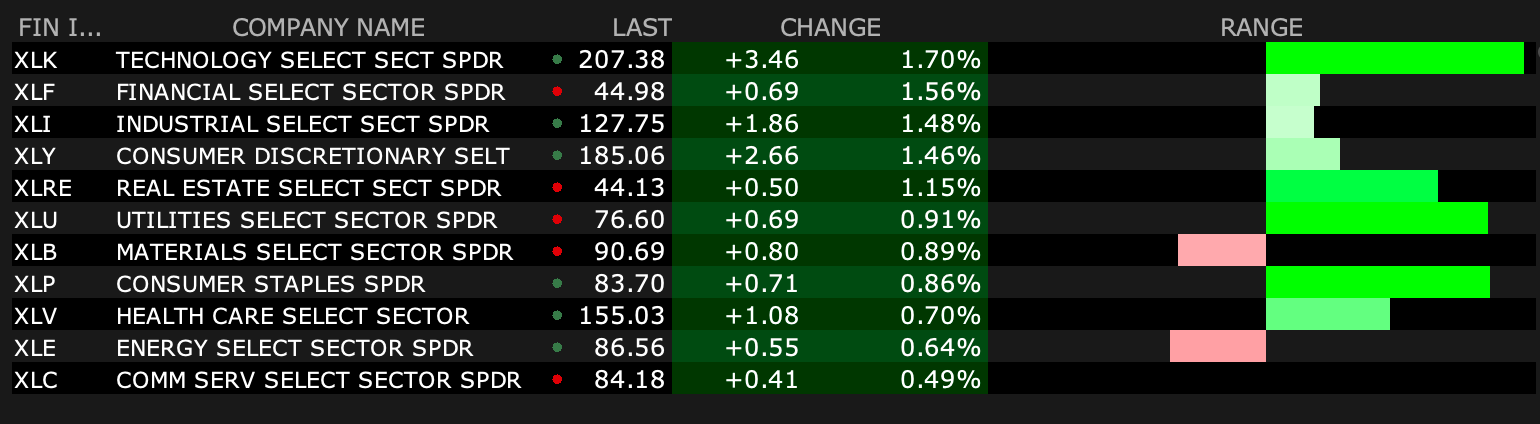

After-Hours Movers

As of 4:23 p.m.:

BY Doug Kass · Sep 9, 2024, 5:05 PM EDT

As of 4:23 p.m.:

BY Doug Kass · Sep 9, 2024, 5:05 PM EDT

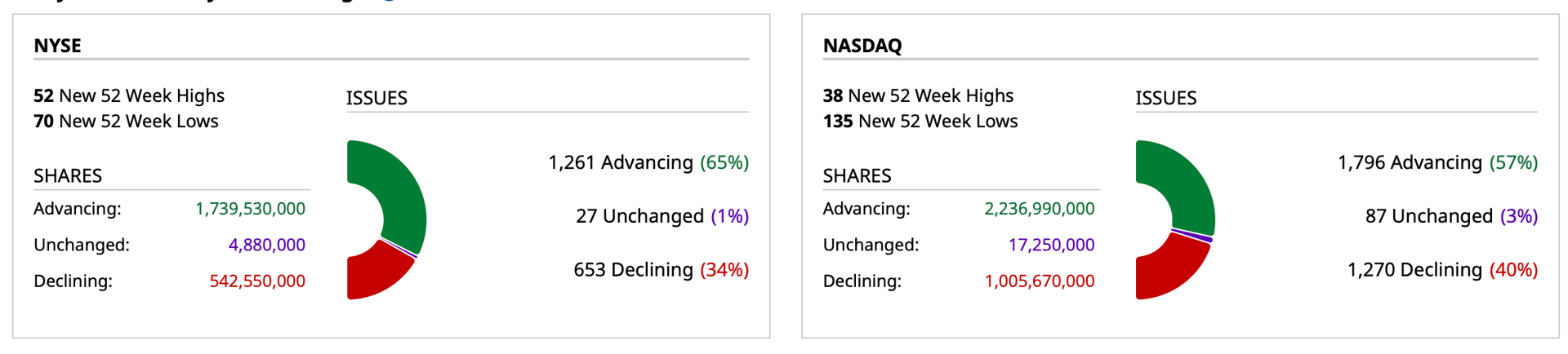

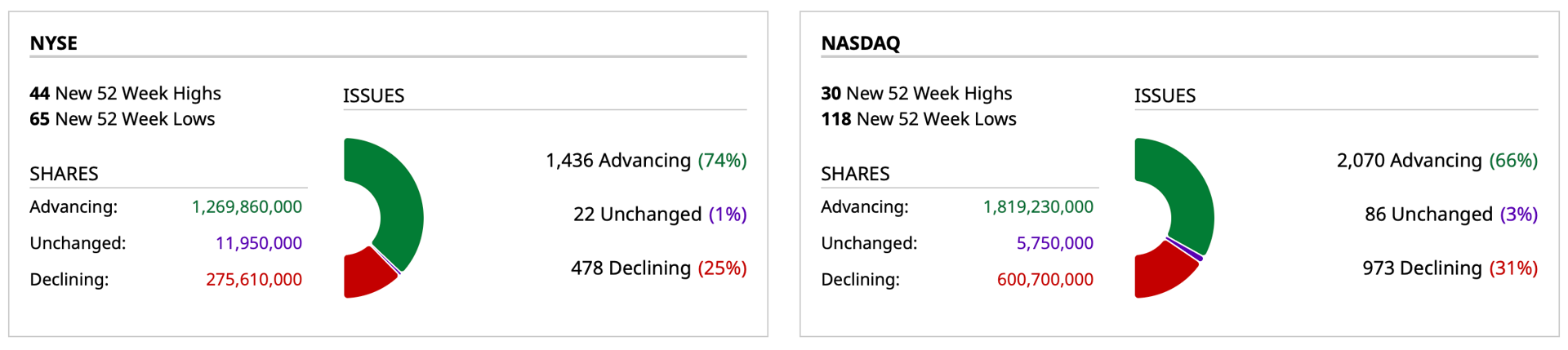

- NYSE volume 10% above its one-month average;

- NASDAQ volume 5% above its one-month average;

BY Doug Kass · Sep 9, 2024, 4:59 PM EDT

* A follow up from the last column...

Longs — DIS $88.25, OIH $26.16.

Short Covers — SPY $543.59, QQQ $452.61.

Shorts — APO $108.35, AXP $252.52, BX $140.04, DHI $189.09, KKR $118.77 and TOL $141.49.

