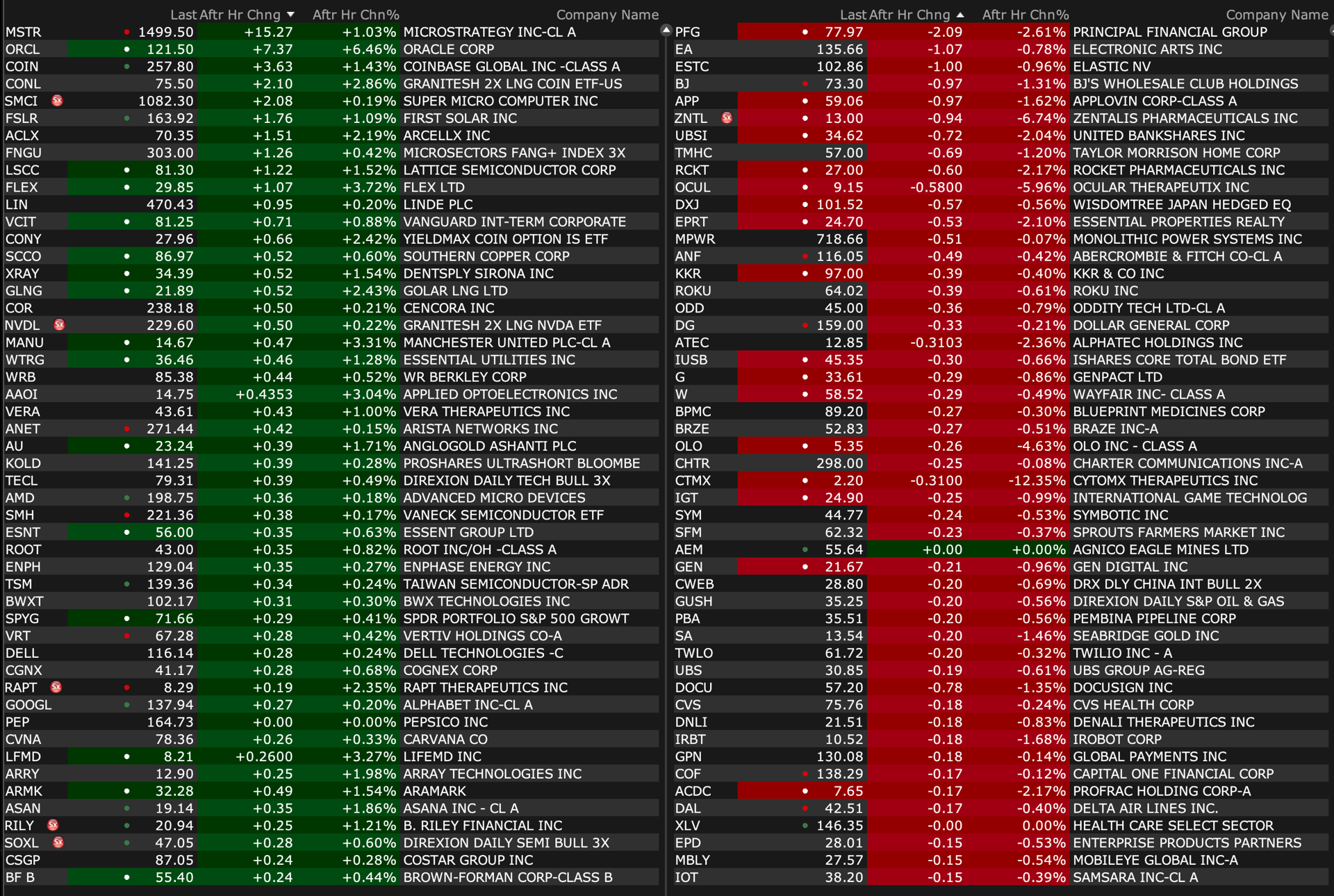

After Hours Movers

BY Doug Kass · Mar 11, 2024, 4:28 PM EDT

BY Doug Kass · Mar 11, 2024, 4:28 PM EDT

* Yucky!...

