Boockvar: 10 Year Note Auction Mixed to the Soft Side

From Peter:

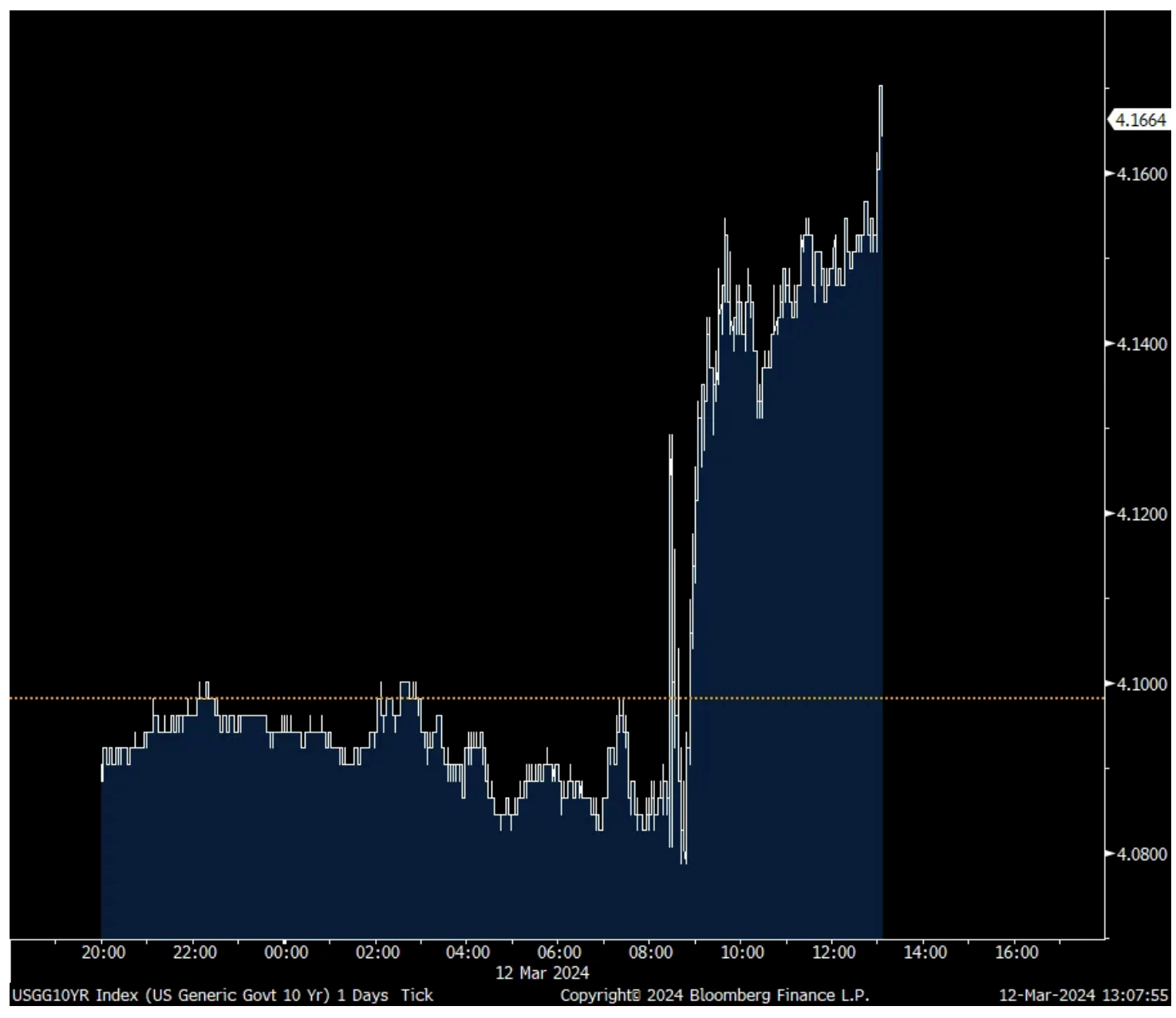

The 10 yr note auction was a mixed bag. The auction tailed about 1 bp with a yield of 4.166% and vs the when issued of 4.157% and dealers were left with 17% of the auction, slightly above the one yr average of 15% but the bid to cover of 2.51 was just above the 12 month average of 2.48, though a 4 month low.

Bottom line, after the CPI was fully digested, yields have been slowly rising all day and are now at the highs of the day post mediocre auction. Also post CPI, inflation breakevens across the yield curve are up about 3 bps. I still think 10 yr yields will retest 5% at some point latter this year.

Earlier today I highlighted the weakness in bond prices as stocks advanced:

Bond Market Update

Like the hit in bond prices and rise in yields yesterday from the morning lows, bond prices are resuming their decline and interest rates are again rising:

* The yield on the 2 year US note is+5 bps to 4.58%.

* The yield on the 10 year US note is +4 bps to 4.14%.

* The yield on the long bond is +3 bps to 4.31%.

This should be market unfriendly, but for now the momentum dictates prices.

But as you can see from my premarket trading (shorting), I am raising my short profile.

With the S&P Index (cash) rising almost 25 handles from the lows and +20 on the day -- in only a few minutes -- I have added to my SPY and QQQ short call positions.

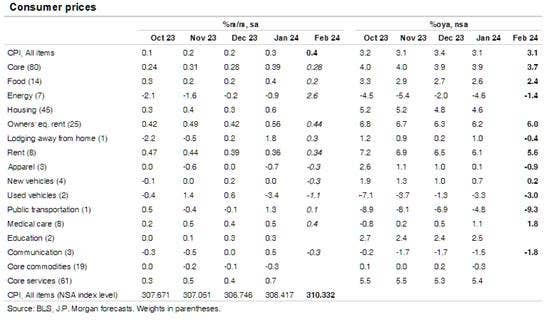

February CPI rose .4% both headline and core with the former in line with expectations while the latter was one tenth above. Versus last year, prices rose 3.2% headline and 3.8% core vs 3.1% and 3.9% respectively. Energy prices rebounded by 2.3% m/o/m though still lower by 1.9% y/o/y, driven by gasoline prices, no pun intended.

Food at home prices were unchanged m/o/m and up by 1% y/o/y but eating out is still running hotter. A full service meal price was higher by one tenth m/o/m and by 3.8% y/o/y while the quicker service also saw a one tenth increase after .6% in the month before and up by 5.2% y/o/y.

