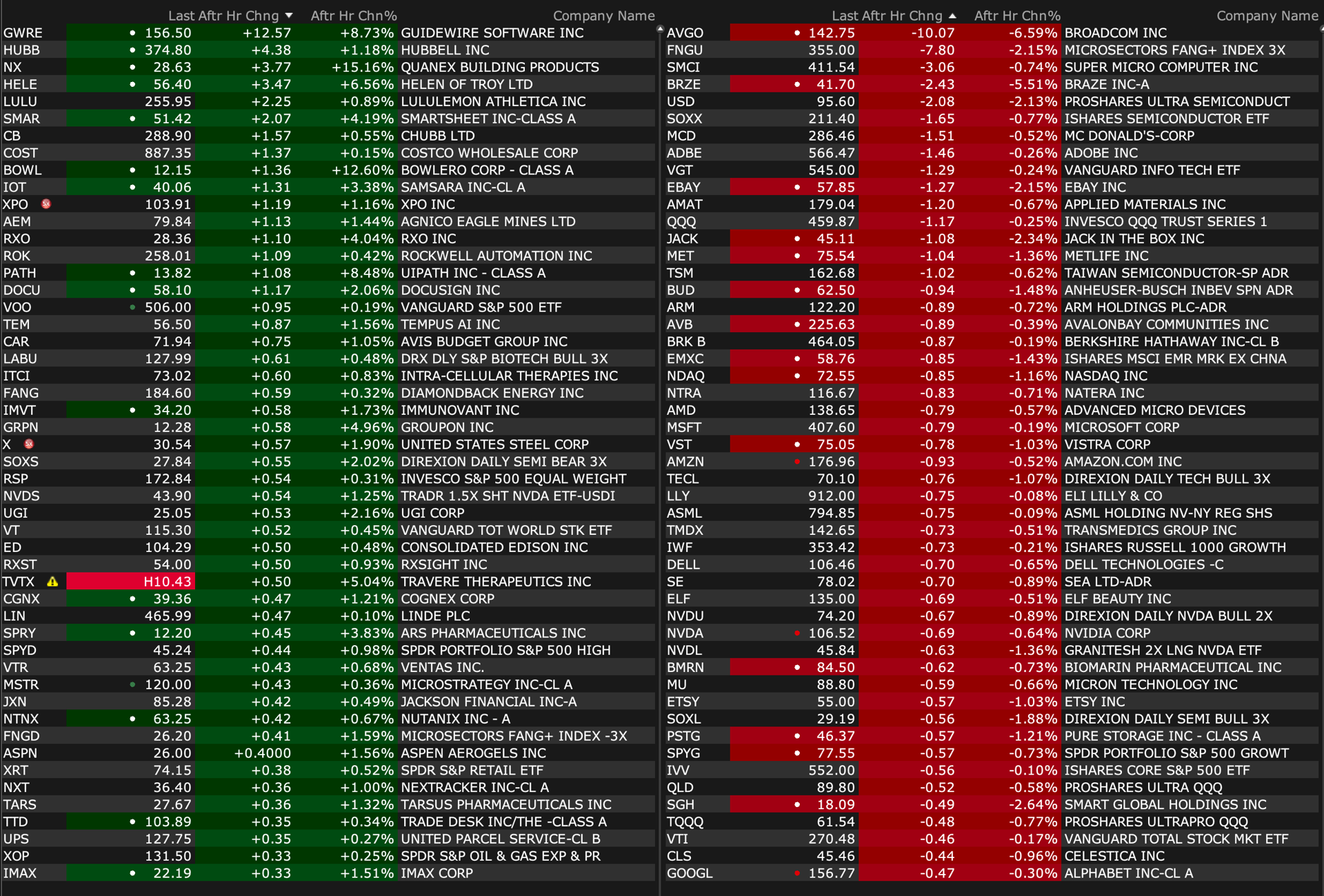

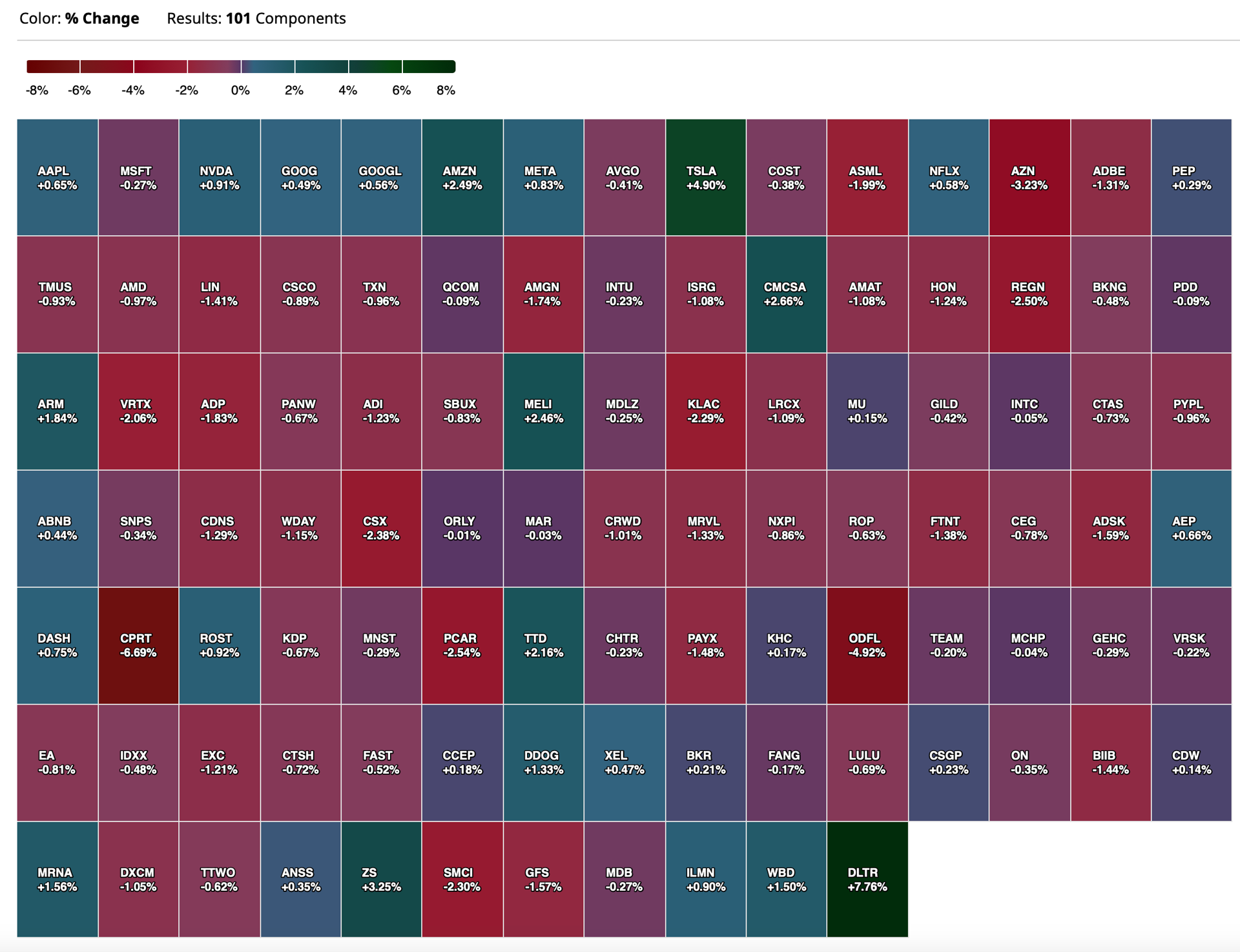

After-Hours Movers

BY Doug Kass · Sep 5, 2024, 5:53 PM EDT

BY Doug Kass · Sep 5, 2024, 5:53 PM EDT

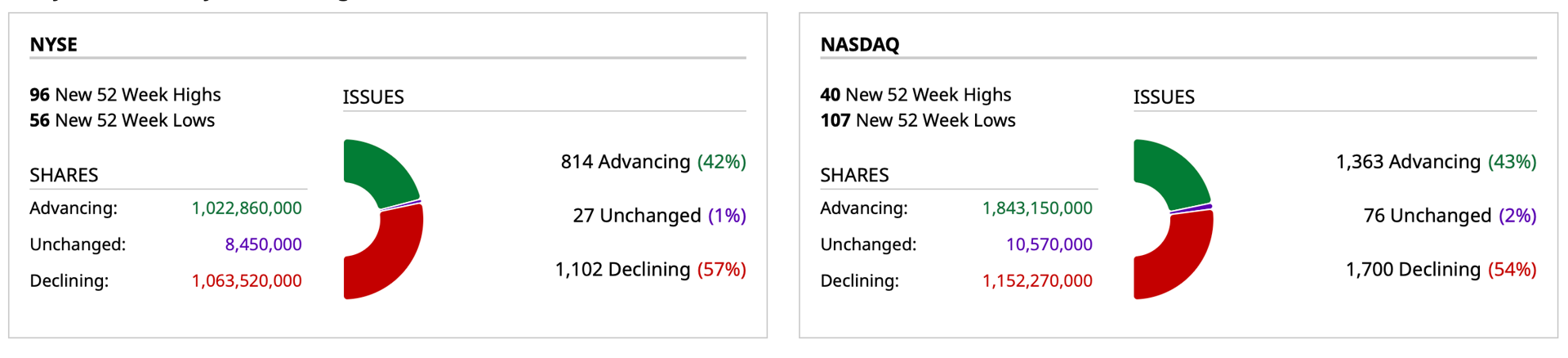

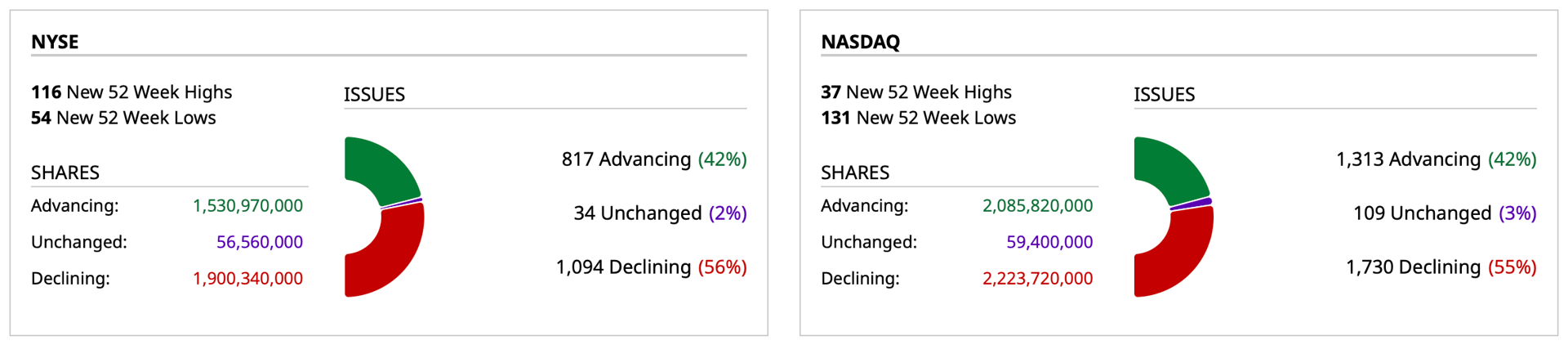

- NYSE volume 1% below its one-month average;