- NYSE volume 421M shares, 9% below its one-month average

- Nasdaq volume 4.02B shares, 11% below its one-month average

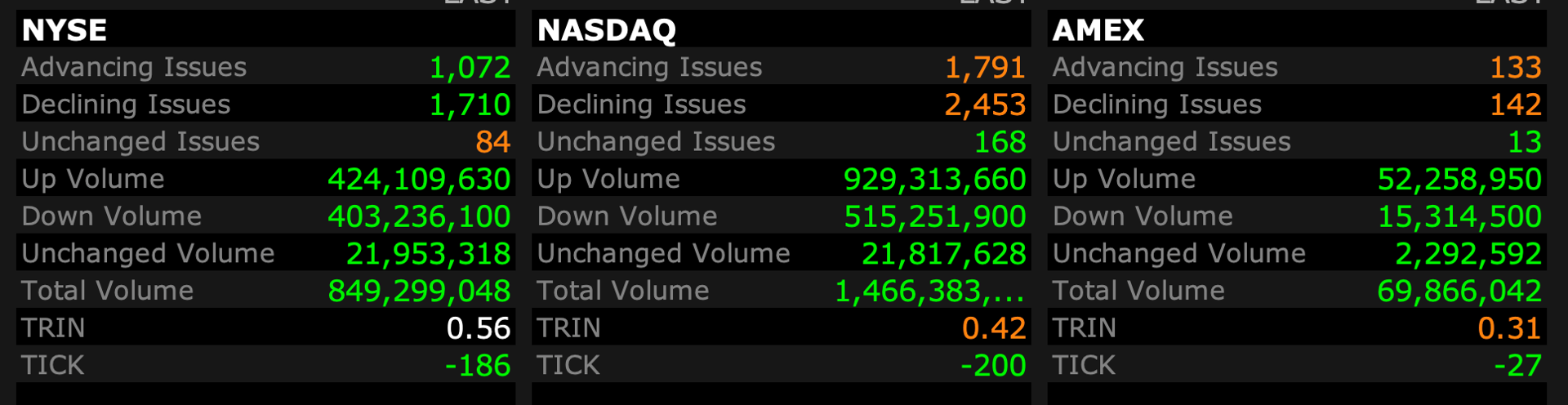

Breadth

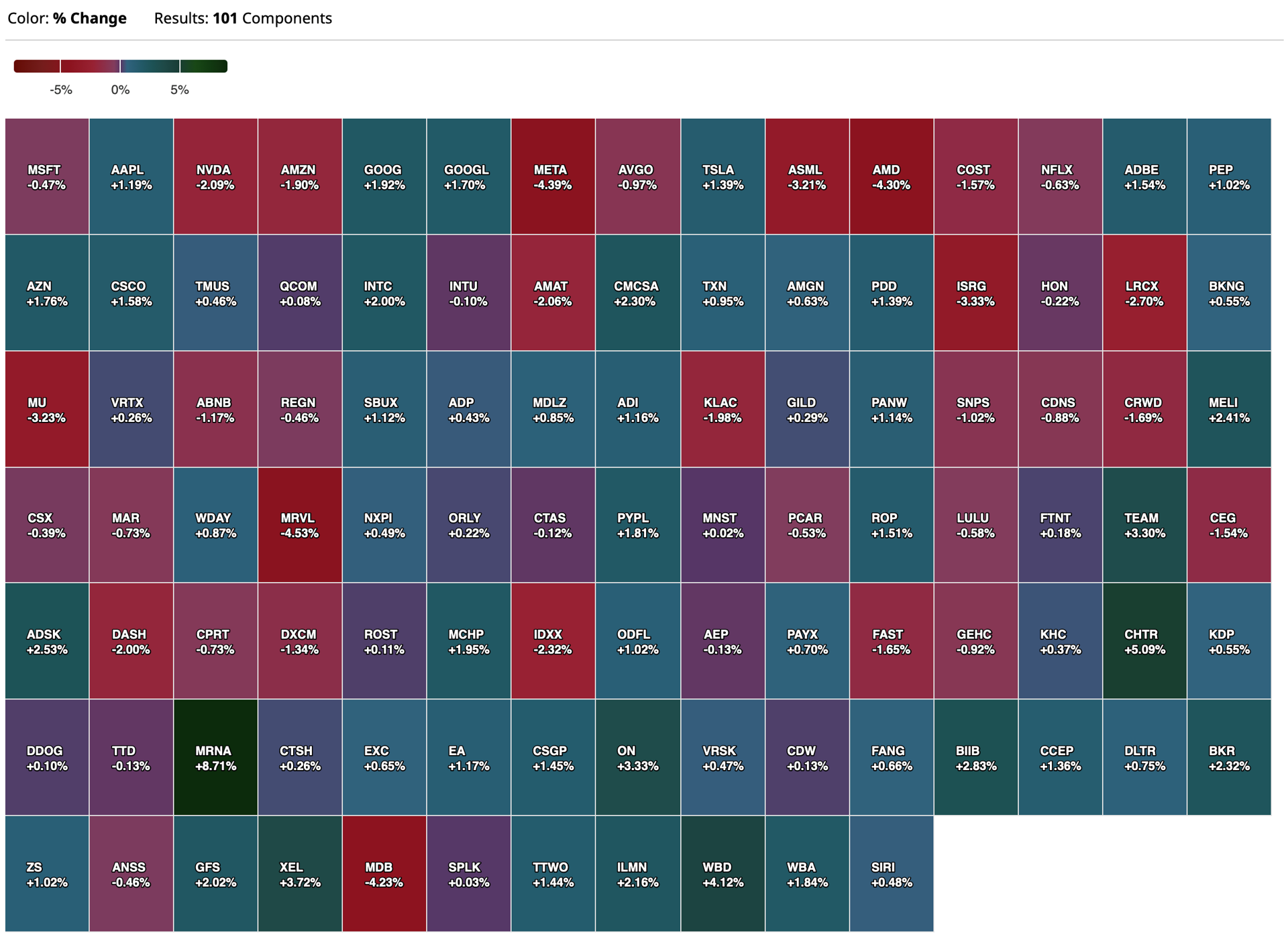

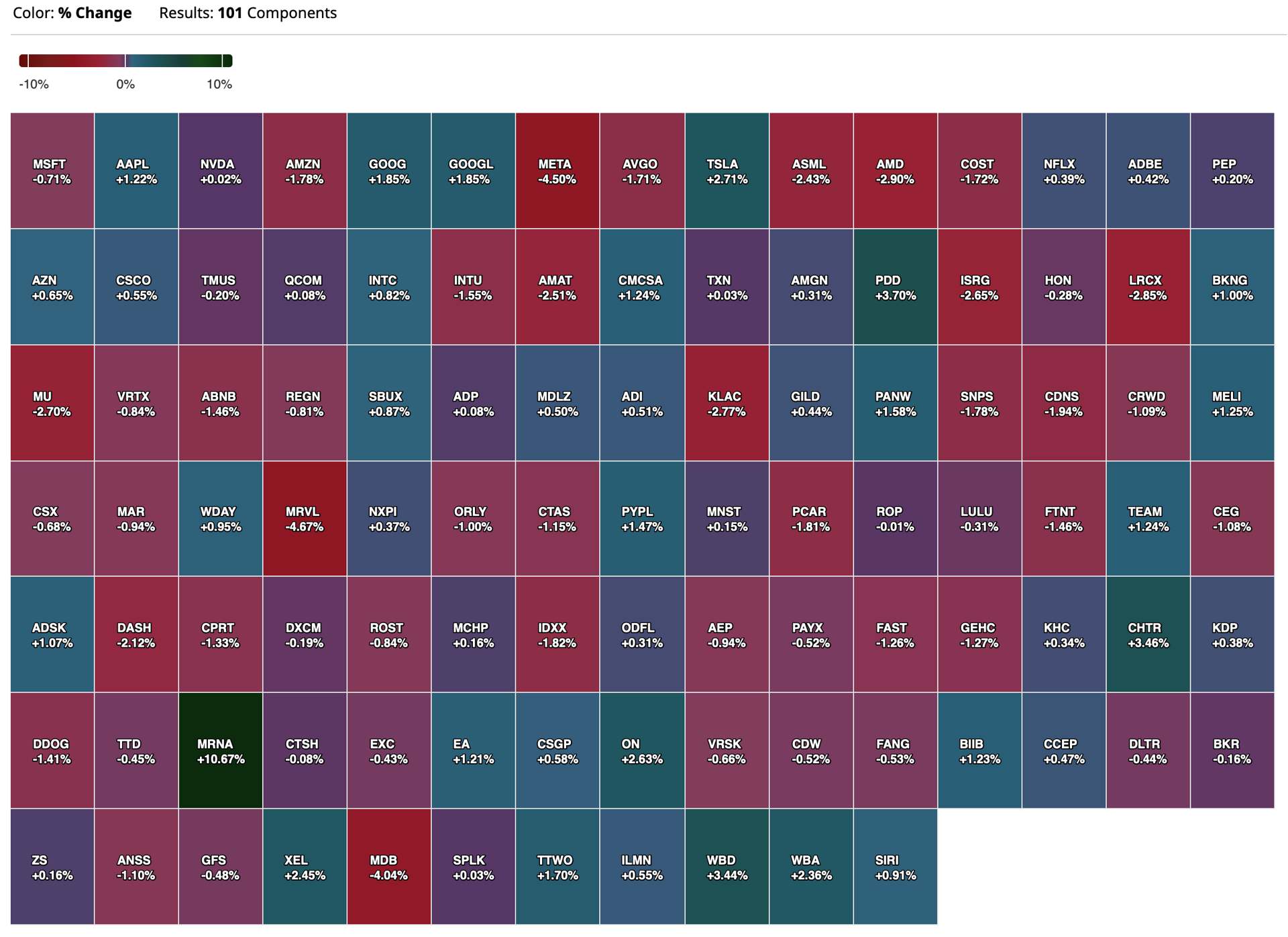

Nasdaq 100 Heat Map

BY Doug Kass · Mar 11, 2024, 4:18 PM EDT

I have moved to very large in MSOS.

More tomorrow...

BY Doug Kass · Mar 11, 2024, 4:00 PM EDT

Goldman Sachs previews Tuesday's Consumer Price Index:

We expect a 0.32% increase in February core CPI (vs. 0.3% consensus), corresponding to a year-over-year rate of 3.71% (vs. 3.7% consensus). We expect a 0.44% increase in February headline CPI (vs. 0.4% consensus), which corresponds to a year-over-year rate of 3.15% (vs. 3.1% consensus). Our forecast is consistent with a 0.38% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.21% increase in core PCE in February. We will update our core PCE forecast after the CPI is released and again after the PPI is released.

