According to the players on FIN TV (after the close) it seems they believe that all the technical and fundamental indicators are being bypassed by the calendar (i.e., September is a weak market month).

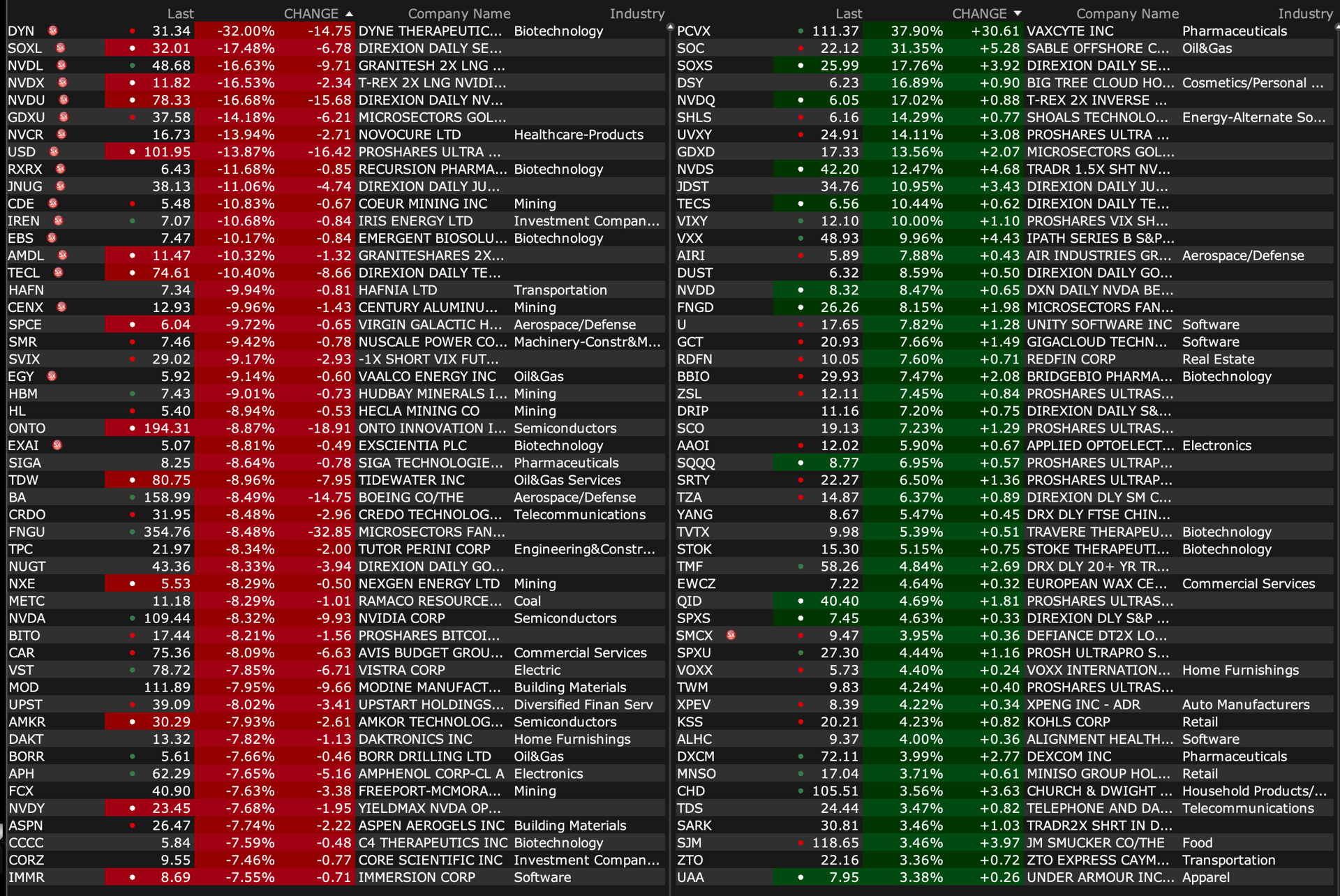

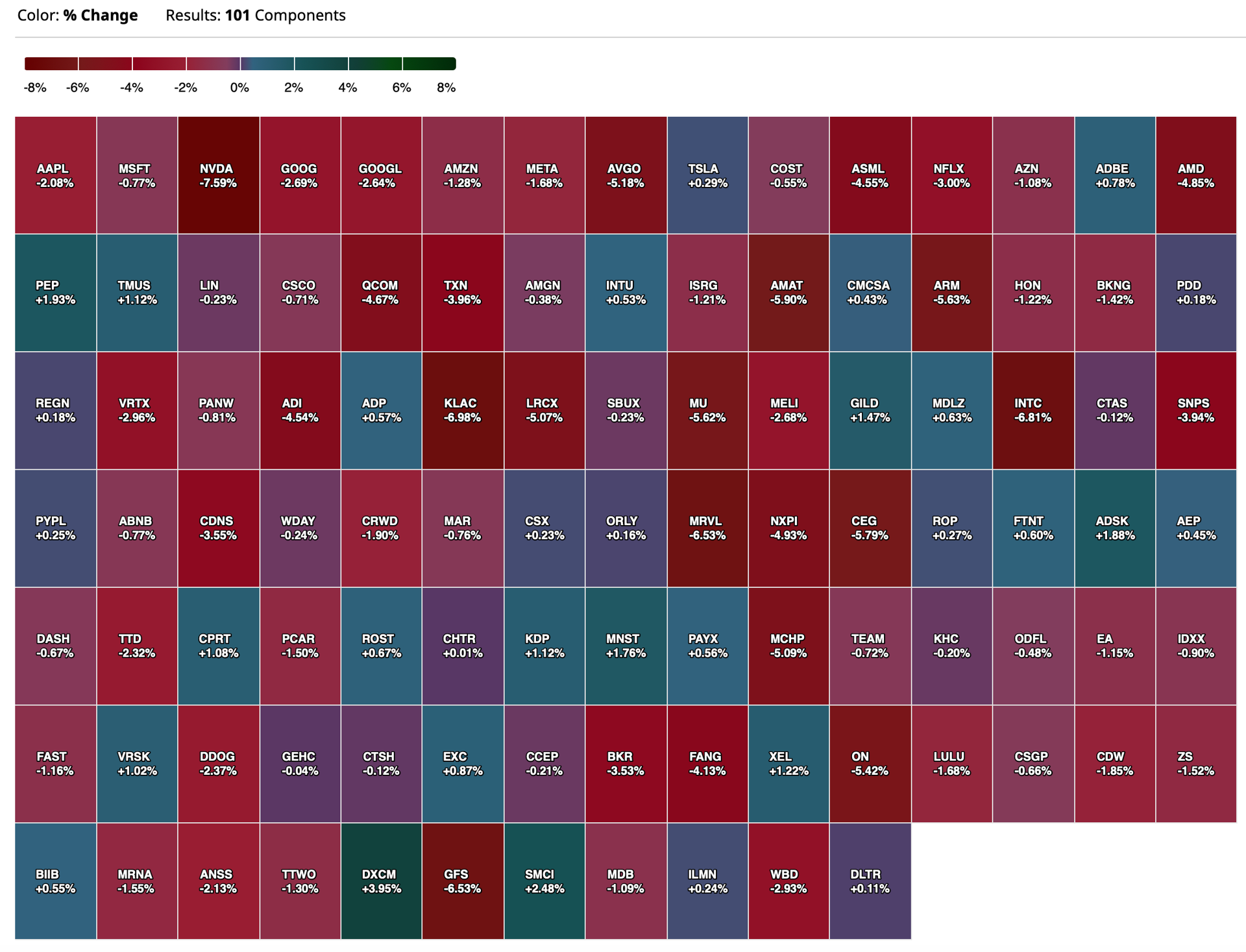

Bad economic news out of Europe today. I don't trust much that comes out of China, but almost all reports indicate their economy is getting worse, if not already in dire straits. The USA economy macro numbers continue to be ok, but any look behind the curtain indicates things are not as great as advertised. At least to this observer, the facts on the ground are not yet reflected in government numbers. If Doug K's continued reminders of AI/NVDA fails ring true, even the next tech revolution is in doubt. It is hard to imagine the fanciful projections for the world's economy not being revised lower.

I cannot envision central banks having much alternative to continued liquidity support, as longer term solutions require governments making difficult decisions which their countries populace are unlikely to support.

This leaves many investors like myself in a conundrum. I am not able to trade as adroitly as Doug K et al, as he has so correctly pointed out, shorting is hard, and I have not been very good at it. What has worked for me for the last ten years is not working right now, and a return to the growth of the last decade is getting more unlikely.

Gold should benefit in such times, but again, my long term experience has shown it can be very disappointing. I have not sold what I have owned for many years.

If BTC turns out to be a real thing, which I am becoming more convinced of, it should also benefit in such a world. However, it remains outside of the universe of most investors, and it's lack of classic valuation parameters makes analysis at best idiosyncratic and at worst fanciful. Prudence dictates limiting allocations.

Fairly valued, growing companies in a thriving economy are wonderful investments, but are getting a lot harder to find. I would not characterize the present day market in such terms.

More cash, lower expectations, and higher stops until something changes.

Moores law. As we come to its subatomic closure. There are a few more efficiencies to be gained. And the next distant wave of the future very well may be quantum. And a new quantum law that people follow for the next 40 years. Maybe 10 years from now quantum will begin to come to fruition. Who has the cash flow to develop? Surprise! The mag 3 and they are all doing it. Just as they did investing in the cloud without immediate reward. The