BY Doug Kass · Sep 9, 2024, 3:40 PM EDT

* To stay abreast and as a reminder — I introduced this new column last week.

* Give me feedback in the Comments Section if this is helpful or if you would like me to add anything to the column.

I came into the day modestly net long and almost halved my long exposure:

* I did this principally in the very very early morning — like 4 a.m.! — when I sold out my Index positions (SPY and QQQ) for a quick profit. (I sold out too early!) Note: I currently have no Index longs or shorts.

* I modestly added to longs DIS and OIH.

* I re-shorted what I had covered on Friday's market schmeissing in XLF, XLU, KKR, BX, APO, DHI, TOL — after most of these gapped higher during the day.

* I took a new short position in AXP — after that stock rose by about $9/share.

A market comment: Given the market volatility I am trading around my positions more actively today and over the last few weeks.

Tomorrow I will update my market outlook!

Short XLF S XLU S KKR S BX S APO S DHI S TOL S AXP S

BY Doug Kass · Sep 9, 2024, 3:00 PM EDT

BY Doug Kass · Sep 9, 2024, 2:48 PM EDT

I have watched nearly every Apple AAPL presentation.

This one, thus far, is the most uninteresting.

I made a mistake in covering my short a few days ago.

BY Doug Kass · Sep 9, 2024, 2:38 PM EDT

Re-shorting what I covered on Friday in private equity and homebuilders now — after today's gap higher.

Working with scales higher.

BY Doug Kass · Sep 9, 2024, 1:35 PM EDT

Back short American Express AXP at $252.93.

BY Doug Kass · Sep 9, 2024, 1:26 PM EDT

BY Doug Kass · Sep 9, 2024, 1:20 PM EDT

Adding back to my XLF short ($45.06), which was covered Friday afternoon.

BY Doug Kass · Sep 9, 2024, 12:28 PM EDT

All-time low (and that's a long time!) for investment short Chegg CHGG — now at $1.83.

The shares were added to my Watch List (Best Ideas) (short) on September 19, 2023 at $9.50.

BY Doug Kass · Sep 9, 2024, 12:05 PM EDT

Energy stocks outperforming for the first time since my Bar Mitzvah.

Pressing oil longs.

BY Doug Kass · Sep 9, 2024, 11:10 AM EDT

BY Doug Kass · Sep 9, 2024, 10:55 AM EDT

BY Doug Kass · Sep 9, 2024, 10:46 AM EDT

Adding to OIH, DIS and VVV longs.

Re-shorting (on a scale higher) what I covered on Friday afternoon in private equity (BX, KKR and APO).

BY Doug Kass · Sep 9, 2024, 10:25 AM EDT

From Boockvar: Life is about trade-offs/A few other things

As Federal Reserve rate cuts will certainly ease the pressure off anything/anyone reliant on debt, let's do some very easy math on the flip side of that. That being the beneficiaries of interest income, particularly the lenders to the US government. In the 10 years leading into the first Fed rate increase in March 2022, the average 1 yr T-bill rate was .74%. On $1,000,000 of savings one was receiving $7,400 in annual income pre tax on average. A rate around 5% is of course $50,000 of income. That is quite a difference with the balance paying for many things, including vacations and trips to the restaurants. So, as the Fed cuts rates, those relying on that savings for spending, particularly baby boomers for cruises, and other things, that income will be reduced. In fact, that $50,000 annual income that becomes possibly around $40,000 by year end and to maybe $30,000 by next summer if the fed funds futures is accurate in today's pricing, is the difference in taking that cruise, vacation or buying that $65 filet instead of the $40 chicken.

Bottom line, life is about trade offs and this is one of them as rate hikes and cuts have differing impacts on the economy. And it's not just money in money market funds but also a lot now in CDs that will be affected.

Dollars in Money Market Funds, $6.3 Trillion, much of which previously sat in savings/checking accounts

From ABM Industries, a stock we own, who employees about 125,000 people, talking about the labor market:

"on the labor front, we're feeling really good because wages haven't been rising to the same extent as they were in the last couple of years. And that's been widely publicized, you could read about that. So, that's playing through for us. And also, availability of labor is getting much better for us, as well, in terms of getting people on board quicker." This talk was what we heard from many Districts in the Fed's Beige Book.

Taiwan, the home of Taiwan Semi of course, said exports in August grew by 16.8% y/o/y, about double the estimate of up 8.5% and to a record high. Shipments to the US led the way as we are their top export destination. Their economic ministry said, "August's export value hit a record as business for AI and high-performance computing continued to be strong, as well as international brands stocking up on new products." That said, AI growth is offsetting softness elsewhere as total semi exports fell .5% y/o/y.

China's August CPI rose .6% y/o/y vs .5% in July but one tenth below expectations. The core rate was little changed, higher by .3% y/o/y and has been below 1% for a 6th straight month. Price stability indeed and with the Chinese consumer clearly retrenching, low inflation is a good thing for them.

PPI fell 1.8% y/o/y, more than the forecast of down 1.5%. This is reflecting both the pullback in commodity prices and the manufacturing struggles that the whole world is experiencing.

Chinese stocks sold off, but more following the US weakness Friday rather than in response to this data.

The only thing of note out of Europe was the September Sentix investor confidence index on the Eurozone and it weakened to -15.4 from -13.9. That's the weakest since January. From Sentix, "The economy in the Eurozone remains under pressure...The economy is threatening to tip into recession. Once again. As an EU heavyweight, the German economy is playing a major role in this...The German economy is collapsing in the open. The only hope is that it is probably the 'last days of the traffic lights' that are paralyzing the country."