We highlight three key component-level trends we expect to see in this month’s report. First, we expect the temporary boost to core CPI from start-of-year price increases to fade, which should result in a slowdown in the medical care services, personal care services, communication, and daycare categories. Second, we expect used car prices to decline 0.4% and new car prices to decline 0.3%, reflecting lower auction prices and higher dealer promotional incentives. Third, we expect shelter inflation to slow on net (we estimate +0.42% for rent and +0.47% for OER), as the gap between rent and OER growth normalizes following last month’s jump.

Going forward, we expect monthly core CPI inflation to come down to 0.20-0.25%. We see further disinflation in the pipeline in 2024 from rebalancing in the auto, housing rental, and labor markets, though we expect small offsets from a delayed acceleration in healthcare and the outperformance of rent growth for single-family units relative to multifamily units. We forecast year-over-year core CPI inflation of 3.0% and core PCE inflation of 2.3% in December 2024.

BY Doug Kass · Mar 11, 2024, 3:26 PM EDT

Ironically, coincident with the intraday rally in equities off the lows, the bond market has deteriorated.

Yields started the day lower by 1-2 basis points and are now higher on the day:

* The yield on the two year Treasury note is +5 basis points to 4.54%.

* The yield on the ten year Treasury note is +2 basis points to 4.11%.

* The yield on the long bond is also +2 basis points to 4.28%.

BY Doug Kass · Mar 11, 2024, 2:55 PM EDT

I have closed out my PARA and WBD investment shorts for nice profits.

BY Doug Kass · Mar 11, 2024, 2:20 PM EDT

The word "AI" triggers Apple buy algos... until they release that its just for Ad product Apple Tests AI-Powered App Store Ads, Similar to Performance Max

13:41 - AAPL - Reportedly testing an AI-powered Ad product for app store for efficiency

BY Doug Kass · Mar 11, 2024, 2:04 PM EDT

MRKT Call with Guy and Danny.

And it's free!

BY Doug Kass · Mar 11, 2024, 1:15 PM EDT

BY Doug Kass · Mar 11, 2024, 1:00 PM EDT

From Charlie, here.

BY Doug Kass · Mar 11, 2024, 12:32 PM EDT

* But taking "baby steps"....

More SPY and QQQ calls shorted with S&P cash -8 handles.

BY Doug Kass · Mar 11, 2024, 12:05 PM EDT

Dougie, everything bearish you have been saying recently makes me wonder why you aren’t buying any Gold stocks. You read Barron's “Up and Down Wall Street” column from Randall Forsyth this weekend. You love to buy out of favor, cheap stocks. Why not GDX, GOLD, AEM, NEM? Better upside potential there in the next 12-18 months than any long you have recommended in recent months.

Dougie Kass:

Like bitcoin I can't establish an intrinsic value for the price of gold.

It is sentiment driven.

If I analyze St Joe Company and come to the conclusion it is worth $60/share - I would likely buy it at $50 and buy more at $45, etc. etc.

I can't do that with bitcoin or gold so I stay away of trading and investing in asset classes I generally don't know the value for.

BY Doug Kass · Mar 11, 2024, 11:50 AM EDT

- NYSE volume 139M shares, 14% below its one-month average

- Nasdaq volume 1.35B shares, 18% below its one-month average

Breadth

Nasdaq 100 Heat Map

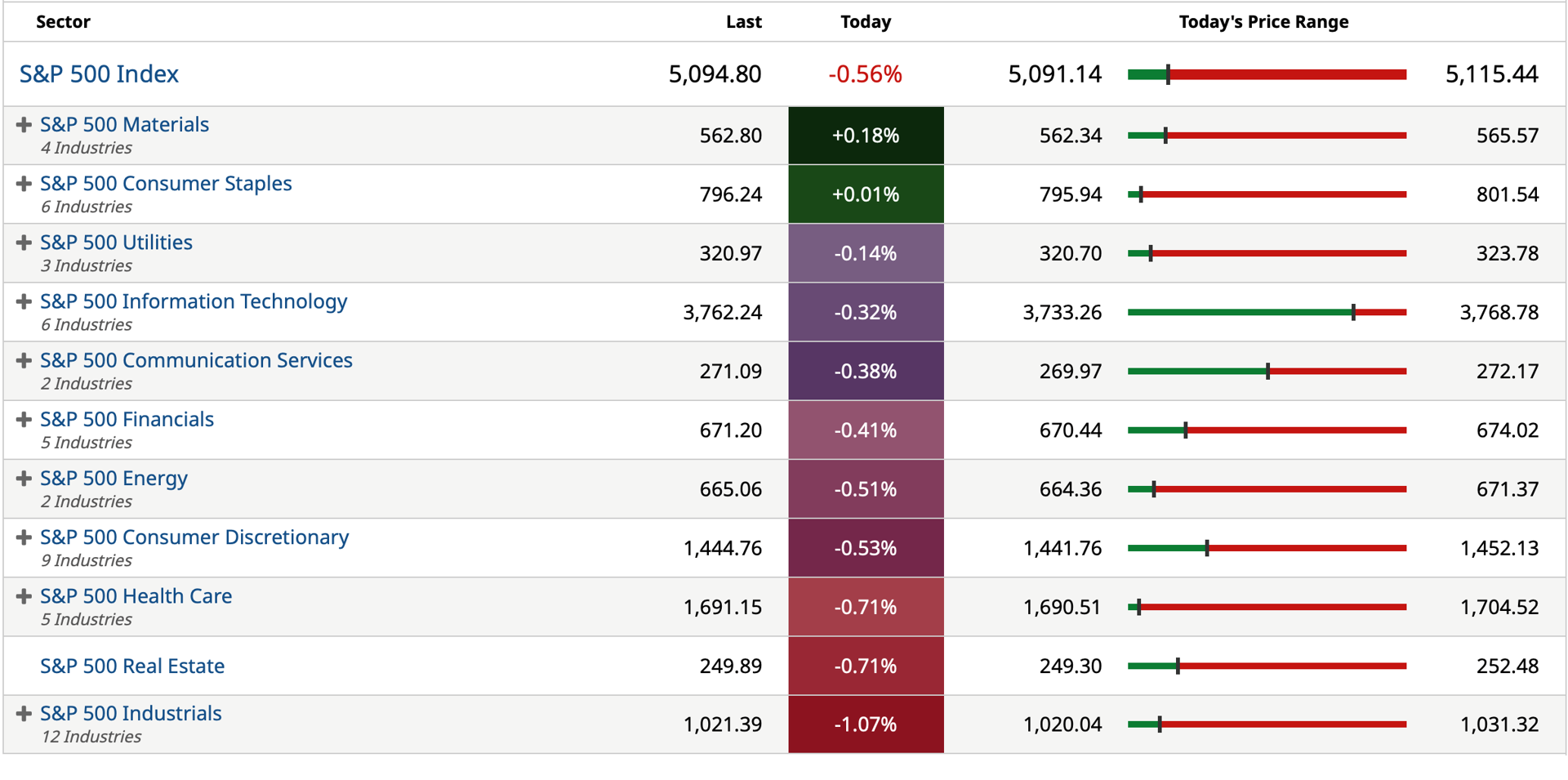

S&P 500 Sectors

BY Doug Kass · Mar 11, 2024, 11:38 AM EDT

I am down to tagends on my investment short of Starbucks SBUX.