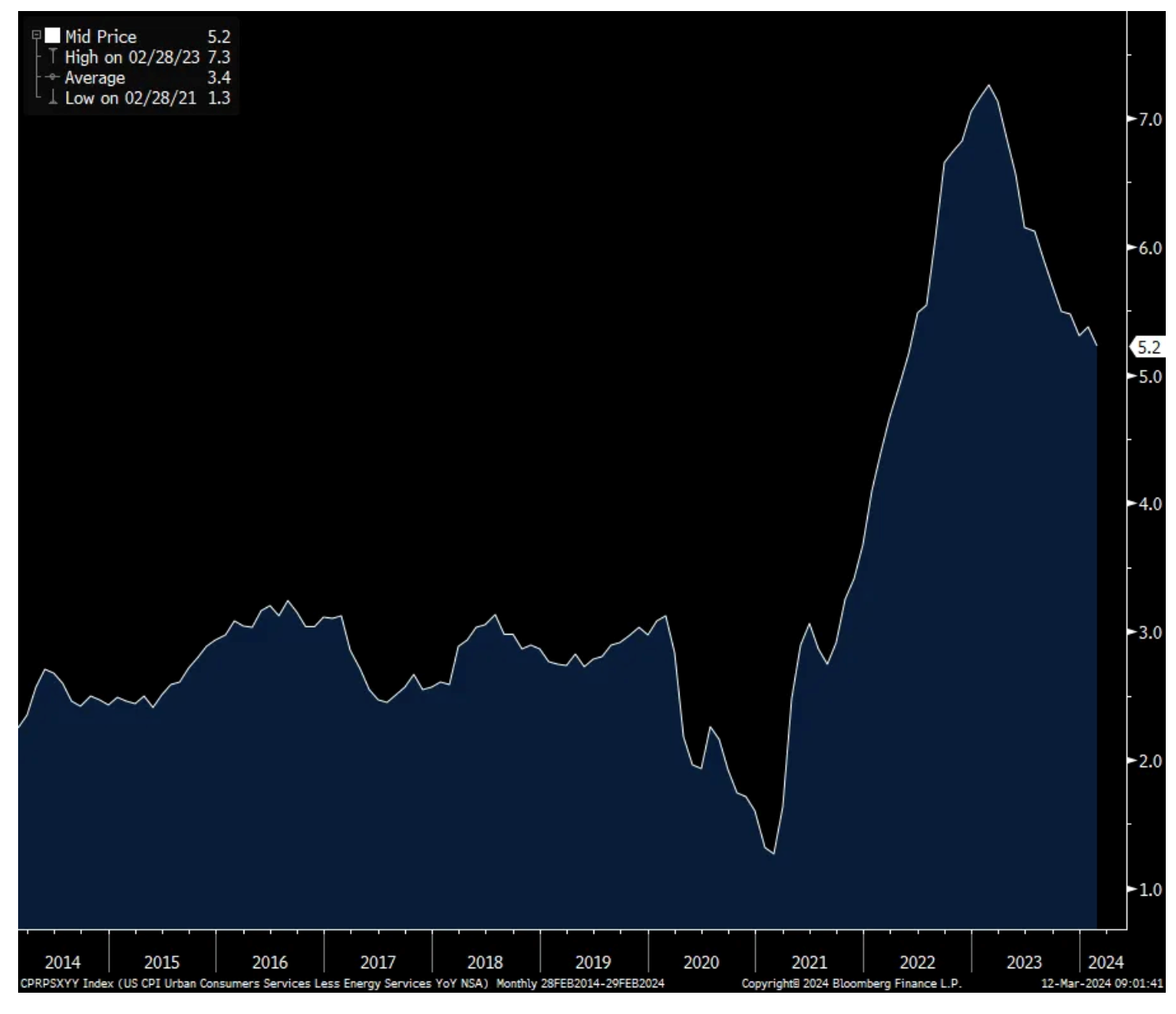

Services inflation ex energy rose .5% m/o/m and 5.2% y/o/y with again housing leading the way with respect to the rental calculation. OER was up by .4% m/o/m and 6% y/o/y. Rent of Primary Residence was higher by .5% m/o/m and 5.8% and does include a slightly raised allocation to single home rentals which have been running above apartments. As with apartments, we know the current blended rate is running lighter than these calculations but CPI will eventually catch up on a very lagged basis.

Medical care costs were unchanged m/o/m which kept a lid on core prices after they rose by .5% in the month before. They are higher by 1.4% y/o/y. Health insurance prices after a string of 1%+ monthly gains were up by .4% m/o/m. Auto insurance prices continue to skyrocket, rising another .9% m/o/m and 20.6% y/o/y. The cost of maintenance/repair prices remained robust too, up by .4% m/o/m and 6.7% y/o/y. Airline fares jumped by 3.6% m/o/m but still lower by 6.1% y/o/y. Hotel prices were little changed after the 2.4% jump last month but are down .9% y/o/y.

By the way, for those who want to further slice and dice, core service prices ex housing were up by .5% m/o/m and 4.3% y/o/y, still far from 2%.

