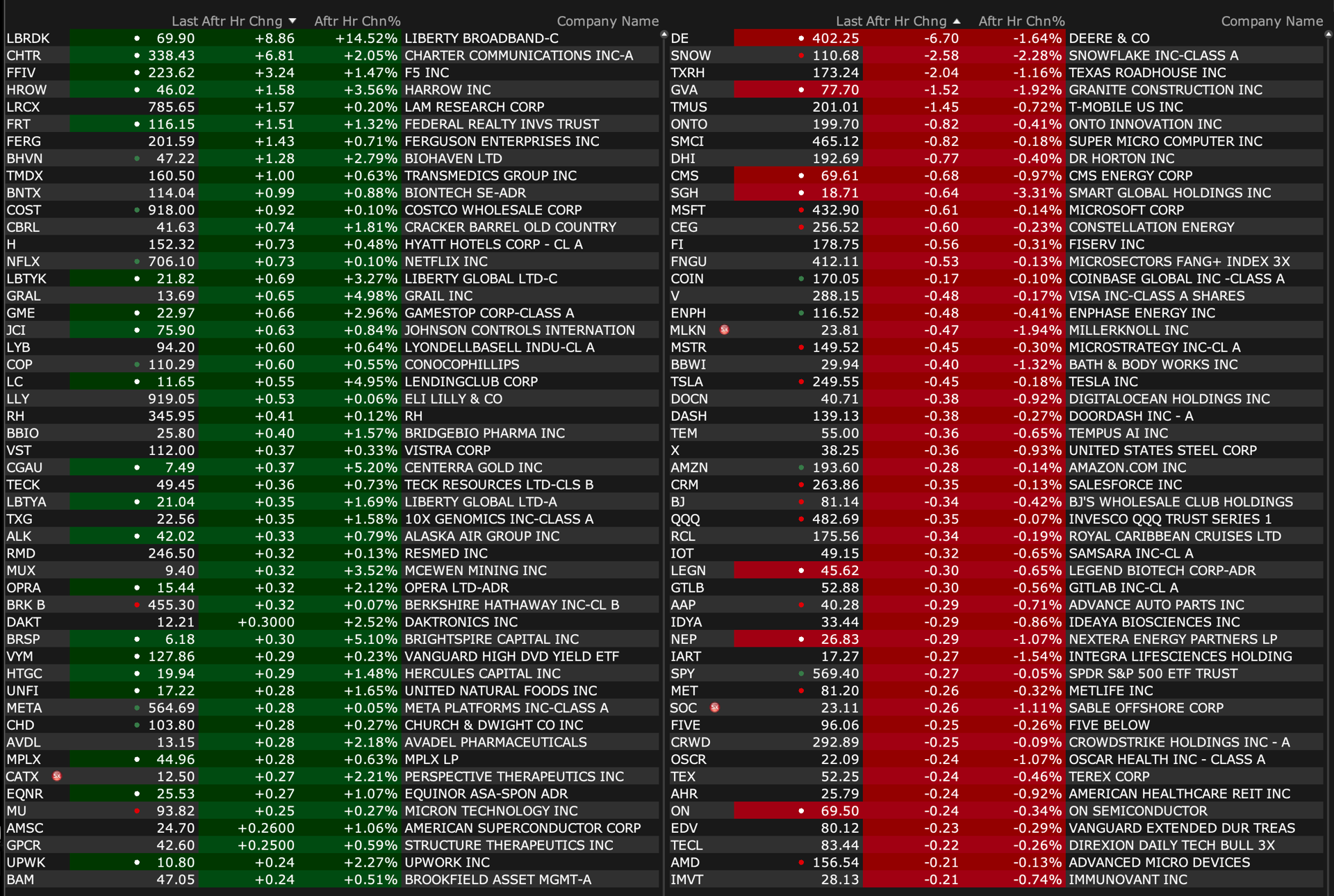

After-Hours Movers

As of 4:25 p.m.:

BY Doug Kass · Sep 23, 2024, 4:50 PM EDT

As of 4:25 p.m.:

BY Doug Kass · Sep 23, 2024, 4:50 PM EDT

BY Doug Kass · Sep 23, 2024, 4:20 PM EDT

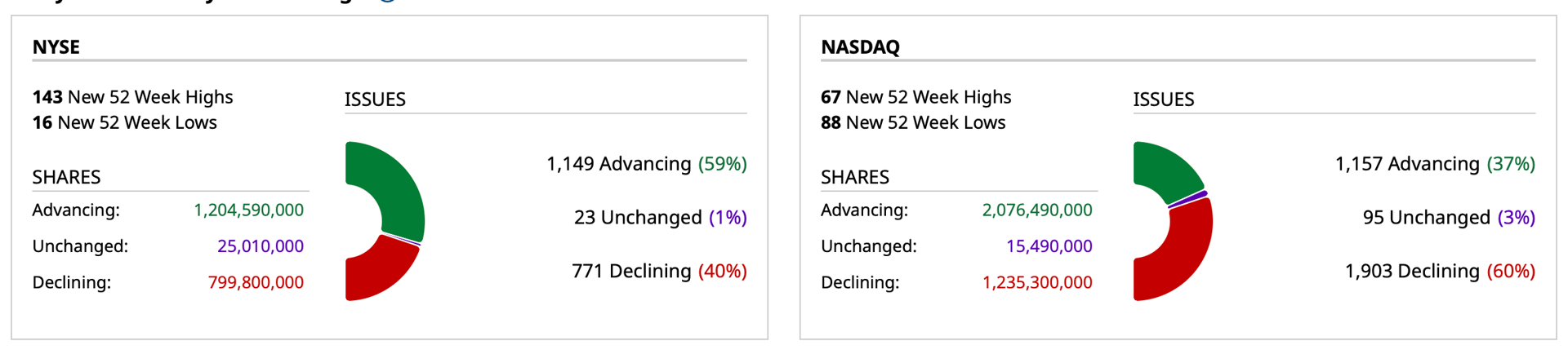

As of 3:20 p.m. the market has been range bound throughout the day.

I ended the day modestly net short in exposure.

The "things":

* In the premarket I increased SPY $569.10 and QQQ shorts $483.02. I further added to my Index shorts during the regular session (at around 11:30 a.m.) — SPY $569.57 and QQQ $483.31.

* I added to my ARES $157.83, BX $159.95, TOL $153.11, KKR $134.54 shorts this morning.

* New shorts GM $47.76 and GRBK $81.61 (I expect good earnings and a possible secondary offering).

* I once again added to my cannabis holdings this morning. TSNDF and MSOS.

* OXY (my largest individual equity long), strong in the morning, sold off midday and I added to my calls (out a month or two and slightly in the money).

* I covered my XLU short for a small loss.

BY Doug Kass · Sep 23, 2024, 3:55 PM EDT

The pairs trade long CMG/short SBUX is doing a nice job again today.

BY Doug Kass · Sep 23, 2024, 3:30 PM EDT

Long-held investment short Winnebago WGO is trading lower today.

According to a report by Hunterbrook Media there is a "potential cover-up" with Grand Design RVs, which "appear to be experiencing widespread frame failure, potentially affecting thousands of units sold for more than a billion dollars."

The report speculates that "the defect has led to costly damage and potential safety hazards, and rendered some RVs unroadworthy."

Hunterbrook's report also says "Winnebago has used NDAs, buybacks and online censorship to silence complaints about frame failure, potentially violating consumer protection laws."

BY Doug Kass · Sep 23, 2024, 3:25 PM EDT

I am preparing my 40th Tales From Nvidia!

So you know where I stand:

chrisk

Great opener Dougie Kass ...working and finally had a chance to read it. I wanted to flag that, even Jim Cramer, seemed to be much less bullish on AI after his weeklong trip to SF last week. He said the main beneficiaries so far with actually real world applications and MSFT, AMZN, META and GOOGLE...He was much more pessimistic than usual.

BY Doug Kass · Sep 23, 2024, 3:14 PM EDT

* I added to my ARES $157.83, BX $159.95, TOL $153.11, KKR $134.54 shorts this morning.

* New short GM $47.76

BY Doug Kass · Sep 23, 2024, 11:29 AM EDT

From Peter Boockvar:

Continued contrast b/w Services and Mfr'g/Buy duration here?

