric Transportation)

-HOTH +17% (presents 'promising' preclinical results for Alzheimer's Drug HT-ALZ)

-VNCE +9.7% (earnings)

-TALK +9.4% (partners with Amazon Health Services to further mental health benefits)

-INSG +8.0% (announces sale of Telematics Business for $52M cash; affirms Q3 guidance)

-MBOT +6.9% (successfully enrolls 50% of patients in Pivotal Human Clinical Trial for LIBERTY Endovascular Robotic Surgical System)

-INTC +6.7% (Intel and AWS expand strategic collaboration)

-TDOC +6.6% (recent notable strength being attributed to Jefferies note highlighting return to growth for Teladoc’s BetterHelp segment)

-INOD +6.1% (Craig-Hallum Initiates INOD with Buy, price target: $23)

-CURV +5.8% (William Blair Raised CURV to Outperform from Market Perform)

-MBLY +5.8% (reportedly one thing that is not on the Intel table is a sale of Intel’s stake in Mobileye)

-ACIU +5.5% (receives second milestone payment of CHF24.6M from Janssen following progress in Phase 2b ReTain Trial of ACI-35.030 in Preclinical Alzheimer’s Disease)

-VIGL +4.5% (US FDA removed Partial Clinical Hold on VG-3927)

-BOOM +4.4% (Steel Connect issues statement reiterating $16.50/shr offer)

-WBX +4.0% (files to sell up to 49.8M shares on behalf of holders)

-HPE +3.8% (Tier1 firm Raised HPE to Buy from Neutral, price target: $24 from $21)

-SENS +3.7% (Eversense 365 cleared in US as a continuous glucose monitoring (CGM) system for Type 1 and Type 2 diabetes)

-AISP +3.4% (wins Multiple Awards for State and Local Law Enforcement Acropolis Enterprise Video and Data Management Platform Deployments)

-SHOP +3.1% (Redburn Atlantic Raised SHOP to Buy from Hold, price target: $99)

-CMP +2.9% (prelim earnings, guidance)

-DDD +2.9% (receives FDA Clearance for First-to-Market Multi-material, Monolithic Jetted Denture Solution)

-DELL +2.6% (Mizuho Securities Initiates DELL with Outperform, price target: $135)

-GEV +2.6% (Tier1 firm Raised GEV to Buy from Neutral, price target: $300 from $200)

-MSTR +2.4% (files to sell private offering of $700M of Convertible Senior Notes)

-PSNY +2.2% (fully compliant with Nasdaq listing rules; ramps up deliveries of its two performance SUVs)

-MSFT +2.1% (raises dividend, announces new $60B share buyback program)

-SEDG -5.5% (Jefferies Cuts SEDG to Underperform from Hold, price target: $17 from $27)

-CI -4.9% (Express Scripts confirms to sue FTC, seeking order to force agency to withdraw drug pricing report)

-NUE -2.1% (Q3 guidance)

-VSAT -2.1% (JPMorgan Chase and Co Cuts VSAT to Neutral from Overweight, price target: $15 from $29)

BY Doug Kass · Sep 17, 2024, 9:20 AM EDT

Chart from 8:40 a.m. ET:

BY Doug Kass · Sep 17, 2024, 9:16 AM EDT

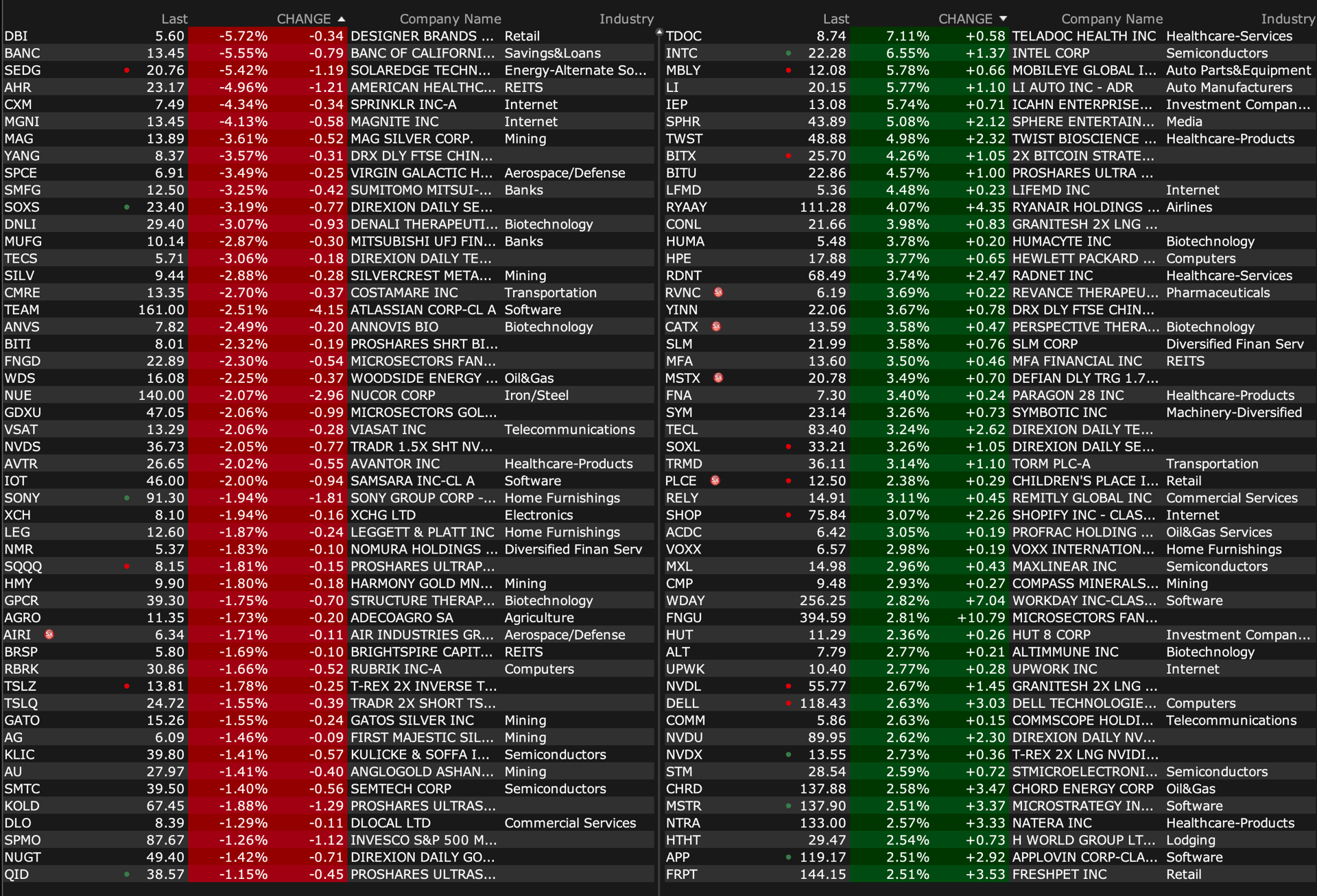

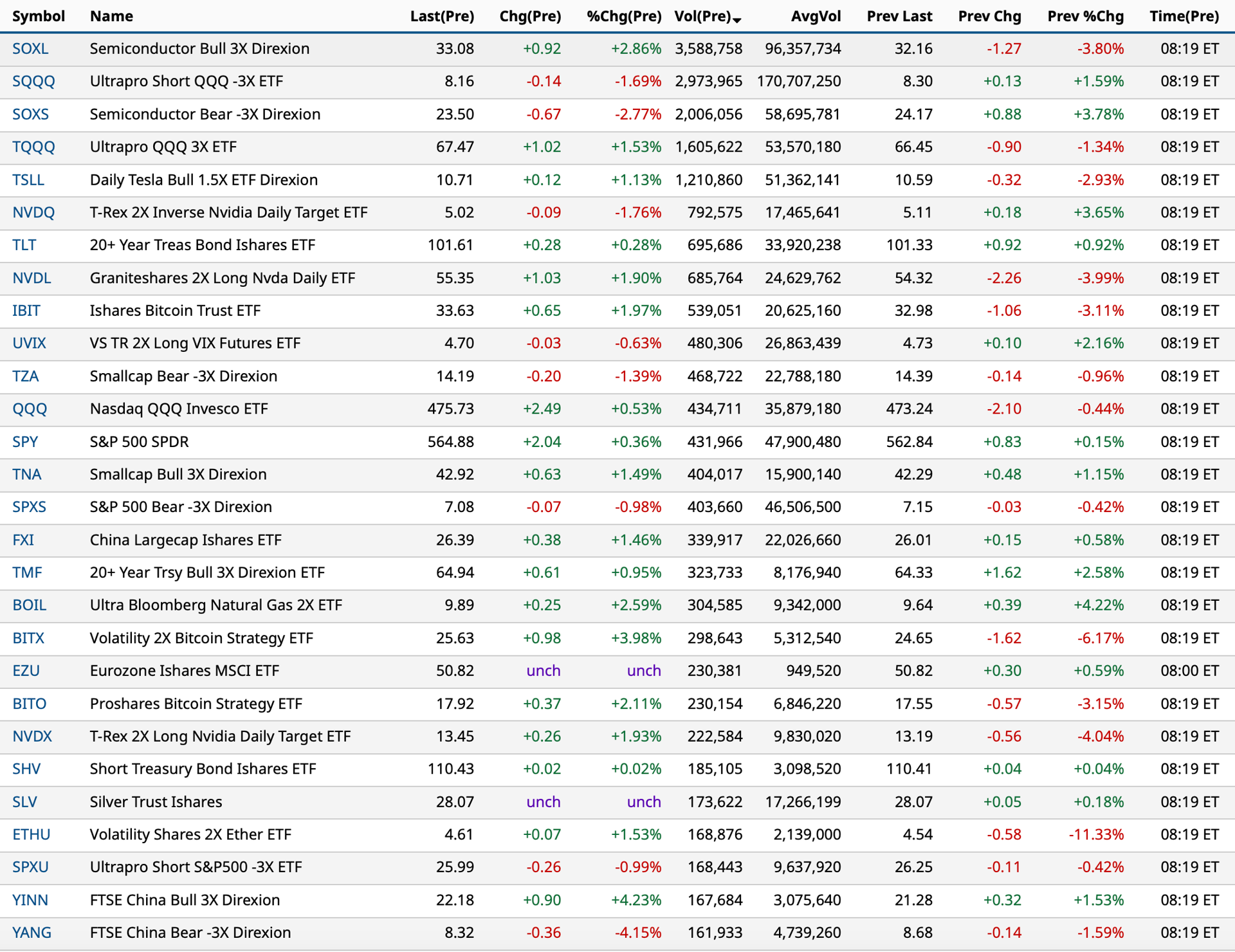

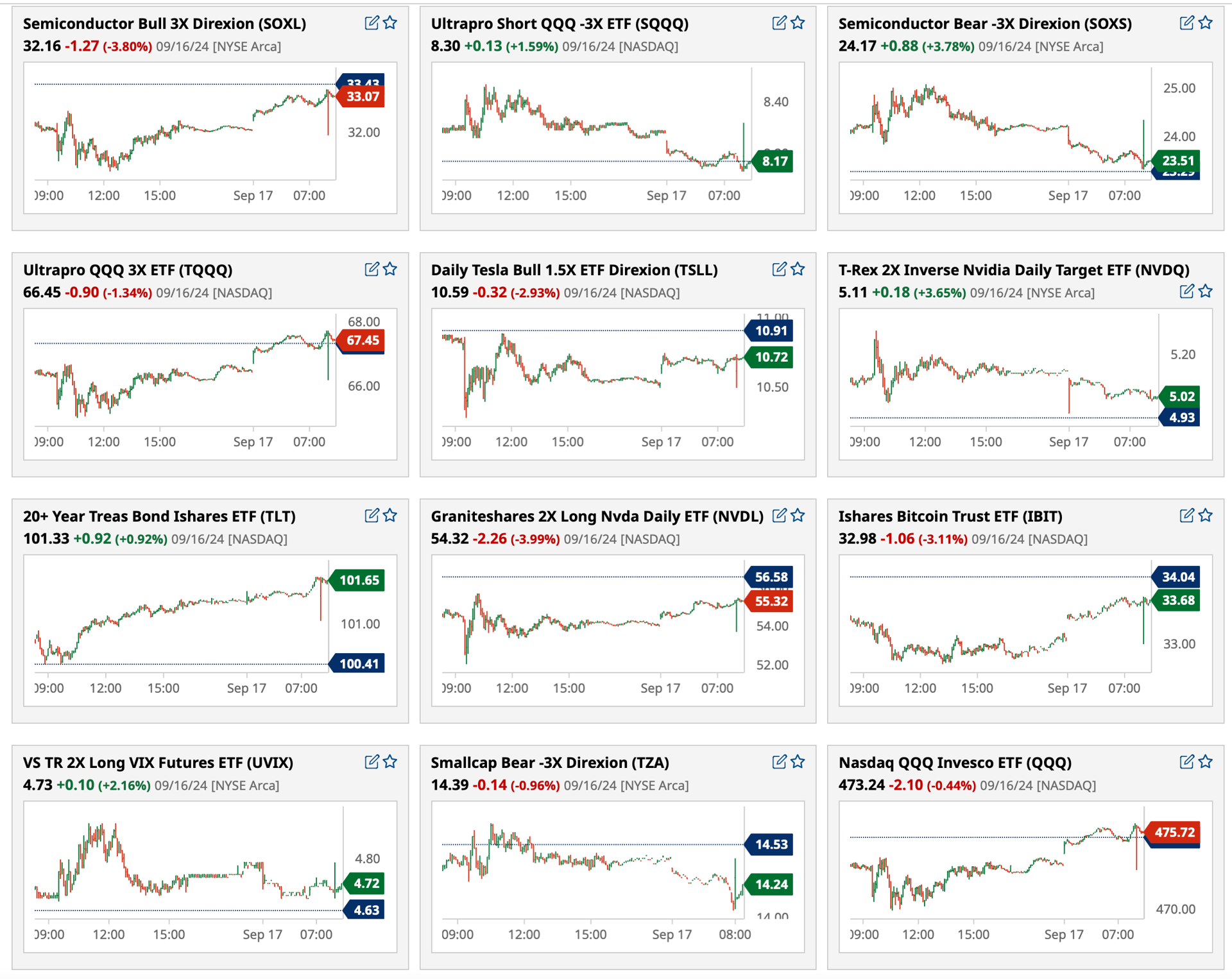

Chart from 8:19 a.m. includes mini-graphs as of this morning below:

BY Doug Kass · Sep 17, 2024, 9:07 AM EDT

President Biden gave the cannabis industry a rare mention during his speech at the 2024 CBCF Phoenix Awards Dinner, acknowledging his administration’s efforts in shaping cannabis policy. It was a breath of fresh air to hear him touch on this evolving sector, but as Dan Ahrens astutely pointed out on TTB yesterday, sometimes "silence is golden." With an upcoming Administrative Law Judge (ALJ) hearing on the horizon, it might be best to keep expectations in check until the regulatory dust settles.

I am growing more optimistic with regard to cannabis equities.

I expect Amendment 3 to pass in Florida (allowing for recreational use) and for the ALJ hearing to clear rescheduling.

I add daily.

BY Doug Kass · Sep 17, 2024, 8:59 AM EDT

* As AI delay cools demand...

From The South China Morning Post:

E-commerce platforms are offering price cuts of up to 11% on Apple's latest smartphones, as Huawei steals the market buzz

Online retailers in China have slashed the prices of Apple's new iPhone 16 series ahead of its official release, as consumers in the world's largest smartphone market hold out for the release of the US company's first on-device artificial intelligence (AI) software.