future imho is obvious and positive and beyond my imagination. I will be too old to participate. I’ve been a day trader for 40 years. Before it was a term. Before internet. It was awful frankly. I suppose we have another year or two of some great trades and gains. I am not in love with nvda but what great trading it is presenting. The media can not panic investors into thinking the AI trade is dead just yet. Only create this magnificent day trading opportunity ! 1. China can not buy American chips. BS. The backlog was 2 years without china . Probably still is. 2. No one is getting a return on their money from AI. The cloud took time. I believe those were pretty good investments. 3. Where else are the mag 3 going to put their money? Has anyone noticed that it is now politically impossible to make a buyout? I remember when google bought YouTube for ? 22 billion???? Don’t recall but the stock crashed. Bottom line is that I am disappointed in the Political social and media critique of big tech. They are still the future. Or would we prefer that another country less governed should take the technological lead. I wish everyone the best in your individual investment decisions. Just keep swimming.

I Don't Think Those Words Mean What You Think They Mean

* As expected, cannabis equities have had a dull reaction to Trump's positive (but vague) comments over the weekend.

* While his remarks will not materially impact the Florida vote on recreational use, fears that Trump might stop or interrupt cannabis rescheduling have now been greatly reduced.

* Given the muted share price response and the favorable longer term reward v risk - I am adding to MSOS at $6.35.

As noted in my weekend tweets (published here earlier this morning) and in the tweet below, I did not expect an appreciable bump in cannabis equities on the indistinct Trump comments on Saturday:

This is an investment and not a trade — as it is unclear, to me, that Trump's vague comments will materially influence the Florida Amendment 3 vote (see Princess Bride quote above!).

Also, his comments will not likely influence the recently delayed timing of a rescheduling of cannabis (which seems to have been delayed from 4Q2024 to approximately 2Q2025).

However, it is important to note that Trump's comments will likely reduce the fear on the part of investors that progress on the rescheduling process (or the rescheduling itself) would be interrupted in a possible Trump Presidency.

And that (previous) possibility was an important concern and unknown factor to cannabis companies and investors.

That fear has now been considerably diminished.