- NASDAQ volume 7% below its one-month average

- VIX: down 7.08% to 19.81

BY Doug Kass · Sep 5, 2024, 4:24 PM EDT

Regarding my opener this morning — especially as it relates to relatively new subscribers...

Please understand the time horizons of comments like mine.

It is important to distinguish my view that "being long equities has become a risky asset allocation" from (what I am not saying) "everyone should run out and short the hell out of the market."

BY Doug Kass · Sep 5, 2024, 1:15 PM EDT

My pal (the brilliant analyst) Larry Haverty comments on my opener:

My favorite is “adjusted EBID.” What is adjusted is bad things. Of the 100 plus companies I monitor is is amazing to see the magnitude of the delta between this and simple EBID which is pretax plus interest plus D. And on top of this, EBITD is not free cash flow.

Last week over 500 net new highs. Contrary to beloved CNBC, the market is broad. That’s the good news. The bad news is the number was only higher once.

It was 2008 , I believe. I have kept these numbers for over 40 years.

Hard to believe all this ends happily. I just cashed out of JWN. Great ride but a take under like Frontier today. So much for “private market value.”

Could today be an outside day on the downside? If so, hold on to your hat!

BY Doug Kass · Sep 5, 2024, 1:00 PM EDT

I just covered my Apple AAPL short from this morning for a $3 gain:

I covered my Apple (AAPL) short for a nice gain last week.

I am re-shorting the shares now (+$4.45/share) at $225.30.

But baby steps and on a scale higher.

Position: Short AAPL (VS)

By Doug Kass Sep 5, 2024 10:50 AM EDT

BY Doug Kass · Sep 5, 2024, 12:34 PM EDT

Adding to Disney DIS at $88.66.

BY Doug Kass · Sep 5, 2024, 12:24 PM EDT

From Peter Boockvar:

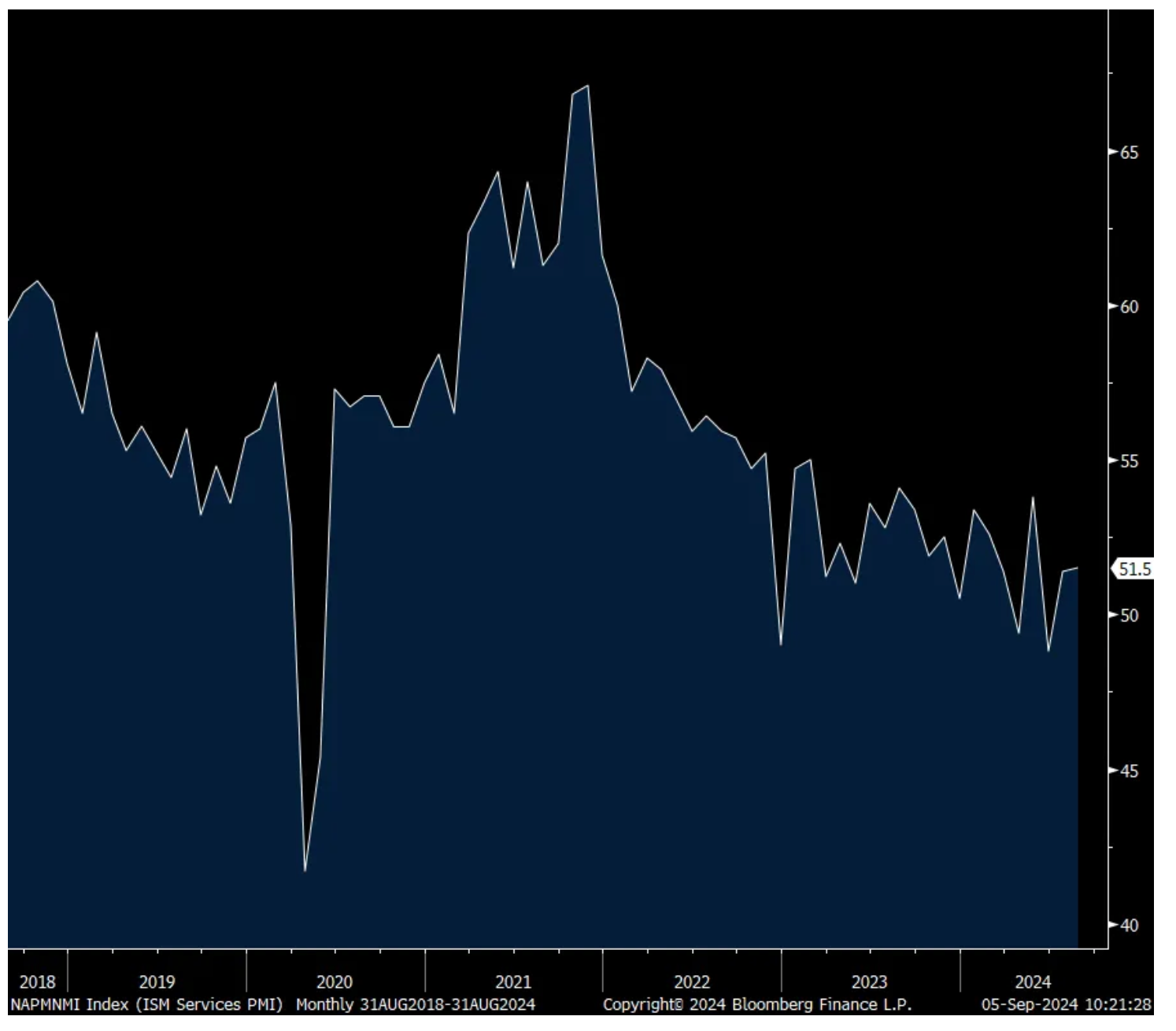

ISM services, remains just above 50

The August ISM services PMI was little changed at 51.5 vs 51.4 in July and around the estimate of 51.4. This compares with 48.8 in June and 53.8 in May.

