From Boockvar: Tough Read on Low-Income Consumers; Also, Travel and Rent

From Peter Boockvar:

An eye opening read on the lower income consumer/Other good stuff

There were two retail earnings conference calls over the past few months that really stood out to me and reflected the plight of many lower income consumers. One was in June (and will be updated next week with fresh earnings) when Casey's General Stores, an owner/operator of convenience stores in the Midwest, said its lower income shoppers were more buying fountain soda rather than a can or bottle in order to save some money. The other was what Dollar General said yesterday about its lower income consumer, which makes up a majority of their customers.

From Dollar General:

“Same store sales increased .5% during the quarter, which was below our expectations. The increase was driven by a 1% growth in customer traffic and was partially offset by a .5 point decline in average transaction amount, which was driven by lower average unit retail price per item. The comp sales increase was driven entirely by the growth in our consumable category as customers continue to focus their spending on the items they needed most for their families. This growth was partially offset by declines in our seasonal home and apparel categories.”

“From a monthly cadence perspective, same store sales growth was strongest in June before turning negative in July. Notably, the three softest comp sales weeks of the quarter were the last week of each of the calendar months. This pattern suggests that our customers are less able to stretch their budgets through the end of the month. With that in mind, as well as our continued softness in discretionary sales in our own customer data and survey work, we believe the softer than anticipated sale performance in Q2 is at least partially attributable to a core customer that is less confident of their financial position.”

And a deep dive on their customers, “I want to provide some additional context around what we’re seeing and hearing from our customers. The majority of them state that they feel worse off financially than they were six months ago as higher prices, softer employment levels and increased borrowing costs have negatively impacted low income consumer incentive. As a result, our core customer who contributes approximately 60% of our overall sales comes predominantly from households earning less than $35,000 annually.

Inflation has continued to negatively impact these households with more than 60% claiming that they have had to sacrifice on purchasing basic necessities due to the higher cost of those items, in addition to paying more for expenses such as rent, utilities and healthcare. More of our customers report that they are now resorting to using credit cards for basic household needs and approximately 30% have at least one credit card that has reached its limit. And in our latest survey, 25% of our customers surveyed noted they anticipated missing a bill payment in the next six months.

While middle and higher income households are seeking value as well, they don’t claim to feel the same level of pressure as low income households."

From Burlington Stores:

“we continue to see very strong performance in full price selling. Our merchants are focused on offering really sharp value out-of-the-gate at the initial ticketed price. This is driving faster turns and lower markdowns. This means that there is less inventory making it to the clearance rack.”

On the consumer, “Two years ago, our core low income customer was under severe economic pressure from the higher cost of living. Since then, it feels as if two things have happened. As inflation has moderated, the situation for lower income shoppers has somewhat improved. In parallel, economic pressure and uncertainty has spread and broadened well beyond lower income shoppers. There is now greater focus on value across demographic groups and income bands. This greater focus on value is helping our business…I think a big part of what we’re seeing is that value-conscious customer is trading down into our stores.”

While they raised guidance, “Included in this updated guidance is an expected ocean freight headwind of approximately $.10 impacting the back half of the year, which reflects the rapid increase in ocean container rates since we last updated our guidance in late May.” I’ve said multiple times that someone was going to have to eat the spike in container prices.

From Best Buy:

“From a category perspective, we drove comparable sales growth in tablets, computing, and services. This growth was more than offset by declines in appliances, home theater, and gaming.”

“Overall, customers remained deal focused and attracted to more predictable sales moments. With 4th of July, Black Friday in July, and the beginning of back-to-school sales events, July comps were the best of the quarter. In this environment, many categories, including major appliances and TVs, continued to be very promotional in pursuit of stimulating interest and sales.”

“For the 3rd quarter specifically, we expect comparable sales to be down approximately 1% vs last year. Based on our month-to-date performance, we estimate August comparable sales will be approximately flat to last year.”