On a longer-term basis, cannabis equities provide an exciting upside reward vs. downside risk.

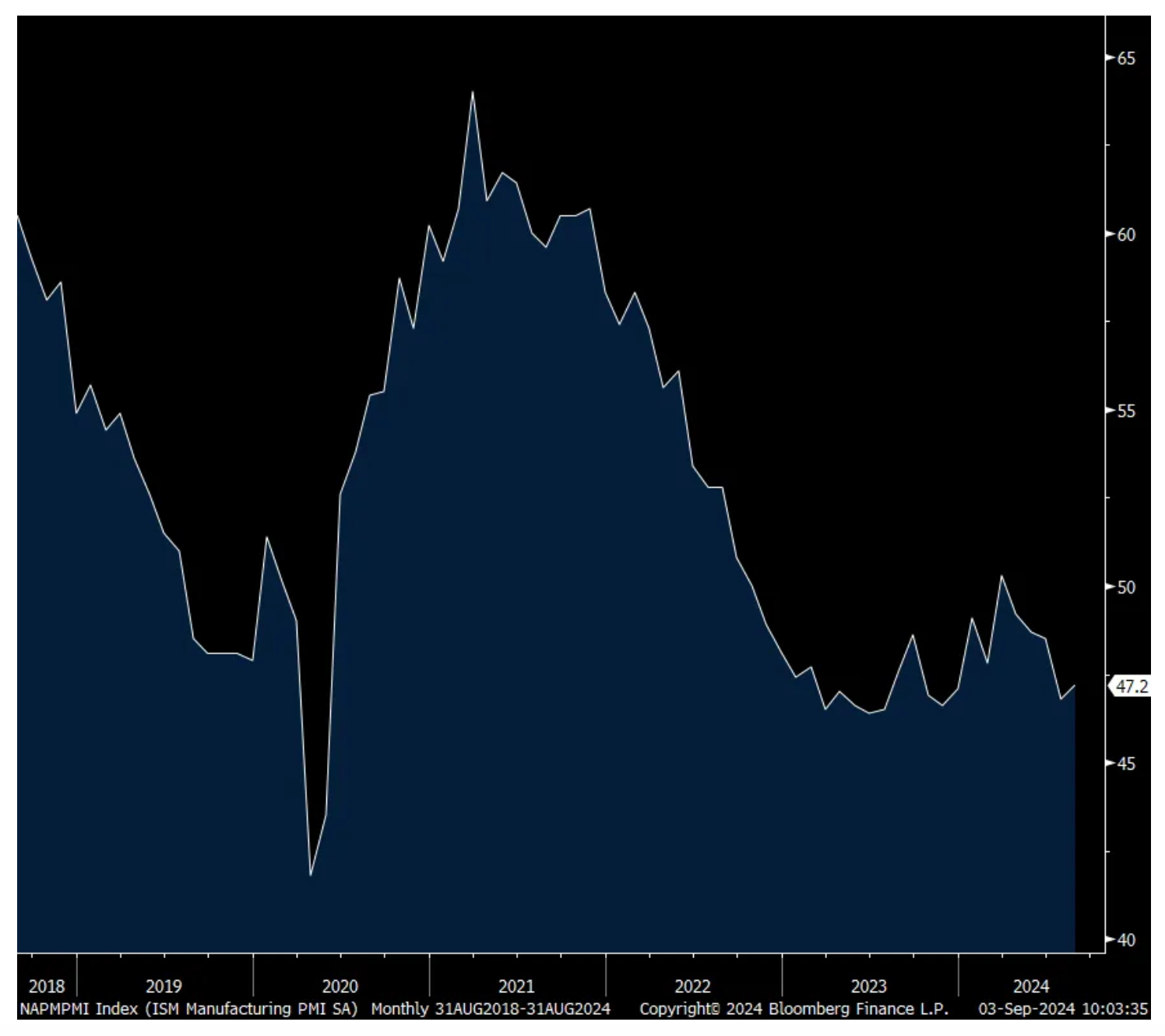

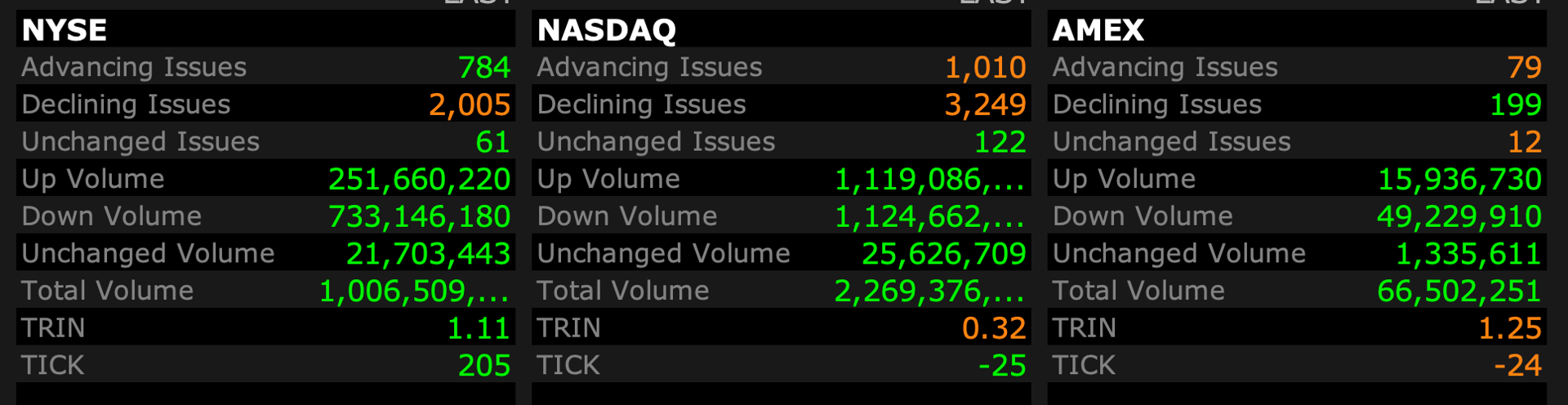

ISM mfr'g still weak, bad news is bad news now, and vice versa

The August ISM manufacturing index was little changed m/o/m at 47.2 vs 46.8 in July and 48.5 in June and thus remaining in contraction. The 6 month average is now 48.5. The bottom line, with numbers and anecdotes below to corroborate, is US manufacturing remains in a recession with little sign that the situation will change any time soon, but we’ll of course see to what extent, if much at all, some rate cuts will help result in some more activity. As for the stock market, we’re seeing more evidence that bad economic news is bad for stocks, and vice versa. Treasury yields are at the lows of the morning.