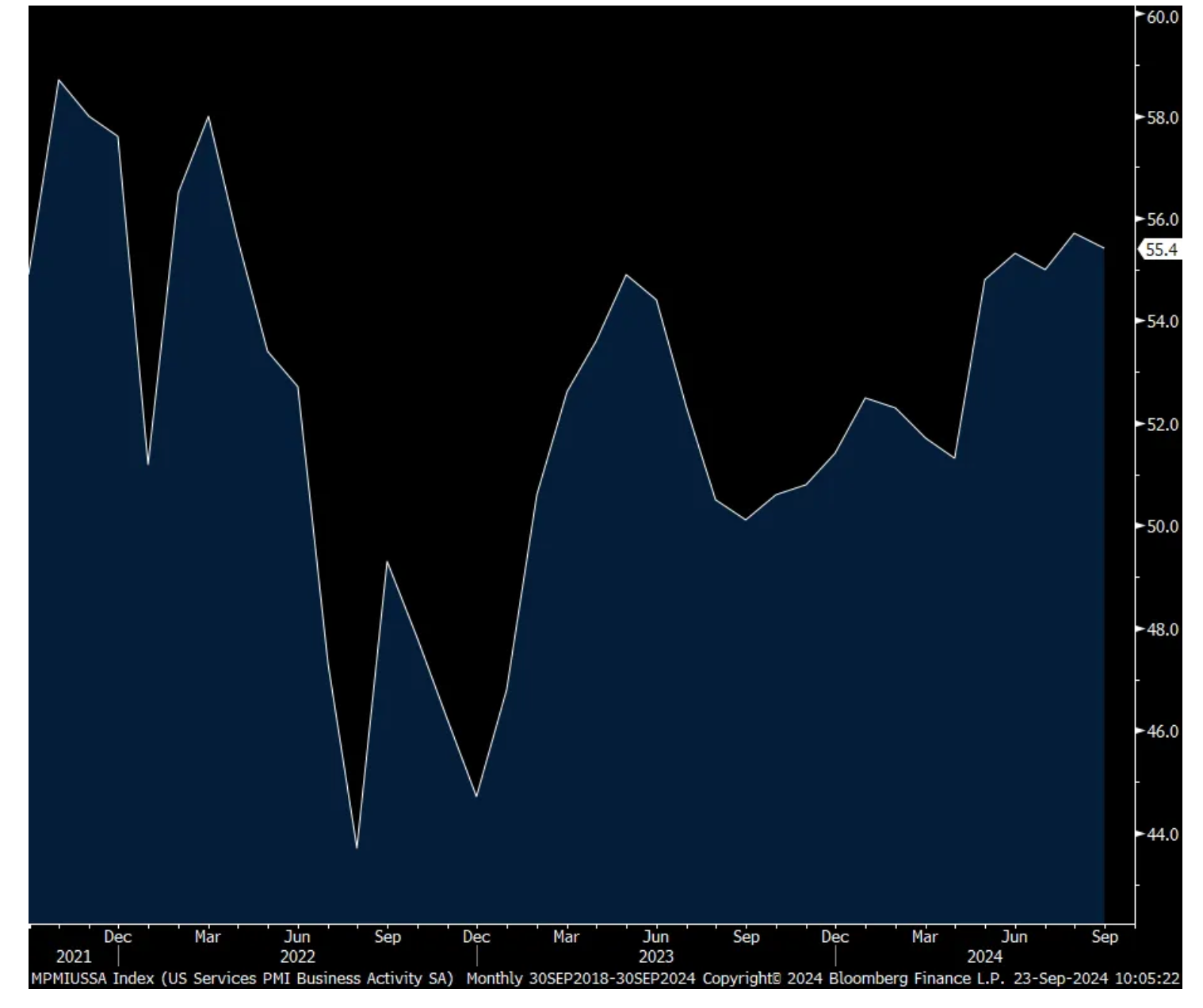

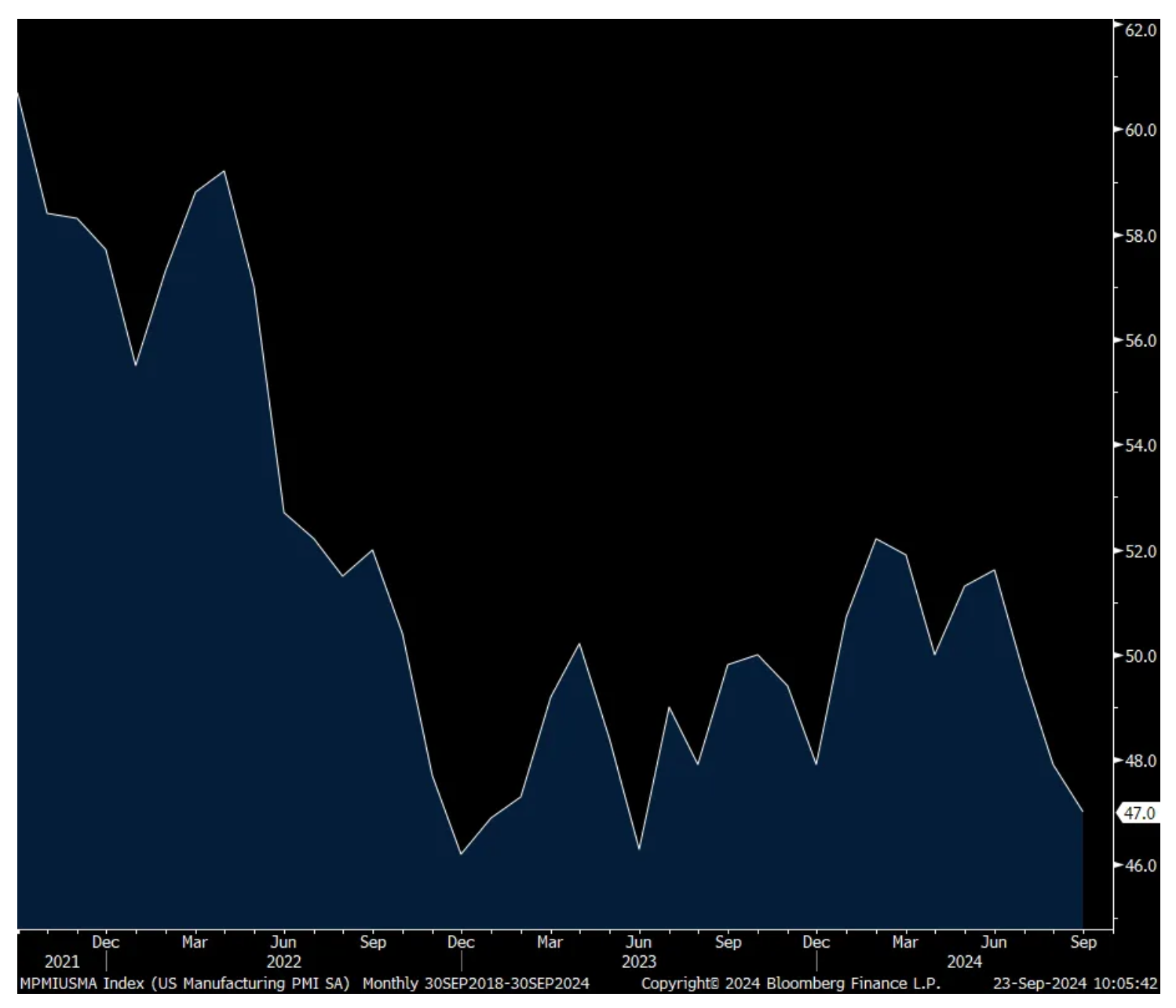

The September US PMI fell a touch to 54.4 from 54.6 with manufacturing remaining weak at 47 vs 47.9 in August, the slowest since June 2023 while services continue to carry the day at 55.4 vs 55.7 in the month before.

With manufacturing, “The largest negative contribution to the PMI came from new orders, which fell at the fastest rate since December 2022, followed by employment, which fell at a pace not seen since June 2020.” Ex Covid, the employment component was the weakest since January 2010 “as an increasing number of firms reported the need to reduce operating capacity in line with weak sales.”