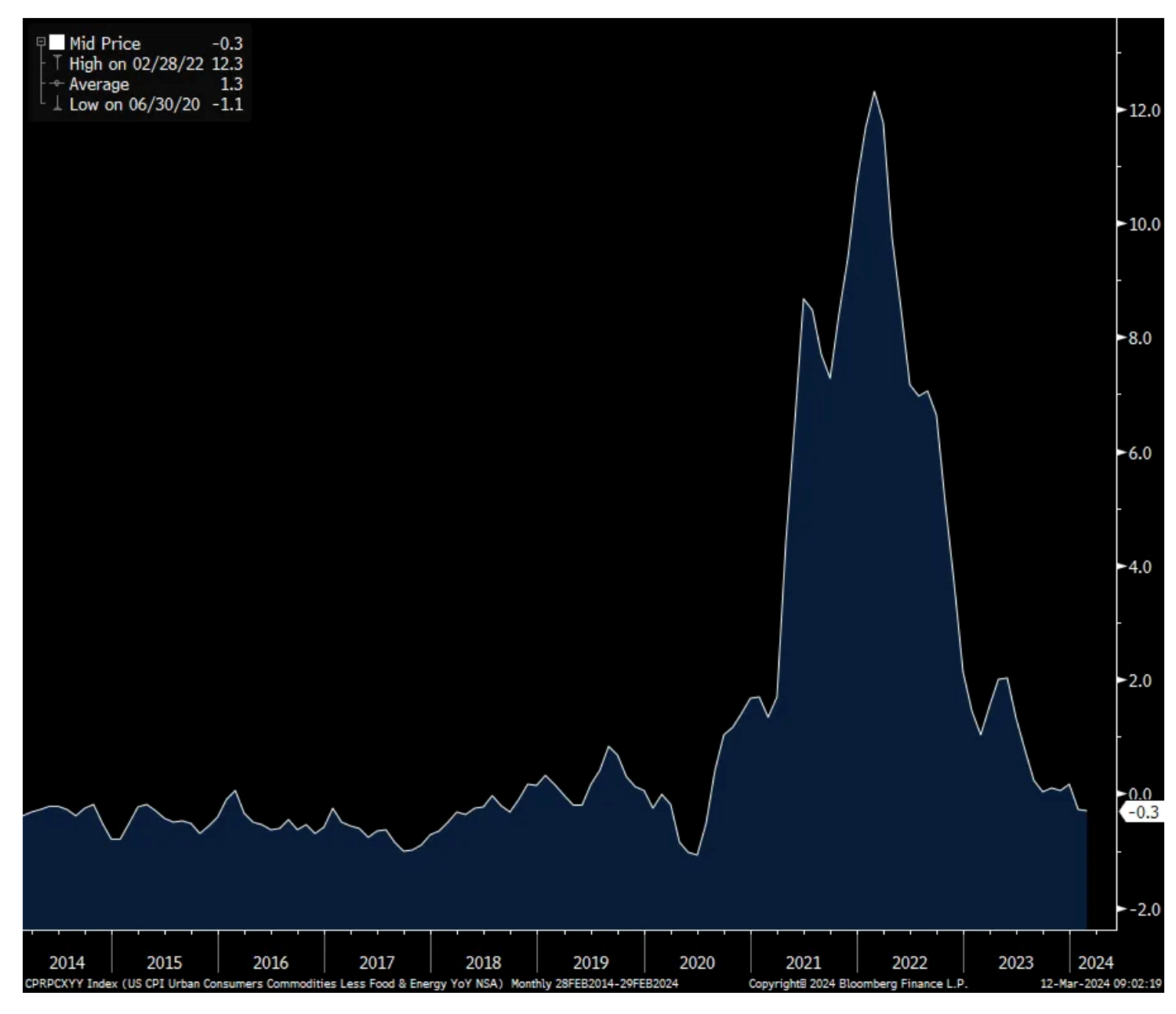

On the goods side, core prices were up .1% m/o/m after 3 months of declines and are lower by .3% y/o/y. Again, the 20 yr trend leading into covid for core goods prices was zero so we’re back to trend. The question though is whether we stay here or not. Used car prices rose .5% m/o/m after a 3.4% drop in January and they are lower by 1.8% y/o/y.

I expect prices to stabilize this year relative to the pullback seen last year because of the slowing pace of new used car supply. New car prices were little changed both m/o/m and y/o/y. Pricing related to the home fell .3% m/o/m and 2.3% y/o/y. Apparel prices were up by .6% m/o/m but after dropping by .7% last month. They are flat y/o/y.

Bottom line, we still have a runway of deceleration ahead in core service prices because of slower rent growth but that is a slow process and has other offsets within services, particularly on the insurance side and how companies are still managing higher labor costs.

On the goods side, as stated we are back to the pre Covid trend of zero but I don’t think we stay here as the pullback in used car prices won’t be repeated, transportation costs have risen and a restocking of some sort is just ahead. I’ll add, higher energy prices as something huge to watch too along with other industrial material prices which have risen of late as seen in the CRB raw industrial index.

I’ll add this, for all the talk of rate cuts and Jay Powell himself saying they don’t need to wait until inflation gets back to 2% to start cutting, it’s amazing to me how everyone has forgotten the lessons of the 1970’s. As inflation fell notably then, the Fed got complacent and inflation spiked anew.

You’ll also hear today people taking out this and that with inflation in order to get to one’s preferred low inflation rate but either way, nothing here changes the likely reality of 1-3 rate cuts this year so as to provide a range. The fed funds futures are still pricing in about 3. After initial falling in response to the about in line data, the 2 yr and 10 yr yields are right back to where they were before the print at 4.55% and 4.11%. The 2 yr inflation breakeven is down by 2 bps, but still near one yr highs while the 5 yr is little changed.

Like the hit in bond prices and rise in yields yesterday from the morning lows, bond prices are resuming their decline this morning and interest rates are again rising:

* The yield on the 2 year US note is+5 bps to 4.58%.

* The yield on the 10 year US note is +4 bps to 4.14%.

* The yield on the long bond is +3 bps to 4.31%.

This SHOULD BE market unfriendly but, for now the momentum dictates prices.

But as you can see from my premarket trading (shorting), I am raising my short profile.