Lastly with BBY, “it is still an unpredictable and uneven consumer environment. And while we made it explicit to say we haven’t seen anything so far this year that changes that behavior, I think we’re acknowledging there will be an election impact. And there always is, historically, no matter what kind of election we’re entering into. So, we know that that is likely coming. And you’re entering into the holiday season, which often can also create some unpredictable consumer behaviors, probably consumers who might even wait for some of the more values that they, I would guess, assume that they’re going to see over the holiday. And so, I think we’re looking at consumer indicators that continue to be uneven.”

From Ulta Beauty whose comps fell 1.2% y/o/y:

"Although we anticipated the headwinds experienced in the first quarter would continue, our results were short of our expectations, driven by a decrease in comp store sales, specifically comp store transactions. E-commerce sales increased as expected."

"We attribute the decline in comp store transactions to four factors. First, while the beauty category remains resilient, growth is normalizing after three years of unprecedented gains. Additionally, consumer behavior is starting to shift as consumers increasingly focus on value and become more cautious with their spending...Second, competitive intensity in the beauty category remains high." The third was internal as they had some disruptions with their ERP transformation. "The fourth factor impacting our performance this quarter was the effect of incremental promotions, which did not deliver the expected sales lift."

From Lululemon:

Specifically on the US, revenue was flat. "Our brand remains strong in the US market. Traffic was up across both channels, and Google Search queries remain positive. Guests are looking for our product, coming into our stores, and visiting our e-commerce sites. While we continue to see growth in our men's business, we have experienced a slowdown in women's."

I’m going to shift to China for a minute because if there is one consumer bright spot in their economy it is their desire to travel. From Trip.com, a stock we own:

“During the quarter, our outbound hotel and air ticket bookings recovered to 100% compared with 2019 levels, continuing to outpace the industry average by an impressive 20% to 30%. Remarkably, bookings surged to more than 120% of 2019 levels during the May Labor Day holiday and over 100% during the Dragon Boat Festival.”

Also, “The APAC region remains the top choice for Chinese travelers with visa-free destinations such as Singapore, Thailand and Malaysia seeing a strong resurgence. In Northeast Asia, a favorable exchange rate has made Japan an even more attractive destination and Korea has also experienced a notable increase in bookings. Long-haul destinations are also gaining popularity. Improved visa processing and international events such as the Euro Cup and the Olympics have further fueled this trend, leading to y/o/y increase of over 100% in travel to France and Europe during the summer.”

A quick stat, the Chinese tourist spent $250 billion internationally in 2019.

Lastly on the earnings calls, from Dell Technologies:

"Our AI momentum accelerated in Q2 and our results and outlook demonstrate that we are uniquely positioned to help customers leverage the benefits of artificial intelligence."

About what HP Inc said the other day, "We are optimistic about the coming PC refresh cycle, as the installed base continues to age, Windows 10 reaches end of life later next year and the significant advancements in AI-enabled architectures and applications continue."

Storage revenue fell 5%.

Finally, back on the PC side, "The consumer market is lagging relative to the commercial market in terms of its performance or its growth and it's a competitive environment there."

