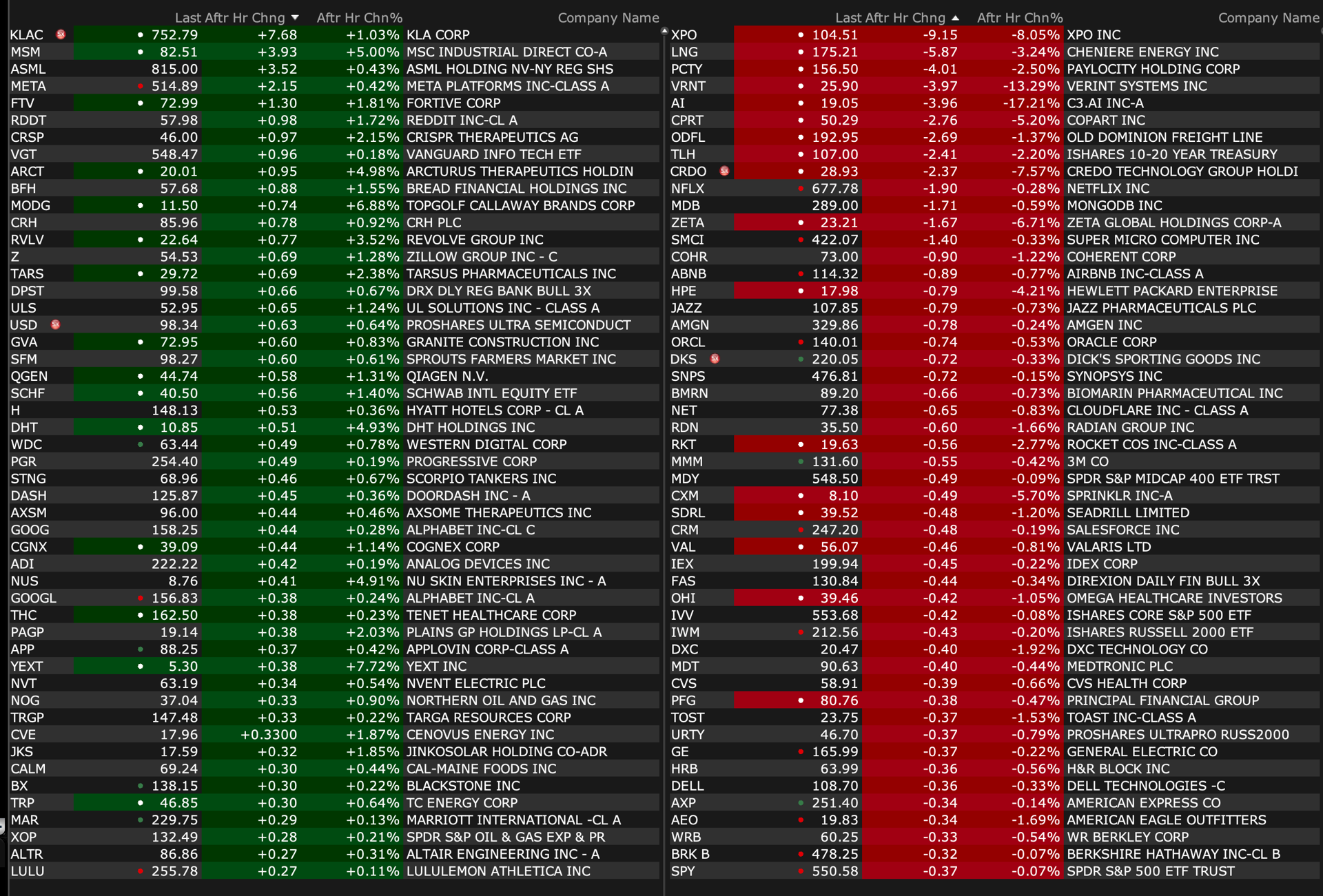

After-Hours Movers

As of 4:38 p.m.:

BY Doug Kass · Sep 4, 2024, 4:50 PM EDT

As of 4:38 p.m.:

BY Doug Kass · Sep 4, 2024, 4:50 PM EDT

Wolf Street on labor "normalcy."

BY Doug Kass · Sep 4, 2024, 4:30 PM EDT

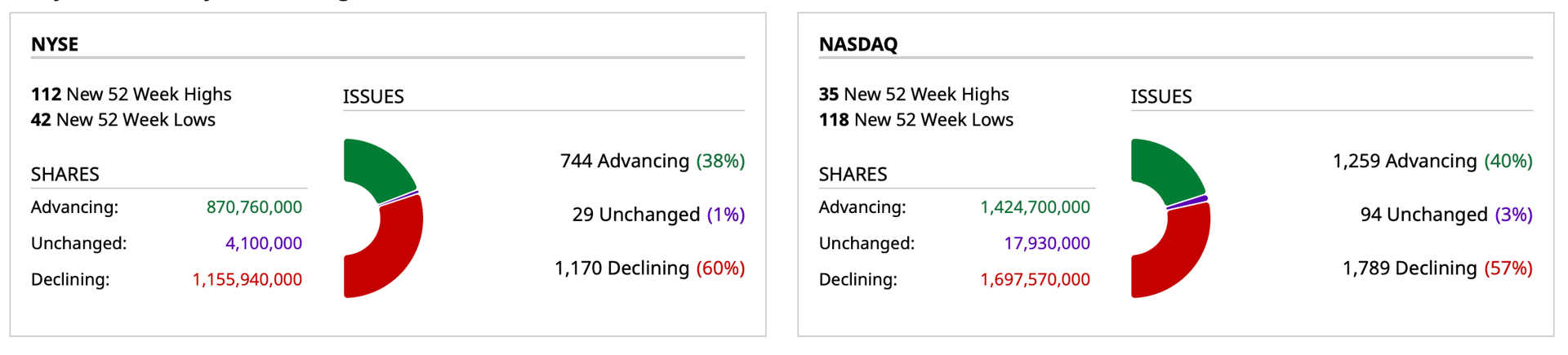

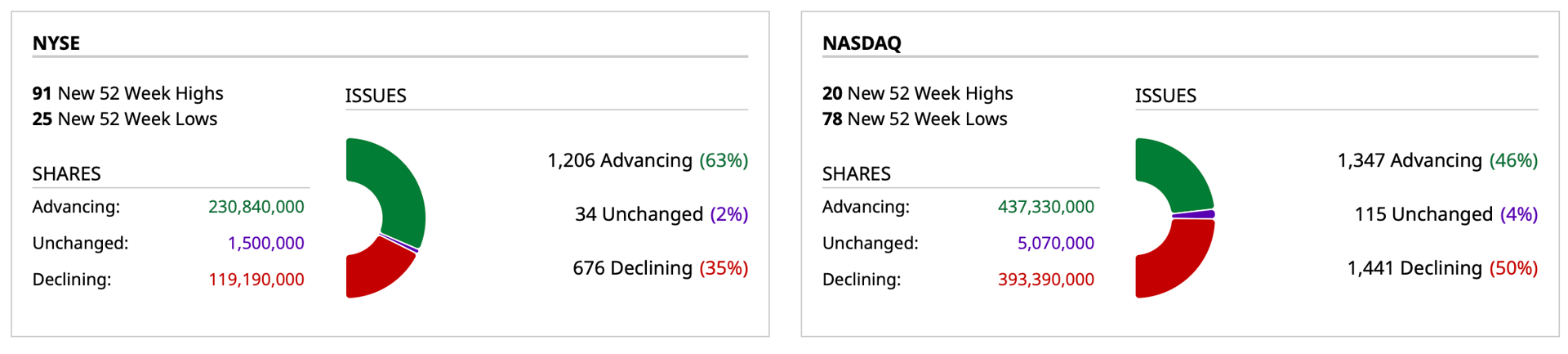

- NYSE volume 1% below its one-month average;

- NASDAQ volume 6% below its one-month average

BY Doug Kass · Sep 4, 2024, 4:15 PM EDT

From Peter Boockvar:

Maybe sounds like a .5-1% GDP growth rate, certainly not 3%

I’ve been arguing for months that the US economy feels much more like a 1-1.5%, and certainly not the 3% print for Q2 (though first half is averaging 2%). After reading the Fed’s Beige Book introductory paragraph, I might even be generous with the upper end of my range and should lower it to .5-1% growth outlook.