Interestingly there was an aggressive buyer of out of the money calls that expire on Friday - something to watch as there is no news (on EPS, etc.) expected this week.

See the option and the common intraday below.

BY Doug Kass · Mar 11, 2024, 11:15 AM EDT

With S&P and Nasdaq cash rallying to only -12 and -35, respectively -- I am adding to my short calls now.

BY Doug Kass · Mar 11, 2024, 11:00 AM EDT

From Rich:

My favorite stat:

If you bought NASDAQ in March 2000 it took you 14 years just to break even.

BY Doug Kass · Mar 11, 2024, 10:28 AM EDT

I have added to my Financial Select Sector SPDR Fund XLF short on the opening.

I plan to get large sized in this ETF.

BY Doug Kass · Mar 11, 2024, 10:12 AM EDT

Former President Trump dumped on META on CNBC this morning.

META shares are -$20/share.

Let's go to the tape!

BY Doug Kass · Mar 11, 2024, 10:00 AM EDT

* The parallels between March 2024 and March 2000 are conspicuous...

In this morning's opening missive I will explain why we may be at the foothill of a bubble in which the distribution of likely investment outcomes are skewed negatively.

In the late 1990s, much like 2023-24, a speculative fever materialized, animal spirits were ignited and the performance of technology stocks dwarfed everything else.

Twenty-five years ago Warren Buffett's investment portfolio was principally composed of financial and consumer equities. Nary a technology stock was in Berkshire Hathaway's largest investment holdings.

Near the end of the dot.com boom in technology stocks in late 1999/early 2000, Warren Buffett wrote these words in the Berkshire Hathaway Annual Report in response to the company's lagging portfolio:

Even Inspector Clouseau could find last year's guilty party: your Chairman. My performance reminds me of the quarterback whose report card showed four Fs and a D but who nonetheless had an understanding coach. "Son," he drawled, "I think you're spending too much time on that one subject."

My "one subject" is capital allocation, and my grade for 1999 most assuredly is a D. What most hurt us during the year was the inferior performance of Berkshire's equity portfolio -- and responsibility for that portfolio, leaving aside the small piece of it run by Lou Simpson of GEICO, is entirely mine.

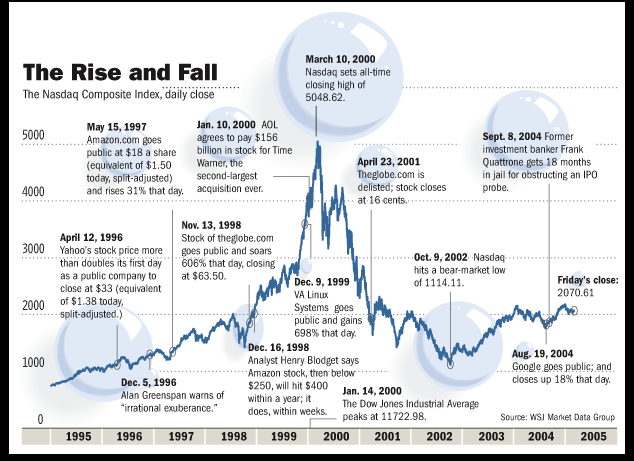

Today I feel much like Warren did in early 2000.

Of course, the rest was history and, beginning in March 2000, the Nasdaq began an unprecedented decline that reached in excess of -80%:

Fortunately, just as the dot.com bubble burst at the turn of the (2000) decade, Berkshire Hathaway's portfolio began a steady and consistent climb. Warren and Berkshire avoided the market's drawdown in the early 2000s and produced superior returns over the next 2 1/2 decades

Today, in March, 2024, Buffett's Berkshire Hathaway BRK.B sits with a record $170 billion of cash - up $40 billion in the last twelve months. Not only has the conglomerate made few meaningful new investments in the recent market rally, Berkshire has actually reduced the size of its investment portfolio since mid-2023!

Many investors seem to want the optimal solution for the moment even as the future has become increasingly uncertain and investment risks have expanded.

As my Grandma Koufax once told me and Warren Buffett has proven, "You have to be willing to look like an idiot in the short term to get the best long-term investment results."

The assessment of upside reward vs. downside risk and the search for "a margin of safety" - the key ingredients of value investing - make me (and Berkshire) seem out of touch at times. But you have to be willing to ignore emotion and "animal instincts" when investing and to do something different to get superior intermediate-term returns.

To return to the 2000/2024 parallel, in this cycle we can replace the term dot.com with the word AI.

History rarely repeats itself but it often rhymes and, as noted above we may be at the foothill of a market bubble.

As of this week, the price/sales ratio of the S&P technology has surpassed the dot.com peak and has hit an all-time high:

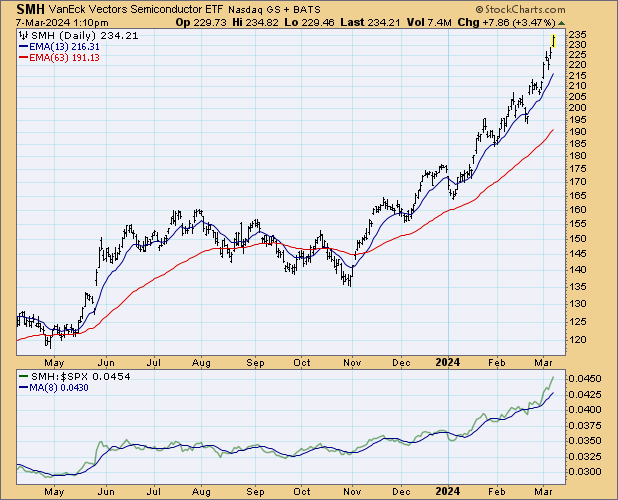

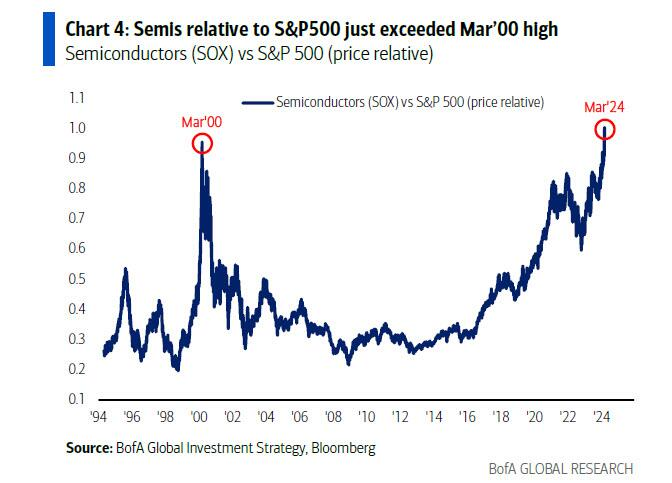

Here are charts of the semiconductor Index - in absolute terms and as compared to the S&P Index:

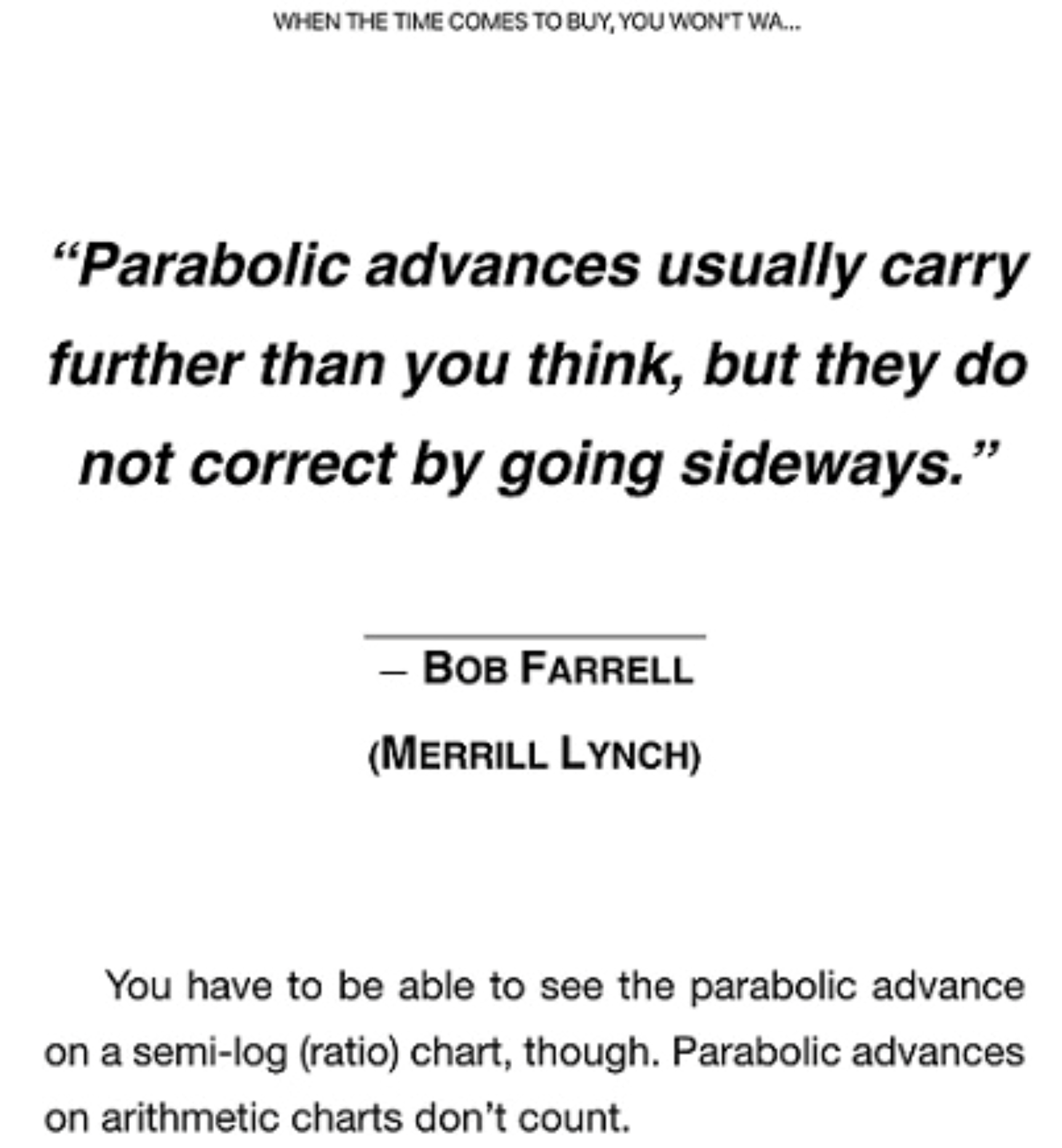

Here are Bob Farrell's sage words, that modify the charts, above, and throw caution to the wind:

It is not likely different this time...

Though not expecting equities to cascade as the did in the early 2000s - we hold to the view that there are some similarities between 1999-2000 and 2023-2024 and that stocks are overvalued in absolute terms and relative to the fixed income markets.

The only question to us is whether we are in the middle of 1999 or in the first quarter of 2000.

Given the large market cap appreciation in the shares of AI-related equities over the last fifteen months we are of the view that we are in early 2000 and not in 1999.

_____

Markets are making new highs, valuations have expanded -- without any real increase in 2024-5 S&P EPS estimates --and investor sentiment is ebullient based on the introduction, the perceived proliferation of artificial intelligence opportunities and the apparent notion that we are in the mid-cycle of an economic advance.

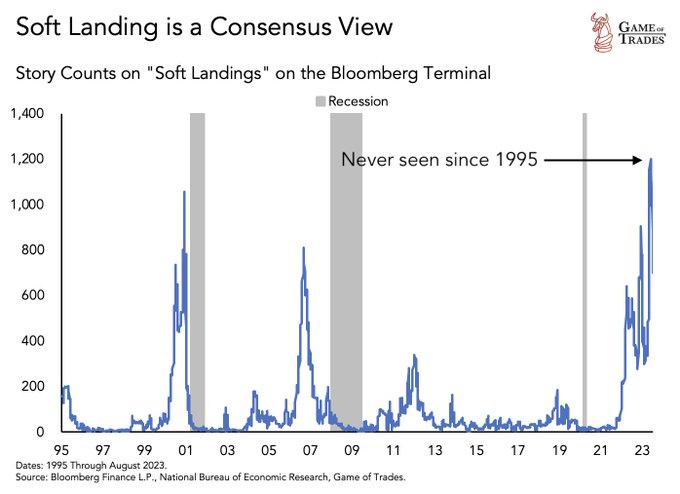

Like 2000 and 2007, a "soft landing" is now the consensus view.

Those two prior periods ended poorly for the economy and for investors:

In contrast to the consensus' growing market and economic confidence we have the following concerns:

* Stacked or cumulative inflation will weigh on the U.S. consumer - especially the lower income segment.

* In part reflecting sticky inflation, interest rates will be higher for longer - squeezing overleveraged borrowers, especially in commercial real estate.

Of note, commodities have recently begun to advance, after moving steadily lower in late 2023:

Notably, the price of oil is tracking higher:

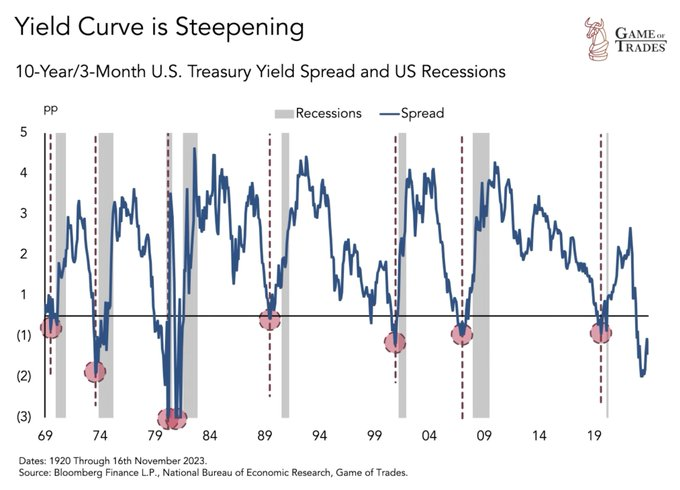

* Yield curve inversions are not a signal to be ignored. Recessions occur only five months (on average) from a steepening after an inversion:

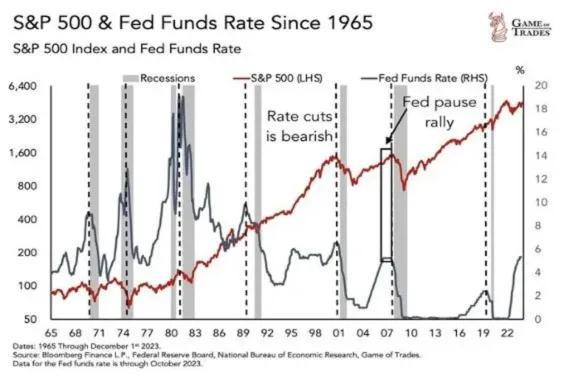

* Interest rate cuts are not necessarily market friendly:

* QT is about to kick in as RRP (reverse repo) drains to near zero.