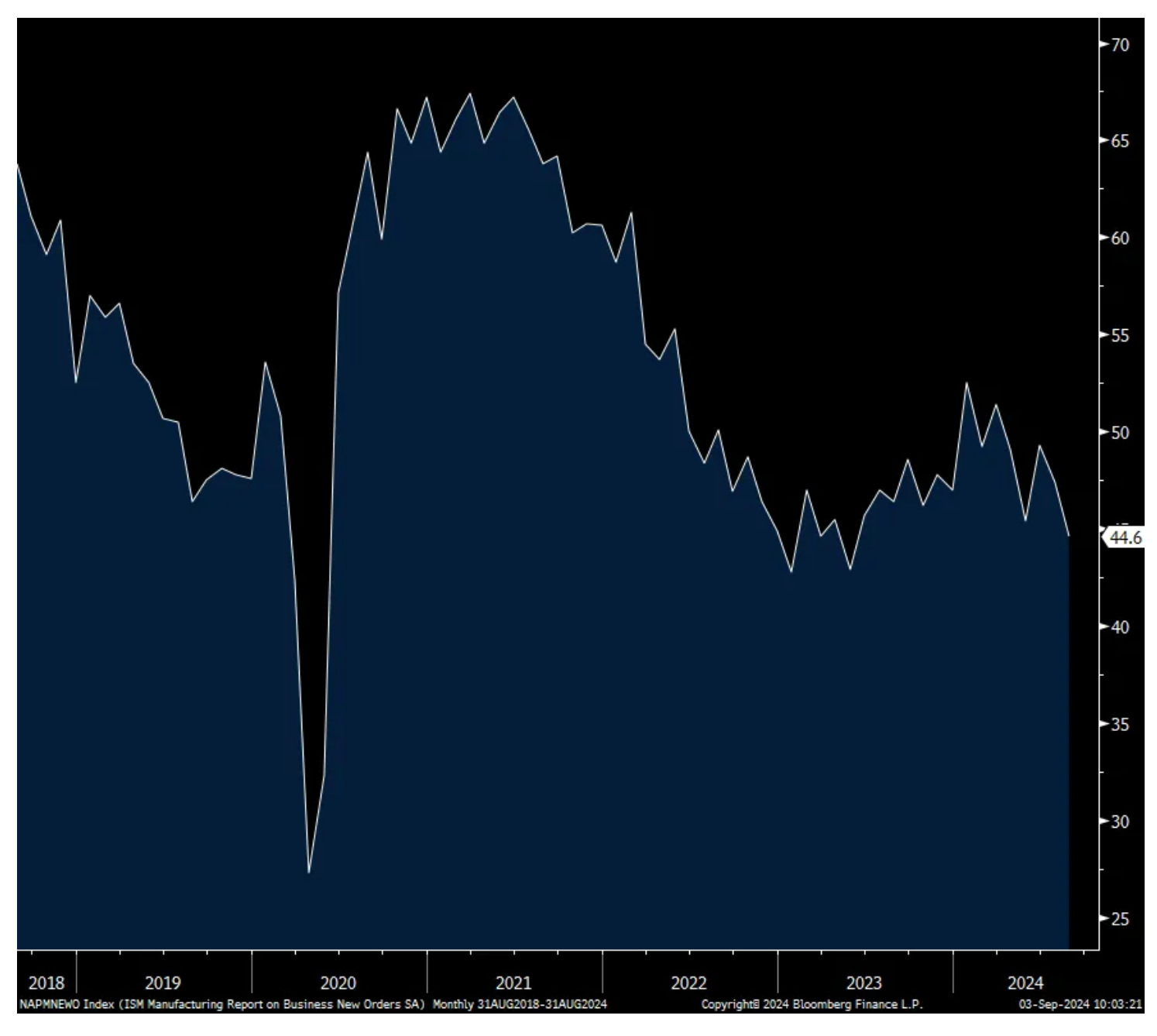

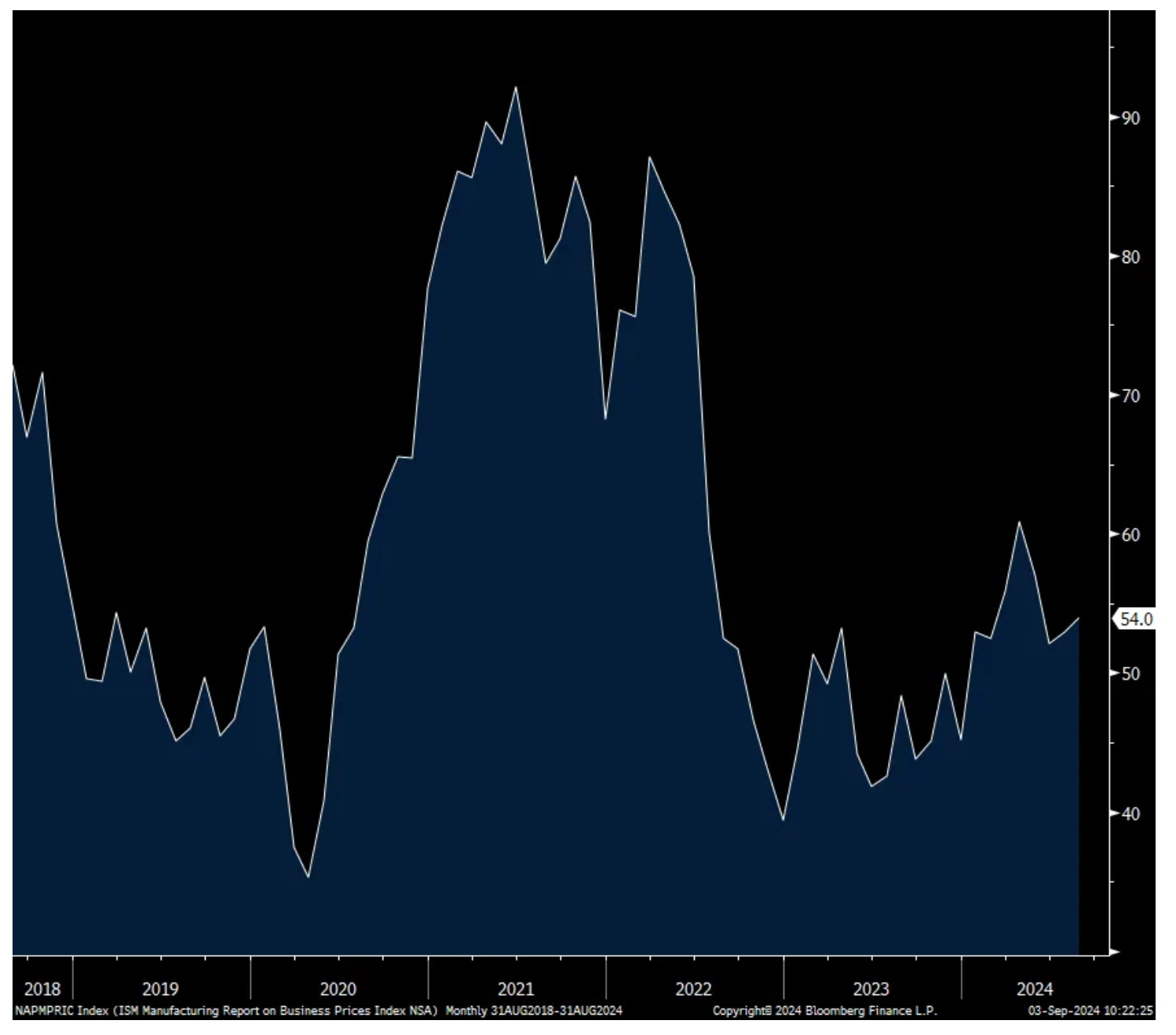

New orders softened further to 44.6 from 47.4 and that is the weakest since May 2023. Backlogs were less bad at 43.6 vs 41.7 but still well under 50. Inventories bounced back to 50.3, the first time above 50 since January 2023 while those at the customer level was up 2.6 pts to 48.4. Export orders fell a touch to 48.6 but below 50 for the 4th month in the past 5. Prices paid was up 1.1 pts m/o/m to 54, a 3 month high but still below its 6 month average of 55.5. Employment was up 2.6 pts but still in contraction at 46. Finally, supply chains are seemingly pretty normal with deliveries at 50.5, though we know there has been some front loading of deliveries for those who rely on ocean shipping.

In terms of breadth, just 5 industries of 18 surveyed reported growth, the same number seen in July while 12 experienced a contraction with one not seeing any change in business.

The ISM said “Demand remains subdued, as companies show an unwillingness to invest in capital and inventory due to current federal monetary policy and election uncertainty.”

Specifically with new orders, “Of the six largest manufacturing sectors, only one (Computer & Electronic Products) reported increased new orders. Panelists noted a continued level of uncertainty and concern about a lack of new order activity — with a 1-to-1.6 ratio of positive comments versus those expressing concern — and their confidence in the future economic environment remains at its lowest levels since the coronavirus pandemic recovery,” said ISM.

On employment, “Respondents’ companies are continuing to reduce head counts through layoffs, attrition and hiring freezes. Sentiment in August indicated continued staff reductions compared to July, supported by the approximately 1-to-1.2 ratio of hiring versus head-count reduction comments,”

On the inventory lift, “Manufacturing inventories grew as a result of panelists’ companies adjusting to lower new output levels and the subsequent timing issues.”