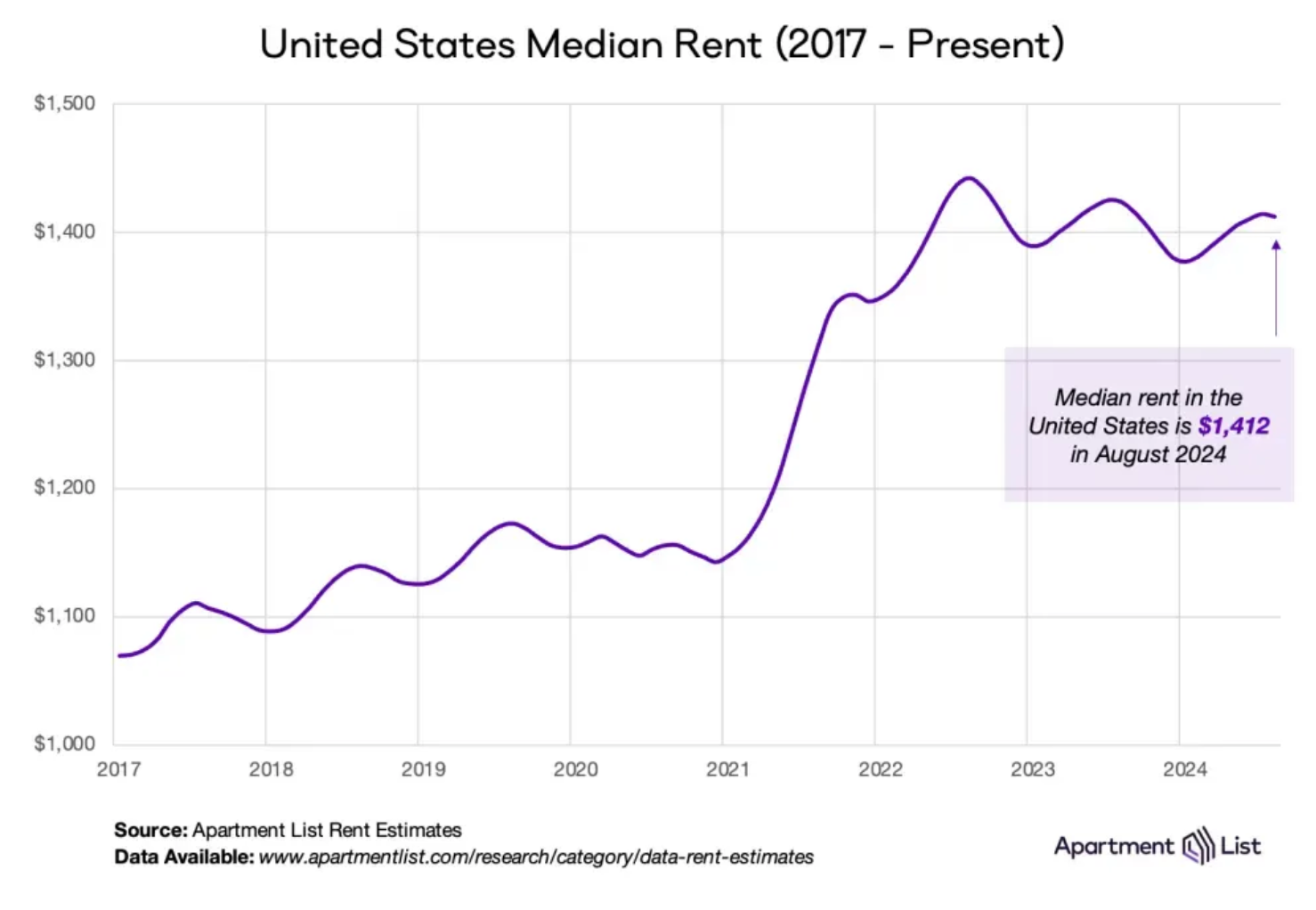

Ahead of the PCE today where healthcare prices are the biggest component with housing second, the reverse of CPI, Apartment List gave us their August stats yesterday for NEW leases. Rents fell .1% m/o/m "as the market remains sluggish thanks to a windfall of new supply." The y/o/y drop is .7% "and has now been in negative territory for over a full year. Despite this, the national median rent is still more than $200 per month higher than it was just a few years ago."

The vacancy rate stood at 6.7%, the same level as in July but the most since August 2020. The sunbelt states is where most of the excessive supply is coming to market and where rent growth is the softest. In contrast, "many large cities in the Midwest and Northeast are still experiencing positive annual rent growth."

While we all focus on rate of change, the average person is not and while "the national median rent is a few percentage points below its August 2022 peak," it still is "more than 20% higher than at the start of 2021." And, I expect that once this supply is absorbed, and it will be with home price still very high relative to income, along with limited additional supply, rent growth in the back half of 2025 and into 2026 will head back higher again.