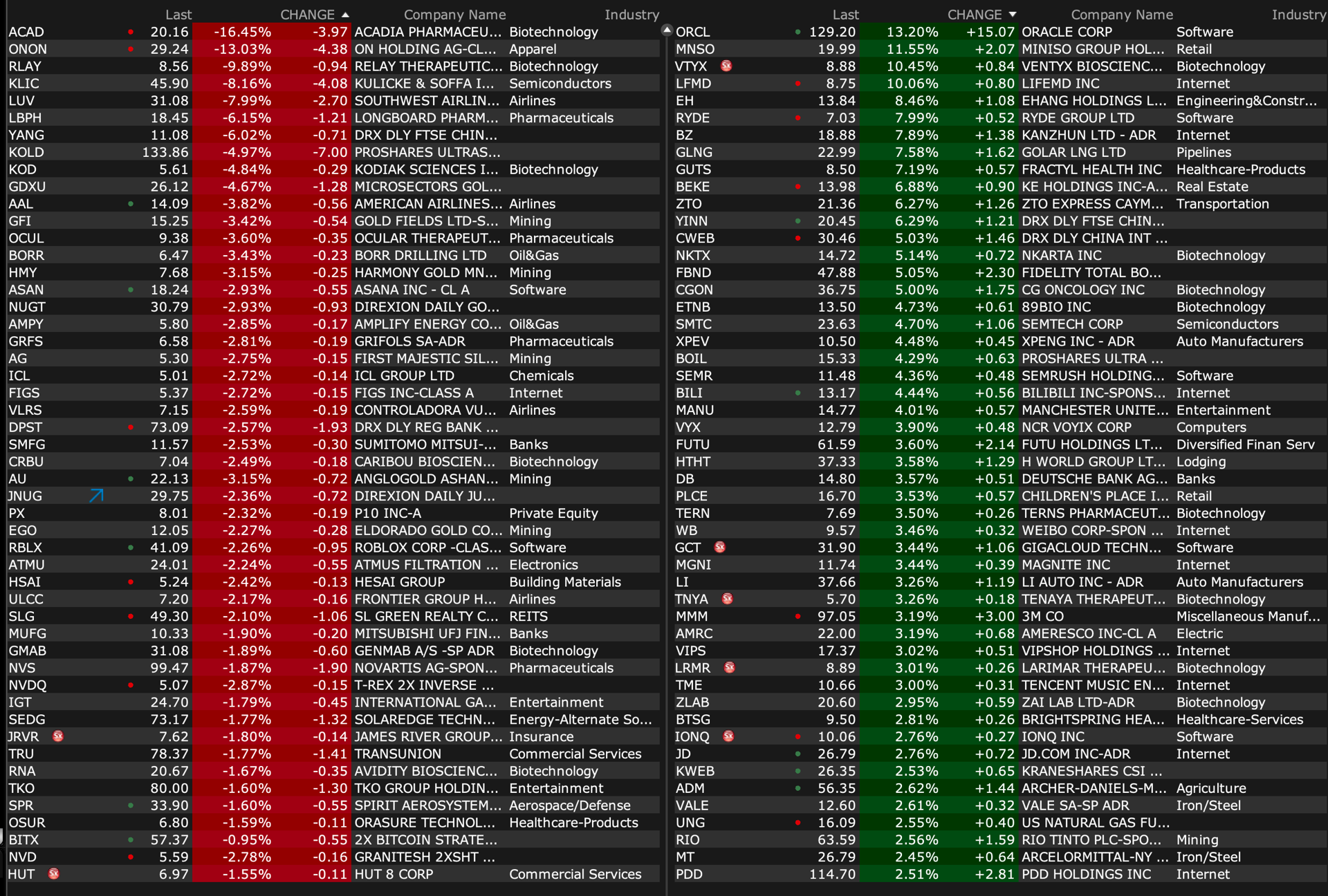

-RGLS +55% (positive topline data from second cohort of patients in phase 1B multiple-ascending dose (MAD) clinical trial of RGLS8429 for treatment of Autosomal Dominant Polycystic Kidney Disease (ADPKD)) -MDAI+30% (announces new US government contract to accelerate the development of the handheld version of DeepView Wound Imaging System) -SPRC +21% (MitoCareX reveals promising results with discovery of novel anti-cancer small molecule structure) -ORCL +13% (earnings, guidance) -BZ +7.4% (earnings, guidance) -ETNB +4.7% (initiates Phase 3 ENLIGHTEN-Fibrosis Trial of Pegozafermin in Non-Cirrhotic Metabolic Dysfunction-Associated Steatohepatitis (MASH) patients with Fibrosis) -MMM +4.5% (former L3Harris's CEO William Brown appointed as new CEO, Michael Roman appointed 3M Executive Chairman; Effective May 1, 2024) -ADM +3.3% (earnings, guidance; add $2B to share buyback; to take $137M charge related to animal nutrition unit, cooperating with BOJ) -CRBP +3.2% (earnings) -CMT +3.0% (earnings, guidance)

Downside

-NRXP -18% (initiates strategy to combat naked short sales; contemplates reverse stock split) -ONON-11% (earnings, guidance) -LUV -7.5% (earnings, guidance) -NOTE -5.9% (earnings, guidance; sells Board.Org community engagement platform for up to $103M) -MTN -4.3% (earnings, guidance; raises dividend) -AAL -3.8% (adjusts guidance)

We enter today's CPI figure, the headline of the week, with rate cut odds of 62% for June but if they don't in June, it's 100%+ for July. As for combining the next two meetings after March, we're pricing in a 46% chance of a 2nd in July if they go in June. By yr end we're still pricing in about 3. So, I know today's figure is going to shift these numbers around, stocks will have their thing in response, but won't change the likelihood of 1-3 cuts this year that have been fully priced in.

Therefore, I continue to emphasize that at this point, the fate of the balance sheet should be the biggest priority of focus and which we'll get more clues next week as the Fed discusses it at the table. I keep mentioning the balance sheet because we're nearing a point where QT starts to exceed the reduction in the Fed's reverse repo facility and liquidity starts to drain as a result. With regards to asset prices, that is more relevant now than whether the Fed cuts once, twice, three times or not at all this year off a 5.33% effective fed funds rate.

While there was no change in the one yr inflation outlook at 3% in the updated Consumer Expectations Survey from the NY Fed, the 3 yr and 5 yr guesses rose to 2.7% and 2.9% from 2.4% and 2.5% respectively. Expectations for another 3% annual rise in home prices remained the same. They ticked up for gasoline but fell for medical care, rent, and college and were unchanged for food prices at 4.9%.

With the unemployment rate at a 2 yr high as seen in the BLS report, the answers to the labor market were mixed. There was a drop to a 2 yr low in expectations for a lift in the unemployment rate but a higher expectation for the loss of one's job in the coming 12 months. And if one's job is lost, the mean probability of finding a new job fell to 52.5% from 54.2%. Income expectations were unchanged while spending expectations rose a touch.

Of note, "Perceptions of credit access compared to a year ago deteriorated with a larger share of respondents reporting tighter conditions and a smaller share reporting looser conditions compared to a year ago. Expectations about credit access a year from now also deteriorated with a smaller share of respondents expecting looser credit conditions and a larger share of respondents expecting tighter credit conditions a year from now."

Bottom line, to add all the retail comments we've heard over the past few weeks, the higher end consumer is of course spending more freely than the lower end. The higher end is focused still on traveling, eating out, and other experiences while the lower end is much more 'choiceful', focused on value and promotions and sticking within a tight budget. Spending on services is the priority over stuff, and for many, needs not wants. And, the labor market tightness continues to loosen.