* Political and geopolitical headwinds are fierce and show no signs of abating.

* Our growing annual deficit and nation's debt load has not and will not likely be addressed by an unprecedented political partisanship:

* The unstable tribal mentality of the extremes on the political left and right (what Arthur Brooks calls the Dark Triad Paradigm) dominate our society: the loss of moderation spells more societal troubles.

Harvard professor Arthur Brooks on finding happiness in an election year

* Valuations, based on historic measures, are almost all above the 90%-tile. Rarely do Bull Markets start from current price earnings levels.

* Equity prices have decoupled from interest rates - the equity risk premium is at a multi-decade low and the spread between the S&P dividend yield and the yield on Treasuries has rarely been wider.

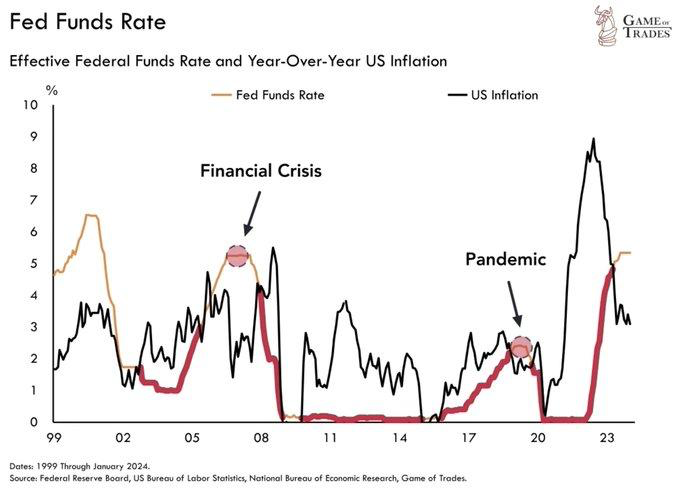

* Very rarely has interest rates been higher than inflation. But, when it does happen, like today, it makes cash a very attractive alternative:

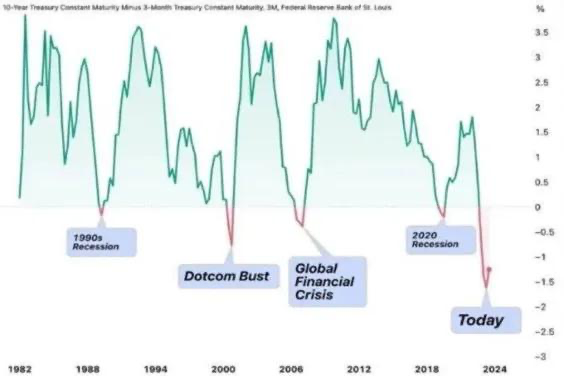

* The last four times the 10-year Treasury note yield minus the 3 month Treasury bill inverted, it led to the 1990s recession, the dot.com bust, the global financial crisis and the 2020 recession

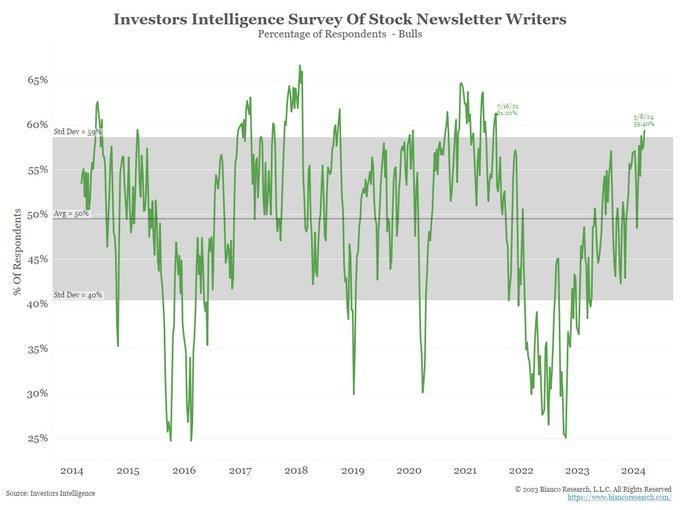

* Investor sentiment is giddy and the Bull Market in Complacency is worrisome - the cover of Barron's this weekend and the Investors Intelligence survey are indicative of this:

* Like prior periods in history, a changing market structure -- casino like ODTE options trading, the proliferation of leveraged quantitative strategies and products and a general dependence on price momentum (not value) as a short-term voting machine -- represent bonafide threats on possible market instability.

The growth in passive investing is affecting market structure in ways the risk of which won't be fully understood until a sustained decline is seen. Its effect on upside momentum will like pose an equal (or greater) and opposite risk on the downside:

* On Friday we may have seen the impact (and risk) of the structural change in our markets when Nvidia NVDA, the third largest company in the world fell by -10% (or $250 billion) in less than thirty minutes on no news. Nvidia's market capitalization is $2.3 trillion - it is not a penny stock(!):

Sell, Mortimer... Sell!