I’m going to go through the rest of the Fed commentary but the only area of economic growth I see is from the higher income consumer spending on travel, leisure, and hospitality and that includes live entertainment (I did see Pearl Jam last night at MSG and the place was packed), anything related to AI spend, and of course government spending, covering healthcare, interest expense (aka, helping the beneficiaries of all that interest income, particularly that higher income saver/boomer), defense and the CHIPS Act and IRA.

From the Beige Book and I bolded for emphasis:

“Economic activity grew slightly in three Districts, while the number of Districts that reported flat or declining activity rose from five in the prior period to nine in the current period. Employment levels were steady overall, though there were isolated reports that firms filled only necessary positions, reduced hours and shifts, or lowered overall employment levels through attrition. Still, reports of layoffs remained rare. On balance, wage growth was modest, while increases in nonlabor input costs and selling prices ranged from slight to moderate. Consumer spending ticked down in most Districts, having generally held steady during the prior reporting period. Auto sales continued to vary by District, with some noting increases in sales and others reporting slowing sales because of elevated interest rates and high vehicle prices. Manufacturing activity declined in most Districts, and two Districts noted that these declines were part of ongoing contractions in the sector. Residential construction and real estate activity were mixed, though most Districts' reports indicated softer home sales. Likewise, reports on commercial construction and real estate activity were mixed. District contacts generally expected economic activity to remain stable or to improve somewhat in the coming months, though contacts in three Districts anticipated slight declines.”

BY Doug Kass · Sep 4, 2024, 4:01 PM EDT

BY Doug Kass · Sep 4, 2024, 2:50 PM EDT

I am using a $9.75 limit to buy more Green Thumb GTBIF.

BY Doug Kass · Sep 4, 2024, 2:40 PM EDT

BY Doug Kass · Sep 4, 2024, 2:35 PM EDT

Adding to MSOS with a $6.50 limit — that's a higher buy level than yesterday— and buying September/October in the money calls.

BY Doug Kass · Sep 4, 2024, 1:42 PM EDT

Financials are beginning to roll over in a possible sign of exhaustion.

BY Doug Kass · Sep 4, 2024, 1:20 PM EDT

From Peter Boockvar:

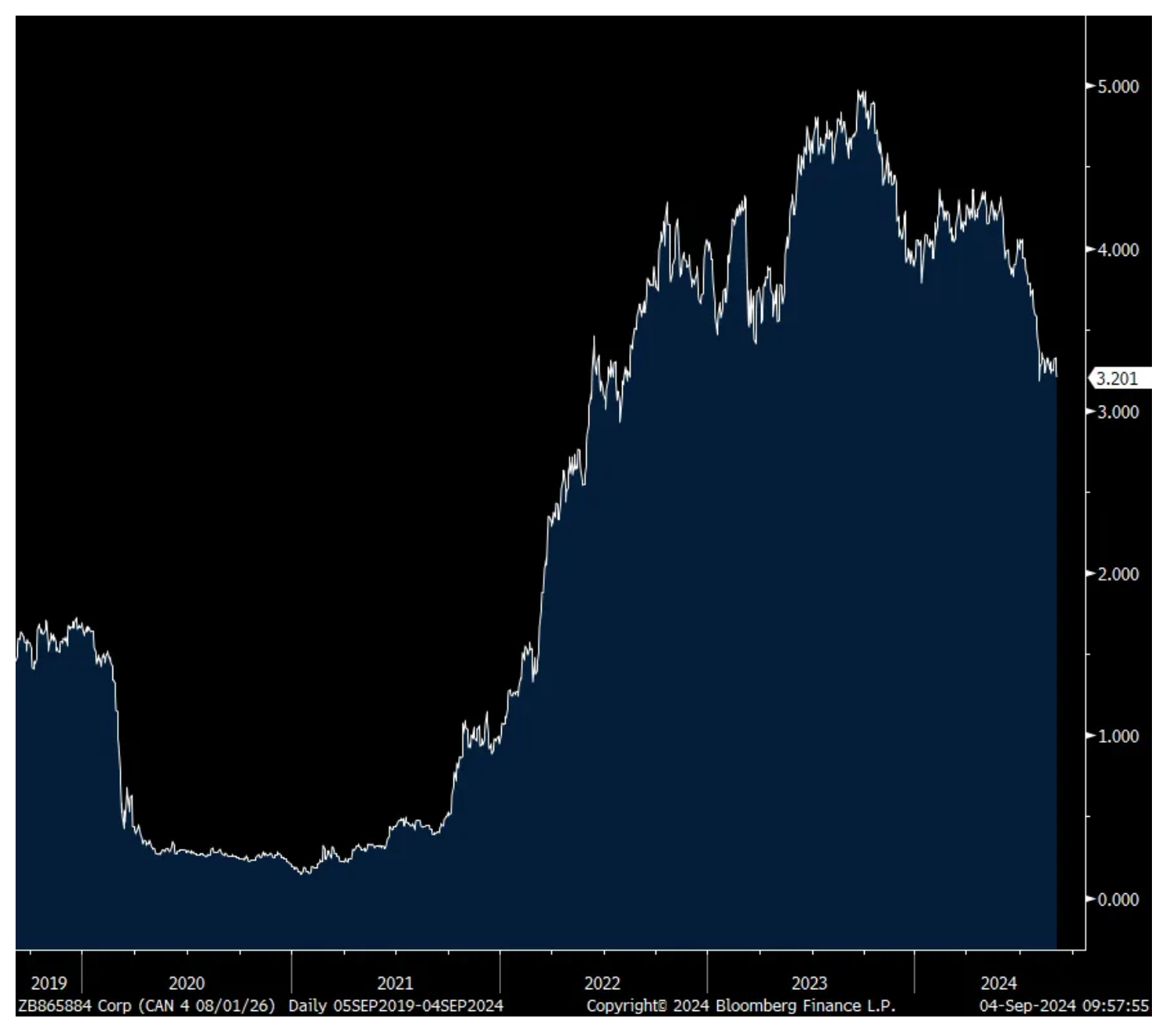

BoC cuts, as expected/Job openings shrink again

The Bank of Canada cut its main rate by 25 bps as expected to 4.25% and this now totals 75 bps of cuts off the peak of 5%. In contrast, they continue on with QT, aka, “balance sheet normalization.”

The reason given for the cut, “With continued easing in broad inflationary pressures, Governing Council decided to reduce the policy interest rate by a further 25 bps. Excess supply in the economy continues to put downward pressure on inflation, while price increases in shelter and some other services are holding inflation up.”

As for what comes next, Governor Macklem said “If inflation continues to ease broadly in line with our July forecast, it is reasonable to expect further cuts in our policy rate.” We’ll of course see what the reduction in interest rates will mean for shelter prices as Macklem also said “shelter price inflation is still too high.” The tricky job of this central bank.

On the prospect of more cuts to come, the 2 yr Canadian yield is lower by 4.5 bps in response but the Canadian dollar is up a touch as the US dollar is broadly weaker again today.

This cut will be followed most likely by the ECB a week from tomorrow and the Fed the week after as worries shift to economic growth from inflation. That said, won’t lower interest rates help lift interest rate sensitive things like housing and autos that could in turn reignite inflation? The tricky job of all central banks.