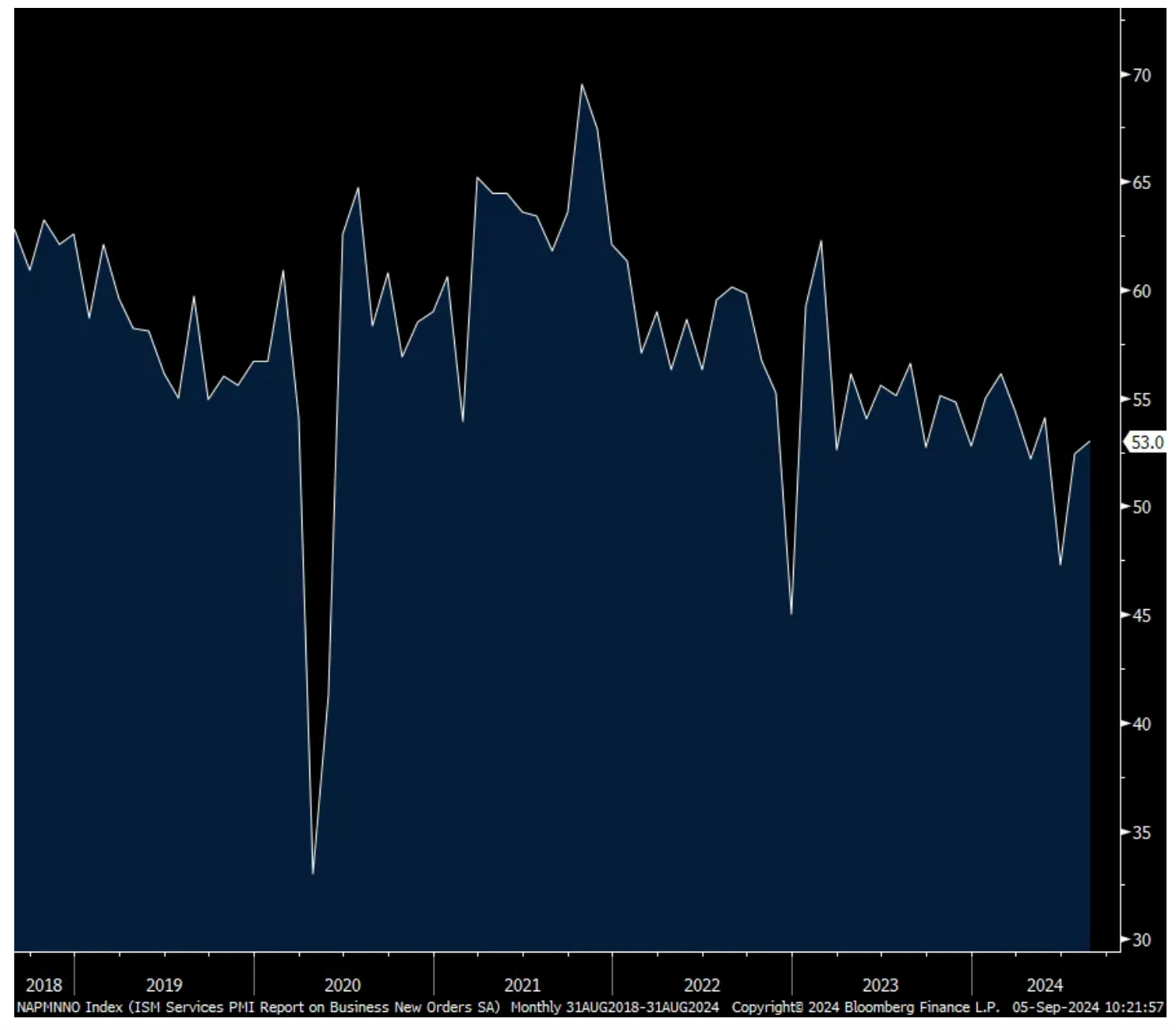

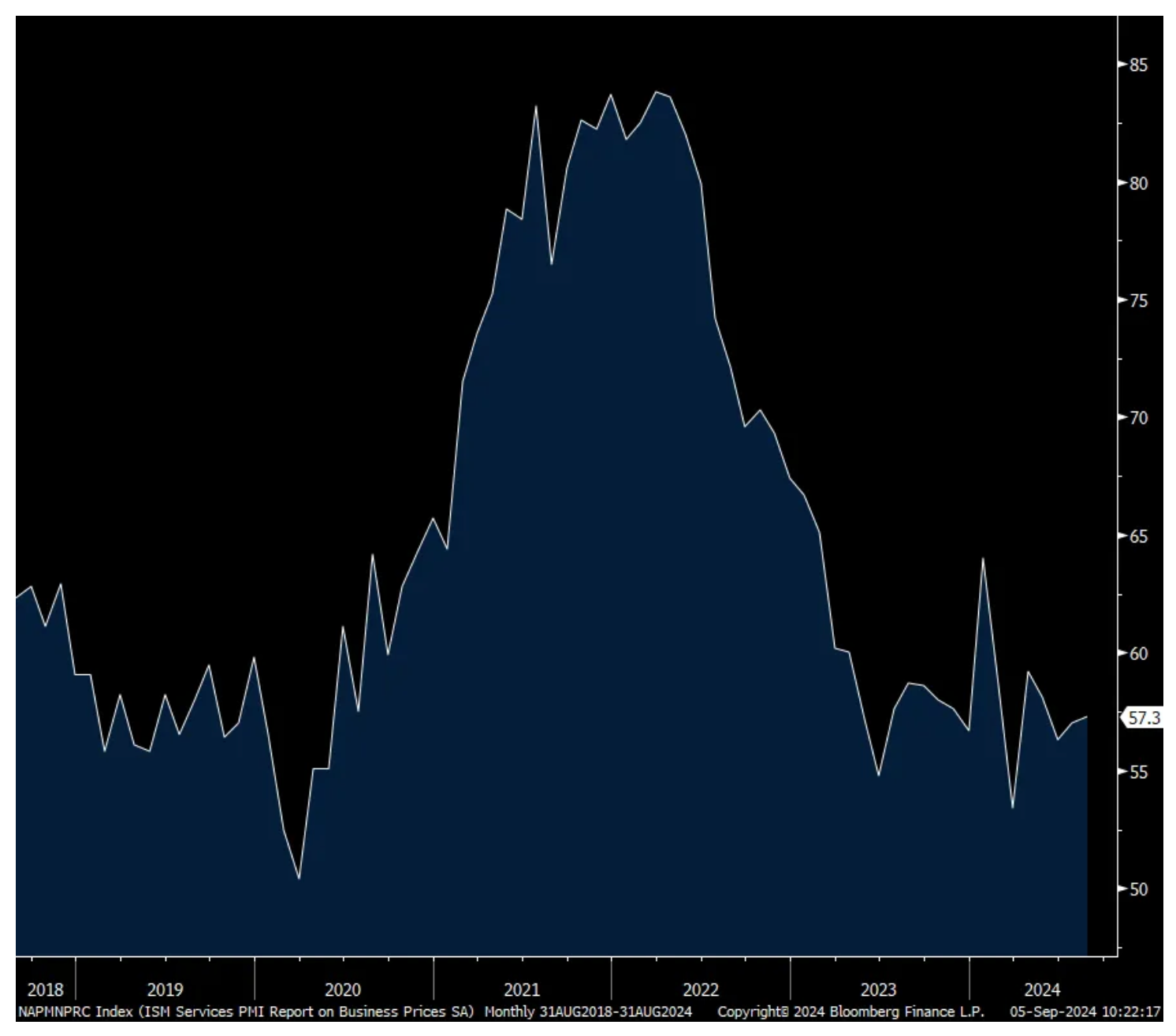

New orders rose to 53 from 52.4 and a touch above the 6 month average of 52.2 but just 8 industries of 18 saw an increase vs 10 in the three prior months. Backlogs though plunged to 43.7 from 50.6. Inventories got back above 50 at 52.9. Prices paid rose slightly to 57.3 from 47, around where the 56.9 six month average is at and remaining well above 50 but also well off its 2022 highs of over 80. Also, 13 of 18 industries said they paid higher prices vs 11 in July and 13 in June. Ahead of tomorrow, the employment component fell to 50.2 from 51.1. but still above 50 for a 2nd month after 5 months below. Just seven of 18 sectors added to their payrolls.

With respect to industry breadth, 10 of 18 industries saw growth, the same number seen in July. Seven saw business contract vs 8 last month with one seeing no change.

With this index barely above 50, the bottom line from the ISM was this, “Slow-to-moderate growth was cited across many industries, while ongoing high costs and interest-rate pressures were often mentioned as negatively impacting business performance and driving softness in sales and traffic.” I’ll add, barely above 50 for a 2nd month squares with the only slight economic growth that I’m seeing in the aggregate.

Some mixed commentary from respondents:

“Generally, business is good. However, there are concerns of slowing foot traffic at restaurants and other venues where our products are sold.” [Agriculture, Forestry, Fishing & Hunting]

“Housing market continues to be dampened by higher borrowing costs. All segments of the industry are affected. Single-family homes for sale, build for rent, and multifamily units are all feeling the effects.” [Construction]

“Activity is increasing.” [Finance & Insurance]

“Business continues to be strong.” [Health Care & Social Assistance]

“Overall business is improving.” [Information]

“Hiring of employees, contractors and consultants continues to decline as companies look to control costs during a period of economic and political uncertainty. Employee layoffs continue across a broad range of companies and industries.” [Management of Companies & Support Services]

“Business has slowed, and it is harder than ever to find talent, but less jobs available as well.” [Professional, Scientific & Technical Services]

“Up in business and activity.” [Transportation & Warehousing]

“Steady interest rates are impacting investment in nonregulated business silos.” [Utilities]

“High food costs are impacting customer demand, and weak sales performance has resulted in negative growth overall. Business activity is stable, and supplier costs are generally flat.” [Wholesale Trade]

ISM Services

New Orders

Prices Paid

BY Doug Kass · Sep 5, 2024, 12:10 PM EDT

BY Doug Kass · Sep 5, 2024, 11:55 AM EDT

RSP (equal weighted S&P) -0.87% compared to:

SPY -0.52%

QQQ -0.39%

BY Doug Kass · Sep 5, 2024, 11:50 AM EDT

I will be out of the office for the day at 2 p.m. as I have a few research/company meetings.

BY Doug Kass · Sep 5, 2024, 11:40 AM EDT

I covered the other half of my trading short rental in Berkshire Hathaway BRK.B at $468.50 (-$10).

BY Doug Kass · Sep 5, 2024, 11:33 AM EDT

The S&P Short Range Oscillator lifts from 2.54% to 3.26%.

BY Doug Kass · Sep 5, 2024, 11:20 AM EDT

I am adding to my homebuilder and private equity shorts now.

BY Doug Kass · Sep 5, 2024, 11:10 AM EDT

Dougie Kass

Covered half of my BRK.B short at $472 for a quick gain.

Dougie Kass

Long OIH $280.20

BY Doug Kass · Sep 5, 2024, 11:00 AM EDT

I covered my Apple AAPL short for a nice gain last week.

I am re-shorting the shares now (+$4.45/share) at $225.30.

But baby steps and on a scale higher.

BY Doug Kass · Sep 5, 2024, 10:50 AM EDT

* Investors tend to believe what they want to believe.

* Bullishness is often a contrarian sign.

* Investors are more bullish than ever.

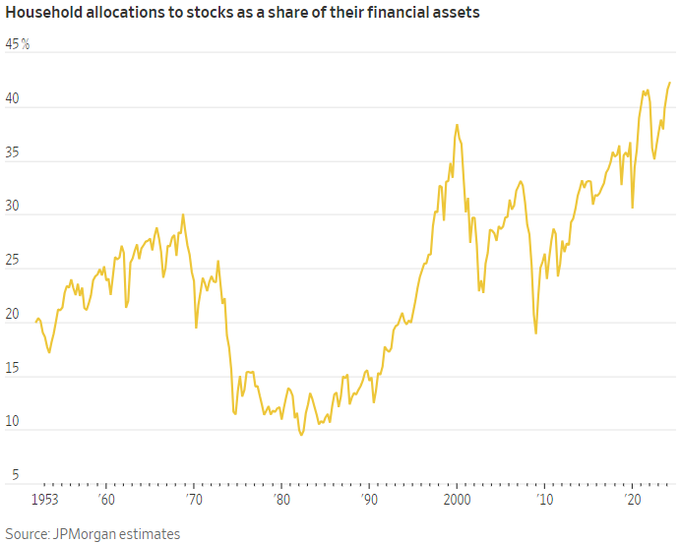

* Household allocation to equities is at the highest level since 1952 — in part to the belief of a "Goldilocks" fairytale (an economy not too hot and not too cold).

* I call BS to the level and manner in which S&P EPS are calculated in order to support bullish valuation arguments.