BY Doug Kass · Mar 11, 2024, 9:25 AM EDT

BY Doug Kass · Mar 11, 2024, 9:10 AM EDT

BY Doug Kass · Mar 11, 2024, 9:00 AM EDT

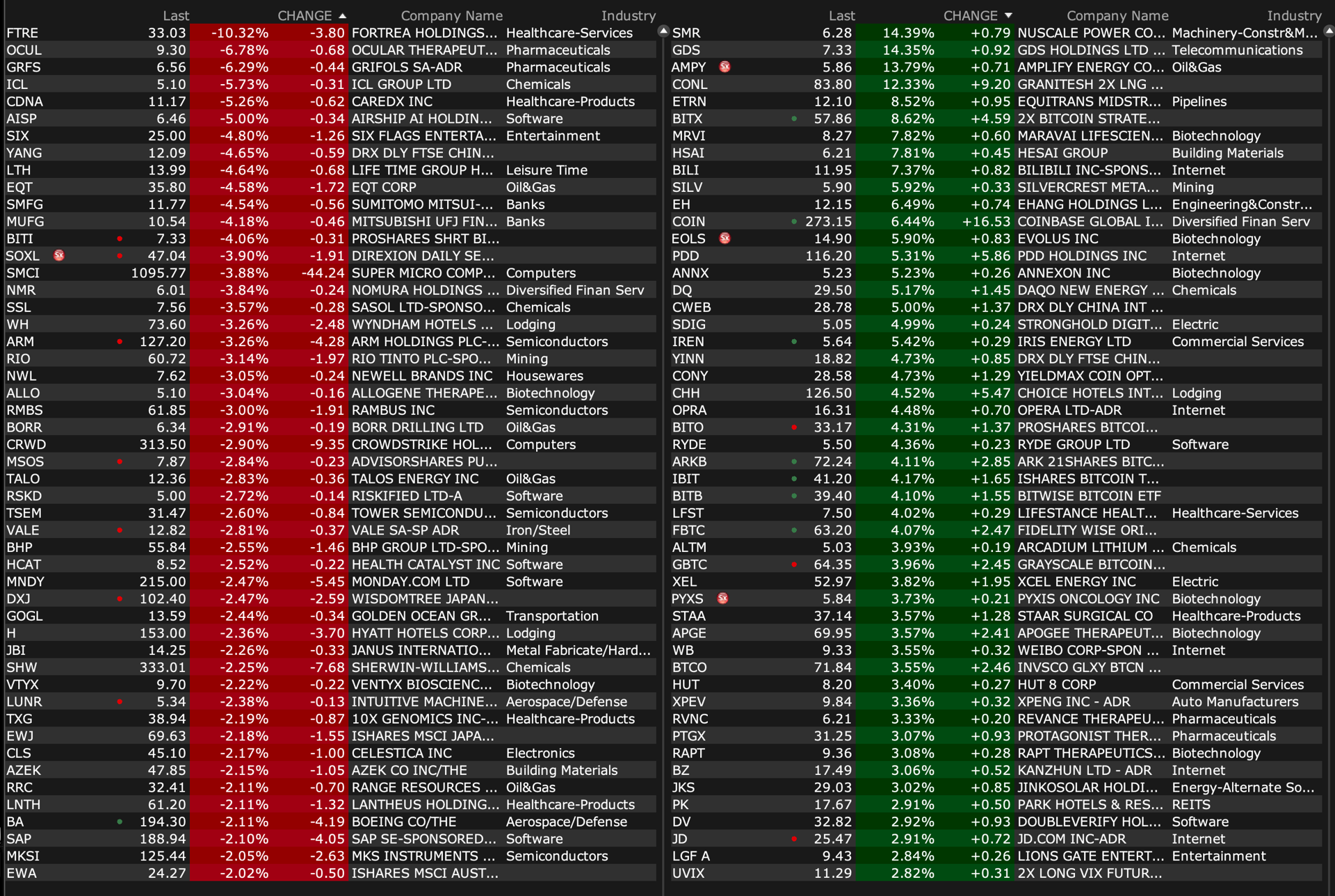

Upside

-MESO +22% (U.S. FDA supports an accelerated approval pathway for rexlemestrocel-L)

-KC +13% (JPMorgan Chase and Co Raised KC to Overweight from Neutral, price target: $4.20)

-AMPY +11% (provides update on Southern California oil sheen: Remains confident that the sheen is not related to our operations)

-MLTX +9.1% (announces significant improvements with Nanobody sonelokimab over 24 weeks in active psoriatic arthritis (PsA) and other important updates at its R&D Day; now rapidly pursuing plans to commence Phase 3 trials in both HS and PsA before end of year and identify new indications)

-MSTR +8.9% (discloses between Feb 26 and March 10 acquired ~12,000 bitcoins for ~$821.7M in cash)

-ETRN +8.2% (confirms to be acquired by EQT at $12.50/shr in all-stock deal)

-LXRX +6.5% (to resubmit Sotagliflozin NDA for Type 1 Diabetes Following Feedback from FDA; files to sell 2.3M convertible shares at $108.50/shr in $250M private placement; reports Q4 earnings)

-RVNC +6.2% (CEO Foley bought 30K shares at $6.98/shr)

-COIN +6.0% (BTC strength; PT raised at Jefferies)

-MARA +5.8% (BTC strength)

-PDD +5.1% (Jefferies Raised PDD to Buy from Hold, price target: $157)

-STAA +4.5% (Stifel Nicolaus Raised STAA to Buy from Hold, price target: $50)

-CHH +4.1% (increases share repurchase authorization by 5M shares to 6.8M in total; Wyndham Board sends letter to shareholders noting clear path to deliver shareholder value substantially in excess of Choice's inadequate and uncertain offer; upgraded at Jefferies)

-SILV +4.1% (earnings, guidance)

-EXK +3.2% (earnings)

Downside

-ELTK -10% (earnings)

-FTREX -10% (earnings, guidance; to divest endpoint clinical and patient access businesses to Arsenal Capital Partners for $345M)

-SMCI-4.4% (broker downgrade)

-EQT -4.1% (ETRN confirms to be acquired by EQT at $12.50/shr in all-stock deal)

-VLEEF -2.4% (confirms CEO Bartolomeo extends contract and will stay in the post until Dec 31st, 2024)

-BA -1.8% (weakness from DOJ probe)

BY Doug Kass · Mar 11, 2024, 8:50 AM EDT

BY Doug Kass · Mar 11, 2024, 7:45 AM EDT

BY Doug Kass · Mar 11, 2024, 7:35 AM EDT

BY Doug Kass · Mar 11, 2024, 7:25 AM EDT

I am buying MSOS under $7.80 in the premarket after a negative (but silly) story on the front page of the Wall Street Journal on Saturday.

More on this later in the day!

Long MSOS (M) common (M and calls (S), Short MSOS calls (S)

BY Doug Kass · Mar 11, 2024, 7:15 AM EDT

* The market's steady rise was interrupted last Friday

* Before 11 a.m. on Friday I made a Ludacris Call (it wasn't so ludacris!):

What's Your Fantasy?

A Ludacris Forecast may not be so ludacris!

End of message.

Position: None

BY DOUG KASS MAR 8, 2024 10:58 AM EST

* Futures are a tad lower this morning

* We continue in an overbought condition with the S&P Short-Range Oscillator at 2.84% vs. 3.28%

* Yields are slightly lower (1 basis point) this morning and crude oil prices are modestly higher (+$0.29) -- gold is up again (+$1.60) and Bitcoin is bolting higher (+$2,100)

* The U.S. dollar is losing again vs. the yen.

"Talkin' to myself and feelin' old

Sometimes I'd like to quit

Nothin' ever seems to fit

Hangin' around

Nothin' to do but frown

Rainy days and Mondays always get me down"

- The Carpenters, Rainy Days and Mondays

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

- Bob Seger, "Night Moves"

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures are slightly lower in an expanded range. S&P futures peaked at +5 and bottomed at -22. Nasdaq futures peaked at +12 and bottomed at -111. At 6:09 a.m. ET, S&P futures were -8 and Nasdaq futures at -18.

* Commodities are mixed to higher with Brent crude +$0.19 at $82.28.

* The S&P Short-Range Oscillator remains overbought at 2.84% vs. 3.28% .

* The VIX is making an outsize move and is higher at 15.52 (+0.78).

* The U.S. dollar is weaker against the yen and flat compared to the pound and euro.

* Treasury yields are a bit lower. The 2-Year Treasury yield is flat at 4.492% and the 10-Year is -1 basis point to 4.075%. Over there, the yield on the 10-Year U.K. Gilt bond is -2 basis points.

* Overnight, the inversion of the 2s/10s Treasuries curve is flat at -42 basis points. Real rates remain quite elevated; the 10-year is still about 1.85, again in real terms.

* Gold is +$0.90 and sits at $2,186.