Canadian 2 yr yield

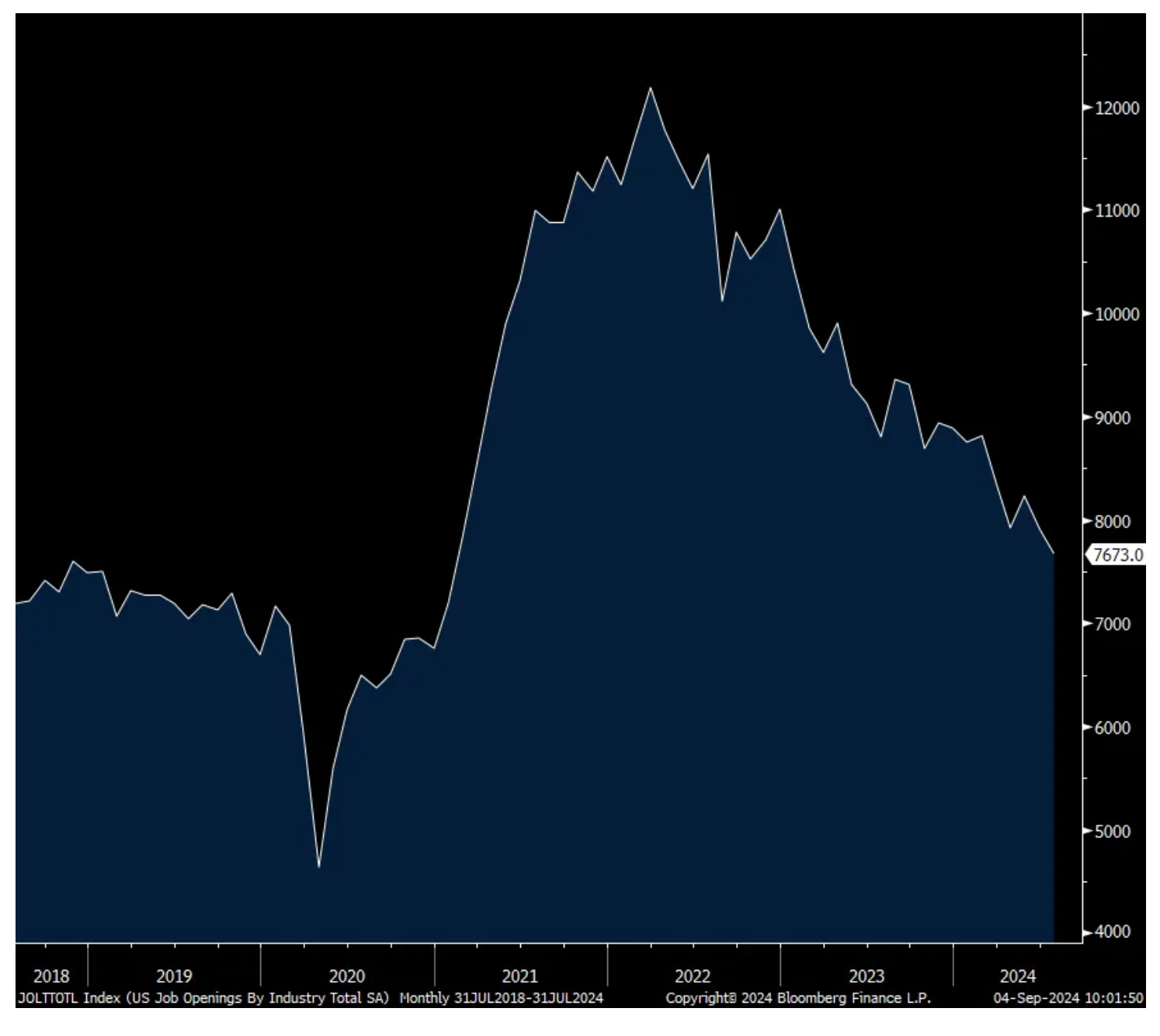

Job openings in July (thus somewhat dated) totaled 7.673mm, below the estimate of 8.1mm and down from a revised 7.91mm in June. That is the least since January 2021 and is approaching the level it stood at pre Covid (when it was likely more accurately calculated as job openings weren’t double/triple/quadruple counted and before WFH went viral, pun intended).

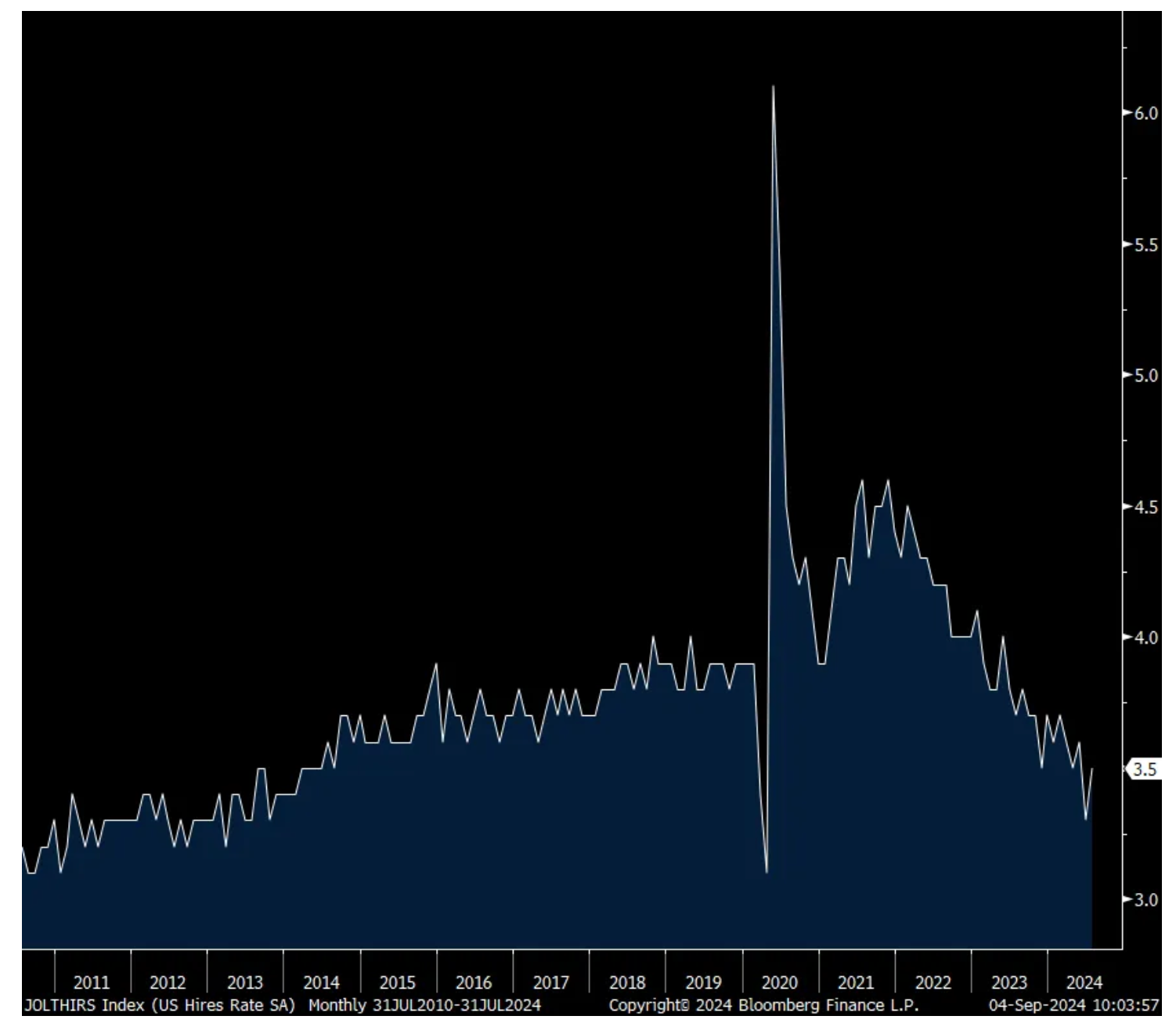

After falling to the lowest level since 2013, not including Covid, the hiring rate did tick up to 3.5% from 3.3% in June and vs 3.6% in May. The quit rate was 2.1%, up one tenth m/o/m. Offsetting the uptick in hiring was also a pick up in layoffs.

Separating out the private sector and government, the former saw job openings shrink to 6.75mm from 6.89mm in June. The demand for government jobs did fall too, by 92k m/o/m to 924k after a one year high was seen in May.