On prices paid, “Commodity prices continue to be volatile, especially oil, natural gas, aluminum, corrugate, freight transportation and plastic resins. Steel prices remain at historical lows. Twenty-one percent of companies reported higher prices in August, compared to 23 percent in July,”

The commentary below from some respondents in a variety of industries was pretty mixed:

“A noticeable slowdown in business activity. Staffing and production rationalization has been triggered. Previous optimism about future growth has been dashed.” [Chemical Products]

“Backlog has dropped in half as invoicing remains strong, but orders have slowed significantly. Hoping to see orders pick back up for the fourth quarter and into 2025 but expect third quarter to remain slow for incoming orders.” [Transportation Equipment]

“After a slow start and lower year-over-year sales volume during the first half of the year, we are now seeing a mild increase in year-over-year sales volume, along with more steady growth.” [Food, Beverage & Tobacco Products]

“Business outlook is good. Recovery from the electronics slowdown is strong for the second half of the year.” [Computer & Electronic Products]

“New order intake is sluggish at best. Interestingly, even though orders are down, inquiries are up. Customers have indicated capital has been approved for equipment purchases, but they were directed to put projects on hold until the fourth quarter of 2024. This indicates the uncertainty around the election. We anticipate a strong end of the year, with a rise in backlog going into 2025.” [Machinery]

“Our order levels are on a slow, steady decline; it looks like the trend will continue through the end of the year. We are downsizing through attrition and not hiring backfills, but there have been no layoffs to date. The bright spot is a few customer programs have helped increase orders for parts, resulting in some production areas to be very busy while others have little work. Redeploying people where we can.” [Fabricated Metal Products]