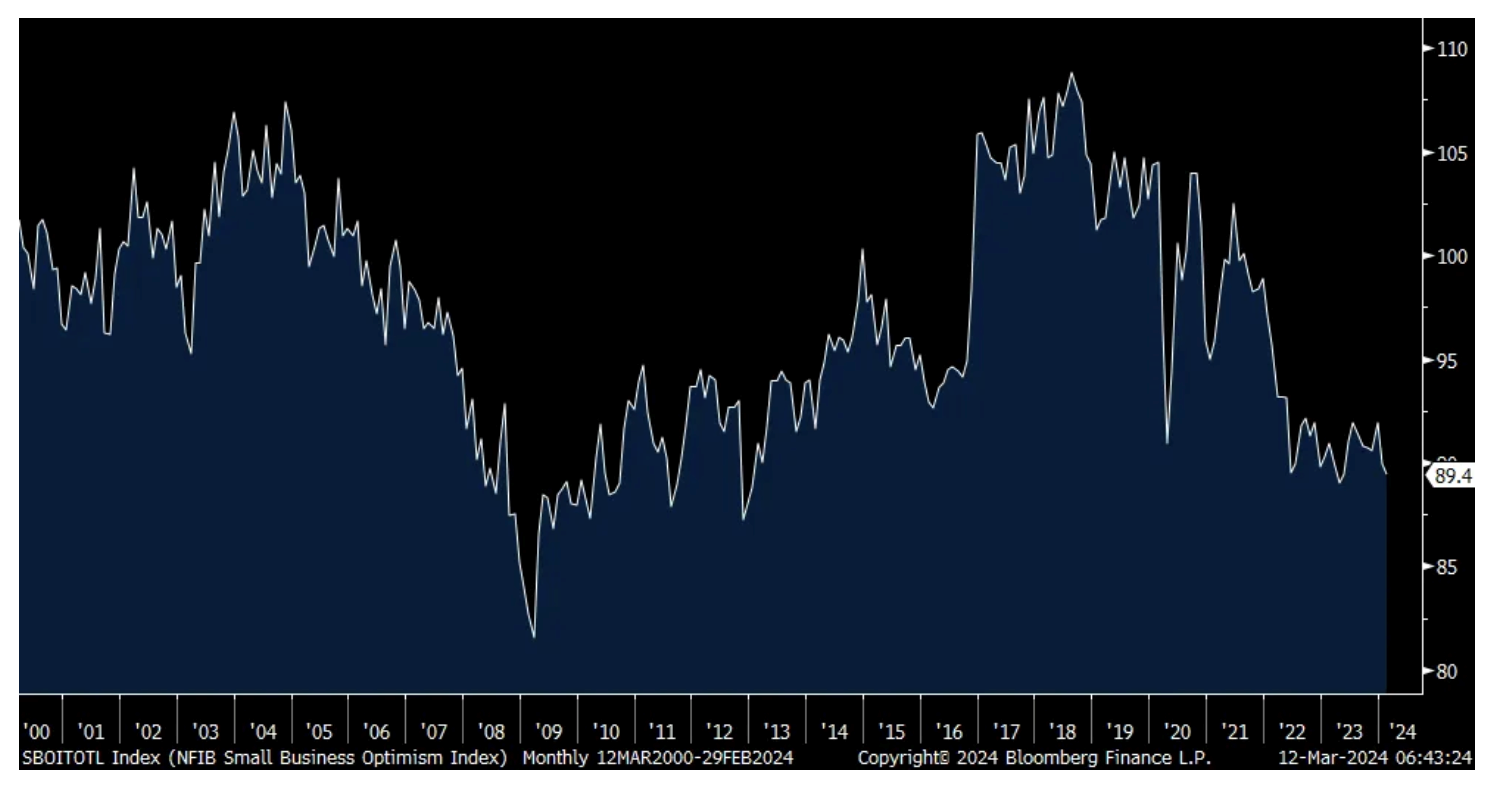

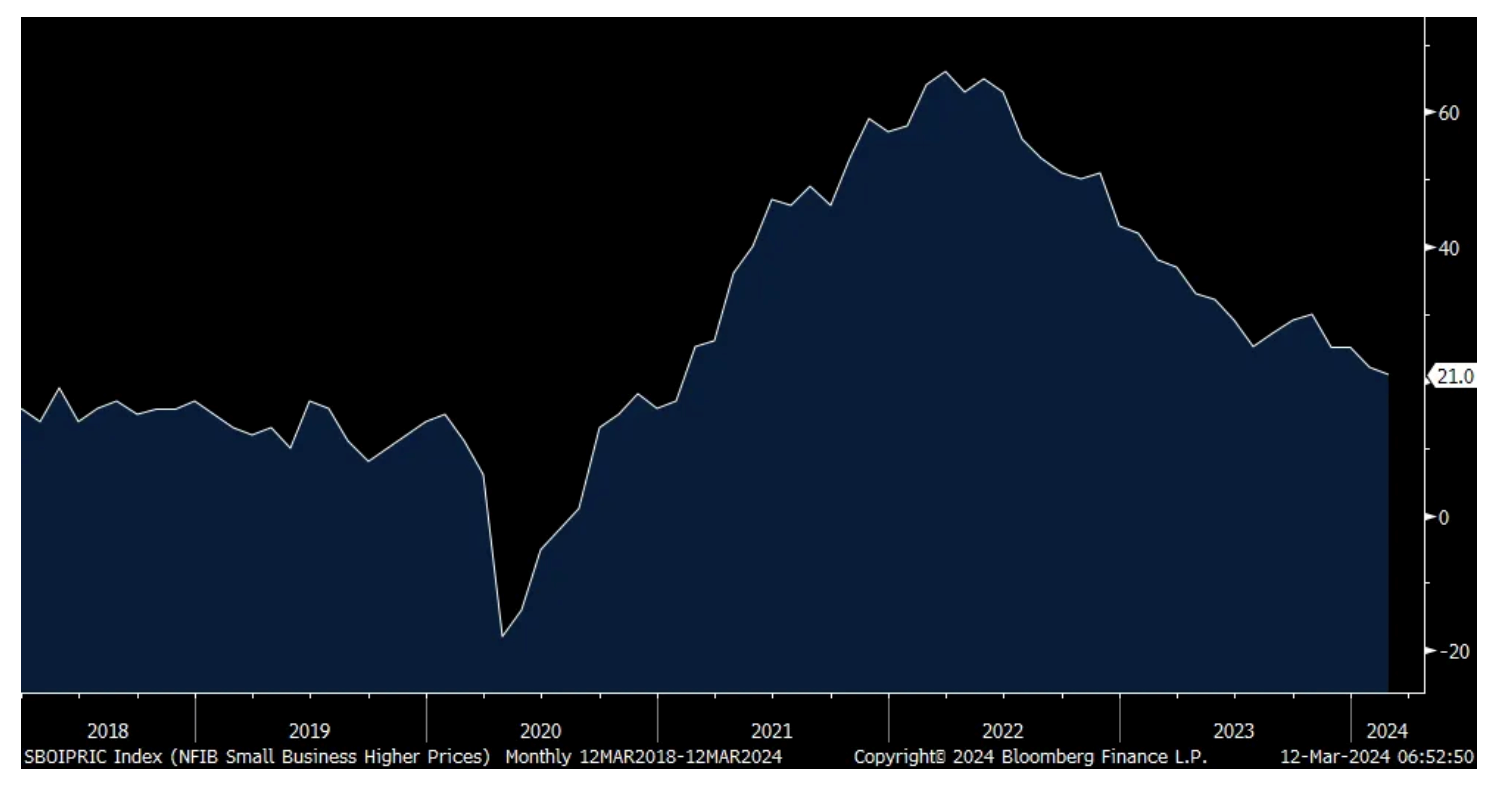

The February NFIB small business optimism survey was less optimistic again, slipping to 89.4 from 89.9 and that was a print last seen in May 2023. It's also nearing again the lowest level since 2013 and for perspective, the 50 yr average is 98. To add to more evidence of the slowdown in hiring, Plans to Hire fell another 2 pts, after dropping by a like amount in each of the prior two months, to 12% and that is the least amount since 2016 not including Covid.