While services held growth on its shoulders, S&P Global said the overall drop in headline optimism about output in the coming 12 months “was led by the service sector amid concerns over the outlook for the economy and demand, often linked to uncertainty regarding the Presidential Election.” With respect to the labor side, “The decline in service jobs was often linked to difficulties replacing leavers, though the addition of new staff was curbed by uncertainty about the outlook.”

Optimism with the one yr outlook lifted in manufacturing on hopes that it can’t get any worse and that lower interest rates will help.

On overall pricing, “average prices charged for goods and services rising at the fastest rate since March, representing the first acceleration of selling price inflation for four months. The upturn lifted the rate of inflation further above the pre-pandemic long run average. Rates of selling price inflation moved up to 6 month highs in both manufacturing and services, in both cases running above pre-pandemic long run averages to point to elevated rates of increase.”

More on this, “Higher charges were driven by increased costs, with input costs rising at fastest pace for a year in September. A one yr high rate of cost inflation in the service sector was often linked to the need to raise pay rates for staff. In contrast, manufacturing input cost growth cooled to a 6 month low thanks to lower energy prices and fewer supply chain price pressures.”

The bottom line from S&P Global is that the current level of the US PMI composite index is typically consistent with 2.2% GDP growth which was about the average seen in the 1st half of 2024.

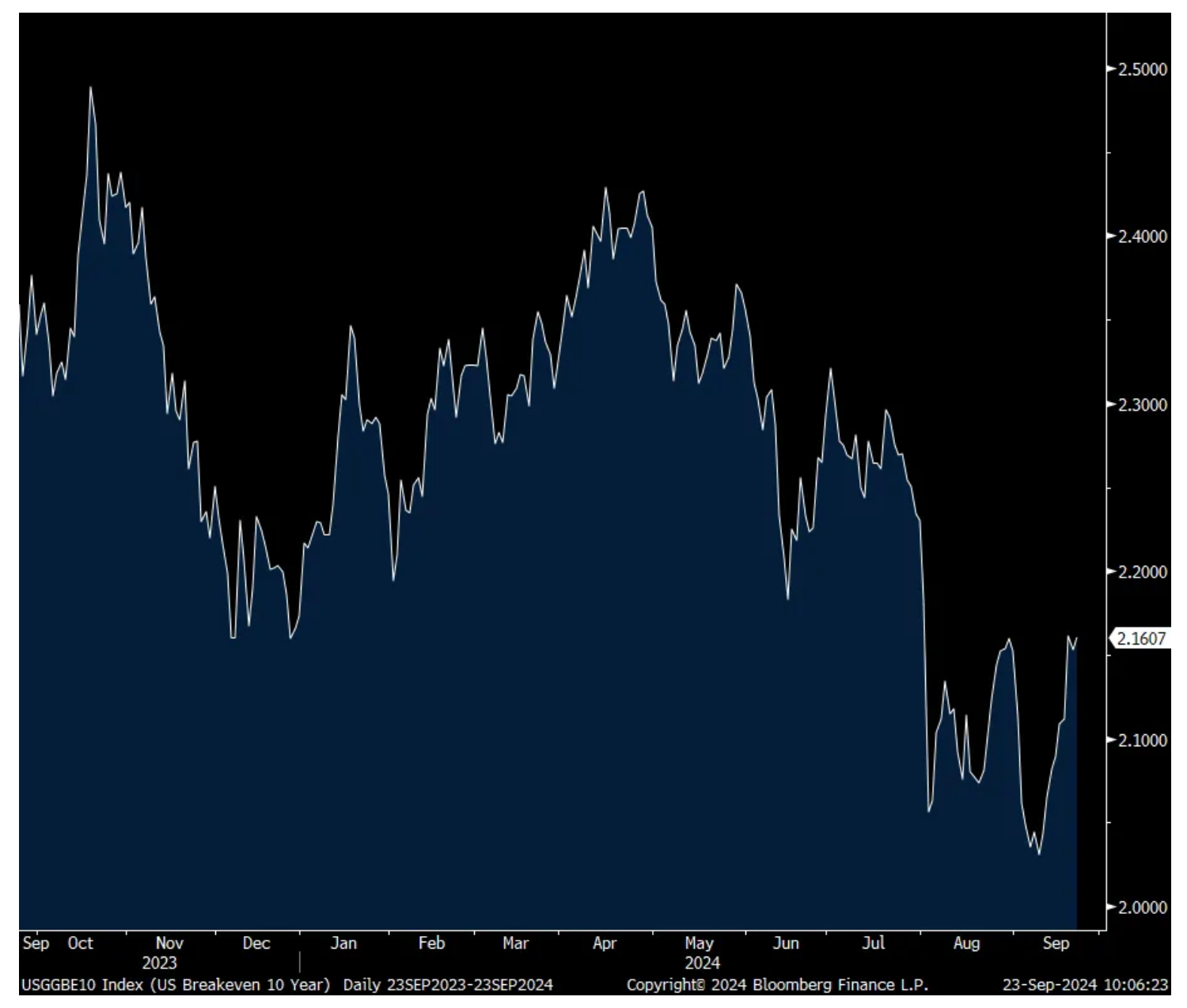

My bottom line, again the services side of the US economy is carrying all the water of economic growth and at least said here comes along with still inflationary pressures in contrast to manufacturing. I do want to point out again, the lift in the 10 yr yield post figure to 3.79% which is at a 3 week high, and something I thought was a high possibility when the Fed would start cutting short rates. Put yourself in the shoes of a market participant in the long end of the US yield curve, and maybe you are one. After the traumatic experience of 2022 with blood in the streets of bond land and a 40 yr high in inflation, do you want to see the Fed aggressively cutting short term interest rates? Is that enticing to buy duration? No.

US Services PMI

US Mfr’g PMI

10 yr Inflation Breakeven

10 yr Yield

BY Doug Kass · Sep 23, 2024, 11:08 AM EDT

* In the end, there is only one absolute truth about investing — Charlie Munger and Howard Marks are right, it is not easy.

* Those that think investing is easy overlook the market's nuances and complexities.

* So, I call BS to "first level thinkers" who see what is on the surface, react to it simplistically — buying or selling stocks on the basis of their reactions.

* I also call BS to the ongoing bullish and near universal narrative regarding the supposedly neat relationship of stock prices to the consensus 2025 S&P EPS forecast.

* And I continue to call BS to the poor quality of reported EPS.

The title of this morning's opening missive is taken from a wonderful quote from Charlie Munger. That quote captures today's market zeitgeist.

The investment mosaic is complex but many "talking heads" try to simplify their analysis. Indeed, today, "first level thinkers" dominate the investing landscape, but as always (as Carl Sandburg does below) should be questioned:

Two cases in point:

* The notion that equity prices neatly track S&P EPS closely.

* The quality of reported and forecast corporate profits (specifically that of the S&P Index) is suspect.

Let's start with the first misnomer — that stock prices track EPS.

This is a constant refrain I have heard in the business media (with only slightly different iterations) over the last two weeks. It is first level thinking personified (see Howard Marks' quote above), that comes off the tongue easily and is easy for the legions of investors to digest. That bullish refrain goes something like this:

"If consensus S&P EPS rise as expected next year (a projected gain of +14%), stocks have a long runway to rise higher."

