Doug Kass: Is the Bull Run Based on a Bunch of Bull?

Investors tend to believe what they want to believe. But fairy tales don't come true... even when it happens to you.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Investors tend to be bullish and believe the superficial BS that comes down the pike.

It is the nature of the human spirit to be upbeat — especially when it comes to our investments.

Unfortunately we can prove anything by statistics except the truth.

But tearing down "the statistics" and accepted truths can sometimes be revealing and lead to being more objective and a better investor.

As proven by the past (especially in the lead up to The Great Financial Crisis) objective analysis can also keep us from being trapped in false narratives and reduce the likelihood of losing loads of money!

Fairytales can come true, it can happen to you

If you're young at heart

For it's hard, you will find, to be narrow of mind

If you're young at heart

You can go to extremes with impossible schemes

You can laugh when your dreams fall apart at the seams

And life gets more exciting with each passing day

And love is either in your heart, or on its way

- Johnny Richards and Carolyn Leigh, Young at Heart

Is the Bull Run Based on BS?

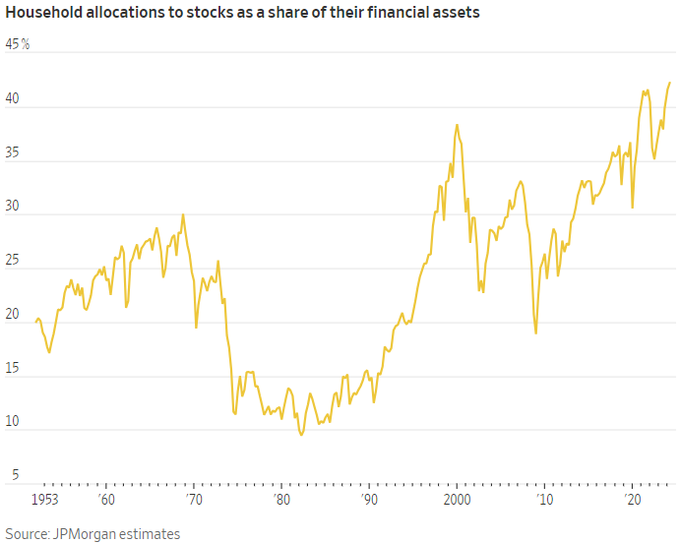

As I have noted recently, at 42%, households' allocations to equities is at the highest level in 72 years:

Household allocation to equities is at the highest level since 1952 — in part to the belief of a "Goldilocks" fairytale (an economy not too hot and not too cold).

To this observer, this allocation and the associated bullish investor sentiment may not be justified in the face of a number of headwinds including but not restricted to economic (slugflation likely lies ahead), policy (fiscal and monetary), political and geopolitical concerns, systemic stability and, the subject of today's missive — serious questions of what is the true level of S&P EPS that supports historically high (above 90%-tile) valuations.

But perhaps even more important is the lack of reliability of the economic data that forms our investment decision process.

From The Credit Strategist:

"Investors are unduly reliant on the Fed lowering interest rates and economic data whose reliability is increasingly subject to question. While they are rooting for the Fed to lower interest rates, it is unlikely that the Fed will do so aggressively. I have argued that the Fed shouldn’t do so at all until next year because it should maintain positive real (inflation-adjusted) rates at a respectable level and I don’t believe real rates are there yet. Despite government inflation statistics, real-world inflation is still pretty high (and remember, it is off a much higher base than before the pandemic). And recent events give little reason for us to trust the data supplied by the government. The recent elimination of 800,000 jobs from 2024 data by the Labor Department was an embarrassing error that shows the unreliability of government economic statistics. This was not a one-off correction. The government routinely retroactively adjusts economic statistics to a degree that shows they were highly inaccurate at the time they were released. This highlights the absurdity of the “countdowns” and other television hoopla that surrounds each Fed meeting and other economic news releases. We just have to hope that Rick Santelli doesn’t throw an embolism hyperventilating about the latest report of whether PCE comes in one-tenth-of-a-percent above or below the (totally blind) consensus. Investors treat this data like Buddhist monks interpreting koans when the information is no more meaningful than the crap printed on Page Six of The New York Post. No wonder the market behaves like a cross between a casino and a circus. The blind are leading the blind and they are all dressed up like Bozo."

Which brings us to the issue as to whether we are utilizing too-high S&P EPS numbers in justifying current valuations. (Make no mistake about it, even before my critical view of corporate profits — valuations are sky high based on historical comparisons!)

It is my conclusion that reported S&P EPS are no more accurate than government statistics. Indeed, I call BS to the level and manner in which S&P EPS are calculated in order to support bullish valuation arguments. And to government statistics that are not worth the paper they are written on.

When strategists and money managers justify their bullish market views based on unrealistic past and forward S&P EPS consider that those EPS numbers are routinely inflated by as much as 25% by non-GAAP adjustments. This serves to disguise cash flow and other key data points that are used in valuing equities.

Most investors disregard "adjustments" — certainly quants, machines and algorithms do! And, as I noted Wednesday, with so much capital flowing into passive products and strategies and with massive infusions of liquidity via central banks, there are few attempts to understand the increasingly complex, adjusted and fine-tuned.

Back to The Credit Strategist:

"The quality of reported earnings, and the quality of earnings reporting, is nothing less than appalling. This may make it challenging (and fun) for those of us trained to dissect balance sheets and financial filings, but it contributes to the false narrative that corporate earnings are robust. It also allows corporate managements to inflate their compensation by pumping up their stock prices with phony numbers. Non-GAAP adjustments contribute to the chronic overvaluation of stocks; they are no less a part of this systemic problem than profligate monetary and fiscal policy. When the book is written on the next financial crisis, bogus earnings will fill one of the chapters."

Bottom Line

Facts are stubborn but statistics are more pliable.

Investors are basing their optimism on the fairy tales of inflated S&P EPS numbers as well as phony government statistics (see the recent revision of 818,000 jobs in the labor market!)

Believing in fairy tales is as old as the hills — and as long as equity prices keep rising (and the system stays intact) few question consensus narratives (as weak and superficial as they may be).

The lack of penetrating or even realistic analysis led up to The Great Financial Crisis, which few recognized as it unfolded.

Many similar issues — in deciphering "real EPS" and in the area of regulation — existed in 2008 that exist today.

Back then the U.S. government solved the debt crisis by creating more debt, rendering the financial system increasingly more fragile and prone to instability.

Since then, the illusion of prosperity (see our burgeoning deficit and U.S. debt) and the too liberal interpretation (at best!) of reported and projected U.S. corporates (measured as EPS) have convinced most investors that equities are inexpensive and that another financial crisis is avoidable.

These optimistic conclusions, like fairy tales, could end badly for investors.

For these reasons and others, the current level of unquestioning market optimism is a classic contrarian sign.

More Trading Basics

- The Most Important Thing I've Learned in 25 Years of Trading

- Day Trading Is Very Difficult: Here Are 6 Tips for Long-Term Success

- Everything You Ever Wanted to Know About the CNN Fear & Greed Index

This commentary was originally posted Thursday, September 5, in Doug's Daily Diary on TheStreet Pro.