* And to government statistics that are not worth the paper they are written on.

Fairytales can come true, it can happen to you

If you're young at heart

For it's hard, you will find, to be narrow of mind

If you're young at heart

You can go to extremes with impossible schemes

You can laugh when your dreams fall apart at the seams

And life gets more exciting with each passing day

And love is either in your heart, or on its way

- Johnny Richards and Carolyn Leigh, Young at Heart

Investors tend to be bullish and believe the superficial BS that comes down the pike.

It is the nature of the human spirit to be upbeat — especially when it comes to our investments.

Unfortunately we can prove anything by statistics except the truth.

But tearing down "the statistics" and accepted truths can sometimes be revealing and lead to being more objective and a better investor.

As proven by the past (especially in the lead up to The Great Financial Crisis) objective analysis can also keep us from being trapped in false narratives and reduce the likelihood of losing loads of money!

As I have noted recently, at 42%, households' allocations to equities is at the highest level in 72 years:

To this observer, this allocation and the associated bullish investor sentiment may not be justified in the face of a number of headwinds including but not restricted to economic (slugflation likely lies ahead), policy (fiscal and monetary), political and geopolitical concerns, systemic stability and, the subject of today's missive — serious questions of what is the true level of S&P EPS that supports historically high (above 90%-tile) valuations.

But perhaps even more important is the lack of reliability of the economic data that forms our investment decision process.

From The Credit Strategist:

"Investors are unduly reliant on the Fed lowering interest rates and economic data whose reliability is increasingly subject to question. While they are rooting for the Fed to lower interest rates, it is unlikely that the Fed will do so aggressively. I have argued that the Fed shouldn’t do so at all until next year because it should maintain positive real (inflation-adjusted) rates at a respectable level and I don’t believe real rates are there yet. Despite government inflation statistics, real-world inflation is still pretty high (and remember, it is off a much higher base than before the pandemic). And recent events give little reason for us to trust the data supplied by the government. The recent elimination of 800,000 jobs from 2024 data by the Labor Department was an embarrassing error that shows the unreliability of government economic statistics. This was not a one-off correction. The government routinely retroactively adjusts economic statistics to a degree that shows they were highly inaccurate at the time they were released. This highlights the absurdity of the “countdowns” and other television hoopla that surrounds each Fed meeting and other economic news releases. We just have to hope that Rick Santelli doesn’t throw an embolism hyperventilating about the latest report of whether PCE comes in one-tenth-of-a-percent above or below the (totally blind) consensus. Investors treat this data like Buddhist monks interpreting koans when the information is no more meaningful than the crap printed on Page Six of The New York Post. No wonder the market behaves like a cross between a casino and a circus. The blind are leading the blind and they are all dressed up like Bozo."

Which brings us to the issue as to whether we are utilizing too-high S&P EPS numbers in justifying current valuations. (Make no mistake about it, even before my critical view of corporate profits — valuations are sky high based on historical comparisons!)

It is my conclusion that reported S&P EPS are no more accurate than government statistics.

When strategists and money managers justify their bullish market views based on unrealistic past and forward S&P EPS consider that those EPS numbers are routinely inflated by as much as 25% by non-GAAP adjustments. This serves to disguise cash flow and other key data points that are used in valuing equities.

Most investors disregard "adjustments" — certainly quants, machines and algorithms do! And, as I noted Wednesday, with so much capital flowing into passive products and strategies and with massive infusions of liquidity via central banks, there are few attempts to understand the increasingly complex, adjusted and fine-tuned.

Back to The Credit Strategist:

"The quality of reported earnings, and the quality of earnings reporting, is nothing less than appalling. This may make it challenging (and fun) for those of us trained to dissect balance sheets and financial filings, but it contributes to the false narrative that corporate earnings are robust. It also allows corporate managements to inflate their compensation by pumping up their stock prices with phony numbers. Non-GAAP adjustments contribute to the chronic overvaluation of stocks; they are no less a part of this systemic problem than profligate monetary and fiscal policy. When the book is written on the next financial crisis, bogus earnings will fill one of the chapters."

Facts are stubborn but statistics are more pliable.

Investors are basing their optimism on the fairy tales of inflated S&P EPS numbers as well as phony government statistics (see the recent revision of 818,000 jobs in the labor market!)

Believing in fairy tales is as old as the hills — and as long as equity prices keep rising (and the system stays intact) few question consensus narratives (as weak and superficial as they may be).

The lack of penetrating or even realistic analysis led up to The Great Financial Crisis, which few recognized as it unfolded.

Many similar issues — in deciphering "real EPS" and in the area of regulation — existed in 2008 that exist today.

Back then the U.S. government solved the debt crisis by creating more debt, rendering the financial system increasingly more fragile and prone to instability.

Since then, the illusion of prosperity (see our burgeoning deficit and U.S. debt) and the too liberal interpretation (at best!) of reported and projected U.S. corporates (measured as EPS) have convinced most investors that equities are inexpensive and that another financial crisis is avoidable.

These optimistic conclusions, like fairy tales, could end badly for investors.

For these reasons and others, the current level of unquestioning market optimism is a classic contrarian sign.

BY Doug Kass · Sep 5, 2024, 10:00 AM EDT

Randy

'OPEC+ nearing agreement to delay oil output hike, sources say' -Reuters

OPEC+ nearing agreement to delay oil output hike, sources say

escondida1

Doug -

Re OXY - I get why Warren likes OXY. They are focused on great ROI and Warren likes that. I don't know that Warren has expressed an opinion about oil prices and I know he's not specifically focused on where we are in a business cycle. That said, I don't get why you love it so much. Over the next year, OXY's stock performance will be more correlated with oil prices that its ROI relative to its competitors. I'm assuming you have a large position b/c you expect a good move (at least within the range) in the relatively short-term. Isn't your investment more an oil price bet than an OXY bet? Sorry for being so wordy!

BY Doug Kass · Sep 5, 2024, 9:40 AM EDT

From Peter Boockvar:

Labor market comments in Beige Book/Earnings call rundown/BoJ has another reason to hike

I'll repeat here again what the Fed's Beige Book's bottom line was. Of the 12 Districts, nine saw "flat or declining activity" vs five in the prior Beige Book. In the other three, "economic activity grew slightly." There is a big disconnect here between what GDP is telling us and this. Maybe right now Gross Domestic Income is a better reflection of the growth rate of the US economy where it printed 1.3% growth in Q2, the same pace seen in Q1.

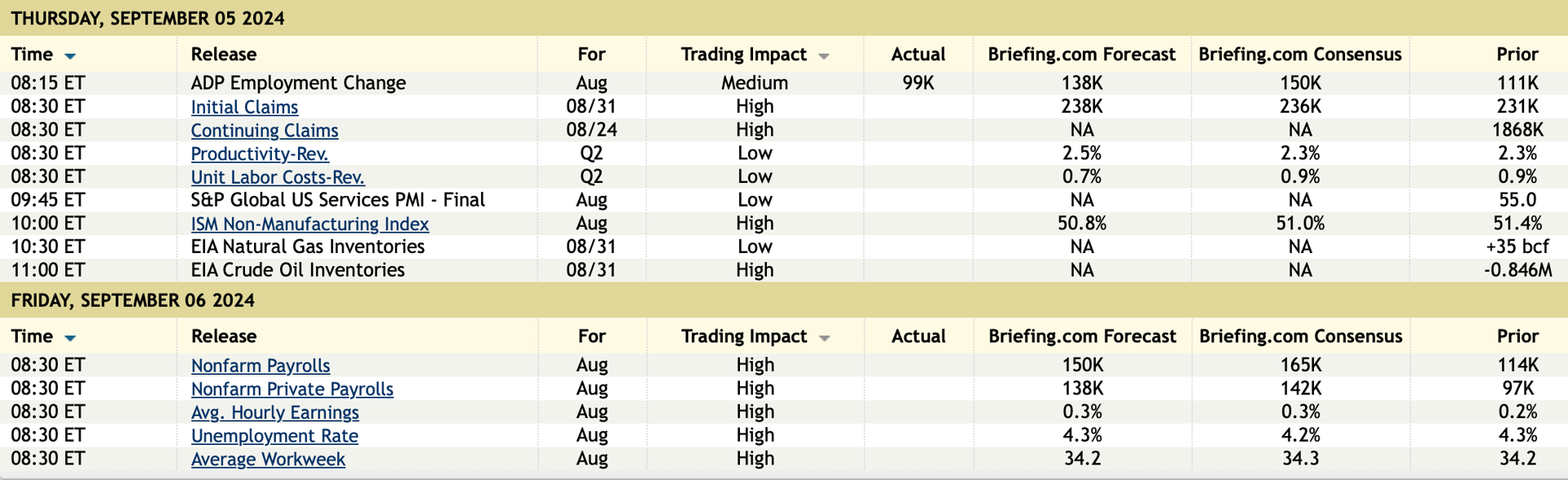

Ahead of ADP today and payrolls tomorrow and the Fed's shift in attention to the labor market, here were some of the key comments on jobs. It reads to me like we're seeing a clear downshift in the pace of adding new workers.

Boston:

"Employment levels were unchanged on balance and no major layoffs were reported...Staffing contacts said that job creation had slowed owing to increased caution in the face of economic uncertainty. Employers reportedly became more selective about workers' qualifications and did not face substantial hiring difficulties."

NY:

"Labor market tightness continued to moderate, with ongoing cooling in labor demand and increased labor supply across the District. Contacts at employment agencies noted hiring activity in both New York City and across upstate New York has slowed as firms are approaching hiring decisions with greater hesitancy. Hiring has shifted to be primarily for replacement, rather than growth, and with uncertainty pertaining to the presidential election ahead, many firms have put hiring plans on hold. It has become much easier to find workers, particularly for firms offering remote or hybrid work options. Still, some contacts from industries that require in-person work reported some difficulty finding skilled workers, particularly in the skilled trades. Multiple contacts reported that worker attrition has declined to exceptionally low levels, and job candidates are lingering on the market for longer."