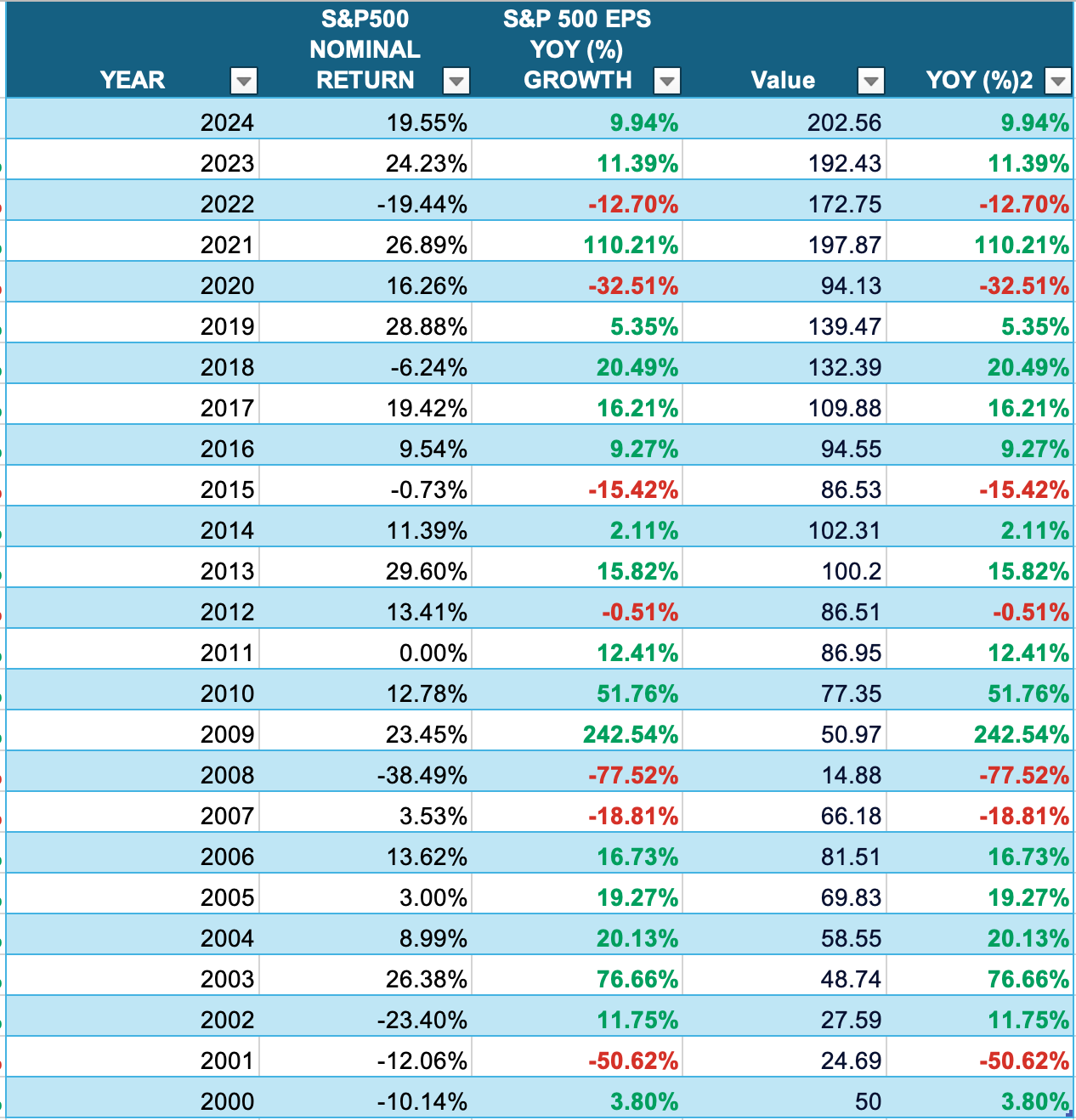

The following table is a 25-year compilation of annual change in the price of the S&P Index compared to the yearly change in S&P EPS EPS:

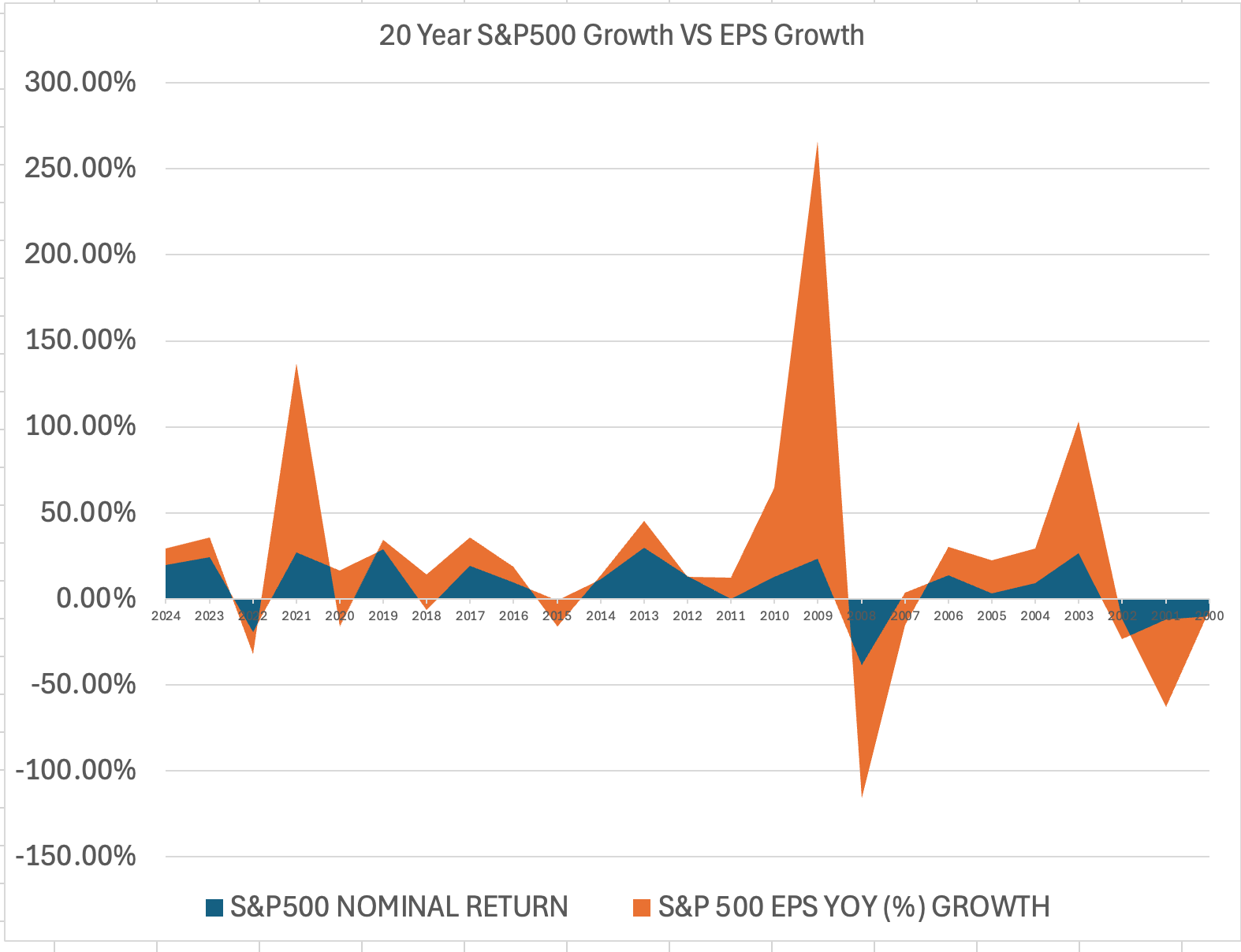

Here is a chart (prepared for us by Peter Boockvar), going back only five years measuring direction of the same two components:

These tables suggest that at times, stocks outperform the S&P Index. When this occurs, it is typically called a valuation reset in which price-earnings multiples outpace profits.

At other times stocks underperform S&P EPS. When this occurs, valuations contract.

Sometimes, as Warren Buffett reminds, our markets are a "drunken sailor."

In looking at the above charts, one can argue that the performance of equities over the last two years (and since 2019) are vulnerable as stock prices have outpaced the growth in reported EPS.

***

Let's now shift back to a column I wrote, "Is the Bull Run Based on a Bunch of Bull?" in early September that questioned the quality and level of reported S&P EPS:

Investors tend to believe what they want to believe. But fairy tales don't come true... even when it happens to you.

Investors tend to be bullish and believe the superficial BS that comes down the pike.

It is the nature of the human spirit to be upbeat — especially when it comes to our investments.

Unfortunately we can prove anything by statistics except the truth.

But tearing down "the statistics" and accepted truths can sometimes be revealing and lead to being more objective and a better investor.

As proven by the past (especially in the lead up to The Great Financial Crisis) objective analysis can also keep us from being trapped in false narratives and reduce the likelihood of losing loads of money!