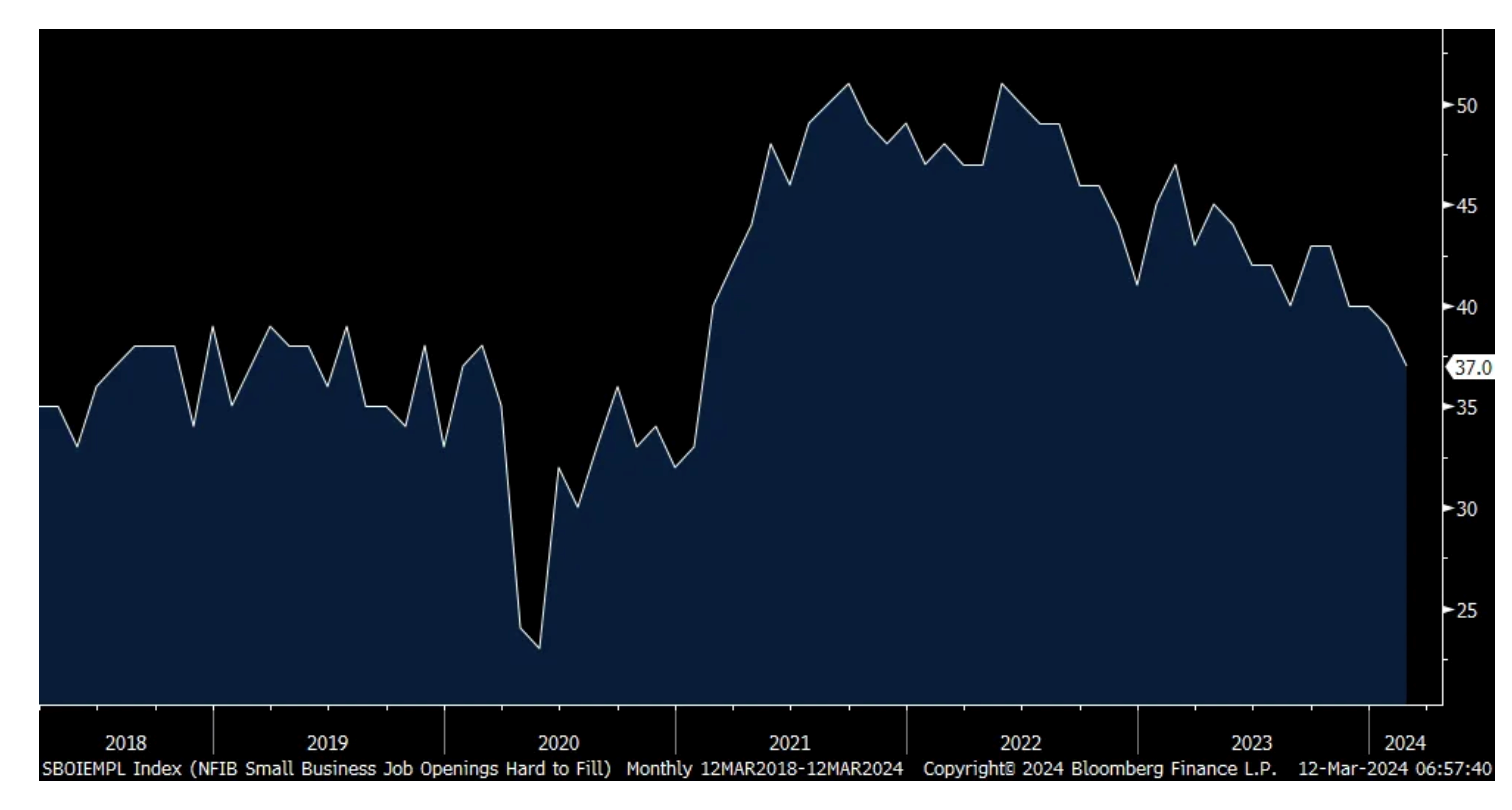

Also, job openings shrunk to the lowest since January 2021. Compensation, both current and future, plans each fell with the latter at the lowest since March 2021. There was also a 2 pt drop in expectations for a capital spending increase to the lowest since April 2023. For those of us hoping for an inventory restock sooner rather than later, Plan to Increase Inventory fell 4 pts to the least in a year. Higher Selling Prices did fall by 2 pts to 21%, the least since January 2021, so at least good news on the inflation front.

Further, those that Expect a Better Economy fell 1 pt to a 3 month low but there was a 6 pt rise in Expect Higher Sales but only after dropping by 12 months in January. Good Time to Expand fell 3 pts to match the lowest since May 2023. The earnings trend dropped by 1 pt to a 3 month low. Easing of Credit Conditions did improve by 2 pts to -6% and the average rate paid on a short term loan fell to a still high 8.7% from 9% in the month before.

My bottom line, there was softness throughout this report, particularly on the labor front.

The bottom line from the NFIB, "While inflation pressures have eased since peaking in 2021, small business owners are still managing the elevated costs of higher prices and interest rates. The labor market has also eased slightly as small business owners are having an easier time attracting and retaining employees." We know there are now less people quitting. More on this from NFIB, "Reports of labor quality as the single most important problem for business owners decreased five points to 16%, the lowest reading since April 2020."

Lastly from the NFIB, "Although the economy has not tanked, the edges are starting to fray...Inflation is sticky. Goods prices have fallen as expected, but service prices are resisting a decline. And, for most small businesses, wage costs are the top operating expense for these labor intensive firms...Adding to the wage stickiness is an increase in various minimum wages, making fighting inflation harder. Labor costs will be passed on to customers through higher prices (or reduction in other services)."

NFIB

Plans to Hire

Job Openings

Higher Selling Prices

While the Cass Freight shipments index got a lift of 7.3% m/o/m in February because of the extra day and a weather recovery from the rougher January, Cass thinks we're seeing a turn up and the beginning of a restock. "While seasonality remains soft in the near term and there are no more extra days on the calendar, underlying volumes have shown improvement." If a turn is here (not seen in the NFIB survey but hopes elsewhere), manufacturing can start to lift too.

While Oracle's stock is ripping higher on all the AI cloud excitement, their revenue guide for fiscal yr Q4 is just 4-6% overall and non-GAAP eps flat to down 2% to an line guide. There were no macro IT spend comments that I saw as most of the call was on their faster growing data center business.

As for services inflation being ALWAYS sticky, Vail Resorts reported earnings too last night and they said for the '24-'25 ski season their Epic Pass price will rise 8% which is similar to the current season and after a 7% increase in the year before that. To a question that this is a wide spread to overall CPI, the CEO responded by saying "We have historically consistently priced above inflation given the investments that we make in the guest experience at our resorts.

If you look at each year, the data that we look at is guest behavior, we look at the investments we're making and we look at inflation. When we're looking at inflation, we're looking at total inflation, but we're also looking at things like services inflation, because obviously we're in the services business and we also look at admissions inflation. So we're really looking holistically at inflation and then our own guest behavior and price elasticity that we have based on the results of our pass business."

While traffic was negatively impacted by less snow in certain places, "I think what we're seeing is that the guests that are coming are still spending money on those ancillary businesses (like ski school, rental business and dining)...I'm not seeing any underlying spending trends that are concerning...I'm not seeing any indicators right now that would reflect a kind of big shift in spend...I'm not seeing any other indicators that would reflect that our guests are pulling back on their spending right now."

Overseas, the UK reported a softer than expected jobs figure in the 3 months thru January and also a rise in February jobless claims. So, gilt yields are falling as a result and the pound is a touch lower while the FTSE 100 is up 1% on hopes for rate cuts at some point.