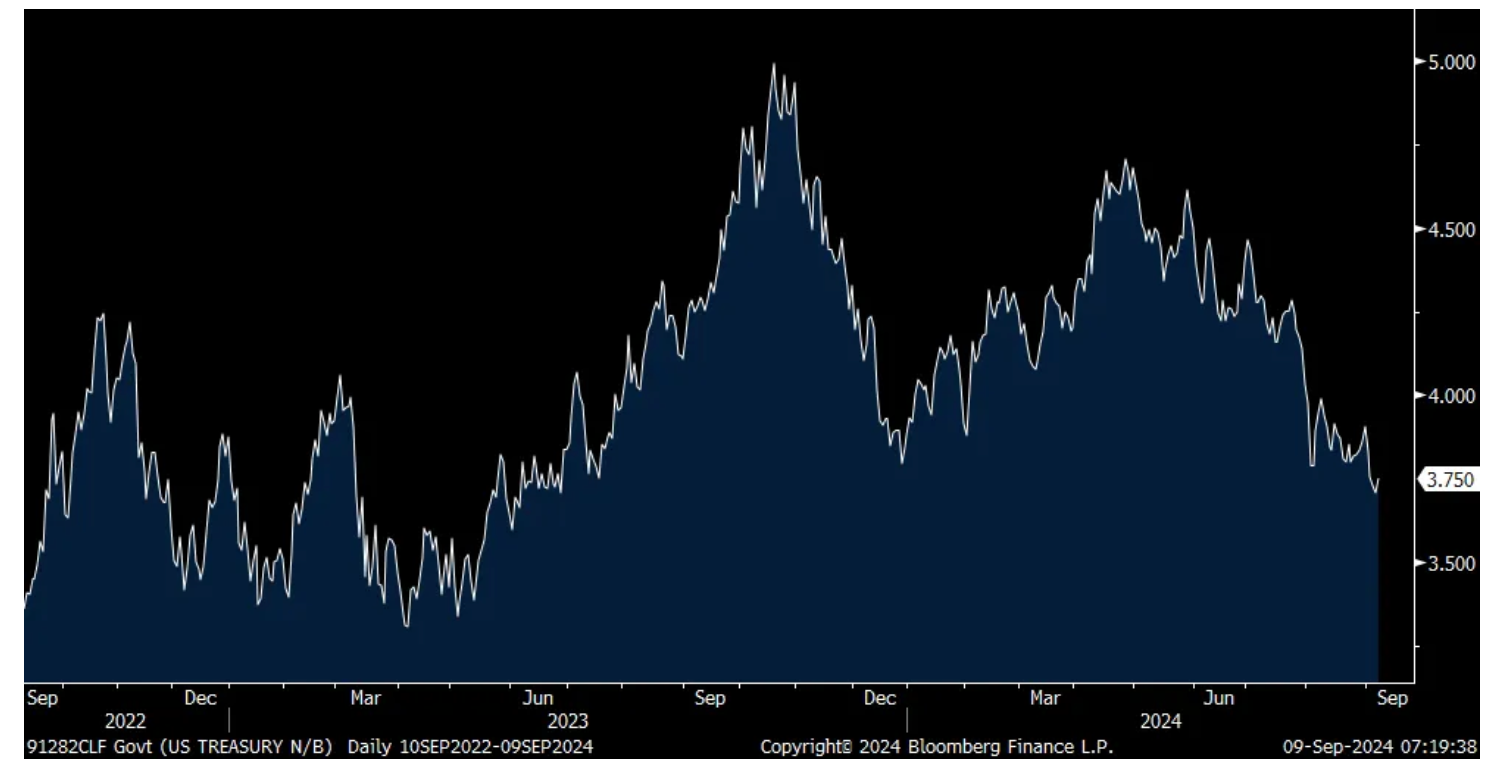

Notwithstanding these comments, somewhat hyperbolic when using the word 'collapsing', sovereign bond yields are higher across the board, but also were too in Asia and with US Treasuries. The dollar is higher too. With respect to US Treasuries, at least for now, and I think it will continue to, the 3.70-3.75% ish rate level on the 10 yr yield continues to hold. Again, that was the launch point last year for the trip to 5% triggered by the end of yield curve control in Japan.

Sentix

US 10 yr yield

BY Doug Kass · Sep 9, 2024, 10:15 AM EDT

I finally got a clearer picture of how much money Open AI loses. (Although one could have inferred this based on how much money they have raised... and how quickly they needed to raise more money).

The article below is self-explanatory: "Report claims that OpenAI has burned through $8.5 billion on AI training and staffing, and could be on track to make a $5 billion loss."

I guess one more reason why investors like Microsoft MSFT want the valuation marked up - is that way they don’t become the majority owner and don’t have to consolidate it on to their own books!

This whole thing started as a non-profit, even though it is no longer technically a non-profit. It is still obviously a non-profit of epic proportions!

Unrelatedly, it does appear Elon Musk has successfully re-filed his lawsuit. It will be interesting how it goes and what the implications are if he wins. It is in Federal Court now so I presume he has a chance.

Frankly, the whole Open AI thing really is shady in my view, soup to nuts what is going on: https://www.cnn.com/2024/08/05/business/elon-musk-new-lawsuit-openai-sam-altman/index.html

BY Doug Kass · Sep 9, 2024, 9:45 AM EDT

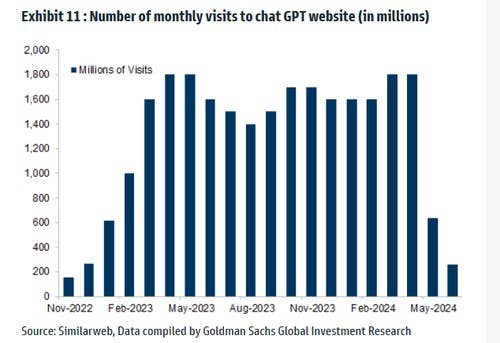

Here is a follow-up thought on this chart showing Chat GPT visits falling off a cliff.

I wonder if part of that is due to kids being away from school and no longer using it to help them cheat on their homework (and of course in school these days hallucinations get you an A+). But if that is the case, there is a huge problem here. If 70%-90% of the user base was kids, who can never pay much for the service and most probably use the free version, there was never ever a there there to begin with. This is about the most low quality user base a business can have. And it also shows you how little traction they were getting in the real world for actually productivity enhancing paid work.

Regardless, the other important takeaway is how quickly it went flat after the initial spike, very early in its theoretical growth cycle. Any growth biz the trajectory inflects up and steepens early and that s curve continues for a long long time. This thing almost instantly flattened after a few months even prior to the competitive models being introduced. That speaks volumes about the value proposition even when it was being given away for free.

Then I keep thinking about the current funding round, and why anyone would do it at such a beefy, and continually marked up valuation. Here is what I can come up with:

* Nvidia NVDA invests in its big customer (again) shady, but legal

* Apple AAPL and MSFT made a bet on the thing as part of their own offerings, they have to keep it in business, and for them they keep all the losses off their own books. Somewhat shady, but legal

* Thrive, well they did the original tender for Open AI as best as I can tell, and they don’t want to see it go under, and nobody wants a down round, so the valuation keeps getting pushed up.

Open AI loses money at auspicious rates, and they keep having to go back to the well. They just did their tender at an $80 billion valuation in February, and are already back to fundraising and they need tons of money: "OpenAI's massive operating costs could push it close to bankruptcy within 12 months."