Fairytales can come true, it can happen to you

If you're young at heart

For it's hard, you will find, to be narrow of mind

If you're young at heart

You can go to extremes with impossible schemes

You can laugh when your dreams fall apart at the seams

And life gets more exciting with each passing day

And love is either in your heart, or on its way

- Johnny Richards and Carolyn Leigh, Young at Heart

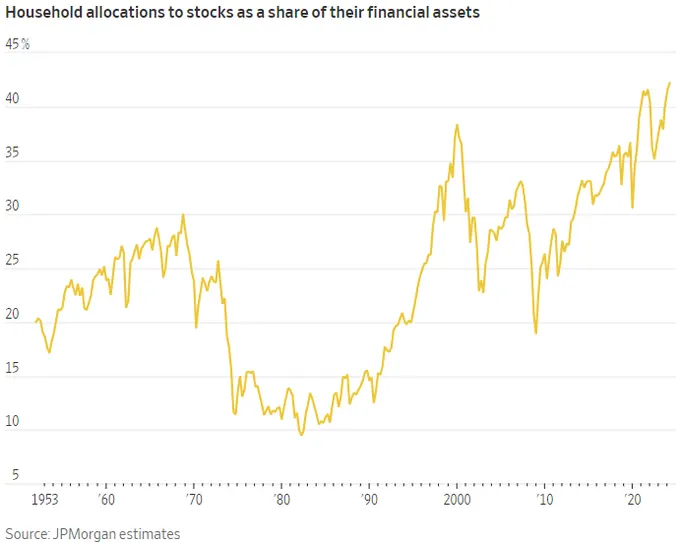

As I have noted recently, at 42%, households' allocations to equities is at the highest level in 72 years:

Household allocation to equities is at the highest level since 1952 — in part to the belief of a "Goldilocks" fairytale (an economy not too hot and not too cold).

To this observer, this allocation and the associated bullish investor sentiment may not be justified in the face of a number of headwinds including but not restricted to economic (slugflation likely lies ahead), policy (fiscal and monetary), political and geopolitical concerns, systemic stability and, the subject of today's missive — serious questions of what is the true level of S&P EPS that supports historically high (above 90%-tile) valuations.

But perhaps even more important is the lack of reliability of the economic data that forms our investment decision process.

From The Credit Strategist:

"Investors are unduly reliant on the Fed lowering interest rates and economic data whose reliability is increasingly subject to question. While they are rooting for the Fed to lower interest rates, it is unlikely that the Fed will do so aggressively. I have argued that the Fed shouldn’t do so at all until next year because it should maintain positive real (inflation-adjusted) rates at a respectable level and I don’t believe real rates are there yet. Despite government inflation statistics, real-world inflation is still pretty high (and remember, it is off a much higher base than before the pandemic). And recent events give little reason for us to trust the data supplied by the government. The recent elimination of 800,000 jobs from 2024 data by the Labor Department was an embarrassing error that shows the unreliability of government economic statistics. This was not a one-off correction. The government routinely retroactively adjusts economic statistics to a degree that shows they were highly inaccurate at the time they were released. This highlights the absurdity of the “countdowns” and other television hoopla that surrounds each Fed meeting and other economic news releases. We just have to hope that Rick Santelli doesn’t throw an embolism hyperventilating about the latest report of whether PCE comes in one-tenth-of-a-percent above or below the (totally blind) consensus. Investors treat this data like Buddhist monks interpreting koans when the information is no more meaningful than the crap printed on Page Six of The New York Post. No wonder the market behaves like a cross between a casino and a circus. The blind are leading the blind and they are all dressed up like Bozo."

Which brings us to the issue as to whether we are utilizing too-high S&P EPS numbers in justifying current valuations. (Make no mistake about it, even before my critical view of corporate profits — valuations are sky high based on historical comparisons!)

It is my conclusion that reported S&P EPS are no more accurate than government statistics. Indeed, I call BS to the level and manner in which S&P EPS are calculated in order to support bullish valuation arguments. And to government statistics that are not worth the paper they are written on.

When strategists and money managers justify their bullish market views based on unrealistic past and forward S&P EPS consider that those EPS numbers are routinely inflated by as much as 25% by non-GAAP adjustments. This serves to disguise cash flow and other key data points that are used in valuing equities.

Most investors disregard "adjustments" — certainly quants, machines and algorithms do! And, as I noted Wednesday, with so much capital flowing into passive products and strategies and with massive infusions of liquidity via central banks, there are few attempts to understand the increasingly complex, adjusted and fine-tuned.

Back to The Credit Strategist:

"The quality of reported earnings, and the quality of earnings reporting, is nothing less than appalling. This may make it challenging (and fun) for those of us trained to dissect balance sheets and financial filings, but it contributes to the false narrative that corporate earnings are robust. It also allows corporate managements to inflate their compensation by pumping up their stock prices with phony numbers. Non-GAAP adjustments contribute to the chronic overvaluation of stocks; they are no less a part of this systemic problem than profligate monetary and fiscal policy. When the book is written on the next financial crisis, bogus earnings will fill one of the chapters."

Facts are stubborn but statistics are more pliable.

Investors are basing their optimism on the fairy tales of inflated S&P EPS numbers as well as phony government statistics (see the recent revision of 818,000 jobs in the labor market!)

Believing in fairy tales is as old as the hills — and as long as equity prices keep rising (and the system stays intact) few question consensus narratives (as weak and superficial as they may be).

The lack of penetrating or even realistic analysis led up to The Great Financial Crisis, which few recognized as it unfolded.

Many similar issues — in deciphering "real EPS" and in the area of regulation — existed in 2008 that exist today.

Back then the U.S. government solved the debt crisis by creating more debt, rendering the financial system increasingly more fragile and prone to instability.

Since then, the illusion of prosperity (see our burgeoning deficit and U.S. debt) and the too liberal interpretation (at best!) of reported and projected U.S. corporates (measured as EPS) have convinced most investors that equities are inexpensive and that another financial crisis is avoidable.

These optimistic conclusions, like fairy tales, could end badly for investors.

For these reasons and others, the current level of unquestioning market optimism is a classic contrarian sign.

I prefer second level thinking over first level thinking.

Importantly, there are numerous and growing headwinds (social, political, geopolitical), off sided and undisciplined (monetary and fiscal) policy, the threat of a reacceleration of inflation, the vulnerability to profit margins (which have expanded steadily over the last five years), etc. that when combined with the recent revaluation higher in stock prices and the low quality of stated EPS suggest caution is now called for.

Not only don't stock prices neatly track reported EPS (which can also be debated in their quality) but it is likely that the aforementioned valuation reset (that has put equities in over the 90% tile in all classical measures of valuation) may have already more than discounted a gain in forecasted S&P EPS next year.

Those that think investing is easy overlook the market's nuances and complexities.

BY Doug Kass · Sep 23, 2024, 10:00 AM EDT

From Peter Boockvar:

Once purchasing power is lost, it is lost forever

Once purchasing power is lost, it is lost forever and Federal Reserve Governor Chris Waller inadvertently made that perfectly clear when he spoke on Friday. He told CNBC in an interview that "What's got me a little more concerned is inflation is running softer than I thought." He's 'concerned' after we just experienced a 21% jump in the cost of living since February 2020? Tell that to the shopper at Walmart or Dollar General. Remember 'average inflation targeting'? That was a policy that the Fed implemented in August 2020 and turned out to be one of the most disastrous policy initiatives in their history dating back to 1913.

It was defined as this, "On price stability, the FOMC adjusted its strategy for achieving its longer-run inflation goal of 2 percent by noting that it "seeks to achieve inflation that averages 2 percent over time." To this end, the revised statement states that "following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time." We know that policy initiative completely blew up on them.