Philly:

"Employment appeared to decline slightly, following modest growth in the prior period. Based on our July and August surveys, full-time employment declined for nonmanufacturing firms and was flat to slightly higher for manufacturing firms, on average. While over half of both manufacturers and nonmanufacturers continued to report no change in employment during the period, a rising share of nonmanufacturers reported a decrease in their number of employees...Staffing contacts continued to report little change in demand. Multiple contacts reported that hiring was broad-based across industries, except for the tech industry. One contact relayed that a tech company had recently laid off its entire recruitment staff. Another contact mentioned that some businesses had slowed internal recruiting efforts, turning to staffing agencies instead."

Cleveland:

"Overall, employment levels were stable to slightly up in recent weeks. Most firms reported keeping their staffing levels unchanged over the recent reporting period, often citing steady demand and a desire not to over-hire for current business conditions. For firms that are adding to their workforce, some reported hiring to accommodate business growth. By contrast, several contacts reported adjusting to weaker demand by leaving open positions unfilled. On balance, firms expected to increase employment levels slightly over the coming months."

Richmond:

"Employment in the Fifth District increased slightly in the most recent period. Several contacts reported satisfaction with current headcounts and were only backfilling for necessary positions. Other contacts were allowing headcounts to decline mainly through attrition. A software company did not expect to increase headcounts due to adequate staffing levels that could handle increases in demand. Finding skilled workers continued to be a challenge. A construction company reported plenty of work but not enough staff despite advertising for open positions. Some businesses reported positive changes in skilled-worker availability."

Atlanta:

"Employment in the Sixth District increased modestly over the reporting period. Most firms continued to report improvements in talent availability. A few noted labor reductions, mostly in the form of cutting regular and overtime hours and, in a minority of cases, layoffs. However, several firms said that further weakening of demand could result in future layoffs. While many firms reported that they will continue to fill vacant positions, several noted that they were slowing the pace of hiring for the remainder of the year. Only a few indicated they would be staffing up in anticipation of future growth."

Chicago:

"Employment rose slightly over the reporting period, but contacts expected job growth to pick up to a modest pace over the next 12 months. Many contacts continued to note difficulty filling higher skilled positions. That said, there were signs of softening in the labor market. Contacts in both the manufacturing and service sectors reported layoffs or shift reductions in response to slower demand. One contact said they were only recruiting to backfill vacated positions, and a fabricated metals manufacturer had paused hiring until demand from the housing sector picked up."

St. Louis:

"Employment has remained unchanged since our previous report. Contacts reported more people applying for open positions. While the majority of contacts noted that hiring pressures have eased noticeably, in several cases employers continue to face challenges filling open positions, particularly for skilled workers. A construction materials supplier noted that finding quality candidates remains an issue. A hotel contact in Memphis reported limited abilities of their workforce was a continuing challenge but it had started to improve with recent hires. While quasi-governmental contacts reported strong recruiting and staffing, business contacts expect slower employment growth the remainder of this year. Contacts also noted they were continuing to reduce employment slightly through attrition, although attrition had decreased considerably since the start of the year."

Minneapolis:

"Employment was flat since the last report. Employers again reported fewer job openings. A small majority of firms reported that they were hiring, but many were replacing turnover, and a smaller share were adding full-time staff compared with earlier in the year. The share of firms cutting workers also grew but remained in the single digits. Overall, firms do not expect staffing levels to grow much over the next six months. A Minnesota staffing contact reported that job orders were down, "and a lot of businesses are getting a lot more picky" about who they hire. Labor availability continued to improve, though labor quality remained an issue. A South Dakota manufacturer said that labor "has undergone shrink-flation. [We're] paying more for lower quality."

KC:

"District contacts reported little job growth over the last month. In the service sector, a slight decline in employment at professional business service firms was offset by modest hiring at consumer-oriented businesses. Overall, business contacts reported their current hiring plans for the remainder of the year will leave their headcount slightly below levels they expected at the beginning of the year, as many firms reigned in their recruiting efforts in recent months. Businesses reported particular weakness in the labor market for entry-level occupations and in the demand for workers with limited experience. Contacts expressed less willingness to hire inexperienced workers as applicant quality improved with greater availability of more experienced workers. Furthermore, contacts noted they posted fewer entry-level positions as they sought instead to reallocate existing employees from business lines with waning demand. Skilled workers in the trades were a notable exception, where demand for workers remained strong regardless of experience."

Dallas:

"Employment was largely flat over the past six weeks. Some firms reported implementing hiring freezes due to economic uncertainty or weak demand, though most view this as a temporary measure and anticipate hiring later in the year. Still some firms noted difficulty hiring for openings ranging from entry-level positions to upper-level management, and especially mid-skill workers including commercial drivers."

SF:

"Employment rose slightly over the reporting period overall. Most contacts across the District cited steady to slightly higher employment levels and improved retention rates, while others, including those in banking and professional services, expanded their payrolls moderately. Nonprofit organizations reported increased hiring to meet the growing demand for community and support services. In contrast, companies in the entertainment and aerospace sectors lowered their headcounts through layoffs. Many contacts continued to note an increase in job applicants, although some cited skills mismatch and difficulty filling specialized positions. Employers continued to see labor turnover slowing, in part due to engaging in more selective hiring and offering enhanced professional development."

By the way, rate cut odds for 50 bps in two weeks is at 42% vs 30% Friday.

On to some earnings calls.

From Dollar Tree:

"As we have seen for several quarters now, demand from Family Dollar's core lower income customer remains weak. Dollar Tree has a broader customer base that includes more middle and upper income households. And beginning this quarter, we started to see inflation, interest rates, and other macro pressures have a more pronounced impact on the buying behavior of these customers. This impacted our 2nd quarter comp performance and is the primary driver of our revised full year outlook."

For Dollar Tree, "While comps were positive in each month, they softened sequentially throughout the quarter...Consumable categories like candy, apparel, snacks and beverages were our best performing areas in Q2, while higher margin discretionary categories like crafts, floral, and home decor underperformed."

For Family Dollar, "Comps were positive in the middle month of the quarter and negative in the first and last months." According to them, "over 40% of Family Dollar customers are eligible for some form of government assistance, including SNAP, and those benefits are a meaningful part of their household resources."

"Shrink remains a major topic across retail. While shrink remains unacceptably high, it appears to be stabilizing. While it is too early to declare victory, I am pleased that our targeted actions and interventions helped our 2nd quarter shrink rate."

From Dick's Sporting Goods:

Their comps grew 4.5%, adjusted for the calendar shift and "This strong comp was driven by growth in average ticket and in transactions. We saw more athletes purchase from us, and they spent more each trip compared to the prior year." Growing market share is also helping their comps.

"this past quarter, we saw growth across all income demographics, which was terrific, and we saw more athletes purchase from us, spending more per trip."

In terms of product, "We did see particular strength in footwear and apparel. And we saw some puts and takes within hardlines."

With regards to their guidance, "the difference between the high end of the range or the low end of the range is balancing the macroeconomic uncertainties that exist. As you know, the consumer continues to be under pressure, and we are balancing our optimism and our confidence in our core strategy against the macroeconomic backdrop."

From Hewlett Packard Enterprises who grew revenue by 10% but whose full year guidance is 1% to 3% in constant currency:

"Overall, the demand environment this quarter has improved. We saw sequential and y/o/y orders growth, but with some geographic variation. Demand was strong in North America, Asia-Pacific, Japan and India, while Europe and the Middle East lagged." They are particularly seeing strength in their AI server systems and hybrid cloud.

"While some customers remain cautious and prioritize mission-critical projects, we are encouraged by the recovery and enterprise demand we are seeing in North America, followed by modest improvement across the other geographies."

"In fact, more than 80% of enterprises are experimenting with GenAI initiatives, which supports our view that the number of customers will continue to trend favorably."

