1) The U.S. economy needed some edge off high short-term interest rates. Whether the Fed was going to cut 25 BPS or 50 BPS though, a lot of rate cuts over the coming year have already been priced in, so it really didn’t matter. How it progresses from here does much more.

2) Initial jobless claims fell to 219,000 from 231,000 and that was 11,000 less than expected. The four-week average fell to 228,000 from 231,000. Continuing claims dropped too by 14,000 to 1.829 and that is the lowest since June.

3) Core retail sales in August were about as expected when including a very slight upward revision to July. They rose .3% month over month after a .4% rise in the month before. They were up by 3.9% year over year in nominal terms.

4) The September NY manufacturing index, the first September industrial number to be seen, surprised to the upside with a print of +11.5 versus -4.7 in August and versus the estimate of -4.0. The six-month business outlook bounced too, to 30.6 from 22.9 and that is the best since March 2022.

5) Not the same upside as seen in NY region, but the Philly index came in at +1.7 from -7.0 and thus around the flat line. The estimate was zero. The six-month business outlook was little changed at 15.8 versus 15.4 in August but still 10 points below the six-month average.

6) The August Cass Freight index reflected a 1% month-over-month rise in shipments after a 3% increase in July. They remain though down 1.9% year over year after a 1.1% fall in July. Cass said, with regards to the year over year declines, "These were the smallest declines in 18 months as goods demand continues to grow slowly, and slowing capacity additions reduce the pressure on for-hire shipments."

7) U.S. industrial production in August rose by .8% month over month, well above the estimate of up .2% but partly mitigated by a three-tenths downward revision to July. Most of the gain was due to a rebound in auto production. Capacity utilization rose to 78% from 77.4%.

8) Housing starts in August totaled 1.356 million, 38,000 above the estimate versus 1.237 million in July and 1.329 million in June. Single-family was the main swing factor over the past few months. In June they were 983,000, fell to 857,000 in July and came in at 992,000 in August, the same figure seen in May. It was over 1 million in the first four months of the year. Hurricane Beryl was the likely factor in July, as they fell notably in the South. Multi-family starts were 364,000 versus 380,000 in July and 346,000 in June and is well off the highs in the 600,000 range in 2022. Permits, the precursor to an eventual start, rose to a five-month high with gains for both single and multi family, but both too well off their highs.

9) With the continued drop in mortgage rates, refi's jumped by 24% week over week and purchases finally responded, rising by 5.4% week over week and are back to flattish year over year.

10) From Lennar: "Although affordability continued to be tested during the quarter, purchasers remained responsive to increased sales incentives, resulting in a 16% increase in our deliveries and a 5% increase in our new orders year over year."

11) From Darden Restaurants: "Last quarter earnings results were lower than our expectations as a result of the sales softness that impacted the industry in July. June same restaurant sales trends were in line with our fiscal 2024 fourth quarter results, and we were surprised by the significant step down in traffic, beginning with the Fourth of July holiday. However, sales trends rebounded in August, resulting in flat same restaurant sales for the month… The first three weeks of September have further improved, resulting in positive same restaurant sales quarter to date for all of our segments except Fine Dining."