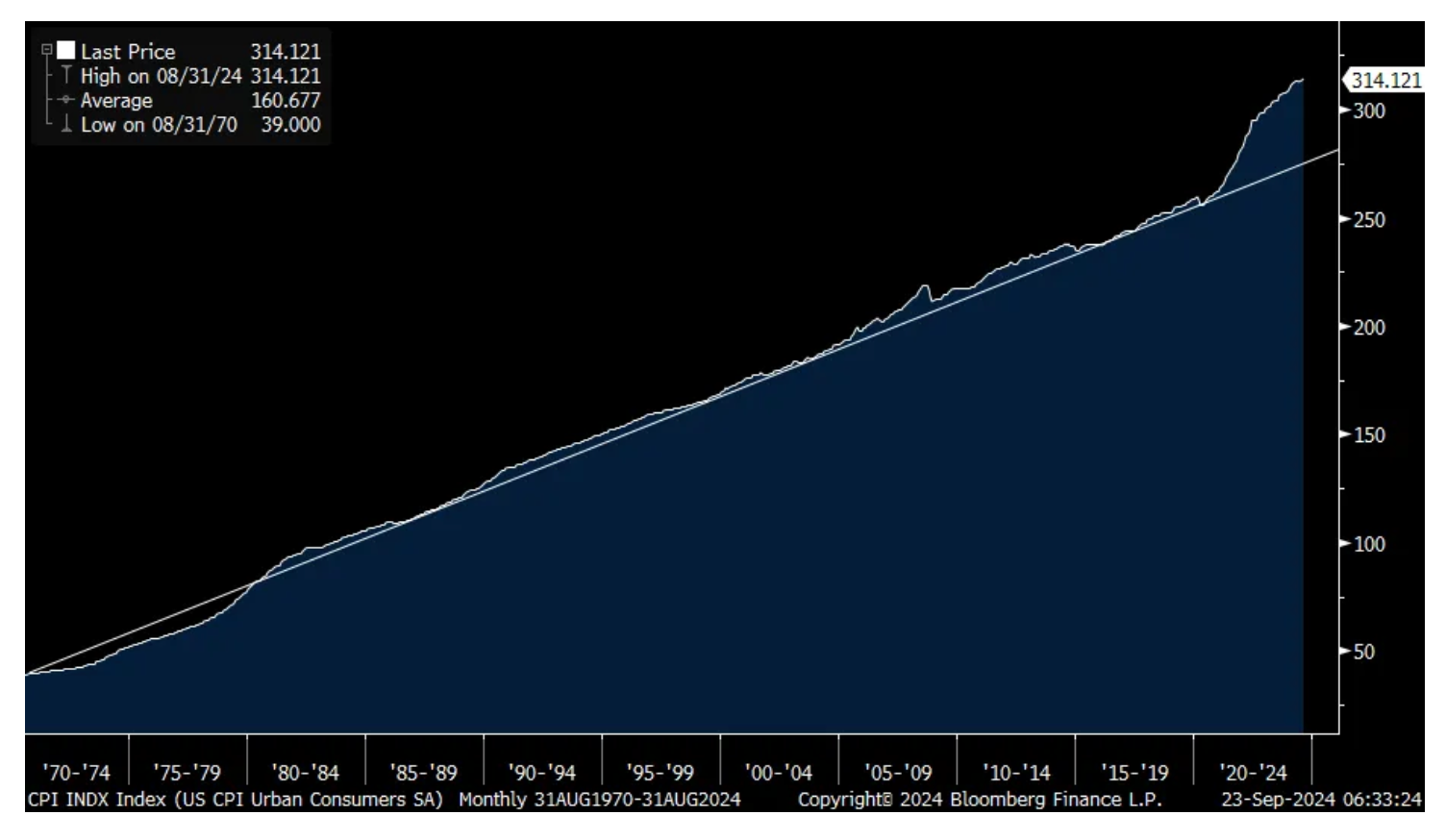

Governor Waller implicitly confirmed that this inflation symmetry policy is out the window as if they stuck to it, they would have to tolerate a period of time of deflation in order to 'average' out the recent period of high inflation at 2%. I'll include a chart here again of how much inflation rose above its long term trend line and say again, once purchasing power is lost, it is lost forever because central bankers won't let you get it back.

CPI index since the 1970's vs its trend line

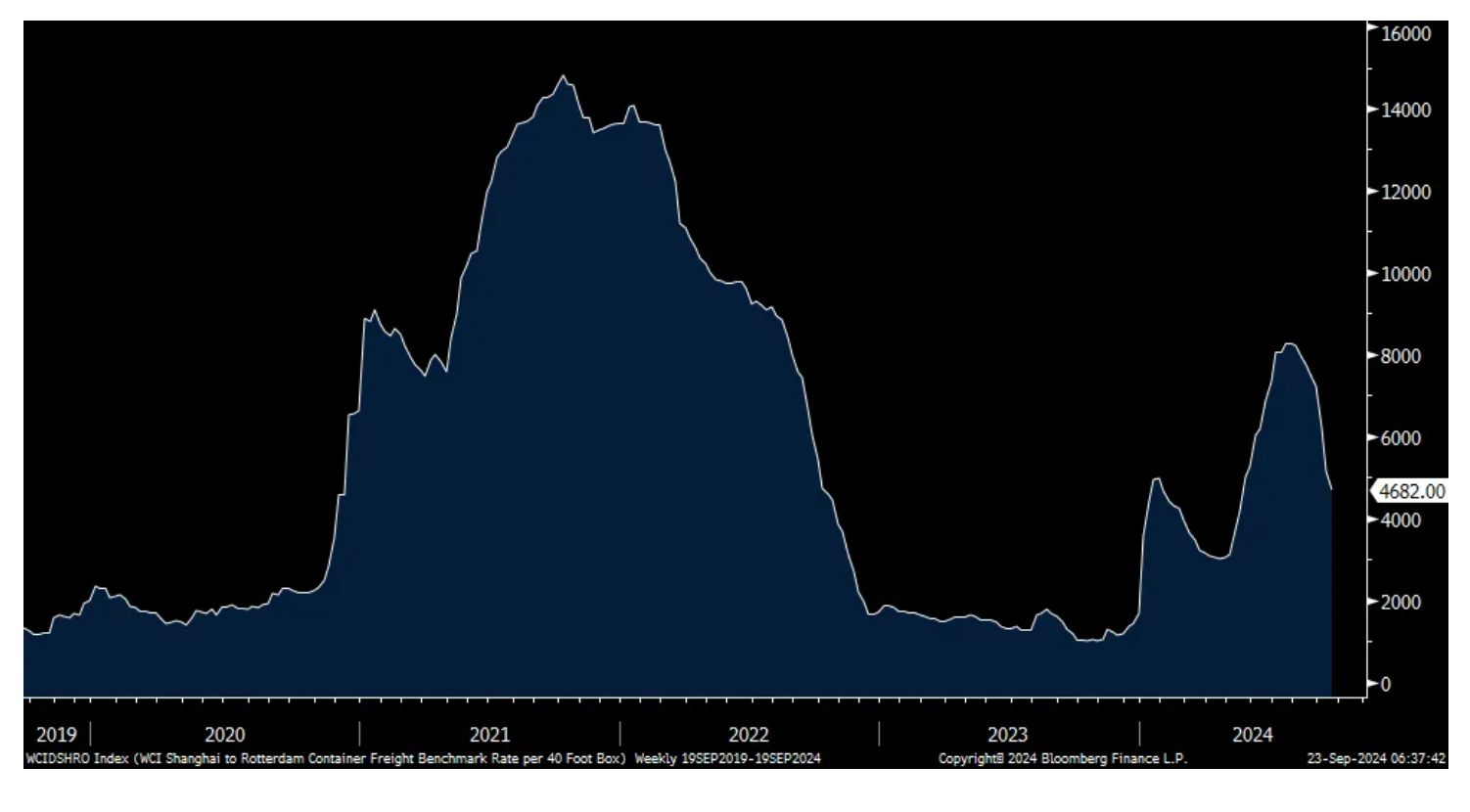

I forgot to mention on Friday the continued deceleration in container shipping prices. The WCI index for the trip to Rotterdam from Shanghai fell by $470 w/o/w to $4,682. Well off its July peak of $8,267 but still up from about $1,700 at the beginning of the year. The route from Shanghai to LA fell by $47 to $5,580. The top this year was $7,512 and ended 2023 at $2,100.

As the scramble to procure goods ahead of the holidays is full on, and worries over the cost and diversions of shipping stuff, air cargo rates continue to be robust. On Friday the World ACD Market data report said "Soaring air cargo spot rates from Bangladesh and Japan and a surge in tonnage from Dubai have further boosted an already buoyant air cargo market in the first half of September."

With respect to rates, "Average worldwide rates edged up slightly further to US $2.58 per kilo, based on a full market average of spot rates and contract rates, with a 1% further increase from Asia Pacific origins partially canceled out by a -2% drop from Middle East & South Asia origins. Nevertheless, average worldwide rates from those two regions are up, y/o/y by 24% and 53% respectively, helping drive average worldwide prices +14% higher, y/o/y and +50% above pre-Covid levels."