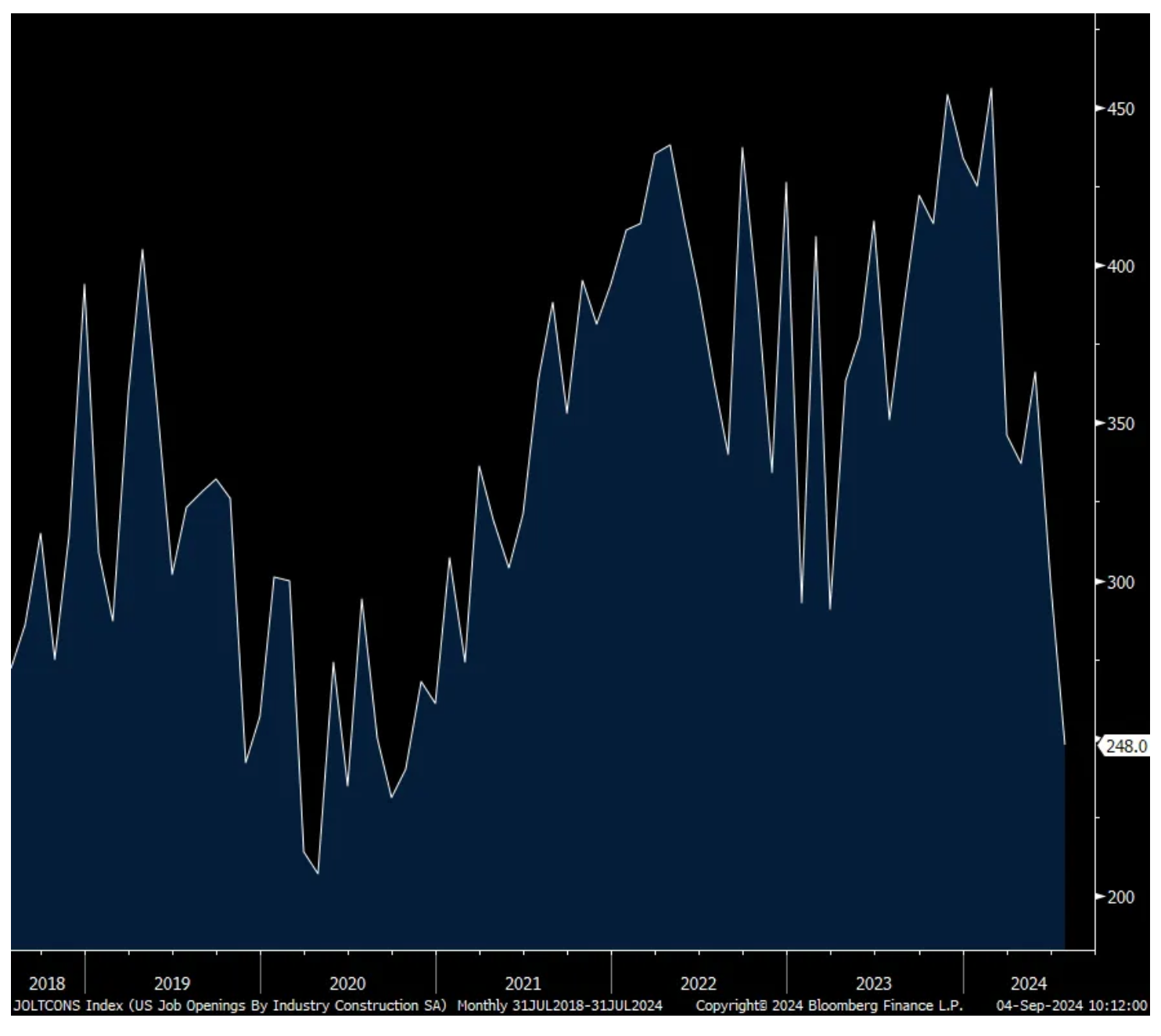

Of note industry wise, construction job openings have fallen to the lowest amount since October 2020 and continuing to catch up to the higher rate environment as when existing projects are getting done, less new ones are getting started. Just see what’s going on in multi family for a great example.

Also, with manufacturing still in a recession, that means less stuff gets transported around and transportation/warehousing/utility job openings fell to just shy of its least amount since September 2020.

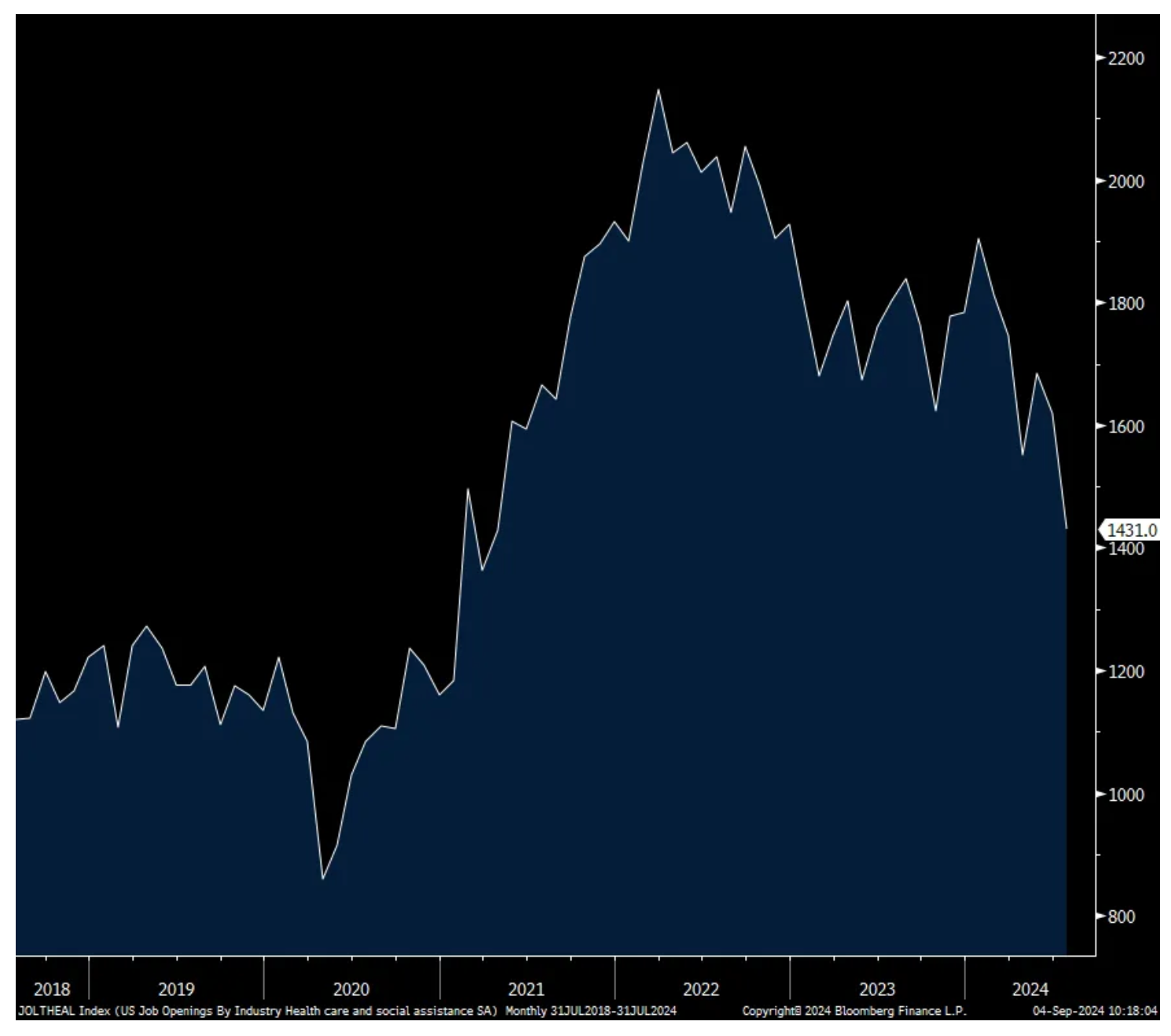

Finally, we know health care has been as steady as you can get when it comes to job creation. Job openings in this category fell to the lowest since April 2021.

Bottom line, the demand for new hires continues to fall.

Treasury yields are down about 3 bps both on the short end and long end with the 2s/10s at about the same level in response. We know the dividing line between a 25 bps rate cut or 50 bps instead will most likely be determined by where the unemployment will read out at on Friday for August.

The stock market wants to continue its celebration of hoped for Fed rate cuts but a switch has been turned where disappointing economic data means more. And on the flip side, any good idea now is celebrated.