“New orders continue to be strong, and inventories are slightly down as a result. Supplier lead times seem to be creeping back up in certain categories.” [Miscellaneous Manufacturing]

“Business is cooling down, and we don’t expect a rebound until after the election is over. As we build our 2025 budget, we continue to have deep concerns about the added environmental costs on energy.” [Paper Products]

“Order book remains strong for now. We are preparing for a slowdown in U.S. auto sales. We are running overtime to keep pace, as hiring hourly employees has been difficult. Some walk off the job within hours because they cannot handle factory work.” [Primary Metals]

“High interest rates are curtailing consumer spending on large discretionary spending for furniture, cabinetry, flooring and decorative trim, which has affected our industry sales potential. At the same time, pent-up demand seems to be growing for housing and remodeling. Interest rate cuts may not happen soon enough to have an impact this year.” [Wood Products]

If one thing is stuck (DRAM), everything is gated.

All improvements are only incremental now, but very expensive.

I also think logic is much closer to the endpoint than the author suggests as well.

Look at all the problems Intel INTC is having now shrinking nodes. Nvidia's NVDA latest part is not a line shrink, just two parts tied together with a newer packaging technology, which is expensive, and not working/scaling quite right. These line shrinks are getting increasingly harder to do, and much for expensive.

We're getting real close to the point where it is just hard to squeeze more juice out of the lemon. This has broader implications for tech too, the whole framework of about the last 30-50 years may change because of this. As long as people have invested in tech, Moore’s Law has been in full effect.

I am surprised there is not more conversation around this issue, and what it means.

Boockvar: Don't Discount the Bank of Japan's Importance

From Peter Boockvar:

The BoJ still really matters/Other things of note

I still wake up and see what went on in Japan overnight as one of my first things, particularly with JGB yields and the yen, and as an owner of some Japanese stocks, as I don't think the global liquidity ripple effects of BoJ monetary tightening is done yet. Especially as the BoJ will be reducing its pace of JGB purchases through March 2026, where QE has been a massive liquidity spigot to the world over many years. BoJ Governor Ueda today, according to Bloomberg News and citing a comment he made in a document given to the Japanese parliament where he gave color on the rate hike in July, said they will continue to hike interest rates "if the economy and prices perform as expected by the BoJ" said the BN news article. The 2 yr JGB yield continues to quietly rebound and is at a one month high. The yen is higher too in response.

2 yr JGB Yield

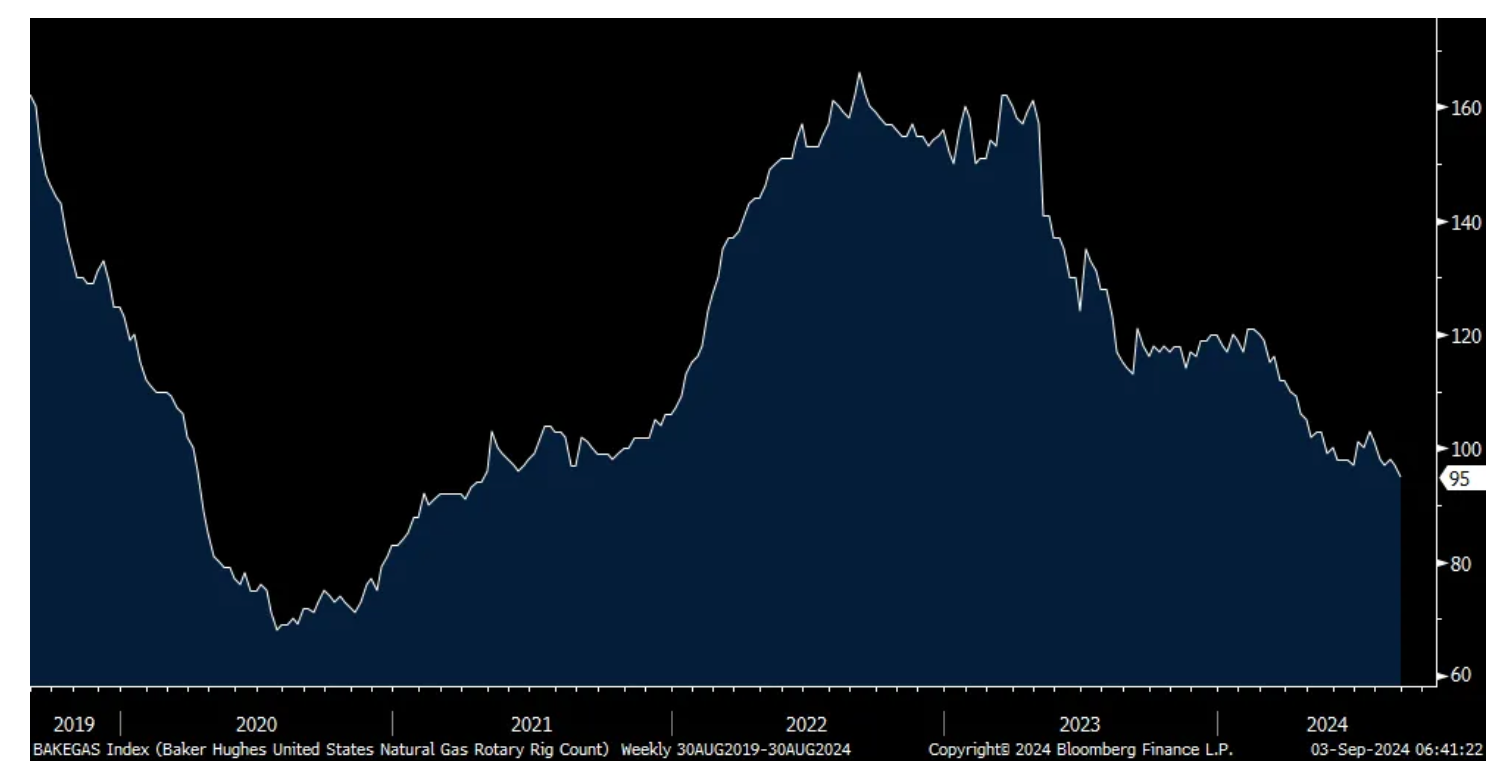

I want to reiterate my positive stance on the price of natural gas and related stocks, like EQT that we own, as around $2 per bcf is an attractive price with the US gas rig count continuing to drop. On Friday, the Baker Hughes natural gas rig count fell to the lowest since April 2021.