I'll finish with overseas inflation stats. The August Tokyo CPI rose 2.6% y/o/y headline, up from 2.2% in July and 3 tenths above the estimate. The core/core rate was up by 1.6% y/o/y, 2 tenths above the forecast and up one tenth m/o/m. Notwithstanding the upside, the market response was muted as JGB yields and inflation breakevens were little changed. The yen is slightly lower and the Nikkei rallied by 3/4 of a percent. I do expect another BoJ hike in the fall. The ripple effects from the reversal of BoJ's epic monetary policy is not over, particularly on the QT side.

On the flip side, we're likely going to get another ECB rate cut in September. CPI, which notably under counts housing costs there as it's only about 6%, was in line with expectations but did moderate to 2.2% y/o/y from 2.6% with lower energy prices keeping a lid on overall prices while the core rate grew by 2.8% from 2.9%. What would keep them from cutting would be the persistent inflation on the services side which rose 4.2% y/o/y vs 4% in July.

While the German economy is under pressure, the number of unemployed rose just 2k in August, well below the estimate of an expected rise of 16k. Their unemployment rate held at 6%.

The market response to the European data was a yawner too. Yields are down about 1 bp, the 5 yr 5 yr euro inflation swap is flattish and stocks are up modestly as is the euro. Summer Friday.