Job Openings

Hiring Rate

Construction Job Openings

Healthcare Job Openings

BY Doug Kass · Sep 4, 2024, 12:10 PM EDT

On cue, Berkshire Hathaway BRK.B is down on the day (after being +$7 in the morning rip):

Berkshire's (BRK.B) shares have been on a tear — it's as if they havent had a down day since my Bar Mitzvah.

My Ludacris Forecast is that they fall today.

I added to a very small short at $482.39 this morning.

Position: Short BRK.B (VS)

By Doug Kass Sep 4, 2024 11:10 AM EDT

BY Doug Kass · Sep 4, 2024, 12:00 PM EDT

My largest incremental equity short put on today was in JPMorgan JPM (at $221.46).

BY Doug Kass · Sep 4, 2024, 11:50 AM EDT

At 11:00 a.m.:

BY Doug Kass · Sep 4, 2024, 11:25 AM EDT

Berkshire's BRK.B shares have been on a tear — it's as if they havent had a down day since my Bar Mitzvah.

My Ludacris Forecast is that they fall today.

I added to a very small short at $482.39 this morning.

BY Doug Kass · Sep 4, 2024, 11:10 AM EDT

* Back in the middle of The Great Financial Crisis (October 2008) Warren Buffett wrote a New York Times editorial entitled "Buy American, I Am"

* In that editorial Buffett explained why he was being greedy in buying stocks (on the cheap) while others were being fearful by aggressively selling stocks (at the lows)

* In marked contrast to 2008, Berkshire Hathaway is now in the process of selling a significant portion of his two largest holdings - Apple AAPL and Bank of America BAC

* Warren Buffett's 2024 sale of some of his outsized Apple holdings would not be surprising, as it had grown to a disproportionately large percentage of Berkshire's investment portfolio and total equity/assets - but his recent and accelerated sale of nearly half of this "forever" position in Apple during 2Q 2024 seems to be a more important statement and at the polar opposite of his market view when he was buying equities 16 years ago

* Moreover the continued sizeable and steady sale of shares in his long standing investment in Bank of America over the last quarter raises even more questions about The Oracle's view of the global economy and our capital markets

* Warren Buffett's multi-decade strategy of making operating and financial decisions that don't result in tax liabilities amplifies the possible significance of the sale of Berkshire's Apple and BofA investments

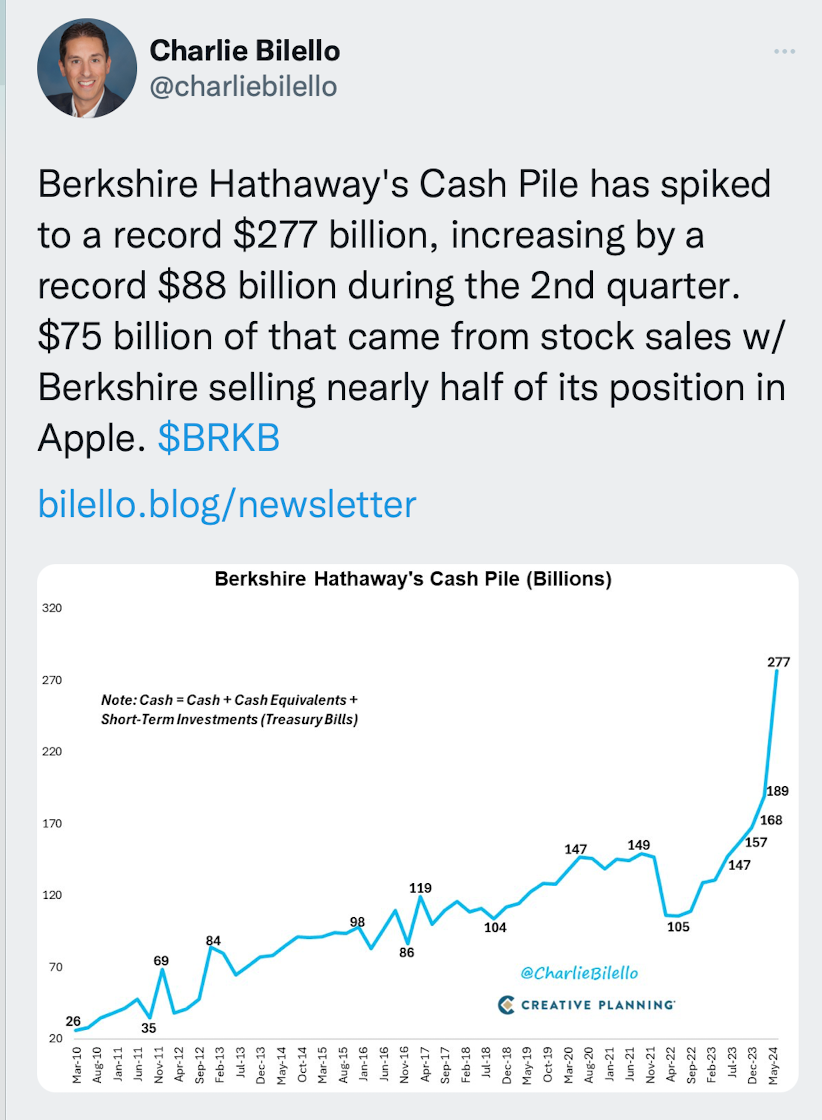

* Berkshire Hathaway has accumulated a record cash hoard that is close to $300 billion Berkshire Hathaway (BRK-B) - Cash on Hand

* Warren Buffett's favorite market indicator (Wilshire market cap to GDP) is flashing a strong sell signal

During the middle of The Great Financial Crisis Warren Buffett famously wrote an editorial in the New York Times in October, 2008 entitled , "Buy American, I Am":

It began:

THE financial world is a mess, both in the United States and abroad. Its problems, moreover, have been leaking into the general economy, and the leaks are now turning into a gusher. In the near term, unemployment will rise, business activity will falter and headlines will continue to be scary.

So ... I’ve been buying American stocks. This is my personal account I’m talking about, in which I previously owned nothing but United States government bonds. (This description leaves aside my Berkshire Hathaway holdings, which are all committed to philanthropy.) If prices keep looking attractive, my non-Berkshire net worth will soon be 100 percent in United States equities.

Why?

A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful. And most certainly, fear is now widespread, gripping even seasoned investors. To be sure, investors are right to be wary of highly leveraged entities or businesses in weak competitive positions. But fears regarding the long-term prosperity of the nation’s many sound companies make no sense. These businesses will indeed suffer earnings hiccups, as they always have. But most major companies will be setting new profit records 5, 10 and 20 years from now.

...

I encourage you to read the entire column.

Buffett's editorial and multiple purchases of stocks in 2008 were not perfectly timed -- since they occurred about six months before the S&P Index bottomed at 666 in the early days of March, 2009. But, in the fullness of time, those stock purchases and his upbeat market view near the low in the S&P 500 index proved to be profitable and materially on target over the next 15 years.

Today, nearly 16 years later, Warren Buffett is making more news -- but now he is selling.

Over the last several months Berkshire Hathaway has substantially trimmed his Apple holdings (by close to 50%): Warren Buffett's Berkshire Hathaway sold nearly half its stake in Apple (cnbc.com)

He is already incurring a meaningful tax liability on an estimated $50 billion of capital gains. Moreover, he is also (now) reducing his Bank of America long (thus far by about 15%) - incurring a tax liabillty on between $5 billion -$6 billion of capital gains.

Selling "forever" holdings like Apple and BofA are not Buffett-esque -- as we do know (from previous comments) that Warren Buffett hates paying taxes unnecessarily.

According to the company's 2021 Annual Report (the last time individual securities cost basis were presented) , Berkshire Hathaway's cost basis on his then holdings of 907 million shares of Apple was about $34/share compared to a current share price of $225/share . Berkshire's cost basis on his position of 1.03 billion shares of BofA was about $14/share compared to the current price of $41/share.

We can fully comprehend Warren's decision to pare back an extraordinarily successful investment in Apple that, thus far, has reaped in excess of $60 billion in profits. A partial sale could have been expected and would have been a conservative and understandable decision even though it would result in a large but manageable tax liability.