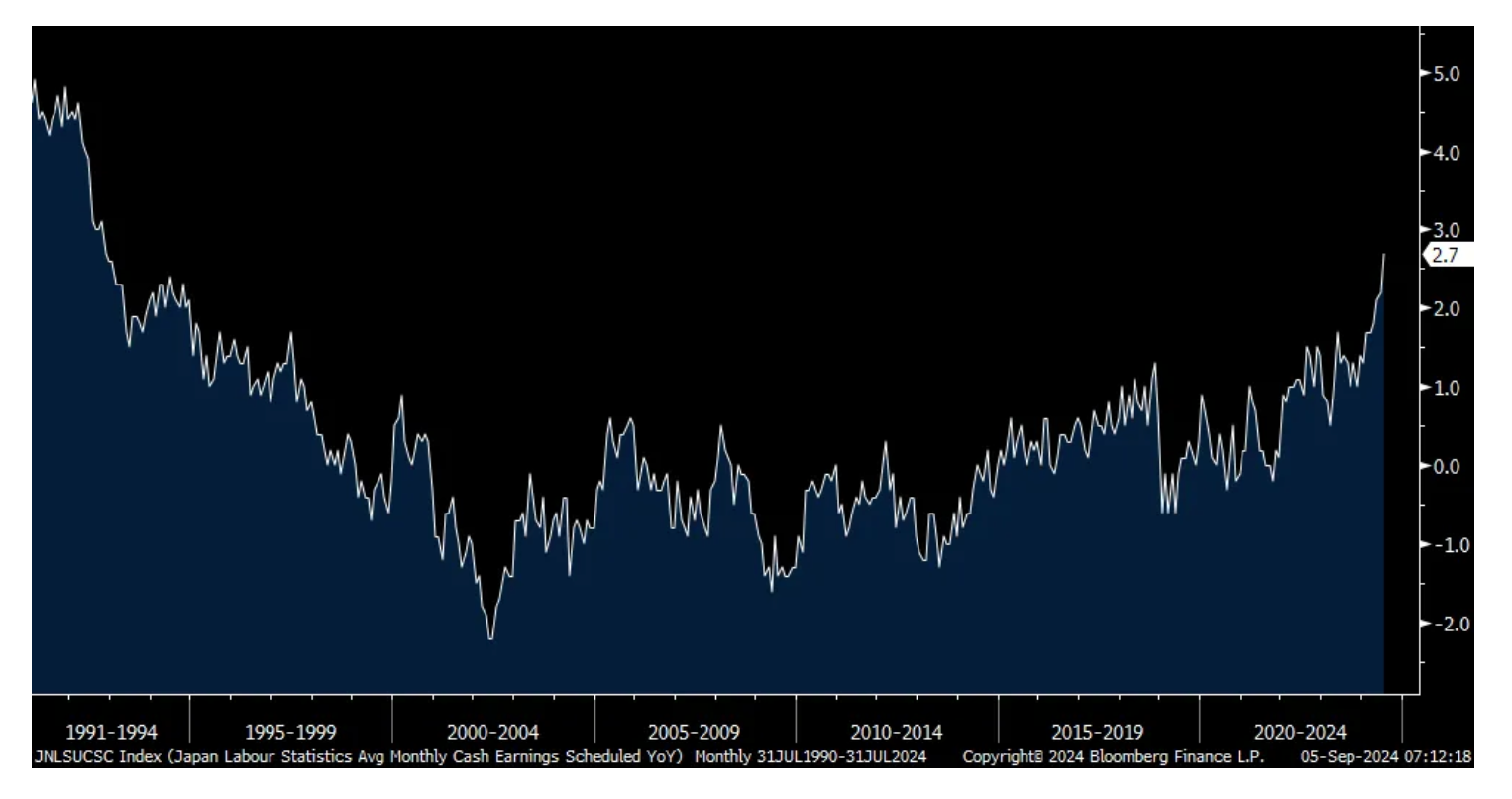

Overseas, the BoJ was given more reason to raise interest rates again as the higher wage Shunto negotiations continues to flow into the data. Base pay rose 2.7% y/o/y in July, the quickest since 1992. JGB yields were unchanged but the yen is slightly higher while the Nikkei sold off again.

Chiming in for a second on the extreme political resistance to the Nippon Steel deal for US Steel, I think it's ridiculous. US Steel has been a challenged company for decades in a very volatile industry and Japan is our friend. The growing protectionism is not good.

Base Pay in Japan y/o/y

German factory orders in July surprised to the upside but was all led by big ticket orders which if not included, they would have fallen by .4%. The headline gain was 2.9% m/o/m vs the estimate of a drop of 1.7%.

BY Doug Kass · Sep 5, 2024, 9:25 AM EDT

-APLD +31% (reportedly raised $160M in funding round that included Nvidia)

-MODD +18% (announces FDA Clearance of the MODD1 Insulin Pump)

-SOAR +12% (announces strategic agreement with flyExclusive and outlines continued growth plans)

-YEXT +9.2% (earnings, guidance)

-INDP +6.1% (reports encouraging new safety data for Decoy20 clinical program)

-JBLU +5.0% (raises Q3 guidance)

-MODG +4.1% (intends to separate into two independent companies; to create leading golf equipment and active lifestyle company and pure play venue-based golf entertainment business)

-FTV +3.9% (confirms strategic plans for separation into two independent public companies; affirms Q3 and FY24 guidance)

-LE +2.6% (earnings, guidance)

-PHR +2.4% (earnings, guidance)

-MOV +2.3% (earnings, guidance)

-AI -19% (earnings, guidance)

-VRNT -13% (earnings, guidance; announces $200M share buyback program)

-BKSY -12% (announces 1-for-8 reverse stock split)

-CRDO -11% (earnings, guidance)

-FYBR -10% (Verizon confirms to acquire Frontier for $38.50/shr in cash)

-TTC -8.6% (earnings, guidance)

-CSWI -7.8% (announces upsize and pricing of public offering of common stock; to sell 1.1M common shares (prior 1.0M shares))

-INAB -7.4% (announces clinical pipeline prioritization to focus on INB-100 for Acute Myeloid Leukemia with additional enrollment in 1H25 and long-term follow-up results anticipated in late 2025 and 2026; to cut workforce by 49%)

-XPO -5.9% (Wells Fargo cuts price target to $119 from $125)

-VVX -5.2% (prices 2M shares at $48/share for selling stockholder)

-CPRT -4.8% (earnings)

-HPE -3.5% (earnings, guidance)

-DSGX -3.0% (earnings)

-CXM -2.9% (earnings, guidance)

-SCWX -2.5% (earnings, guidance)

-UTZ -2.4% (cuts FY24 Rev guidance)

BY Doug Kass · Sep 5, 2024, 9:15 AM EDT

As of 8:52 a.m.:

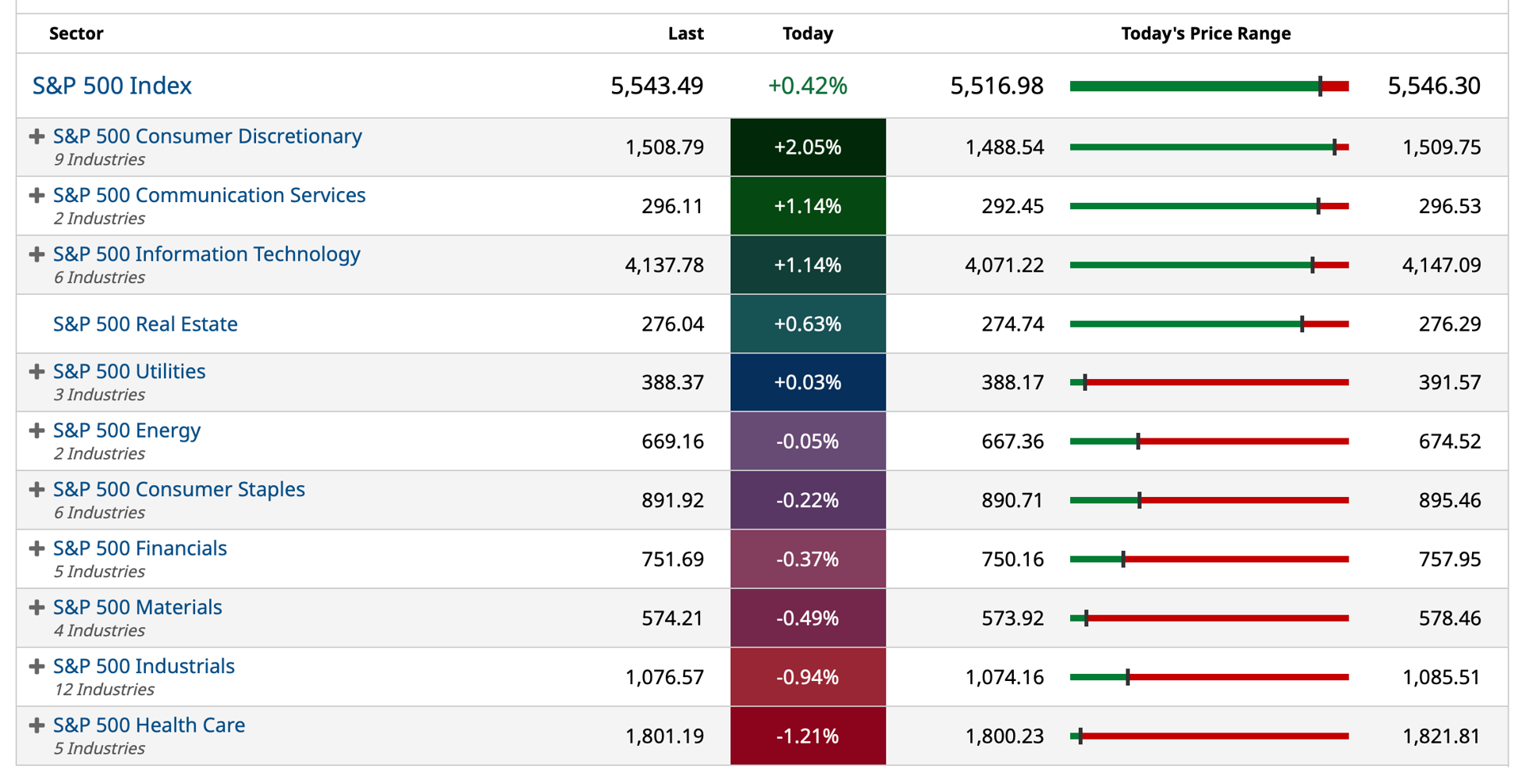

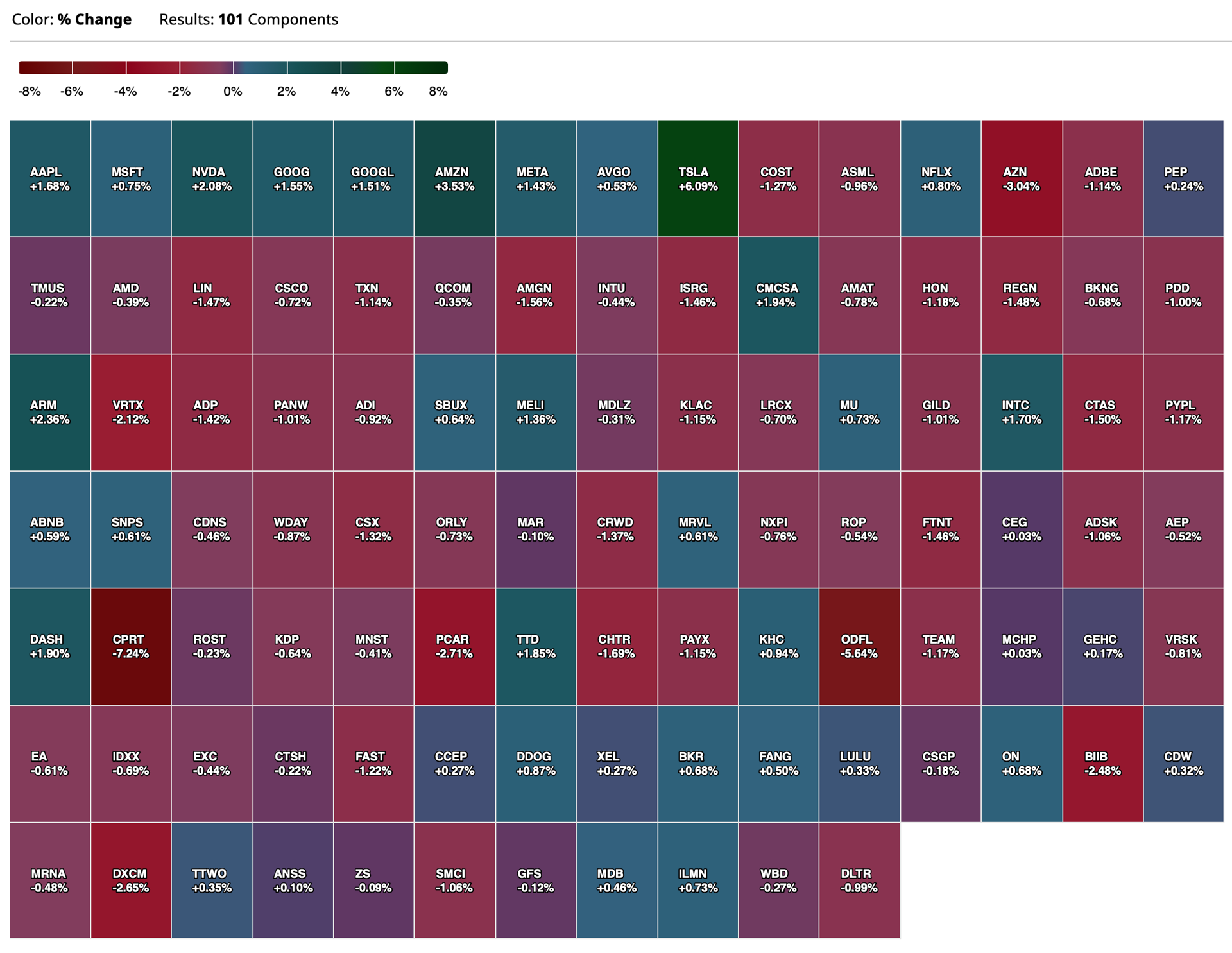

BY Doug Kass · Sep 5, 2024, 9:02 AM EDT

As of 8:29 a.m.:

BY Doug Kass · Sep 5, 2024, 8:55 AM EDT

BY Doug Kass · Sep 5, 2024, 8:25 AM EDT

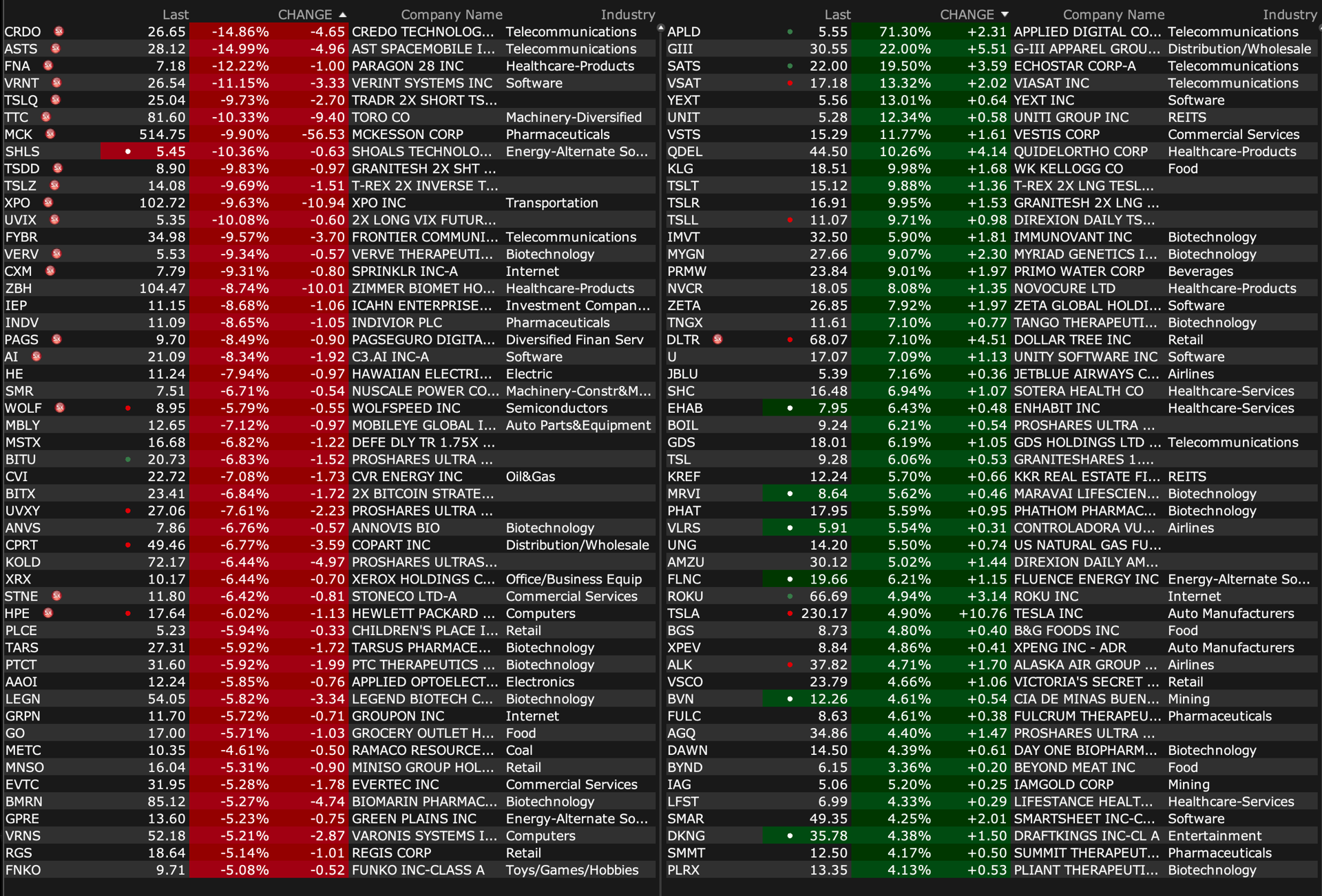

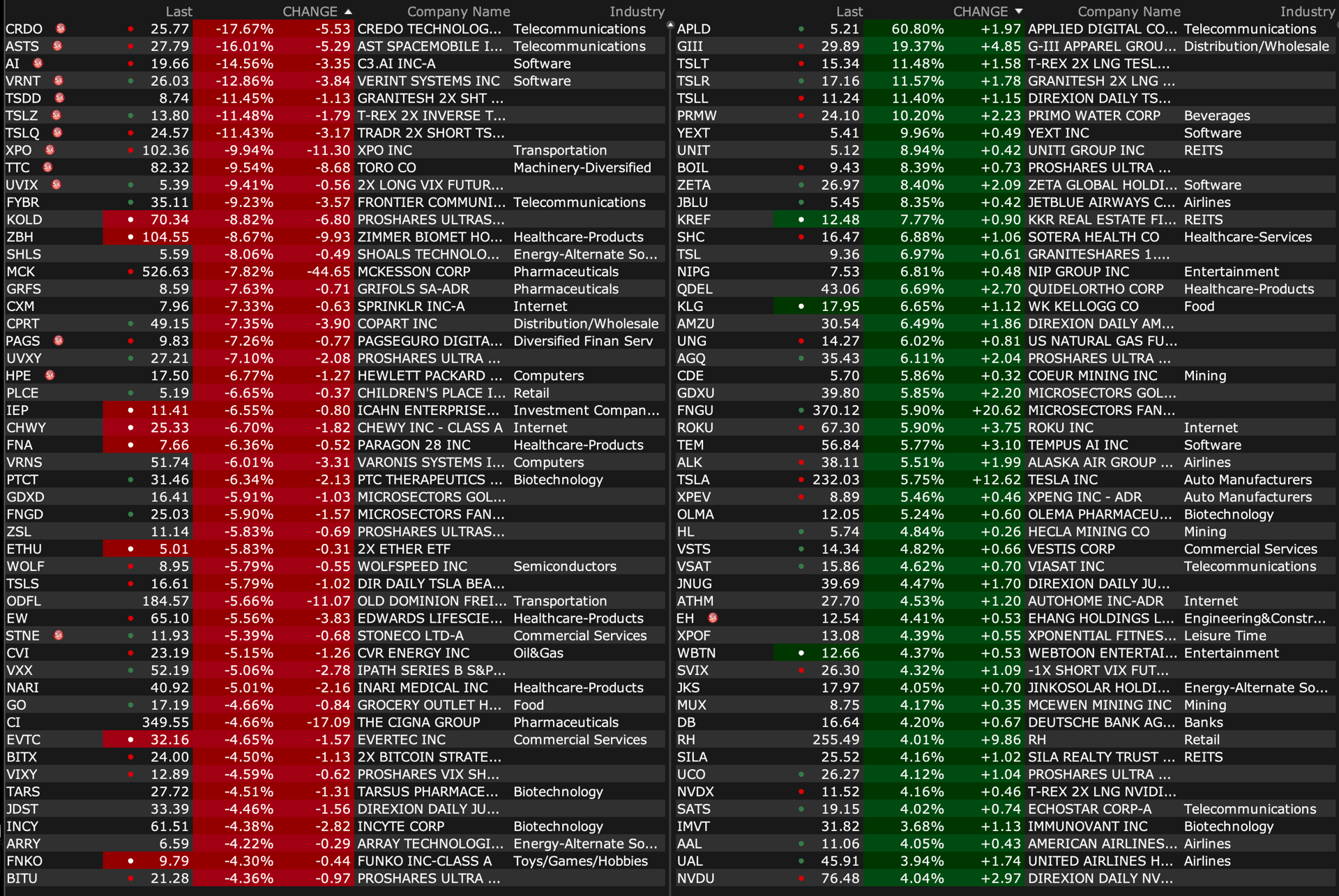

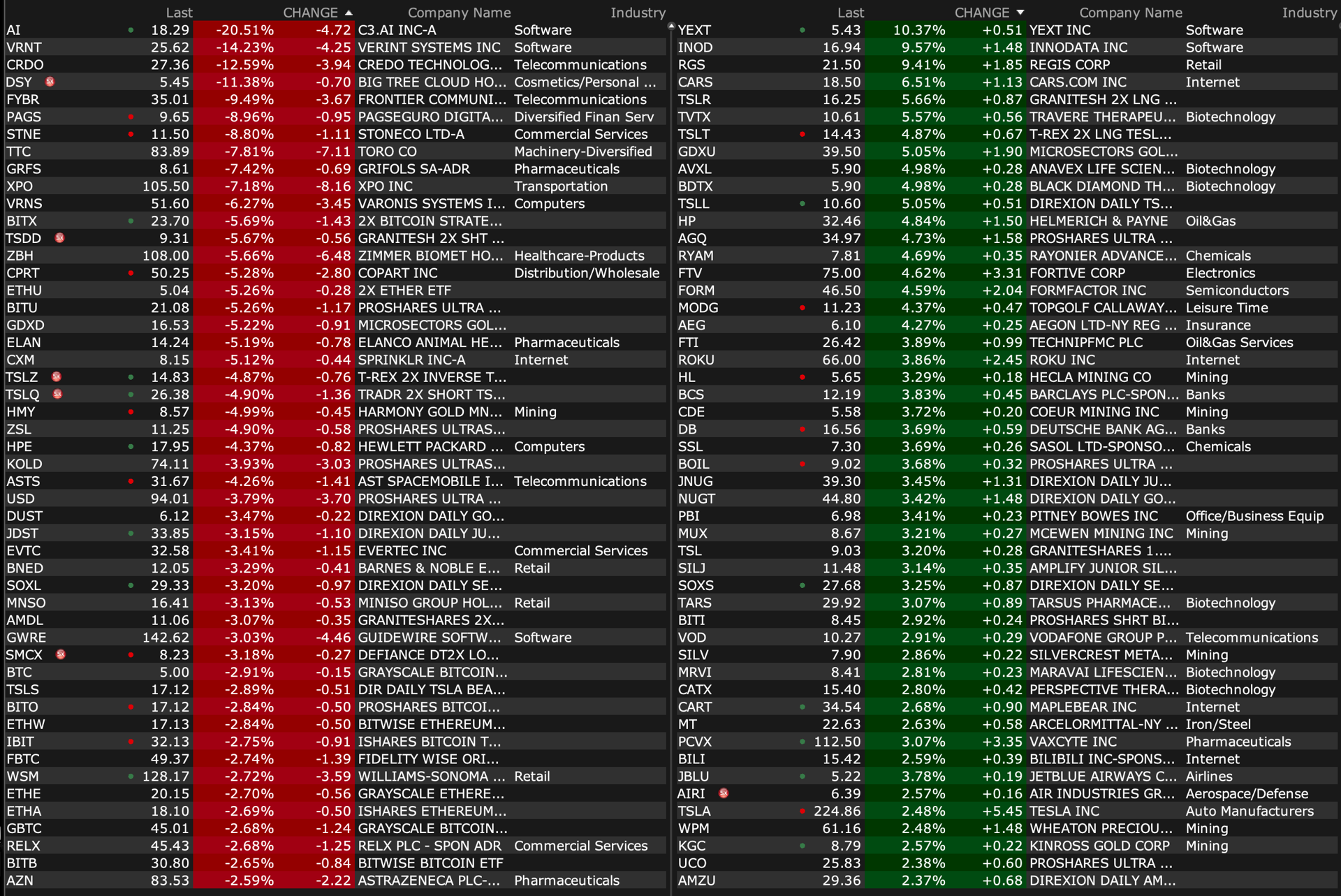

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Sep 5, 2024, 8:05 AM EDT

From JPMorgan:

US: Futs are flat as the global sell-off stabilizes into the most important macro data releases. Pre-mkt, NVDA is +40bps and TSLA +2.3% as the balance of Mag7 is weaker and Semis under pressure, too. Bond yields are 1bps higher, but USD is weaker. Cmdtys are stronger led by Energy and precious metals. 50bps bets are increasing as the growth component of the Goldilocks narrative is challenged. ISM-Srvcs today and NFP tmrw are key facets of the narrative and we should leave for the weekend with a stronger sense of 25bps or 50bps.

and...

EQUITY AND MACRO NARRATIVE: A negative start to the week but the bigger catalysts are today and tomorrow. Today’s ISM-Srvcs, where Feroli is above the Street at 52.0 vs. 51.4 survey and 51.4 prior, will help reshape the growth narrative. ADP will be watched but it is not necessarily predictive of tomorrow’s NFP.

· “We look for the ISM services index to increase slightly to 52.0 in August from 51.4 in July. The index has recently been quite choppy, and while it rose last month the trend has been generally toward softer readings, with the July value and the three month average both below what would normally be expected in an economic expansion.” – Mike Feroli (full note is here).

NFP SCENARIO ANALYSIS

Feroli’s full NFP preview is here. He sees 150k jobs being added, which is below the Street’s estimate of 165k. For the unemployment rate (U.3), he sees 4.3%, above the Street’s estimate of 4.2%.

The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view from JPM US Market Intelligence.

· [5%] Above 300k. This is a tail-risk scenario. The last time we saw an upward surprise of at least 150k job was the February 2 print, where SPX and NDX added 1.1% and 1.7% on the day, respectively. We could see the market quickly remove the possibility of a 50bp cut with yields spiking. Under this scenario, hourly earnings will be critical to assess if the labor surprise coincides with renewed wage inflation. Look for bonds to reprice higher, providing a headwind to bigger 1-day gains but ultimately the improvement in growth is positive for risk assets SPX gains 0.25% to 0.50%.

· [25%] Between 200k and 300k. Given that the highest estimate on the Street is 208k, with NFP printing above most Street estimates, this will rebuild growth confidence from the August print. The recent GDP, spending, and inflation data will give comfort that the elevated real GDP growth experienced over the last year continues. However, a hotter average hourly earnings print could rekindle wage inflation fears. Further, a print at the top of the range may pare rate cut expectations not just to 25bps in September but towards 75bps for 2024 versus the 110bps of cuts priced into markets currently. SPX gains 1.00% to 1.50%.

· [40%] Between 150k and 200k. This scenario is largely in line with Street expectations. Feroli sees 150k jobs being added with the unemployment rate remaining at 4.3%. This scenario is more in line with a 50bp cut at the September Fed meeting given the strong trend in labor supply and softening in labor demand. Even at the top end of the range, we likely see a 50bps cut in September given the softening in labor demand and core inflation that appears under control. .SPX gains +0.75% to +1.25%.

· [25%] Between 50k and 150k. The immediate reaction is negative as the market quickly adapts to higher recession risks. Given Tuesday’s risk-off positioning, the market may be cleaner going into this NFP event than in previous prints. The market will quickly coalesce around a 50bps cut, with the biggest downside risk that the market adopts the recession / growth scare narrative. SPX falls -0.50% to -1.00%.

· [5%] Below 50k. Another tail-risk scenario since NFP has not been under 100k since December 2020. This will immediately create renewed growth fears, and we may start to fully price in a 50bp cut in September with the possibility of expectations for a 75bp cut being introduced. In this case, aligned with rate cutting cycles of the past, the market may believe that the US is already in a recession, and it would not pay to buy the first rate cut. SPX falls -1.25% to -2.00%.

· WHAT ARE OPTIONS PRICING? For options that expire Friday, September 6, we are seeing about a 1.40% move.

· US MKT INTEL VIEW – We see a bullish outcome after an inline print. Subscribing to the Mike Feroli view of the Fed, where by there is enough evidence that shows the Fed needs to be materially less restrictive and that neutral rate is likely ~200bps before current levels. Given that the Fed missed on “transitory inflation narrative”, it seems more likely that they front load rate cuts as they assess the 2-sided risk of either (i) recession or (ii) re-igniting inflation. It will be interesting to see the impact on consumer and business confidence and resulting spending behavior.

· MONETIZATION MENU – Our expression of the tactical bull case remains utilizing the barbell but with a heavier tilt towards the Cyclical/Value components. For clients who disagree and are holding a tactically bearish view, driven by negative seasonality and election uncertainty, you may consider being long Defensives such as Healthcare, Utilities, and Staples while using QQQs to get net short. In both scenarios, I think a bias towards Quality irrespective of sector continues to make sense given bond yields are unlikely to approach pre-COVID levels in the near-term.

BY Doug Kass · Sep 5, 2024, 7:55 AM EDT

I am growing more upbeat on cannabis (and the eventuality of favorable legislation):

BY Doug Kass · Sep 5, 2024, 7:40 AM EDT

BY Doug Kass · Sep 5, 2024, 7:25 AM EDT

* To stay abreast and as a reminder — I am introducing this as a new daily column (tell me if it is helpful)...

* I materially expanded my JPMorgan JPM short.

* Legging into a Berkshire Hathaway BRK.B short.

* In keeping with my JPM and BRK.B shorts (the most significant components of the ETF), I moved to medium-sized short XLF.

* Added considerably to an already large Occidental Petroleum OXY long. Waiting for Warren has been like waiting for Godot over the last few weeks — but, like Elijah, I expect an appearance (and an increased Berkshire Hathaway stake)!

* I added to my cannabis longs — especially MSOS and GTBIF.

BY Doug Kass · Sep 5, 2024, 6:55 AM EDT

From my pal Larry McDonald:

BY Doug Kass · Sep 5, 2024, 6:45 AM EDT

BY Doug Kass · Sep 5, 2024, 6:35 AM EDT

Bonus — Here are some great links:

Technicals to Watch in September

Here Comes the Worst Month of the Year

BY Doug Kass · Sep 5, 2024, 6:20 AM EDT

My concern and one of the reasons we are seeing a consumer-based economic slowdown — stacked/cumulative inflation:

BY Doug Kass · Sep 5, 2024, 6:08 AM EDT

BY Doug Kass · Sep 5, 2024, 5:55 AM EDT

* The longest inversion in history has ended.

* Such a normalization typically occurs near the start of recessions.

BY Doug Kass · Sep 5, 2024, 5:45 AM EDT