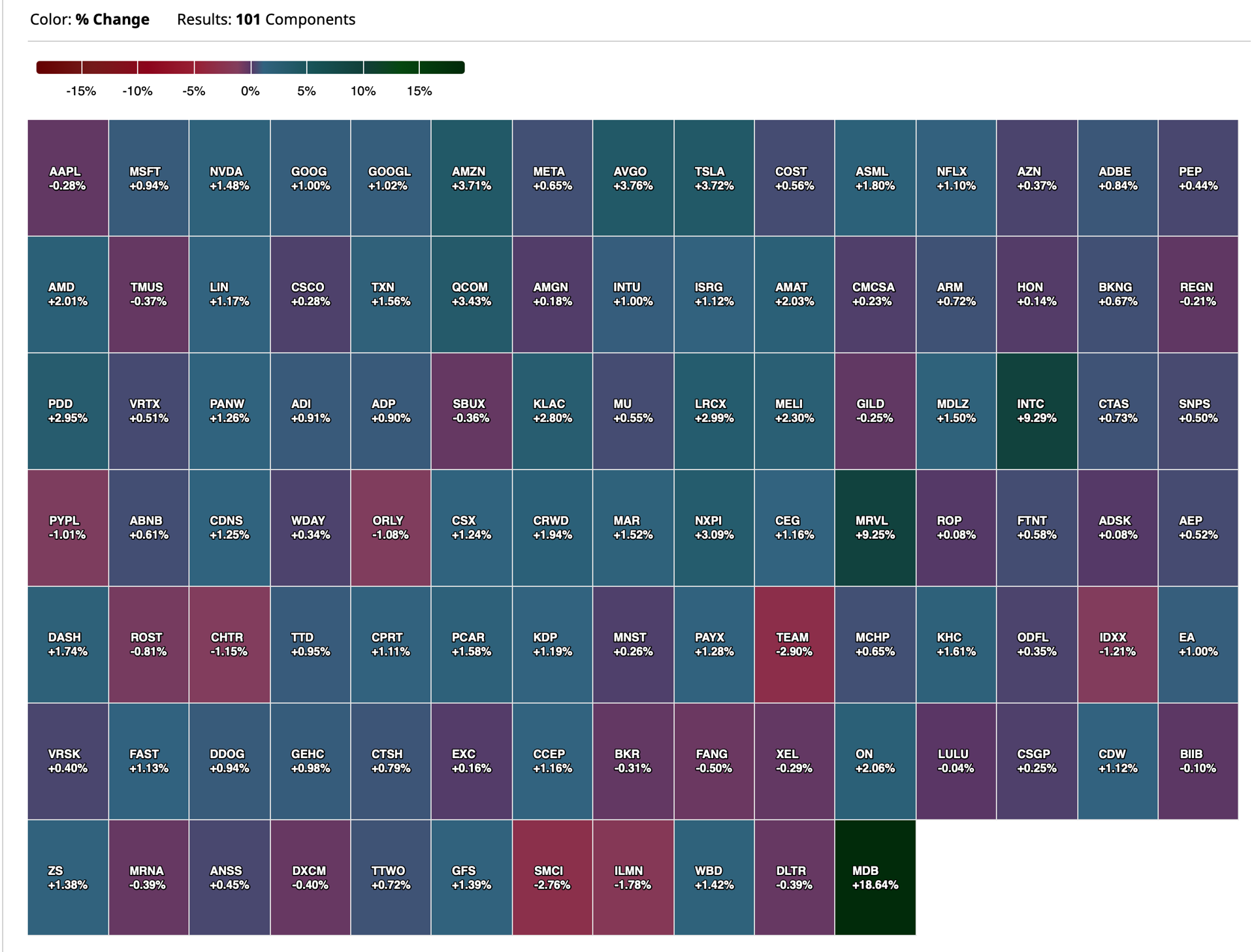

More Tales from Nvidia: This Line from the Earnings Call Says Everything

Maybe this was the most important thing on the Nvidia NVDA call last night:

"Next generation models will require 10- or 20-times more compute to train with significantly more data."

NVDA was trying to be promotional in regard to how big the total addressable market will be. But in my view, the company highlighted the problem, which is generative artificial intelligence does not work well. Spending more money is just brute force. Brute force is what you do when something isn’t working. It is like more drugs for the heroin addict that has built up tolerance. It will never end well, no matter how much you spend or shoot up. Gen AI is glorified auto-complete, and it will always hallucinate (as I have mentioned previously in this series).

There is nothing intelligent about it. And it depends on human-generated content. Spend more money, it will just hallucinate more rapidly I guess.

A new approach is needed. But that approach does not exist yet, it's not even close – whether it is quantum compute or neurons on a chip.

People may argue costs will come down. But it is really hard for costs to come down. Power is still power, and the unit price of power does not move down, only up frankly. Then on top of it more units of power will be required. Then, Moore’s law is basically tapped. It is getting incredibly costly to move down process nodes, and the little hacks, like packaging, are also expensive and not easy, per the problems NVDA is now having with their new part.

The one area where cost can come down is the pricing of NVDA silicon. Look at what its margins were, and what they are now. They might be charging two- to three-times more per part beyond what is economic for their customers (if anything is even economic for an end product that doesn’t work well and has limited demand). This element of cost coming down is obviously not good for NVDA's stock.

The challenge here is that for AI models to do anything more than they are already doing (which isn’t enough), the cost is going up (a lot) not down.

One Last Thing

What is it with the accounting and all the other issues at these AI businesses? Super Micro Wednesday, iLearning Engines Thursday. This doesn’t mean NVDA has issues, but with all the investment-related parties who are their customers and all the other goofy stuff with respect to where their parts are potentially going (directly or indirectly and the export control issues) -- not sure what revenue multiple I would be willing to pay to wait around and see how it all resolves.

Warren Buffett is raising massive amounts of cash (by selling some of his favorite holdings — Bank of America BAC/Apple AAPL), Jensen Huang is selling NvidiaNVDA shares ) and Jamie Dimon is selling down his JPMorgan JPM stake.