But the sale of nearly half of Berkshire's Hathaway Apple position likely represents something far more meaningful and harder to understand.

There are several possible explanations for the size of these sales:

* The sales might have been done in front of an expected Democratic election victory which would undoubtedly lead to an increase in the rate on taxes of realized capital gains (and maybe even on unrealized capital gains). This would be a reasonable explanation but the marginal impact of a higher tax rate really shouldn't dictate the sale as Warren has said in the past:

"It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price."

* There might be some sort of technical accounting offset/benefit to Berkshire's operations which could result in a rationale for harvesting and realizing gains (e.g. an offset to large catastrophic losses). Again, this reason is probably weak and a stretch, especially given the size of the realized gains in Apple already taken.

* The partial liquidation of Berkshire's Apple and Bank of America shares might be an attempt to prepare the company for Buffett's passing on the torch by creating an even larger and more formidable fortress of cash. This seems to be a possible explanation. Or (and most likely), the stock sales might simply relate to a much more ursine economic and market view than Warren is saying out loud. After all, as I have noted recently, Warren's favorite market indicator/barometer has been signalling sell for months.

The Buffett Indicator: Market Cap to GDP - Updated Chart | Longtermtrends

Perhaps ... Buffett is building cash because he wants to sit in his bathtub (see the genesis of his BAC investment during The Financial Crisis, and wait for the type of deals he was able to do in 2008- 2009) .... or he might end up owning all of Japan.

In other words it might be time to Sell American, He Is!

BY Doug Kass · Sep 4, 2024, 9:50 AM EDT

From Peter Boockvar:

Soft data, AI trade in question but some acrophobia too/Commodities/More PMIs/Dollar Tree uses word 'immense'

It was August 1st when weak economic news meant weak stocks and vice versa rather than the market spinning everything into what it would mean for Fed rate cuts. That was the day we saw a jump in initial jobless claims, was followed up the next day by a weak payroll report and was exaggerated that Monday by the yen carry trade reversal. As stated yesterday, that was again on full display but the economic data Tuesday wasn't that much different than expectations both in the US and China. Is it new news that manufacturing around the world is weak? Manufacturing has been in a global recession for about two years now. It seems that the economic worry coincided with stocks getting acrophobia again at the record highs and around 5600 is establishing itself as nose bleed territory in terms of valuations. Also, as mentioned here last week, it’s time for every big cap tech investor to start questioning the ability of these stocks to continue to carry the load, as the AI hype cools down as they all breathe the same economic air as everyone else.

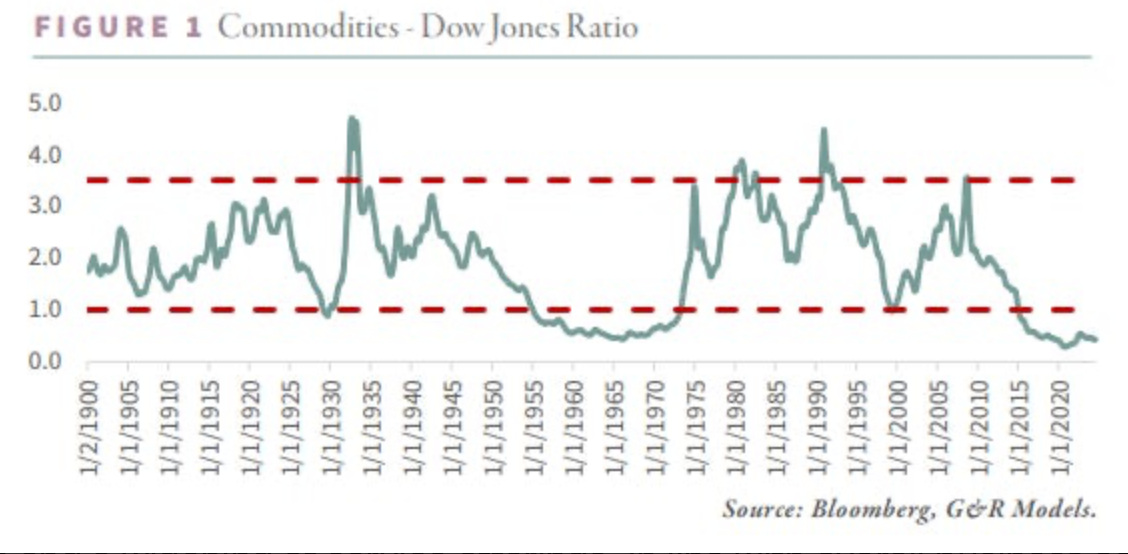

Commodity stocks got slammed yesterday, in case you missed it, and as a bull and owner of some of the stocks, it is always a gut check day. With permission from my friend Adam Rozencwajg, one half of the Goehring & Rozencwajg commodity investment team, I include the chart below from their most recent quarterly letter. It is a ratio chart of a propriety commodity index they created with the Dow Jones going back to 1900, reflecting when one is undervalued or overvalued relative to the other. As seen, commodities are the cheapest vs stocks going back about 125 years, similar to what was seen in the mid 1960's. I remain bullish and long, particularly in energy, uranium, precious metals and ag.

We did get more PMI's from overseas, including some focused on the service side. The August China Caixin services PMI remained above 50 but slipped .5 pts m/o/m to 51.6. The estimate was 51.8. Caixin said, "Service activity expansion was sustained by rising new business inflows in August according to the latest data. Chinese service providers often linked the expansion of new work to better underlying demand conditions and a widening of service offerings. In line with overall business activity, new work inflows expanded at a softer rate compared to July." More inbound tourism was a bright spot. Also of note, "Although still below the series average, the level of optimism rose for a 2nd successive month to the highest since May."

Chinese stocks were not immune from the global selloff. Hong Kong's PMI remained below 50 but was little changed at 49.4 vs 49.5 in July.

India's services PMI rose to a 5 month high at 60.9 vs 60.3 and remains a global economic bright spot. Singapore too as its PMI was up at 57.6 vs 57.2 in the month before. And a key reason why the SGD is at a 10 yr high vs the USD.

Vietnam's manufacturing PMI, one that we should all be watching as it gains global market share, was 52.4 vs 54.7 in July. S&P Global said that output and new orders led the way and "Although growth in each eased from the near records seen in July, rates of expansion remained strong nonetheless and prompted the most marked increase in purchasing activity in more than two years."

Australia's services PMI was revised to 52.5 which was up from 50.4 in July. Japan's held at 53.7.

The August Eurozone services PMI was revised down to 52.9 from the initial print of 53.3 but still up 1 pt m/o/m. This figure was particularly helped by France which of course benefited from the Olympics. On the flip side and reminded by it yesterday, European manufacturing remains in the doldrums.

The UK services PMI was revised up by .4 pts to 53.7 from 52.5 in July and that is a 4 month high. S&P Global said "Survey respondents typically linked rising business activity to the improving economic backdrop and an associated rise in willingness to spend. Some firms also suggested that the prospect of falling borrowing costs had helped to support business and consumer sentiment. There were nonetheless still a number of reports citing pressure on disposable incomes as a factor holding back customer demand."

Dollar Tree (actually $1.25 Tree) missed numbers and lowered guidance, following what Dollar General had to say last week:

In their earnings release this morning they mentioned the "immense pressures from a challenging macro environment."

Part of their earnings miss "reflected the increasing effect of macro pressures on the purchasing behavior of Dollar Tree's middle and higher income customers." Interesting that they didn't blame 'lower end.'

Dick's Sporting Goods beat numbers, including the comp estimates.

"Our Q2 comps were driven by growth in average ticket and transactions."

Purchase applications finally got a bit of a lift from the recent drop in mortgage rates as they rose 3.3% w/o/w. We of course want to see a lot more and hopefully will in the coming months. Refi's though were flat, but still up 94% y/o/y.