Shanghai to Rotterdam

From Lennar's Friday conference call:

"While demand has been and should remain strong, the supply of homes remains constrained. The well documented chronic housing shortage is a result of years of underproduction. This shortage has been exacerbated by continuing shortfalls in production driven by restrictive land permitting and higher impact fees at local levels and higher construction costs across the housing landscape."

And, "Mayors and Governors across the country have become acutely aware of the housing shortage and shortfall in their respective geographies...Awareness has begun to give way to the first signs of action, and more recently, even the national narrative has begun to acknowledge the need for programs that activate supply."

"Of course, affordability has been a limiting factor for demand and access to home ownership to date. Inflation and interest rates have hindered the ability of average families to accumulate a down payment or to qualify for a mortgage. Higher interest rates have also locked households in lower interest rate mortgages and curtailed the natural move-up as families expand and need more space. Rate buy-downs and incentives have enable demand to access the market to date."

They also touched on the impact of the sharp rise in immigration. "On one hand, the influx of the immigrant population has expanded the labor pool and therefore offset the pressure on construction cost increases. On the other hand, the increase in population requires more supply of dwellings to house that growing population."

Ahead of the US PMI data at 9:45am est, Australia's manufacturing and services composite index for September fell back below 50 at 49.8 from 51.7 with both components lower, particularly in manufacturing. India's composite index remained strong but did recede a bit to 59.3 from 60.7 with manufacturing at 56.7 and services at 58.9.

In the Eurozone, its PMI fell back under 50 too at 48.9 with manufacturing slipping all the way down to 44.8 and services at 50.5 from 52.9. The composite index estimate was 50.5. S&P Global said, "The eurozone is heading towards stagnation...Manufacturing is getting messier by the month. The recession has now dragged on for 27 months and even worsened in September. Looking ahead, the sharp drop in new orders and companies' increasingly bleak outlook for future output suggest that this dry spell is far from over."

Also, "Although services business activity continued to rise, the latest expansion was only marginal and the weakest since February." Yields are lower while stocks are mixed in the region. The euro is down a touch after the recent run higher. The Eurozone might get some help from lower short term rates but we know they also have their own self-inflicted form of economic paralysis.

The UK economy is hanging in better with its composite index at 52.9 from 53.8 in August. Both components held above 50 too. That said, the industrial side is not doing as well as services as seen in the September CBI industrial orders index today which fell to -35 from -22. The estimate was -23.