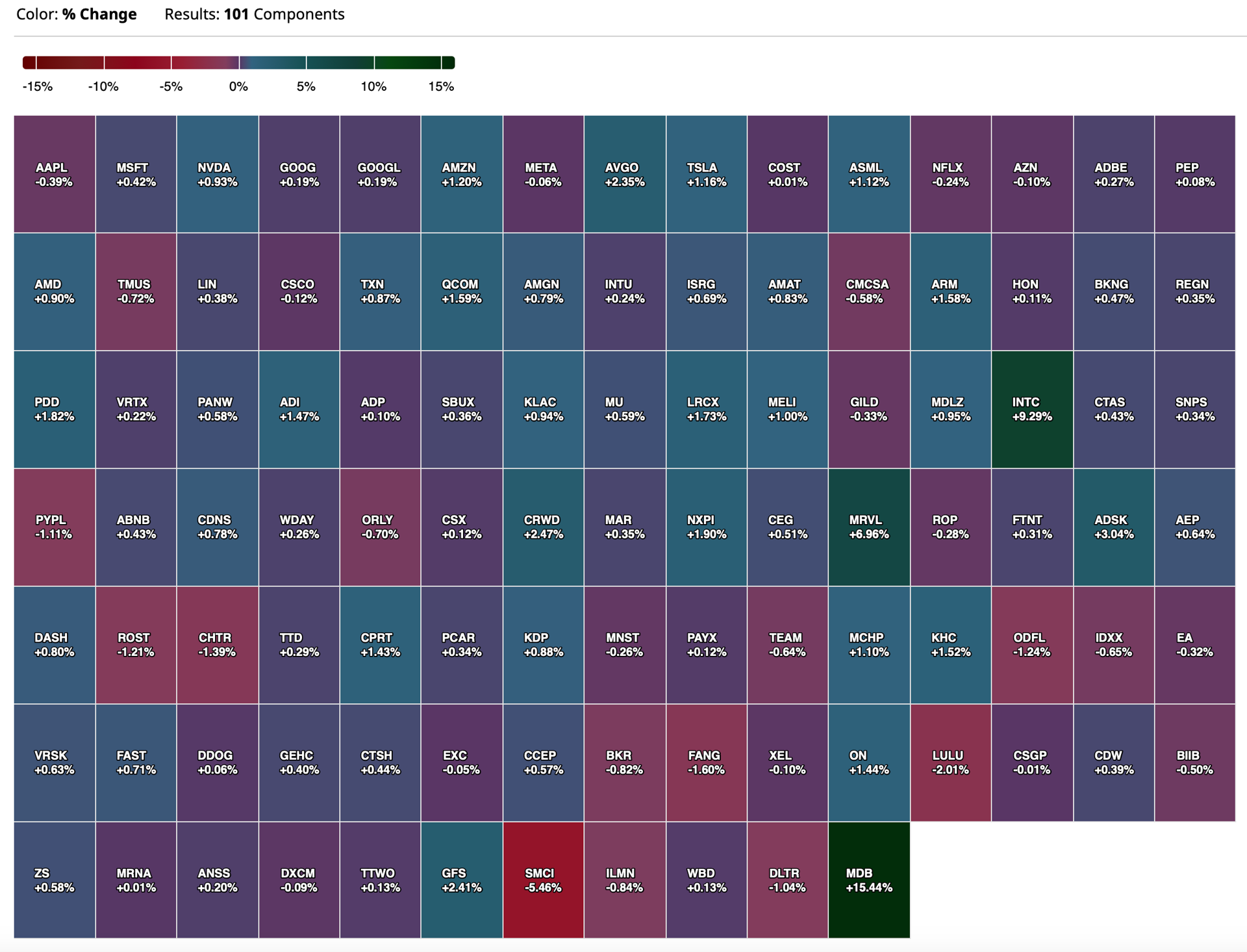

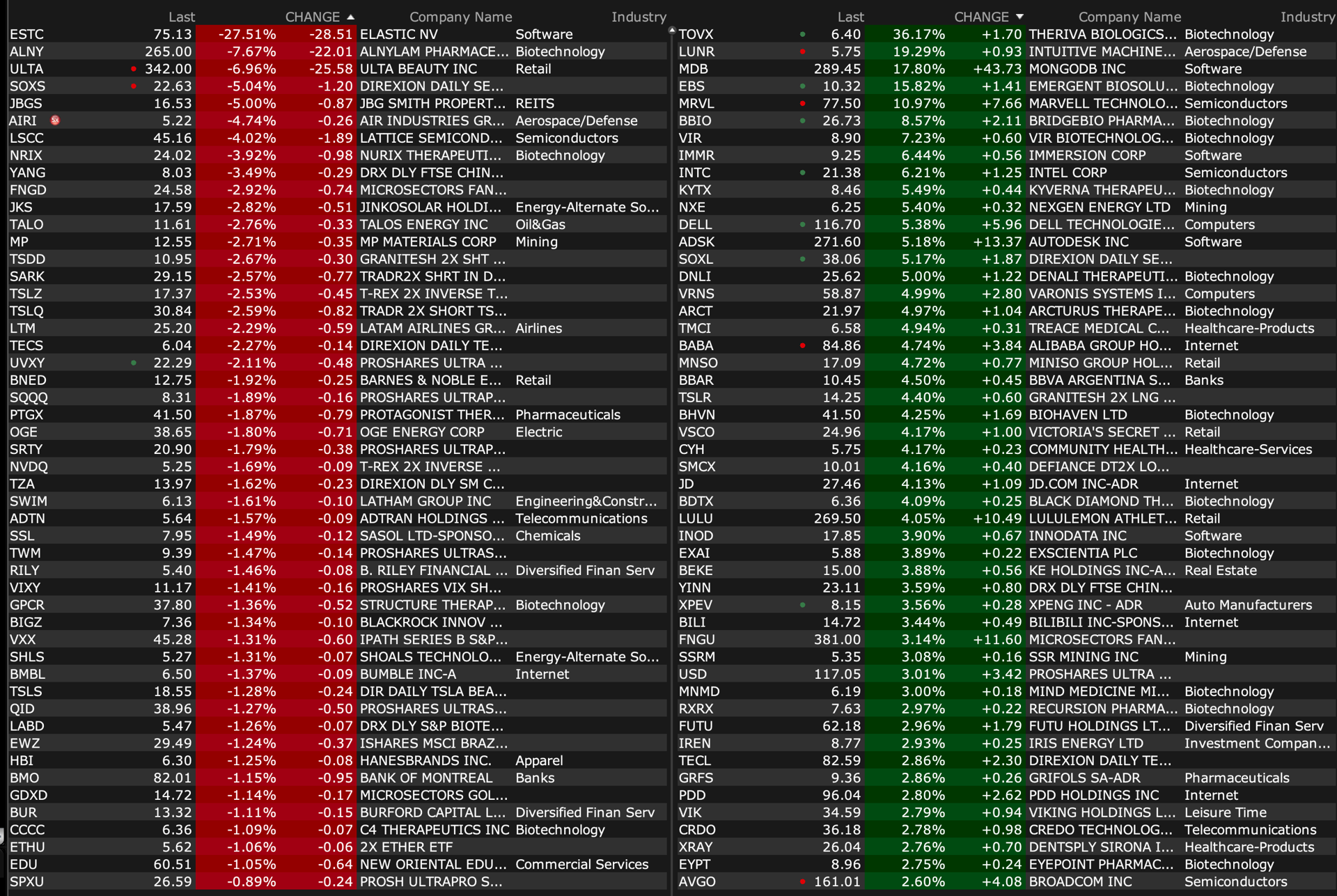

-EBS +16% (receives US FDA ACAM2000 sBLA approval to include prevention of mpox disease in individuals determined to be at high risk for mpox infection; Public Health Mpox Outbreak continues across Africa and other regions)

-MDB +15% (earnings, guidance)

-MRVL +12% (earnings, guidance)

-DELL +5.2% (earnings, guidance)

-LESL +5.2% (CFO Bowman buys 100K shares at $2.58/shr)

-ADSK +5.0% (earnings, guidance)

-MNSO +4.6% (earnings)

-BABA +4.5% (China State Administration for Market Regulation (SAMR) ends antitrust review of Alibaba's monopolistic behavior)

-INTC +4.1% (said to explore options with Goldman, Morgan Stanley; considers splitting off foundry and product units, scrapping factory projects)

-LULU +3.6% (earnings, guidance)

Downside:

-ESTC -27% (earnings, guidance)

-ALNY -12% (presents detailed results from Positive HELIOS-B Phase 3 study of Vutrisiran in patients with ATTR Amyloidosis with Cardiomyopathy at the European Society of Cardiology Congress)

-ULTA -7.2% (earnings, guidance)

-BCDA -5.0% (pricing upsized $7.2M public offering at $3.00/shr)