BY Doug Kass · Sep 4, 2024, 9:35 AM EDT

BY Doug Kass · Sep 4, 2024, 9:25 AM EDT

BY Doug Kass · Sep 4, 2024, 9:15 AM EDT

BY Doug Kass · Sep 4, 2024, 9:00 AM EDT

BY Doug Kass · Sep 4, 2024, 8:46 AM EDT

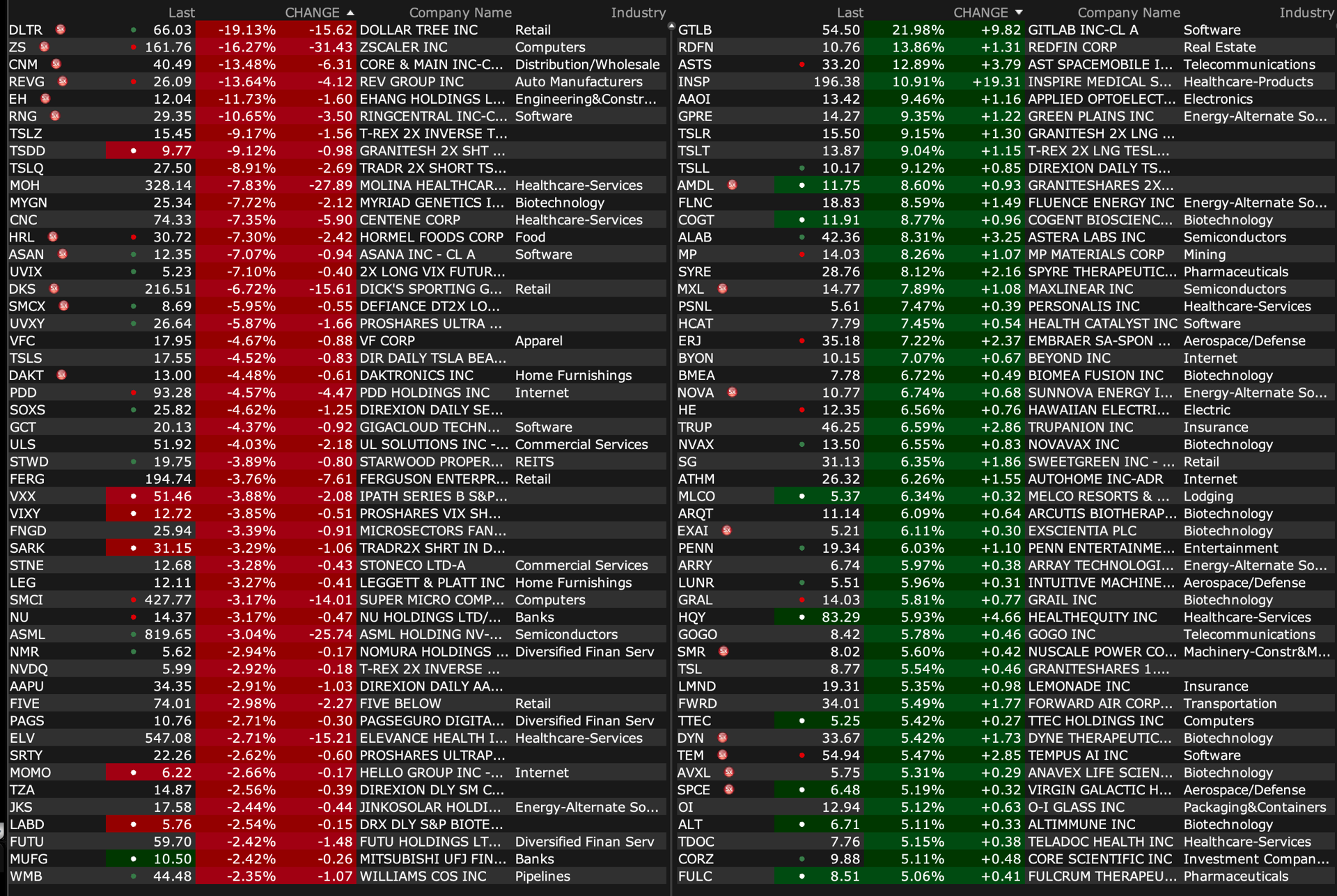

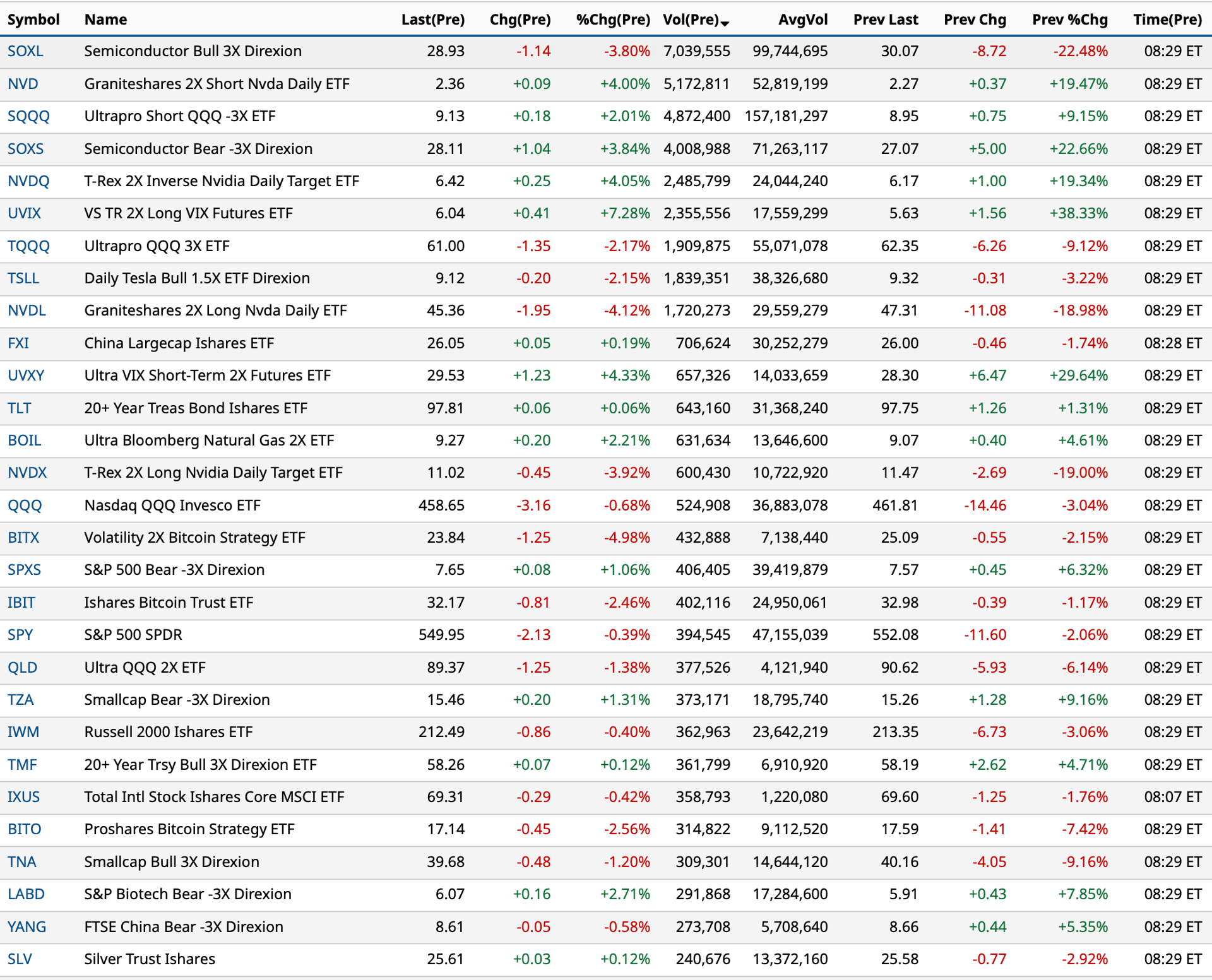

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Sep 4, 2024, 8:26 AM EDT

BY Doug Kass · Sep 4, 2024, 8:15 AM EDT

A thoughtful post from "The Other" Dougie:

Douglass Cassel

17 minutes ago

For those suffused with history, the article below is very concerning. For about 1500 years, Germany has been the key to European conflicts and economic development. Germany made the decision to go all in for automobile manufacturing, which now is being destroyed by Chinese imports. The inherent pact with the government, restraint on wages in return for overall prosperity is in danger of being overturned. The reliance on cheap Russian gas, giving technology to China in exchange for opening markets, and relaxed immigration rules have all turned out to be poor choices. The recent elections are just he beginning. A restless or angry German populace has historically been unfortunate for Germany and the world. Something else to think about.