This cannot happen forever. The business is valued at a point and positioned in a place where they seemingly can only attract money from those who are already tied to it, as opposed to substantial new external capital. The valuation can’t keep getting pushed up, just for the sake of pushing it up so there is not a down round and cap table chaos. There are limits, the game cannot go on forever.

The accounting in this whole industry is really aggressive for lack of a better term:

1. Apple and MSFT keep the losses off the books

2. NVDA invests in their customers

3. The depreciation schedules throughout the industry are nuts. Servers and the silicon given much too long of a useful life, in real terms they depreciate much more rapidly than in accounting terms

4. Then all the stuff going on with Super Micro and some of the other players

5. Then where parts actually end up going directly or indirectly relative to export controls

Again, the chart:

BY Doug Kass · Sep 9, 2024, 9:30 AM EDT

Chart as of 8:14 a.m. ET:

BY Doug Kass · Sep 9, 2024, 9:12 AM EDT

As of 8:22 a.m. ET:

BY Doug Kass · Sep 9, 2024, 9:00 AM EDT

Now I understand why the venture capitalists want to pile into Open AI at a $100 billion valuation.

It is quite the growth business (sic), really broadening the user base. My bad!

My read of the chart above is that people thought it was a fun cute little toy at first. Everybody wanted to play with it and then most everyone found the output not very useful, and it stopped being entertaining to play with it. Probably why they are also trying to charge $2,000 per month for their newer advanced models (strawberry and orion - OpenAI Considers Higher Priced Subscriptions to its Chatbot AI; Preview of The Information’s AI Summit), because they are trying to make up units with price.

Although, I still have no idea who is going to pay $2,000 per month, what they will use it for, and what the newer models do that the prior ones don’t, if they even work well at what they are purported to do, which I highly doubt…

BY Doug Kass · Sep 9, 2024, 8:45 AM EDT

Per More Tales From Nvidia (previous column!), I should have added, maybe Open AI should ask for their Nvidia NVDA parts for free too?

Sam Altman, one of the world’s greatest con men in my view, again I have never seen anything like this.

Like the article's author, Stephen Green in PJ Media, says – duck cough!

OpenAI is begging the British Parliament to allow it to use copyrighted works because it's supposedly "impossible" for the company to train its artificial intelligence models — and continue growing its multi-billion-dollar business — without them.

As The Telegraph reports, the AI firm said in a filing submitted to a House of Lords subcommittee that using only content from the public domain would be insufficient to train the kind of large language models (LLMs) it's building, suggesting that the company must therefore be allowed to use copyrighted material.

The company's complaint claims that "Because copyright today covers virtually every sort of human expression — including blog posts, photographs, forum posts, scraps of software code, and government documents — it would be impossible to train today's leading AI models without using copyrighted materials."

What they mean is, "It would be uncomfortable to our bottom line if we had to pay for the copyrighted materials we'd much rather just take from its owners."

-PJ Media

BY Doug Kass · Sep 9, 2024, 8:25 AM EDT

This one takes the cake.

And I thought I had seen everything.

No idea why these Thrive guys want to pile in.

But I do understand why MSFT does – they get to keep all the losses off their books!

BY Doug Kass · Sep 9, 2024, 8:10 AM EDT

* Trump's support is a strong positive for the cannabis space

* This news is particularly important to Trulieve (which we have been adding to)

On Sunday former President Trump tweeted out his explicit support for liberalizing recreational use of cannabis and specifically stated he would vote yes to Amendment 3 in Florida:

I recently slanted my writings towards the direction that Trump would be supportive — and that cannabis stocks were particularly attractive:

As well, I had positive remarks in my pal Jason Spatafora's "Higher Spaces" on Twitter (4) Jason Spatafora (@WolfOfWeedST) / X on September 5th.

And my column from last week:

* As expected, cannabis equities have had a dull reaction to Trump's positive (but vague) comments over the weekend.

* While his remarks will not materially impact the Florida vote on recreational use, fears that Trump might stop or interrupt cannabis rescheduling have now been greatly reduced.

* Given the muted share price response and the favorable longer term reward v risk - I am adding to MSOS at $6.35.

As noted in my weekend tweets (published here earlier this morning) and in the tweet below, I did not expect an appreciable bump in cannabis equities on the indistinct Trump comments on Saturday:

That said (and tweeted), I am now adding to (MSOS) at $6.35 based on the muted reaction.

“You keep using that word. I do not think it means what you think it means.”

- Inigo Montoya, The Princess Bride

This is an investment and not a trade — as it is unclear, to me, that Trump's vague comments will materially influence the Florida Amendment 3 vote (see Princess Bride quote above!).

Also, his comments will not likely influence the recently delayed timing of a rescheduling of cannabis (which seems to have been delayed from 4Q2024 to approximately 2Q2025).

However, it is important to note that Trump's comments will likely reduce the fear on the part of investors that progress on the rescheduling process (or the rescheduling itself) would be interrupted in a possible Trump Presidency.

And that (previous) possibility was an important concern and unknown factor to cannabis companies and investors.

That fear has now been considerably diminished.

On a longer-term basis, cannabis equities provide an exciting upside reward vs. downside risk.

Position: Long MSOS (L)

By Doug Kass Sep 3, 2024 12:35 PM EDT

BY Doug Kass · Sep 9, 2024, 8:00 AM EDT

BY Doug Kass · Sep 9, 2024, 7:50 AM EDT

and...