* Bitcoin is +$2,100 to $71K.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

More Market Structure Concerns

Here are Friday's trades (I believe in my Diary's full disclosure and transparency of trades/investments -- this is not CNBC (!). How else can you evaluate the value of my actions without memorializing them?):

* I traded profitably in SPY and QQQ

* On the mid-afternoon rally I re-shorted index calls

BY Doug Kass · Mar 11, 2024, 7:00 AM EDT

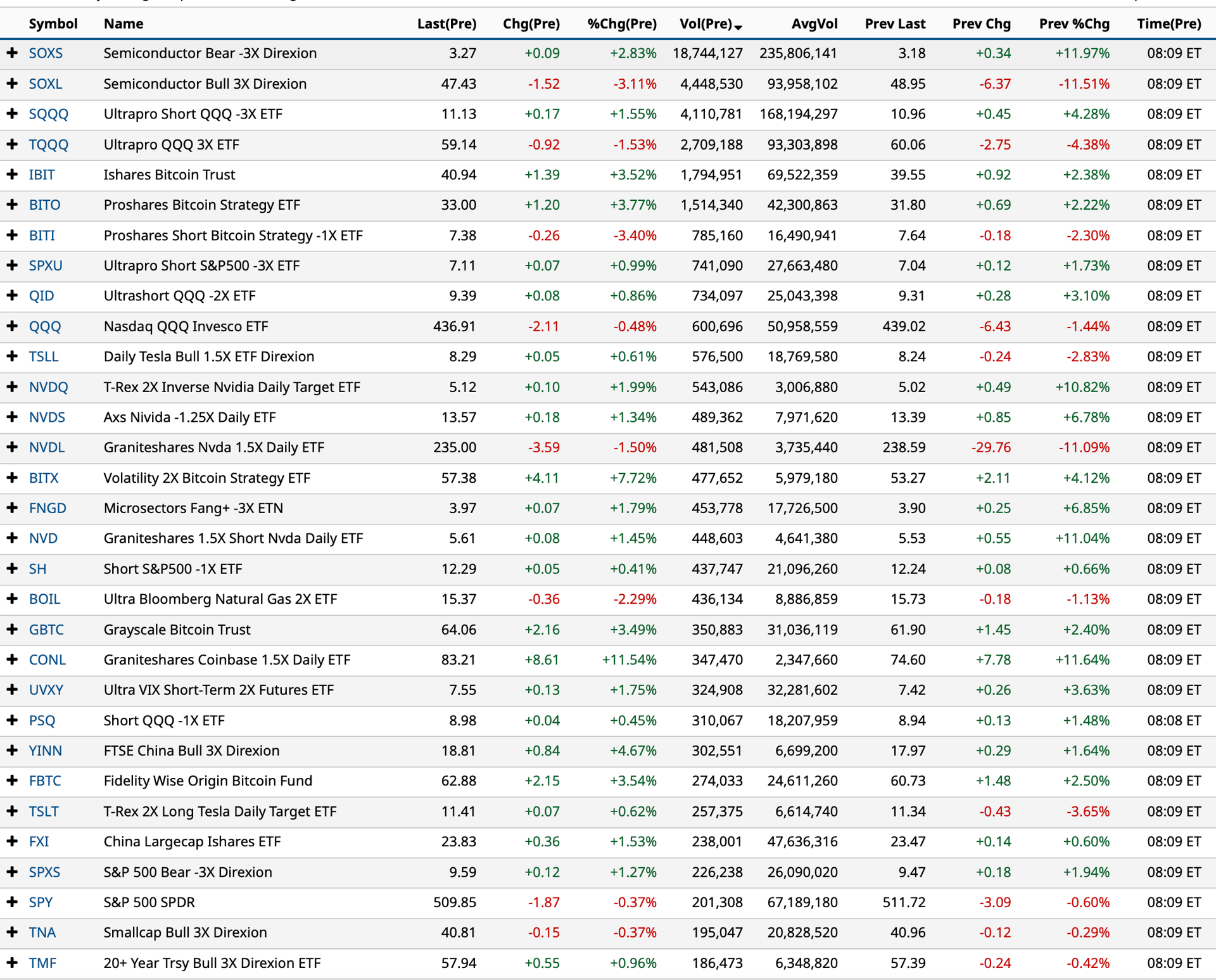

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Mar 11, 2024, 6:50 AM EDT

From JP Morgan:

US: Futs are flat to kick off the week and ahead of tmrw’s CPI print. Friday’s NFP was initially bullish before seeing a strong reversal within TMT and broader mkts, including a 10% reversal for NVDA. NVDA +1.9% pre-mkt and Semis are outperforming Mag7 pre-mkt. Bond yields are mixed with the curve twisting flatter. USD is flat following its worst performing week of the year. Cmdtys are mixed with strength in Energy but weakness in Ags/Metals; base are underperforming precious metals. CPI the focus this week but there are several bond auctions to watch esp. with the potential for BOJ to tweak YCC/ZIRP next week.

and...

EQUITY AND MACRO NARRATIVE: The SPX posted its third negative week of the year but is up 16 of the last 19 weeks, adding 24.4%. The market narrative remains centered on Goldilocks and something between ‘Soft Landing” and ‘No Landing’. Questions on recession have been replaced by question on a second inflation spike, sector rotation, and timing of a pullback so that investors can buy stocks more cheaply. Our tactical bull case remains intact as we approach a series of important catalysts, micro and macro; at/above trend GDP + positive earnings + paused Fed = bull market. That said, it does appear that the market is setting up for a pullback which could be 4-5% but a deeper correction appears unlikely given the strength of the economy. The balance of the note includes (i) update from Positioning Intel; (ii) a look at the Equity rotation and post-Fed pause returns; (iii) US Mkt Intel’s CPI Scenario analysis; (iv) Trading Desk commentary; and (v) a repost of last week’s Bull v. Bear debate with our view and monetization menu.

· ECON – US Chief Economist Mike Feroli increased his GDP forecast. 23Q4 = 3.5%; 24Q1 = 2.25% (up from 1.75%); 24Q2 = 1.5% (up from 0.5%); 24Q3 = 0.75% (up from 0.5%). Feroli thinks rate cuts are coming, beginning in June and sees Fed Funds ending the year at 4.25%.

· EARNINGS – with 99% of the SPX having reported for 23Q4, revenue growth is +4.1% YoY and earnings growth is also +4.1% YoY, according to Factset. Net profit margin is 11.2%. This quarter market the fewest number of companies citing “recession” since 21Q4. Current 24Q1 expectations are for revenue to grow 3.5%, earnings 3.4%, and net profit margin to expand to 11.6%.

· FED / RATES – Powell’s recent comments suggest that the Fed is on track to begin cutting rates this summer. While elevated economic growth is supportive of higher yields, as the Fed begins to cut, that will be the dominant variable. Co-Head of US Rates Strategy, Jay Barry, sees the 10Y yield staying around this level (~4.10%) for the next month but declining into year-end where he has a current 3.80% forecast.

BY Doug Kass · Mar 11, 2024, 6:40 AM EDT

BY Doug Kass · Mar 11, 2024, 6:30 AM EDT

BY Doug Kass · Mar 11, 2024, 6:20 AM EDT

BY Doug Kass · Mar 11, 2024, 6:10 AM EDT

BY Doug Kass · Mar 11, 2024, 6:00 AM EDT