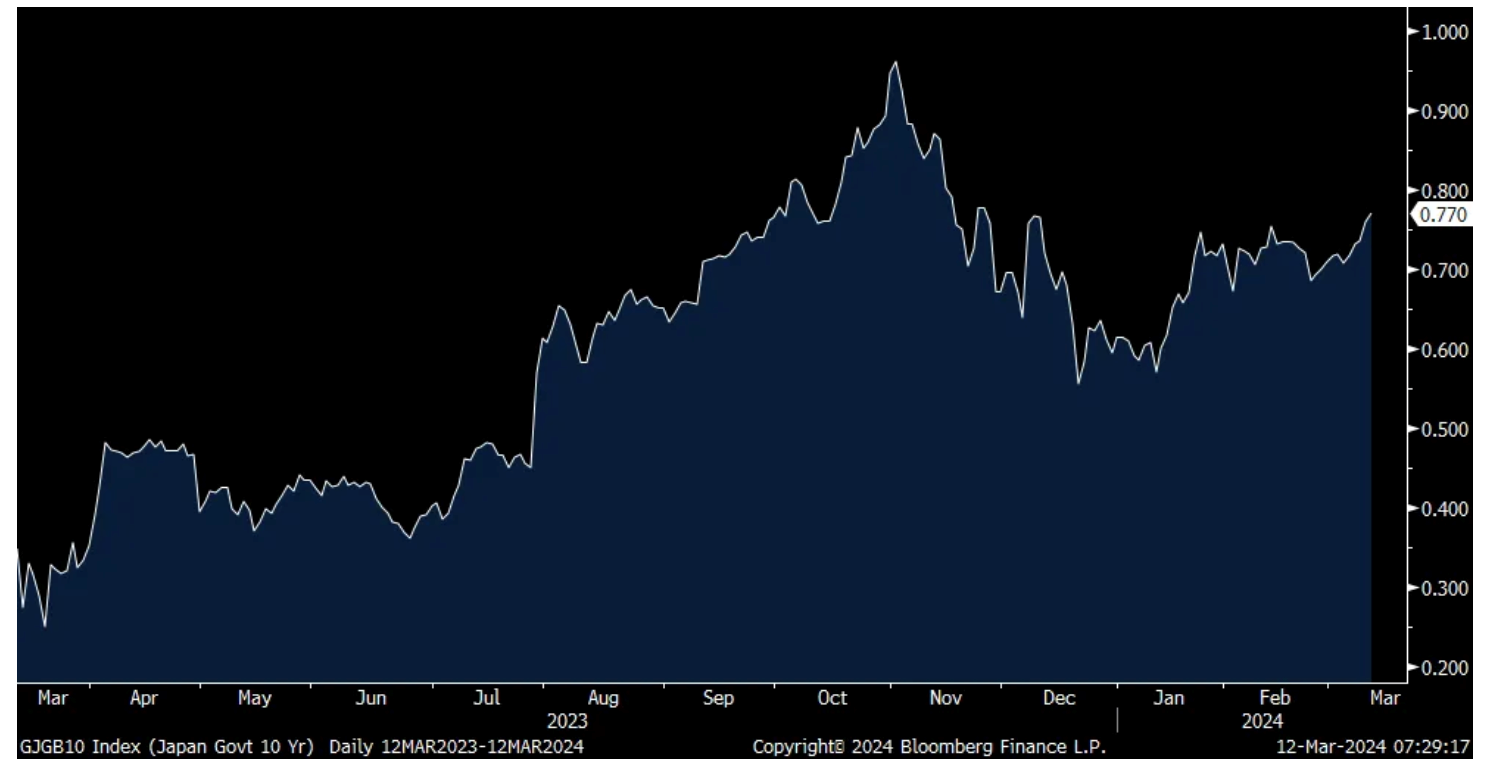

Finally, this story from Bloomberg News again citing 'people familiar with the matter', "Bank of Japan officials are edging closer to raising interest rates and will decide whether to move this month at next week's policy meeting, with the outcome currently too close to call...A final decision will be made after officials see the initial tally from spring wage talks due Friday, according to the people." The 10 yr JGB yield did rise for the 10th day in the past 11 but the yen is down for the 1st day in 6. The Nikkei was little changed.

So it will be next week or in April that NIRP and maybe YCC are gotten rid of. Still quite amazing how it takes this long to decide.

Over the weekend, the Wall Street Journal published an article suggesting that there is resistance with the DEA to the Administration's potential rescheduling of marijuana to Schedule III under the Controlled Substance Act.

Yesterday, cannabis stocks fell in response to the WSJ article.

The bottom line is that the WSJ quoted a few "prohibitionists" who have opposed cannabis for years -- but the trend to rescheduling, to this observer, seems the likely legislative pathway in the next few months.

I believe that there was very little to the article. I moved to a very large position in MSOS on Monday's weakness.

From Veda Partners:

Not only am I optimistic on rescheduling but the odds of Safer Banking legislation are improving. From Jeffries:

Despite the very strong growth outlook for US cannabis, sector valuations remain depressed, largely due to the fact it remains federally illegal, meaning US cannabis names can't trade on a major exchange, there are very few custodians of the stocks, and institutions can't or won't invest given these dynamics. Against this backdrop, the space is desperate for some kind of federal reform that may help address this.

For the last several years, all hope of any sort of federal incremental legislative change has been on SAFER Banking. This then arguably took a back seat in terms of attention, one due to likely near-term rescheduling, and two, after SAFER Banking did not get a vote in the Senate before the end of the year. There was a feeling that the only federal change we could see in the next 12 months was rescheduling.

Over the last month or so, however, there has been increasing optimism that SAFER is not dead, and to this, there were several updates this week that would suggest this could be the case.

First, on Weds, March 6, Senate Majority Leader, Chuck Schumer, in a leadership press briefing, said that his chamber will “work very hard” to enact SAFER banking this year. “As you know, many of the bills we’ve passed are bipartisan,” he said, adding that “we’re going to work very hard on many different things ... first have to fund the government ... But after that, you will see us turn to many of the bills that we passed: the SAFER Act, safety on the rails, so many other things.”

Second, on Thurs, March 7, when contacted by Marijuana Moment, he told them a bipartisan marijuana banking bill remains a “very high priority” for the Senate, and members are having “very productive” bicameral talks to reach a final agreement. Marijuana Moment also reached out to the Democratic Senate sponsor of SAFER, Sen. Jeff Merkley, who said the legislation is “gaining momentum” as lawmakers work to bring it to the Senate floor and pass it “this year”, while the office of the Republican SAFER Banking prime sponsor, Sen. Steve Daines, said that “conversations have been productive and Senator Daines is working to get the bill across the finish line.”

If SAFER Banking does make it to the floor, most likely as part of a wider unrelated package which should boost its prospects of passage, a potential stumbling block is that it is also likely to come with amendments. Encouragingly, while one would be more Democrat focused, specifically measures for provisions on state-legal cannabis expungements, known as the HOPE Act, it will also likely include an amendment that should help secure Republican buy-in, specifically measures around gun rights for cannabis consumers, known as the GRAM Act. To these amendments, on Wednesday, March 6, referencing a Marijuana Moment report on his press briefing, Schumer posted on 'X', “The SAFER Banking Act would be a huge step to help cannabis businesses. And we must pass it along with provisions to expunge records for cannabis offenses like HOPE and GRAM.”

In terms of possible implications of SAFER, from an investment perspective at least, if we also see rescheduling alongside this, having two significant pieces of incremental reform should certainly improve the prospects for possible uplistings and/or greater institutional involvement vs one piece of reform alone.

More Night Moves: A Detailed Look at Overnight Futures and Why/What Markets Are Moving

* The market bent but didn't break on Monday

* Futures resumed an upward ascent overnight

* We continue in an overbought condition with the S&P Short-Range Oscillator at 3.26% v 2.84%

* Yields are mixed to lower this morning, but the intraday reversal to higher yields, surprisingly, was met my higher equity prices, and crude oil prices are higher (+$0.66) -- gold has reversed lower (-$6.80) and bitcoin is a bit lower (-$200)

* The U.S. dollar has reversed higher after losing value over the last few days v. the yen.