Natural Gas Rig Count

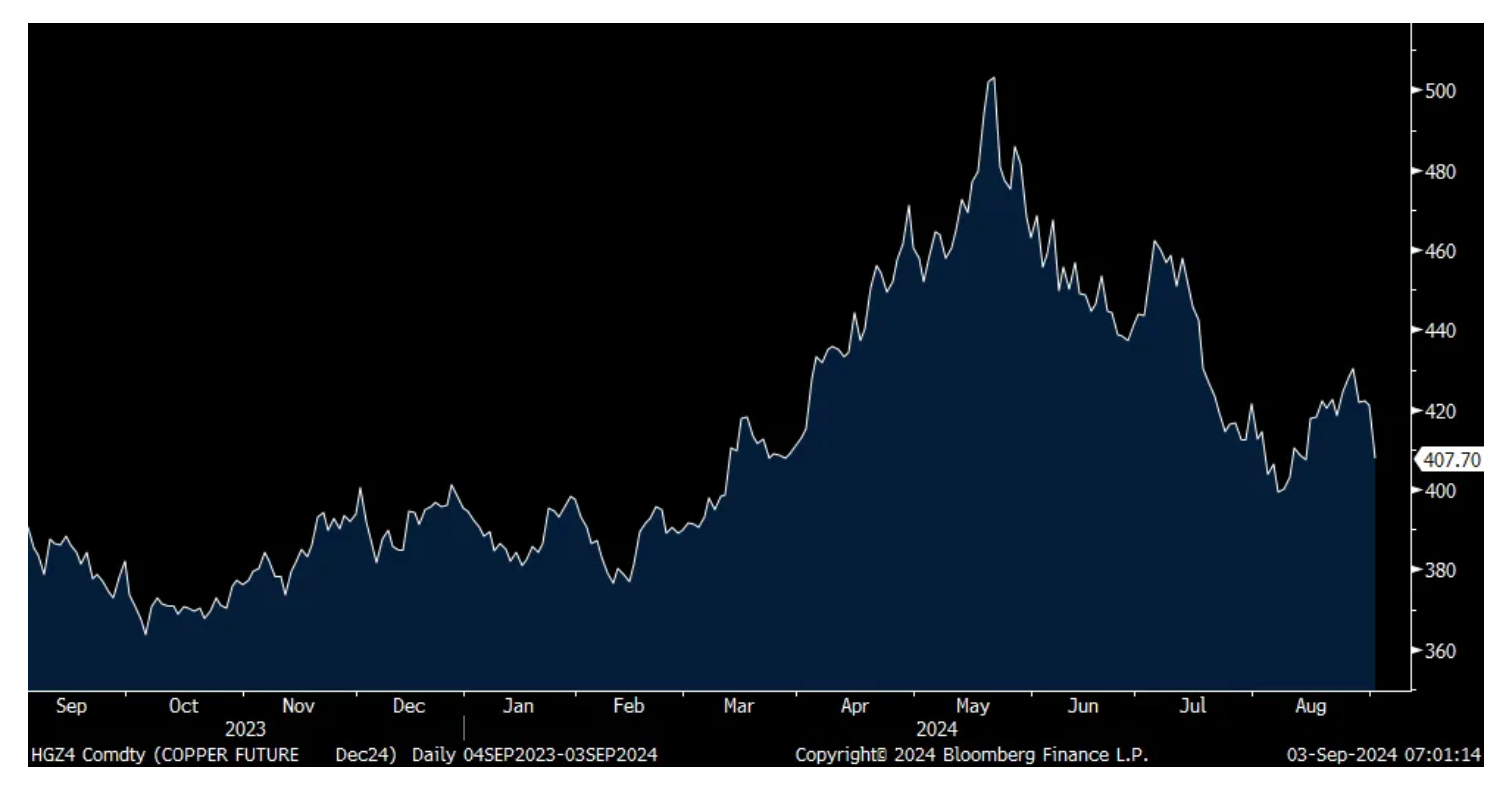

Copper on the other hand is getting hammered today by 3.1% as we worry about Chinese demand. Friday night China's August manufacturing PMI came out and it fell to 49.1 from 49.4 while the non-manufacturing PMI (which includes construction) did hold above 50 at 50.3.

In contrast, the private sector focused Caixin manufacturing PMI did get back above 50 at 50.4 from 49.8 in August. Caixin said "Manufacturing production expanded for a 10th successive month in August, led by firms in the consumer and intermediate goods sectors. Although modest, the rate of growth accelerated from July's low as incoming new orders returned to expansion. Survey respondents revealed that better underlying demand conditions and promotional efforts underpinned the latest rise in new orders." As China has moved up the technology curve, particularly in EVs, their manufacturing prowess cannot be forgotten and the emerging world now as their big customer. That said, the growth mostly came domestically in August according to Caixin as "Export orders were subdued."

Copper

We also got a slew of other PMI's from overseas that was mixed for August. South Korea 51.9 vs 51.4, Taiwan 51.5 vs 52.9, Thailand 52 vs 52.8, Malaysia 49.7 vs 49.7, Indonesia 48.9 vs 49.3, India 57.5 vs 58.1, Japan 49.8 vs 49.1 and Australia 48.5 vs 47.5.