"Germany’s economy has watched some of its largest companies vote with their feet and dollars since its manufacturing industry entered recession more than two years ago. Now, Volkswagen and Intel are poised to add more pain to the country’s coffers in what looks increasingly like a doom loop for the embattled country. Volkswagen, the jewel in Germany’s industrial crown, is turning sour on its native home, which it sees as compounding its struggle to expand its profit margins. For the first time in its 87-year history, Volkswagen is considering shutting down plants in Germany, where it employs around 300,000 people, as the company ramps up efforts to save €10 billion in costs. Intel, another embattled company, is considering its options in the country. Reuters reports that Intel will consider pausing or halting plans for its €30 billion ($33 billion) factory in the east German city of Magdeburg as the semiconductor manufacturer looks for cost savings. Germany had committed €9.9 billion ($10.9 billion) to the project when it was announced in June last year. (Sources: fortune.com, reuters.com)"

BY Doug Kass · Sep 4, 2024, 8:01 AM EDT

From JPMorgan:

US: Futs are lower but off their overnight lows with small-caps outperforming on the move lower; WTI back above $70 a level it breached overnight. Pre-mkt, NVDA -72bps with Mag7 and Semis weaker. Bond yields are lower by 1-3 bps and USD starts the day weaker, too. Cmdtys weakness continues but Energy losses curtailed and base metals the biggest laggards. With no consensus on the trigger for yesterday’s catalyst, this may be an aftershock from last month’s vol explosion. Today’s macro data focus is on JOLTS, Durable/Cap Goods, and Beige Book. Additional consumer data is provided via DKS, DLTR earnings.

and..

EQUITY AND MACRO NARRATIVE: Yesterday’s sharp sell-off lacked a consensus explanation and we did see some clients stepping in to buy the dip. Overall, would say that flows and client behavior lacked panic. This does feel like an aftershock from the early August turmoil. There was $5bn to buy MOC, so perhaps that is the first step in buying the dip.

* JOSH MEYERS (TMT Sector Spec): Lots of questions about the AI/Semis pullback/vol shock, and really still no consensus explanation. A few things coming up in conversations: 1) In the wake of some earnings disappointments (particularly memory – and with that WFE) and concerns post NVDA earnings, some investors were positioned for a pullback (some folks I spoke with are making money today); 2) JPY move has been unsettling, and there are other cross-currents in the market (move in crude, treasuries, HY…); 3) concerns over China macro weakness and Japan/China trade tensions around semis; 4) Citi conf starts today, and we get a ton of commentary/assurances, so by Friday this might (should? will?) all be in the rearview mirror; 5) just hoping we don't get pulled in the direction of non-human traders taking us even lower; and 6) my favorite from Marissa Gitler in Cross Asset Futures, maybe the market has decided to write off today and come back in ready to trade tomorrow. FWIW it was calm and quiet on the Equity trading desk yesterday.

* Post-market, NVDA received a DOJ subpoena according to Bloomberg headlines; the stock fell another ~1.6% post-market.

* PAIGE HANSON (Industrials Sector Spec): Early Feedback during Market Selloff – as with almost every market shift the last 6 months, the September volatility that many were expecting (due to cont’d uncertain macro into very pivotal Fed decision mid-month) over the course of the month is hitting fast & furious in the first few hours of trading post summer, and I wouldn’t say that folks are ignoring it/looking past it, but there seems to be a slightly higher degree of numbness to it and maybe a little less panic compared to similar huge 1-day moves that we saw the second half of the summer. To be clear, I think there is still max pain out there but the panic level in feedback is not quite the same degree, for whatever it’s worth.

POSITIONING INTELLIGENCE – Prime Time / Monthly Wrap | Equity Markets Near ATHs, but Confidence Not

SUMMARY: A month ago, there were multiple areas of performance, flows, and positioning that were looking fairly stretched. With the equity rebound in the last few weeks of August, a lot of those areas have normalized, but despite markets rebounding to around all-time-highs (ATHs), we have not seen a strong impulse across various areas of the market that suggest confidence in the broader market, Tech, or alpha prospects is back to prior highs. Some of this could be chalked up to investors taking time off last month, but it might also suggest a lack of conviction in market trends following a bout of heightened volatility, markets already up strongly YTD, US election / geopolitical concerns, and historically weak September seasonality.

BY Doug Kass · Sep 4, 2024, 8:00 AM EDT

* This likely implies that former President Trump will endorse the Florida Amendment for recreational cannabis use

* Trulieve is the greatest beneficiary

BY Doug Kass · Sep 4, 2024, 7:45 AM EDT

* Back to market structure issues

* The market is a giant auto-correlated mess, and it is getting worse and worse every year

* More algos, more passives and the retail crazies are the cherry on the top of the market's sundae

Back to the market structure issue.

First is a Bloomberg article, where Cliff Asness is called a whiner for believing the market has become less efficient:

Cliff Asness Says Markets Are Less Efficient — And Social Media May Be to Blame

If Bloomberg calls him a whiner, I hesitate to think what CNBC would call him.

Here is a synopsis of the abstract and his actual paper:

Abstract

Market efficiency is a central issue in asset pricing and investment management, but while the level of efficiency is often debated, changes in that level are relatively absent from the discussion. I argue that over the past 30+ years markets have become less informationally efficient in the relative pricing of common stocks, particularly over medium horizons. I offer three hypotheses for why this has occurred, arguing that technologies such as social media are likely the biggest culprit. Looking ahead, investors willing to take the other side of these inefficiencies should rationally be rewarded with higher expected returns, but also greater risks. I conclude with some ideas to make rational, diversifying strategies easier to stick with amid a less-efficient market.

The Less-Efficient Market Hypothesis

Asness believes those who take the other side of inefficiencies will be rewarded with excess returns.

No idea if he is right, but I think since whenever Greenspan started running the Fed, the opposite has been true. You have been better off being a follower, than a leader. Better off following a trend, and even being late, than you are fighting a trend. Most every short seller is out of business. If you are long only, and you haven’t chased everything, you are either out of business or your performance and asset growth has lagged.

The market is a giant auto-correlated mess, and it is getting worse and worse every year. More algos, more passives, and the retail crazies now.

Because everything is so correlated, when things go wrong, they go wrong quickly with devastating effect. But every time this happens, the central bankers step in, and the fiscal side seems to step in right along with them. So nobody is ever punished for the bad behavior, and the bad behavior only gets worse. The system rewards the heroin addicts with more heroin.

But just like the addict eventually dies from the excess drugs, society and the economy are no different. We are finally starting to see it.

Hopefully the poor behaviors are corrected before it is too late, but I am not optimistic. Instead of using crises to reform things, we seem to use crises to take more drugs.

BY Doug Kass · Sep 4, 2024, 7:30 AM EDT

The S&P Short Range Oscillator was way overbought into yesterday's market schemissing - providing a good warning signal.

But, the Oscillator slipped from 5.03% to 2.54% last night.

From last week:

Among all the measures of investor sentiment numbers and indicators (e.g. sentiment surveys, VIX) I prefer the S&P Short Range Oscillator.

As to the numbers... to catch up:

Thursday Night: 5.09%

Friday Night: 6.94%

Monday Night: 7.99%

We are getting more deeply overbought.

Position: Short SPY calls (S)

By Doug KassAug 27, 2024 6:20 AM EDT

BY Doug Kass · Sep 4, 2024, 7:15 AM EDT

BY Doug Kass · Sep 4, 2024, 7:00 AM EDT

BY Doug Kass · Sep 4, 2024, 6:50 AM EDT

Bonus — Here are some great links:

September Is Usually Troublesome

BY Doug Kass · Sep 4, 2024, 6:40 AM EDT

BY Doug Kass · Sep 4, 2024, 6:30 AM EDT

On Trump Media DJT shares:

BY Doug Kass · Sep 4, 2024, 6:20 AM EDT

Wolf Street on the drop in semi stocks.

BY Doug Kass · Sep 4, 2024, 6:07 AM EDT

BY Doug Kass · Sep 4, 2024, 5:57 AM EDT