BY Doug Kass · Sep 9, 2024, 7:40 AM EDT

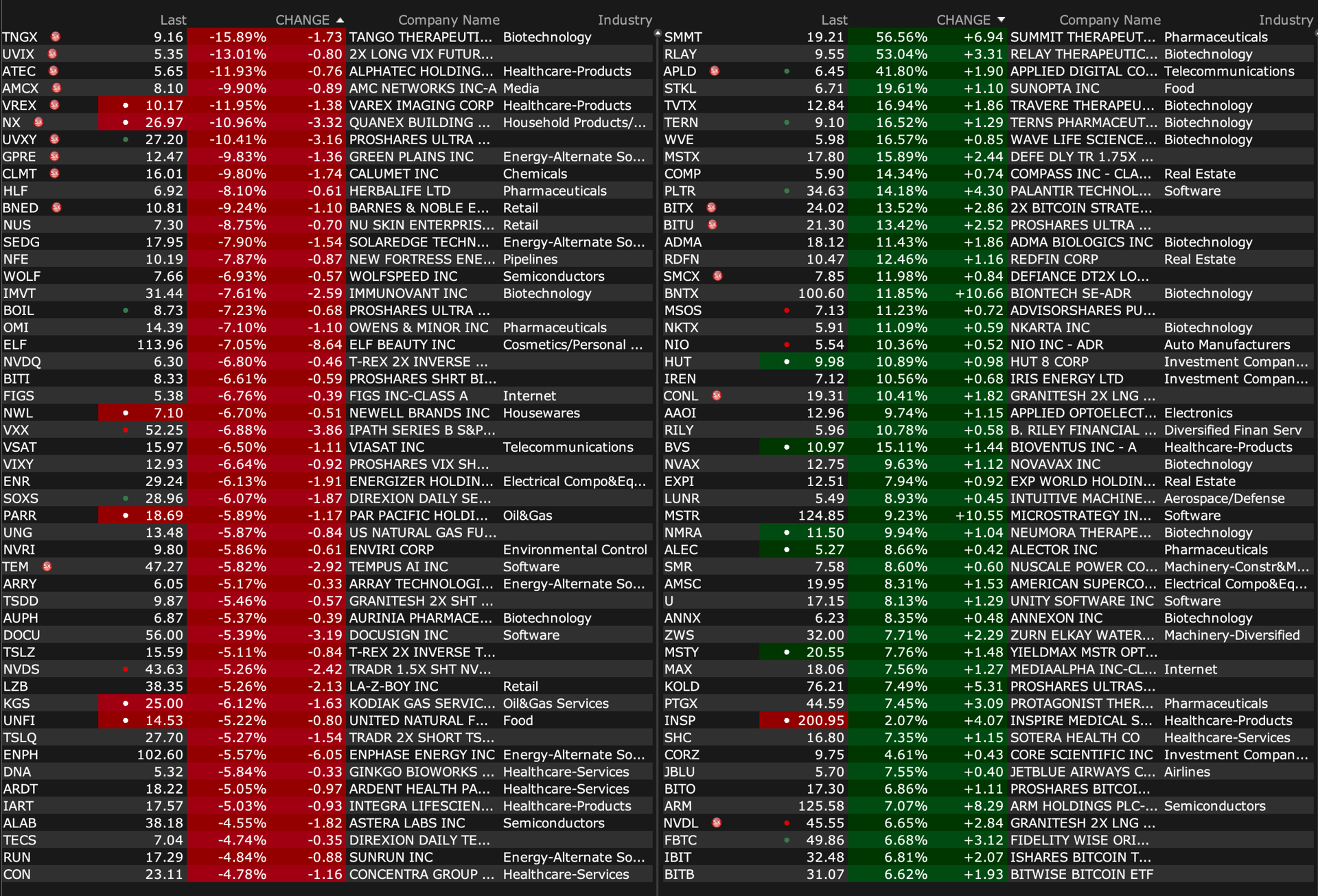

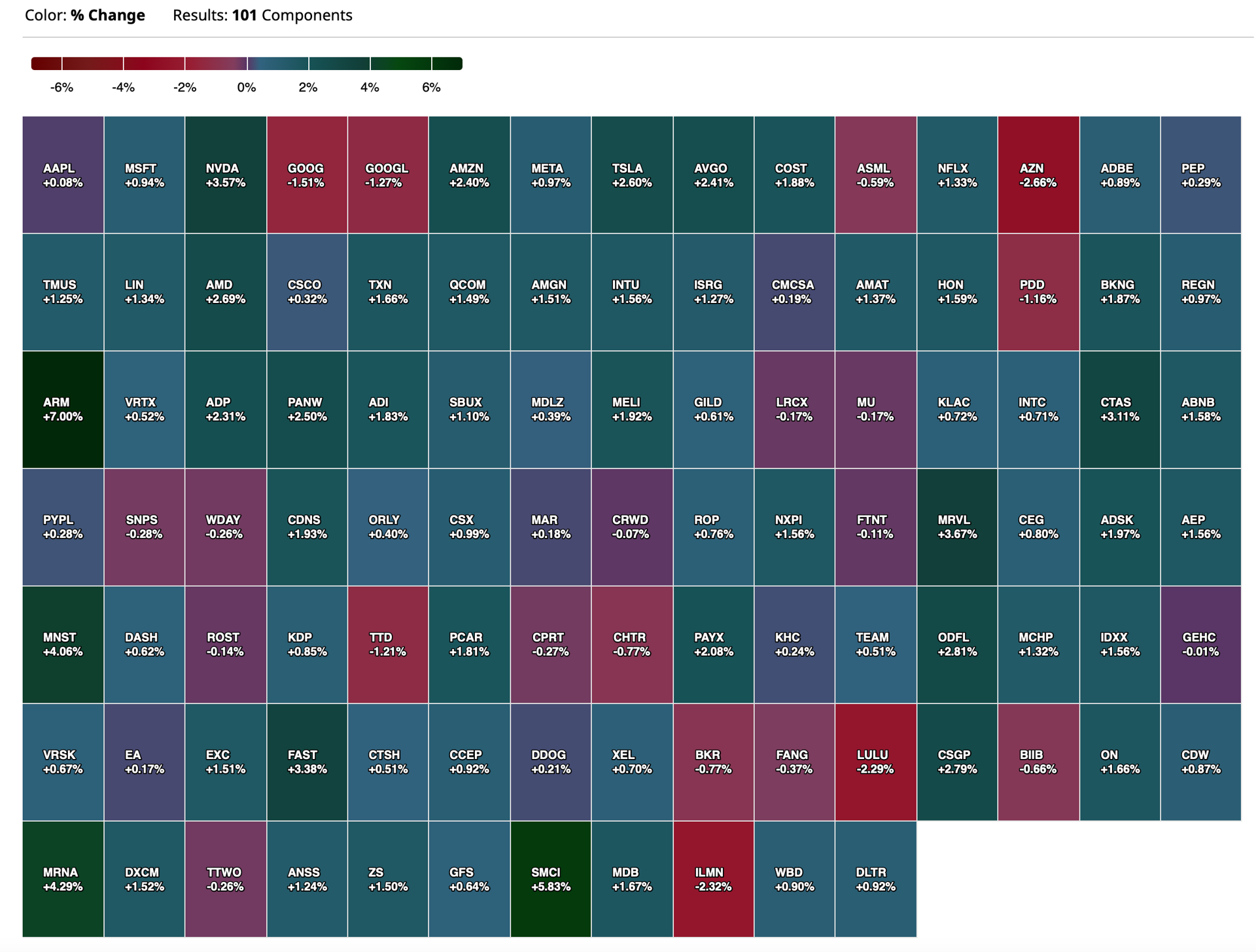

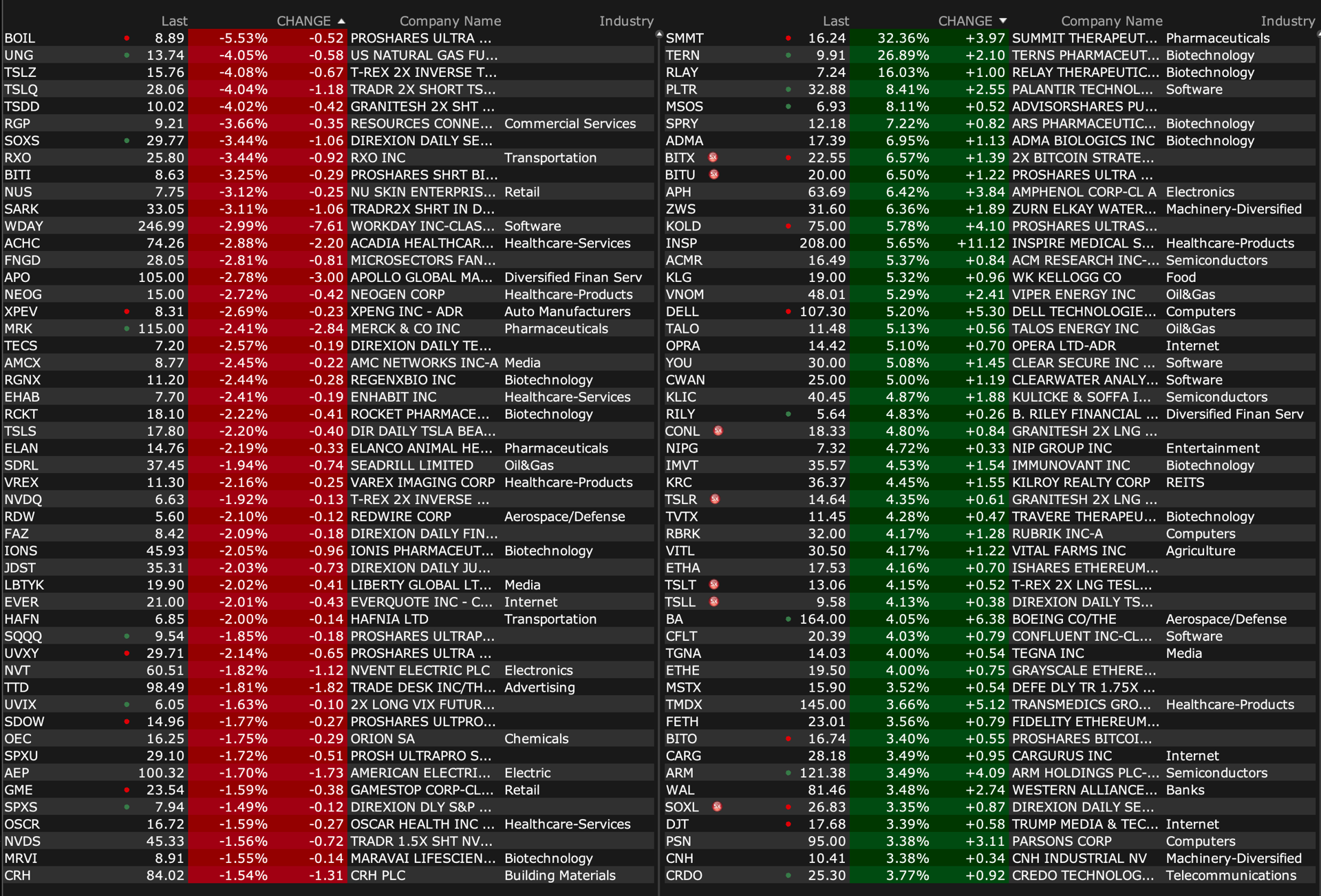

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Sep 9, 2024, 7:30 AM EDT

From JPMorgan:

US: Futs are higher as US sees a relief rally following the worst weekly loss of the year. Pre-mkt, Mag7 and Semis are higher along with new index additions. Bond yields are higher by 4-5bps aiding gains in the USD. Cmdtys are mixed with Energy higher and Ags/Metals lower but with soft patches of strength in base/softs. We enter a week with several major questions to answer and add’l macro data points: near-term or deadcat bounce? 25 or 50bps? Who leads the election? Is AI dead? We attempt to answer these questions in today’s macro narrative.

and...

EQUITY AND MACRO NARRATIVE: Last week, SPX lost 4.3% outperforming the NDX and RTY which lost 5.9% and 5.7%, respectively. When considering seasonality, the SPX has averaged a -4.23% September return over the last five years and -1.65% this century. In either case, we saw a month’s worth, or more, of negative seasonality in the first week of the month. Similar to the vol-shock experienced in early August, there are similar variables, which is to say that this is not a move driven by weakening US fundamentals. My colleague Marissa Gitler did a comprehensive dissection on this phenomenon, and she identified six factors driving both the initial vol-shock and what appears to be last week’s aftershock: (i) Dovish-leaving Fed setup post-Jackson Hole; (ii) Hawkish BOJ commentary; (iii) Bid for US Treasuries; (iv) Equity index futures-led downtrade; (v) Sharp VIX spike; and, (vi) Selling in Equity single names/crowded longs. Please reach out if you would like her full note. Where from here? We spend the balance of the note walking through various facets of the market and our conclusion is here:

· US MKT INTEL TACTICAL VIEW – Tactically Cautious. Longer-term Bullish. When S&P released the Final PMI-Services, their Chief Economist noted that their data points to a 2% - 2.5% growth forecast for 24Q3. Coming off a 3% 24Q2 with corporate profits at record highs, with expanding margins, that the fundamental story is stronger than is reflected by recent Equity price action. Is it more likely that we see growth crater over a 1-2 month period and that Equity price action is reflective of that reality or is it more likely that negative seasonality, stretched TMT positioning, and heightened uncertainty triggered another pullback? I think the latter and think we will see the market set new ATHs this year but recognize that the next 2-3 weeks may be tricky in terms of navigation.

BY Doug Kass · Sep 9, 2024, 7:20 AM EDT

As evidenced by the Boeing BA labor agreement, labor inflation remains an issue and will likely contribute to sticky inflation:

Boeing reaches tentative labor deal with 25% pay hike, new plane commitment | Reuters

BY Doug Kass · Sep 9, 2024, 7:10 AM EDT

Another solid observation from Hedgeye's Keith on Friday's higher volume accompanied by lower prices:

BY Doug Kass · Sep 9, 2024, 7:00 AM EDT

* As I have often written, there are many good charts that lie in the bottom of the sea

* Regarding this featured column (Charting the Technicals), I remarked when stocks were recently breaking out to the upside, the technical comments were universally (and confidentally) bullish

* In the last two days we see the opposite — as the discussion of breakdowns are prevalent

* Interpret this (and use this) — just as you do the Short Range S&P Oscillator and other sentiment indicators, as you wish...