BY Doug Kass · Sep 23, 2024, 9:35 AM EDT

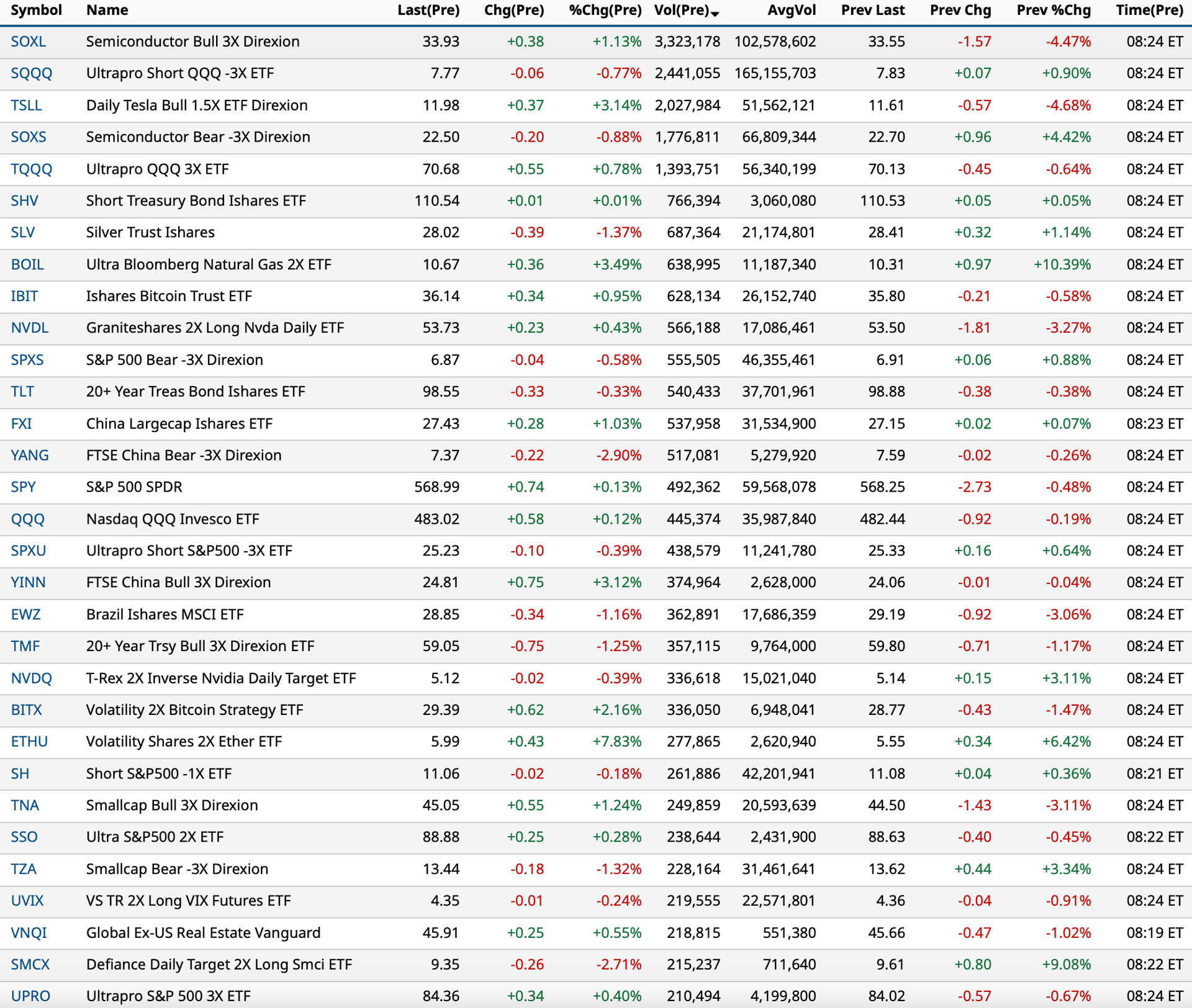

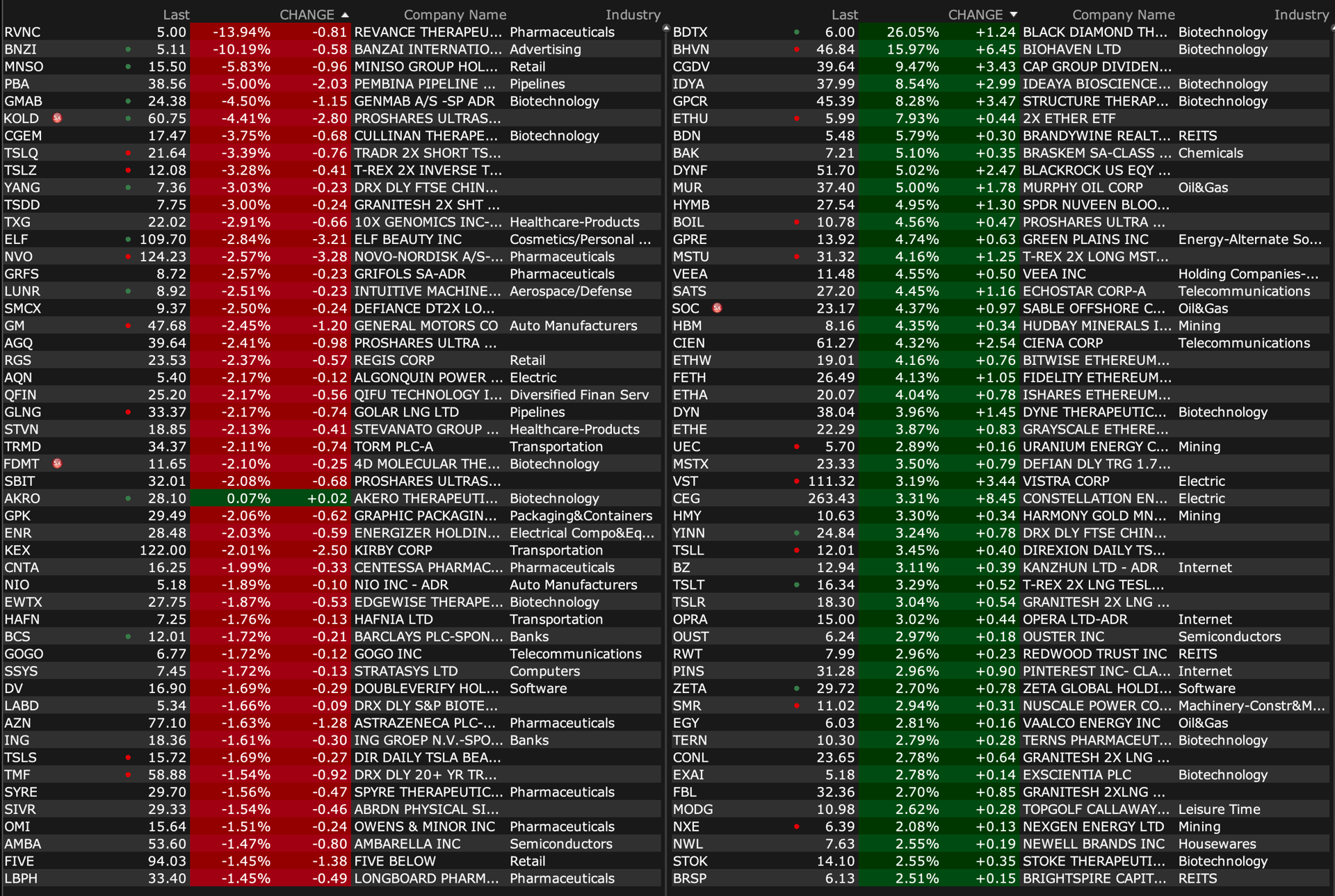

As of 8:24 a.m.:

BY Doug Kass · Sep 23, 2024, 9:12 AM EDT

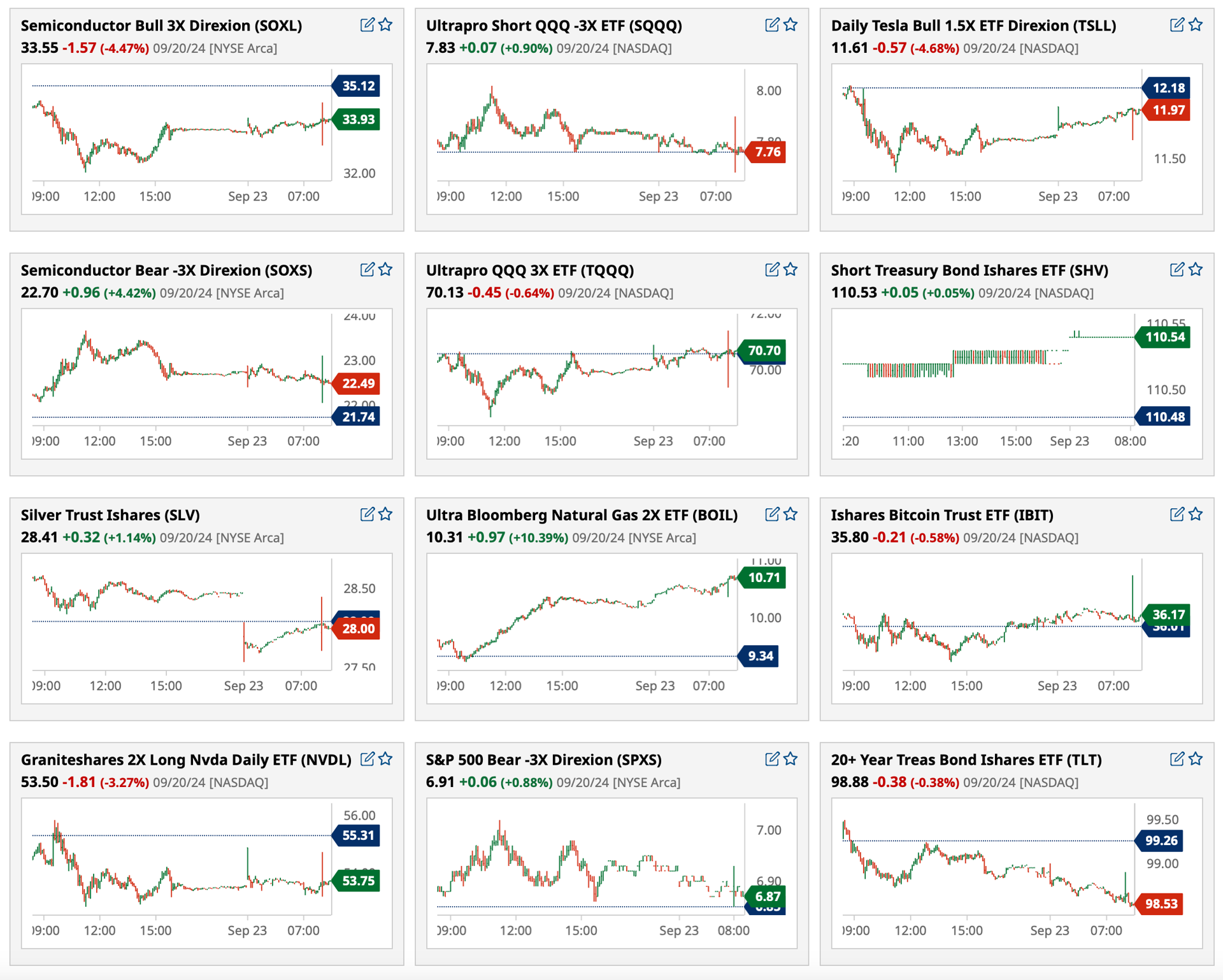

As of 8:43 a.m.:

BY Doug Kass · Sep 23, 2024, 9:05 AM EDT

Upside:

-BDTX +37% (announces Initial Phase 2 Data with Favorable Tolerability Demonstrating Robust Anti-tumor Activity of BDTX-1535 in Patients with Recurrent EGFRm NSCLC who Present with a Broad Spectrum of Classical, Non-classical, and C797S Resistance Mutations)

-BHVN +17% (Troriluzole 200mg dosed orally once daily, met the primary endpoint in patients with SCA, showing significant improvements in f-SARA scores after 3 years)

-LTRN +7.3% (announces Three US FDA Rare Pediatric Disease Designations Granted to LP-184 in Multiple Ultra Rare Children’s Cancers)

-IDYA +7.1% (reports positive interim phase 2 data for Darovasertib and successful FDA Type C meeting on registrational trial design for regulatory approval in Neoadjuvant Uveal Melanoma)

-NNE +4.5% (launches new subsidiary, NANO Nuclear Space Inc. (NNS), to explore the potential commercial applications of the Company’s developing micronuclear reactor technology in space)

-UEC +2.9% (acquires Rio Tinto's Sweetwater Plant and Wyoming Uranium assets for $175M)

-MBRX +2.7% (announces Positive In Vivo Efficacy Data of Annamycin in Orthotopic and Experimental Lung Metastatic Models of Sarcoma)

-ELEV +2.6% (receives Fast Track Designation from FDA for EO-3021 for treatment of adult patients with advanced or metastatic gastric or gastroesophageal junction cancer expressing Claudin 18.2)

-EBF +2.3% (earnings)

Downside:

-TOVX -3.4% (weakness following reaching targets patient enrollment in VIRAGE Phase 2b Trial of VCN-01 with Gemcitabine/nab-Paclitaxel for Treatment of Metastatic Pancreatic Cancer)

-GM -2.7% (to lay off ~1.7K workers at Fairfax Assembly plant in Kansas)

BY Doug Kass · Sep 23, 2024, 8:59 AM EDT

From my friend Keith McCullough at Hedgeye:

BY Doug Kass · Sep 23, 2024, 7:55 AM EDT

BY Doug Kass · Sep 23, 2024, 6:05 AM EDT

BY Doug Kass · Sep 23, 2024, 5:45 AM EDT