PDD Holdings' Pinduoduo, one of the country's most popular e-commerce platforms, has started selling the iPhone 16 Plus with 512 gigabytes of storage for 8,999 yuan (US$1,268), a 10 per cent discount from the official price of 9,999 yuan. The 128GB iPhone 16 is being sold at an even steeper 11 per cent discount.

You can read the entire story here but some key points include:

BY Doug Kass · Sep 17, 2024, 8:53 AM EDT

BY Doug Kass · Sep 17, 2024, 8:45 AM EDT

* Market expectations and monetary policy narratives are inconsistent.

* I call BS to more "cowbell."

Many market participants are begging for more easing tomorrow (50 basis points from a number of economists and 75 basis points from Senator Elizabeth Warren):

But some of the conditions (like elevated asset prices and others below) that exist argue for less ease:

Regardless, as noted by the GOAT (in his quote at the beginning of this column), Stan Druckenmiller, the Wall Street narratives (as they relate to anticipated/desired monetary policy) are terribly inconsistent and asymmetric.

Stop begging.

BY Doug Kass · Sep 17, 2024, 8:00 AM EDT

* MSFT is trading +$8/share on the buyback and dividend news.

* I would argue that this reaction is plain silly.

* Higher stock prices are the enemy of the rational investor.

Just like with Nvidia NVDA, the buybacks and dividend increases at Microsoft MSFT do not move the needle.

These announcements are aimed at retail and algos (that probably use AI and therefore cannot do math and understand this is meaningless). If good things were happening, these companies would not have to resort to these games:

Subject: (TIF) Microsoft Raises Dividend 10%, Plans $60 Billion Share Buyback

$60 billion on a $3.2+ trillion market cap. This is about two percent of the outstanding shares. Moreover, the last buyback of $60 billion from 2021 was not completed.

10% dividend hike — on a base of a 0.77% yield!

Importantly, when we combine them (aka buyback and dividend) and not 3% and that’s before all the stock options, which probably means they are not even retiring shares anymore...

Microsoft Raises Dividend 10%, Plans $60 Billion Share Buyback

Aaron Holmes

(The Information)

Source: The Information

Microsoft will raise the quarterly dividend that it pays investors to 83 cents a share, up from 75 cents, beginning in November, the company said late Monday. The software maker will also buy back $60 billion in stock, replacing its previous $60 billion stock buyback that the company initiated in 2021 that had almost run out. Shares rose by roughly half a percentage point on Monday evening after the company’s announcements.

Microsoft is returning cash to shareholders as they await a return on the company’s unprecedented spending on AI in recent years. Microsoft has invested.

$13 billion in OpenAI in exchange for the rights to reuse its software and a share of its profits, and projected that it will spend more than $50 billion in capital expenditures this year to build out datacenters to power AI applications.

Meanwhile, Microsoft has been generating revenue from OpenAI’s use of Azure servers, The Information previously reported, but has told investors to hold out for an AI-driven bump to software sales as customers hold back on spending heavily on Microsoft’s AI-infused applications.

BY Doug Kass · Sep 17, 2024, 7:17 AM EDT

* Targeted trading rental shorts (though small) in MSFT, SPY and QQQ...

With the S&P Index virtually at an all-time high (and with futures gapping higher at the get go) I am adding to my small Index shorts in the premarket:

* Shorted more SPY $564.91.

* Shorted more QQQ $475.96.

I also initiated a trading short rental in Microsoft MSFT (for an explanation see my next column on the company):

* Shorted MSFT $440.28.

BY Doug Kass · Sep 17, 2024, 6:59 AM EDT

BY Doug Kass · Sep 17, 2024, 6:45 AM EDT

The Short Range S&P Oscillator rose to 3.26% from 1.95%. We are now in a deeper overbought.

BY Doug Kass · Sep 17, 2024, 6:31 AM EDT

Wolf Street howls about the curious activity in used cars.

BY Doug Kass · Sep 17, 2024, 5:50 AM EDT