Bonus — Here are some great links:

BY Doug Kass · Sep 9, 2024, 6:45 AM EDT

BY Doug Kass · Sep 9, 2024, 6:35 AM EDT

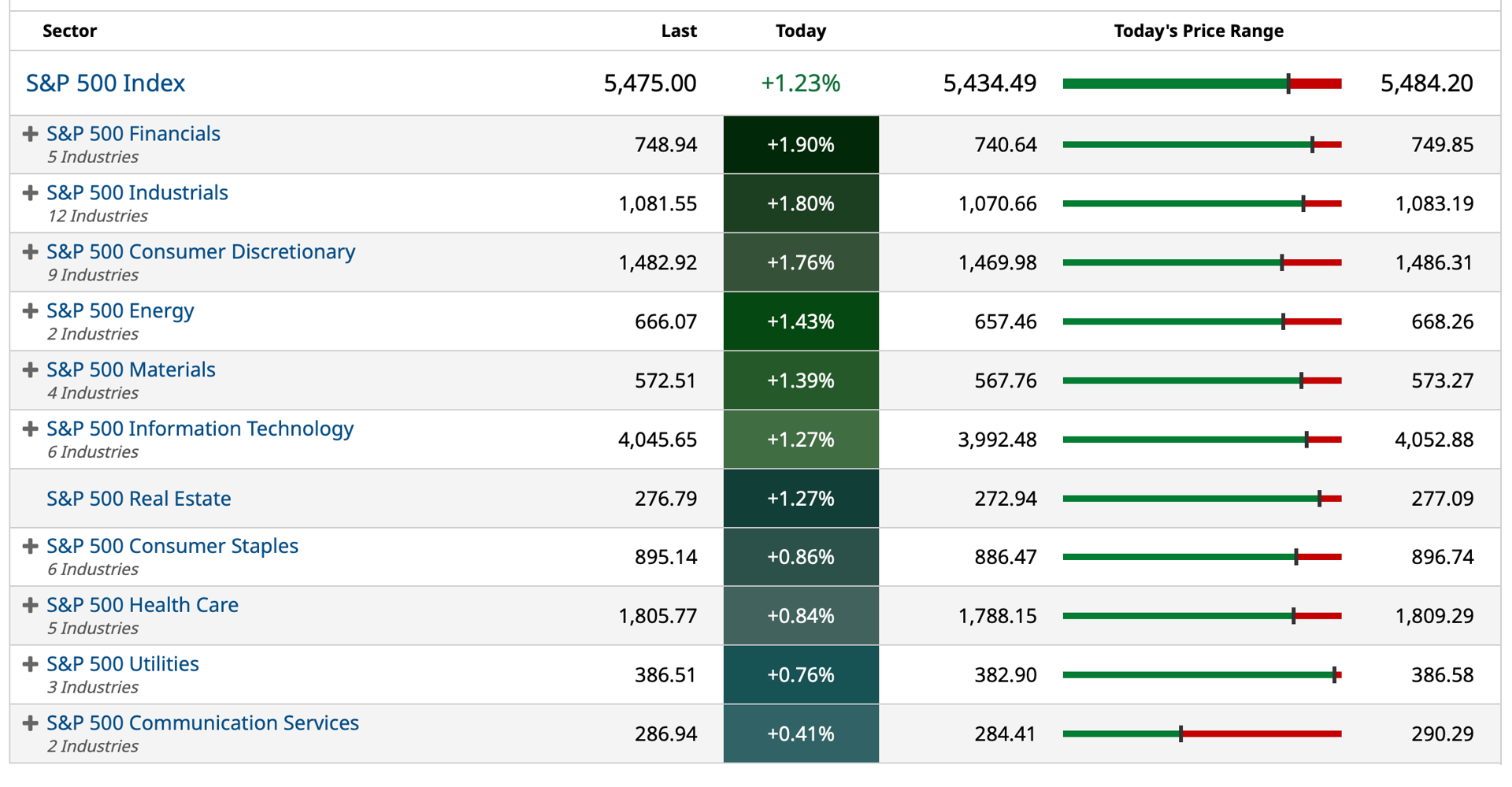

* This is a wonderful table...