The Eurozone manufacturing PMI was revised to 45.8 from 45.6, still deeply under 50 and at that exact level for a 3rd straight month. The UK manufacturing PMI continues to outperform its European peers with a print of 52.5 in August which is the highest since June 2022. S&P Global said with the UK index, "The upturn continues to be driven by the domestic market, which is helping to compensate for lost export orders."

As for the Eurozone, S&P Global said, "Things are going downhill, and fast. The manufacturing sector has been stuck in a rut...New orders, both domestic and international, are slowing down even more, dashing any short term hopes for a rebound."

And, the spike in container shipping prices is rippling thru. "For the first time since April of last year, selling prices rose, driven by France, the Netherlands, Greece and Italy...Higher transport costs are partly to blame for this uptick in price pressure." As a reminder, container shipping costs have tripled this year of their lows.

More Tales From Nvidia: AI Not Working? Call the ... Plumber!

Per point below on the cost on AI in my last "Tales," not dropping like one would expect for a technology product, see these tweets on the water cooling issue.

This is also what happens when the underlying technology does not work well, and you resort to brute force as a solution. Costs go up, not down. When tech turns into plumbing and carpentry, you have real issues.

Despite many embracing the news excitedly, I expect only a very modest bump following former President Trump's vague comments on Amendment 3 in Florida over the weekend:

I view cannabis stocks positively — with large upside and limited downside. But I also view cannabis stocks as investments and not as a trade (especially given the delay in rescheduling well into 2025).

That said, I am considering buying more cannabis equities this morning if the response is muted.

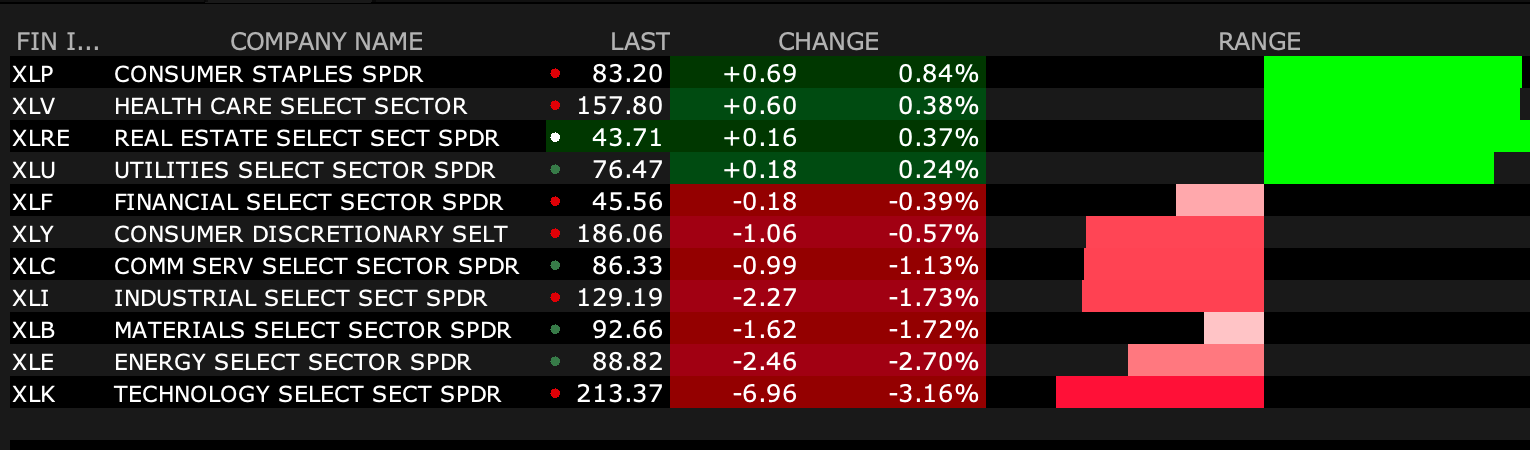

3 Factors Will Impact the Market During the Dangerous Month of September

Since 1950, the S&P 500 has, on average, suffered a loss of 0.7% during the month of September. A recen four years have been particularly bad, with declines of 4.9% in 2023, 9.3% in 2022, 4.8% in 2021, and 3.9% in 2020.

Negative seasonality is not a certainty, but it is a tendency, and it is very important to consider it in the context of potential news catalysts and technical conditions. To some degree, seasonality is self-fulfilling, especially when technical conditions align with significant news events.

The big market event that will occur in September is the Fed meeting on September 18. It is widely anticipated that the central bank will cut interest rates at the meeting, but the big question will be whether it is a quarter-point or half-point cut.

The size of the cut will be determined in part by the August jobs report, which will be reported on Friday, September 6, prior to the market opening.

While the market has been anxiously awaiting a cut for quite a while, a bigger cut isn't necessarily better because it would indicate greater fear that the economy is slowing and may see a recession. Currently, the market is embracing a Goldilocks economic scenario in which inflation is not too hot, and growth is not too cool. If the jobs report is weaker than expected, it could easily tip the balance toward a recession. A few weeks ago, there was near panic over some weak labor data, but it was forgotten in a matter of days, and the market has been trending higher as it awaits more news.

Typically, the poorest action in September occurs in the second half of the month, and that coincides almost perfectly with the Fed's interest rate decision. What makes it even more precarious is that the indexes have become very technically extended and overbought just as this major event occurs. It will be a near-perfect setup for a "sell the news" event, but the big issue is whether the market will start to anticipate that reaction and begin to correct it before it actually occurs.

Seasonality, the August Jobs Report, and the Fed interest rate decision are the three factors that will determine what this market does next. I've been growing increasingly cautious, not only because of the three issues but because of the lack of favorable charts. There are not many potential catalysts to keep positive momentum going.

We have some softness on Tuesday morning but the initial issue will be whether the market starts to anticipate the danger that lies ahead.

At the time of publication, Rev Shark had no positions in any securities mentioned.