Don't question why she needs to be so free She'll tell you it's the only way to be She just can't be chained To a life where nothing's gained And nothing's lost, at such a cost

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were rallying overnight. S&P futures peaked at +25 and bottomed at +5. Nasdaq futures peaked at +130 and bottomed at +30. At 6:22 a.m. ET, S&P futures were +12 and Nasdaq futures at +81.

* Commodities are mixed with Brent crude +$0.67 at $82.87.

* The S&P Short-Range Oscillator is more overbought at 3.26% v. 2.84%.

* The VIX is slightly lower at 15.12 (-0.10).

* The U.S. dollar is stronger against the yen and flat compared to the pound and euro.

* Treasury yields are mixed. The 2-Year Treasury yield is flat at 4.534% and the 10-Year is -1 basis point to 4.089%. Over there, the yield on the 10-Year U.K. Gilt bond is -5 basis points.

* Overnight, the inversion of the 2s/10s Treasuries curve is flat at -43 basis points. Real rates remain quite elevated; the 10-year is still about 1.85, again in real terms.

* Gold is -$6.80 and sits at $2,182.

* Bitcoin is -$330 to $71.7K.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

Here are Monday's trades -- I believe in my Diary's full disclosure and transparency of trades/investments -- this is not CNBC! How else can you evaluate the value of my actions without memorializing them?:

US MKT INTEL: CPI SCENARIO ANALYSIS – originally published in the Mar 11 Morning Briefing and updated with views from Rates Trader, David Nadle.

Feroli’s full CPI preview is here. Feroli sees Headline MoM CPI printing +0.4%, in line with the Street. He sees Core MoM printing +0.28%, below the Street’s +0.3% estimate. On a YoY basis, he sees headline inflation of 3.1% (vs. 3.4% in previous print) and he sees core inflation of 3.7% (vs. 3.9% in the previous print), both aligned with the Street. Feroli’s full comments:

We estimate that the consumer price index (CPI) rose 0.4% in February. We look for a 2.6% increase in energy prices in the CPI to boost the headline inflation print for February after declines in energy prices had helped drag down inflation over the prior few months. Food prices have been trending higher in recent months and we think that continued into February with the food CPI increasing another 0.2%. Away from food and energy, we forecast that the core CPI rose 0.28% in February. While not expecting a particularly soft increase, we think the February monthly change in the core will be modest enough to keep the related year-ago inflation rate trending lower, and we believe the core CPI will be up 3.7%oya in February (down from 3.9% in January).

The 0.39% jump in the core CPI in January was an upside surprise but we think that this will prove to be noise around a softer trend for inflation. Our forecast calls for the February core inflation rate to be a step down from January and close to the average figure reported for the few months before the January surprise. It is possible that price adjustments implemented at the start of the year led to significant firming in inflation in January but that these increases will not be continuously repeated over time. For example, an increase in the price of postage helped push communication prices up 0.5% in January, but we think communication prices will return to their preceding downward trend in February, with a 0.3% move lower. Prices for lodging away from home and airfares also jumped in January, but we look for much more modest increases to be reported for February, with lodging prices up 0.3% and public transportation prices rising 0.1%.

Apparel prices declined in January and generally have been moving lower lately. We think this continued in February, with a 0.3% move down in the apparel CPI that month. The increases in medical care prices in the CPI have been relatively stable lately at 0.4% or 0.5% and we think they behaved similarly in February, with a 0.4% move higher.

Owners’ equivalent rent (OER) was another area that led to the upside surprise in the January CPI. The 0.56% January jump in that measure came despite industry figures pointing to a moderating trend for rental inflation over time and the related tenants’ rent index showing softer price increases that month. We forecast a step down in OER inflation in February, with this measure up 0.44% that month. We also look for continued moderation in the trend for tenants’ rent, with this price index rising 0.34% in February.

While overall core inflation was firm in January, the price changes for vehicles were soft, and industry data point to declines in related pricing in February. We forecast that new vehicle prices in the CPI moved down 0.3% while used vehicle prices dropped 1.1%.

CPI SCENARIO ANALYSIS. The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence. This month we will focus on Core MoM outcomes and 1-day SPX moves.

[7.5%] Above 0.40%. The first tail-risk scenario would likely reflect a stronger than expected gain in housing prices and material strengthening in Core Services. The result of still strong consumer whose spending power is amplified by a still tight labor market and upward pressure on wages. Fears of a second peak in inflation would likely manifest in increased options activity reflecting more rate hikes this year and potentially more yield curve inversion. Negative for risk assets and potentially triggers a full Momentum unwind. SPX loses 1.75% – 2.25%.

[30%] Between 0.30% - 0.40%, inclusive. Similar to the above tail-risk scenario, the worry here would be clear signs of core inflation accelerating, with headline inflation unable to break below 3%. Another factor to watch is evidence of Red Sea/geopolitical conflicts impacting inflation, potentially adding back a fear premium in commodity markets. SPX loses 50bps – 1%.

[37.5%] Between 0.20% - 0.30%, inclusive. An in line print likely causes a muted reaction since that would give little evidence as the presence or timing of Fed cuts this year. A print at the lower end of the range, would build comfort in the disinflationary trend and while not enough to reprice Fed expectations, Equities may take this as a signal for further rotation into more Cyclical/Value sectors. SPX adds 25bps – 75bps.

[22.5%] Between 0.10% - 0.20%, inclusive. In this scenario, we would likely see some of the delayed housing disinflation show up in the print as well as a larger than expected decline in vehicle prices. If we saw a step down in Core Services, this likely restarts the calls for earlier rate cuts, again supportive of the current Equity rotation especially if the yield curve bull steepened. SPX adds 1% – 1.5%.

[2.5%] Below 0.10%. Similar to the previous scenario, expected a collapse in bond yields triggering an ‘everything rally’ within Equities. This would likely coincide with the bond market bringing May rate cut expectations above 50% from its current ~23% level. SPX adds 1.50% – 2%.

US: CPI DAY. Futs are higher led by Tech; ORCL earnings have the stock +13.6% pre-mkt. TMT seeing support from Semis (NVDA +1.9%) and the balance of Mag7 names are up 50bp – 95bps pre-mkt. Bond yields are down 1bps with TBill outperforming. USD flat after yesterday’s gain. Cmdtys mixed with Energy leading, Ags lagging, and Metals mixed (base over precious). The market’s focus is on CPI today but there is also a 10Y auction and some consumer-sector earnings, too.

and...

EQUITY AND MACRO NARRATIVE: Yesterday’s session was a bit quiet as we saw some position squaring ahead of today’s CPI. What follows is a repost of the US Market Intel CPI Scenario analysis, strategy notes from Marko, Dubravko, and Mislav, plus an update from our Delta One team that looks at the impending Momentum Unwind and how to play the move.