BY Doug Kass · Sep 9, 2024, 6:25 AM EDT

BY Doug Kass · Sep 9, 2024, 6:15 AM EDT

BY Doug Kass · Sep 9, 2024, 6:05 AM EDT

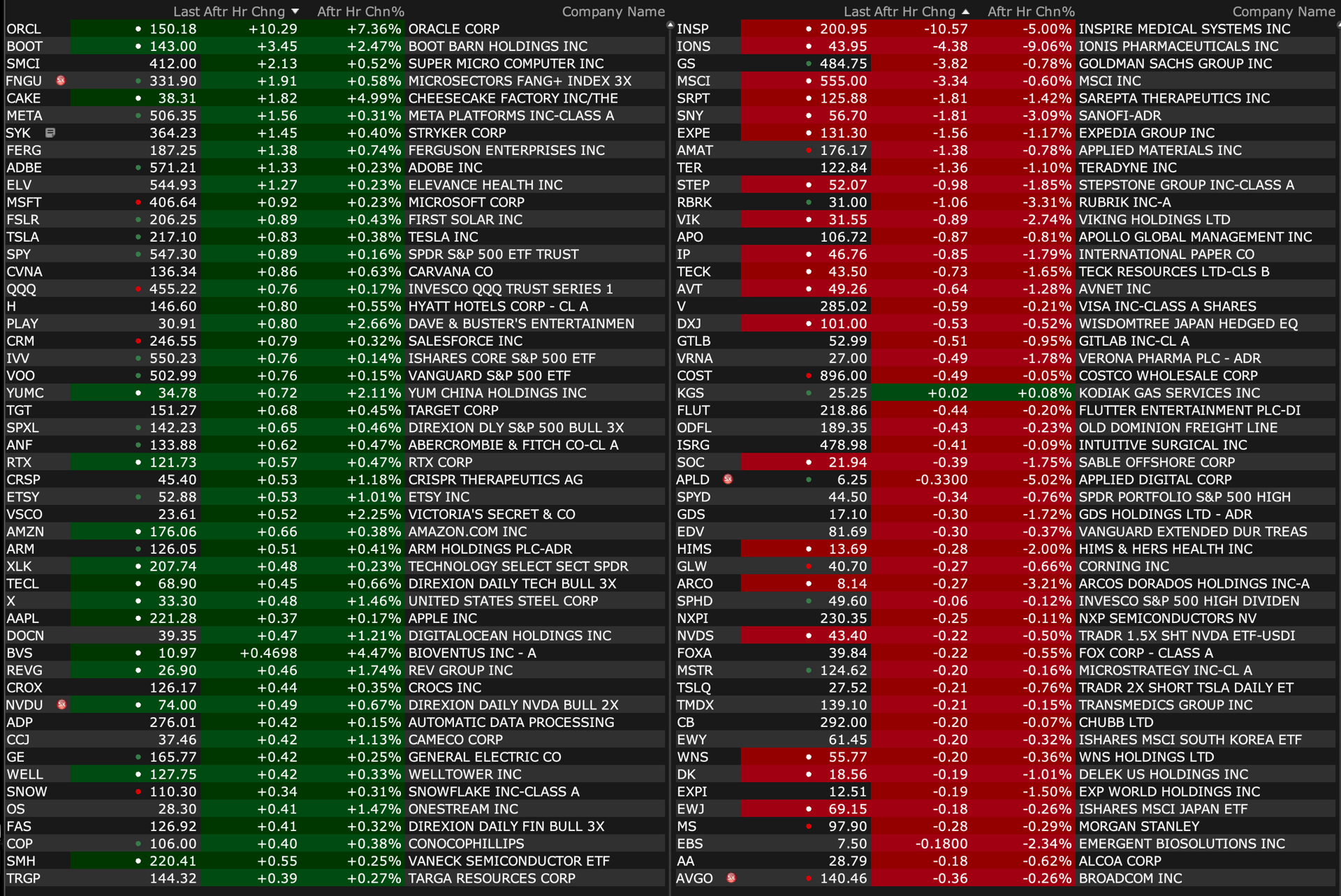

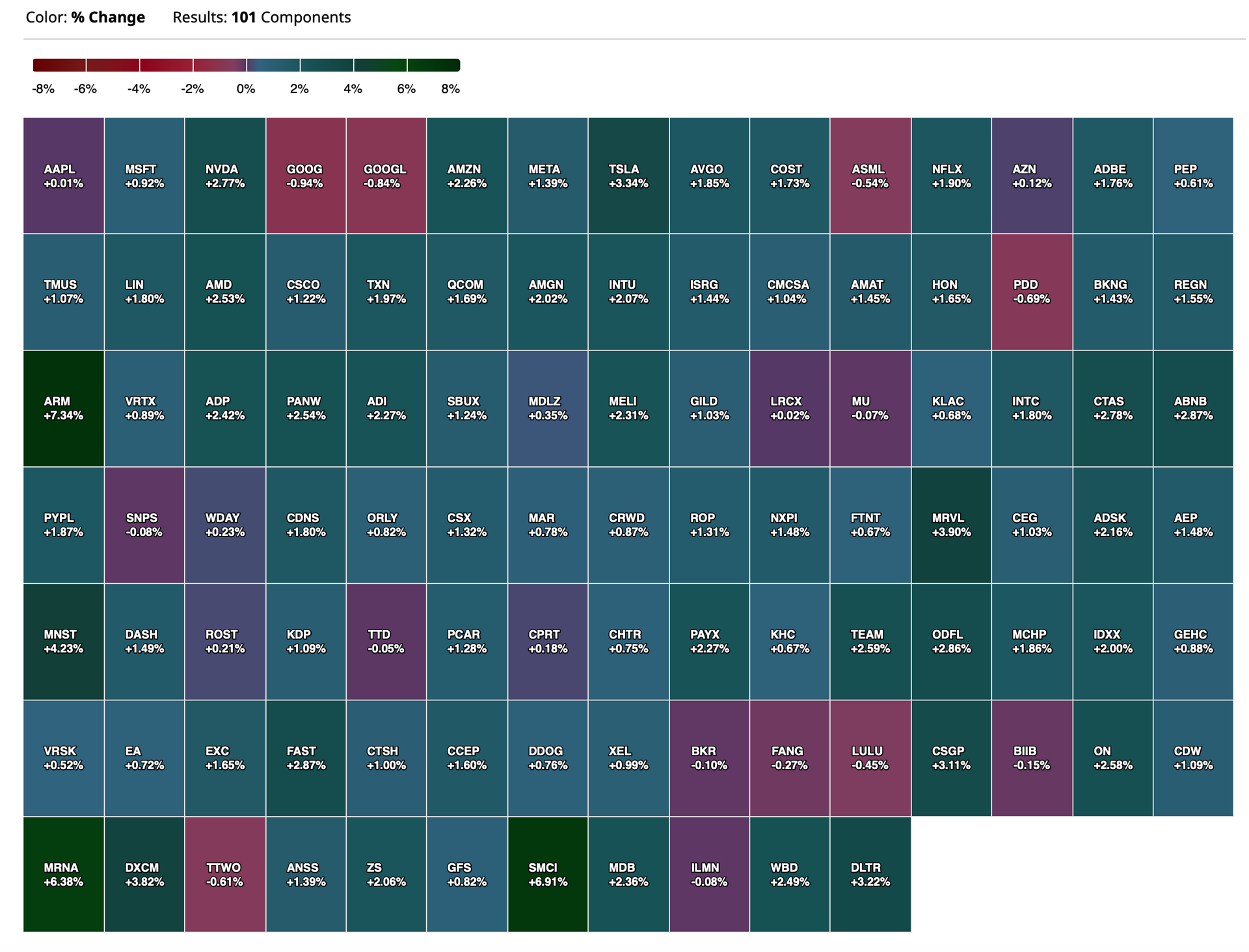

* Friday after hours and Monday (very early) trading...

Dougie Kass

8 hours ago

I was active covering a large number of shorts on Friday's market schmeissing - including but not restricted to a portion of my XLF, JPM, XLU, TOL, DHI, AAPL, APO, BX and KKR shorts.

I also took a trading LONG rental in SPY $538.80 and QQQ $447.15 in the after hours (6PMish).

A lot to be discussed on Monday morning!

Dougie Kass

1 hour ago

At 402 AM Monday - sold LONGS SPY $543.59 and QQQ $452.61. No position in Indices now.

BY Doug Kass · Sep 9, 2024, 5:54 AM EDT

Wolf Street on the predictive ability of the yield curve inversion.

BY Doug Kass · Sep 9, 2024, 5:45 AM EDT