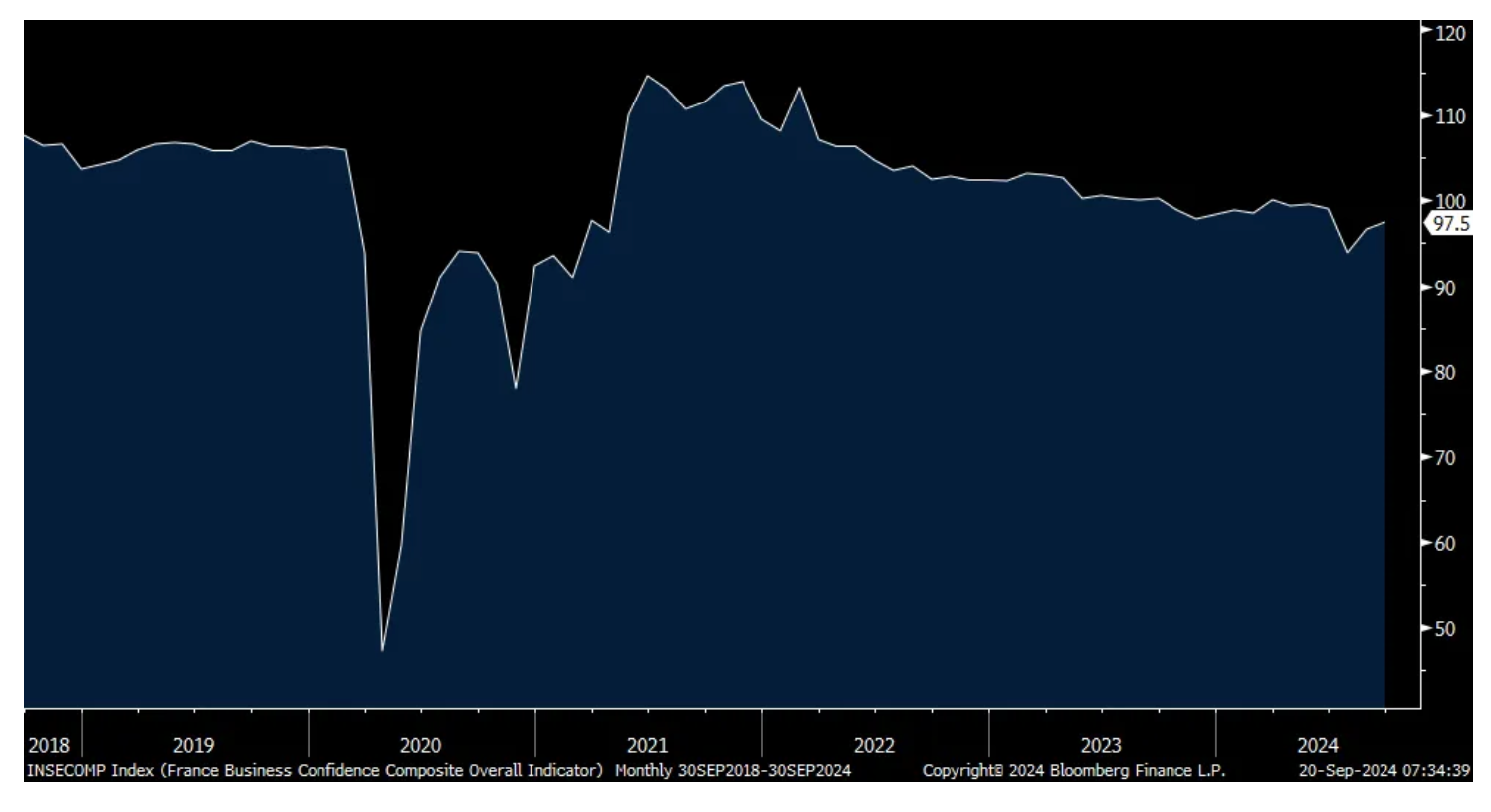

12) French business confidence in September rose one point month over month to 98 but still remains well below its pre-Covid level. A lift in retail and employment led the way as both the manufacturing and services components were unchanged.

13) August retail sales in the U.K. ex. auto fuel surprised to the upside with a 1.1% mont-over-month gain, about double the estimate of up .5%. July was also revised upward. The chief economist at the ONS said, "Retail sales rose in August as warmer weather and end of season promotions helped to boost sales, most notably for clothing and food shops. Retail sales have also increased across the three-month and annual period, following strong growth from online retailers."

14) In the U.K., August headline and core CPI rose 2.2% and 3.6%, respectively and as expected. The services component remains the real sticking point, up by 5.6% year over year. PPI, for both input and output charges, were softer than anticipated.

15) The Brazilian central bank raised its Selic rate by 25 BPS to 10.75% as they remain the most dynamic central bank in the world, both raising and cutting rates in either direction and staying well ahead of whatever curve is thrown at them.

16) Still dealing with services inflation above 5%, the BoE kept its bank rate unchanged at 5% as expected.

17) Having plenty of room to move, Bank Indonesia unexpectedly cut its overnight rate to 6% from 6.25%. The Governor said "the time is right." As for what comes next, "Bank Indonesia will continue to keep an eye on the room for lowering policy rate in line with low inflation forecast, the stable and appreciating rupiah, and the need to boost economic growth higher."

18) The Taiwanese central bank kept its benchmark rate at 2% as expected.

19) The

, "Take a right at the light, keep goin' straight until night, and then boy, you're on your own."

Negatives:

1) The Fed should have cut rates, but little difference by how much with so much priced in already but, Jay Powell & Co. better be careful from here in balancing the need for cheaper money for some, not so much for others, whether inflation proves itself from here in staying sustainably low and the easy financial conditions that we see in markets.

2) The BoJ did nothing as expected but the dovishness over the past few years has put them in a real tight spot with core inflation (ex. food) above 2% for 29 straight months.

3) The September NAHB home builder sentiment index rose to 41 from 39 but as expected and still remaining well below 50. Present conditions rose one point to 45, still in contraction, but the future outlook bounced above 50 to 53 from 49 likely due to hopes that the drop in mortgage rates will lift demand. However, buyer traffic remains punk with the prospective buyers traffic component at just 27 versus 25 in August and 27 in July. As to the lift in the outlook, the NAHB said, “Thanks to lower interest rates, builders now have a positive view for future new home sales for the first time since May 2024.” That said, keeping a lid on the current mood, “the cost of construction remains elevated relative to household budgets, holding back some enthusiasm for current housing market conditions.”

4) From Mercedes: "Overall, the sales mix in the second half of 2024 is expected to remain unchanged versus the first half, and therefore weaker than originally expected." They mostly blamed China, "This was triggered by a further deterioration of the macroeconomic environment, mainly in China. GDP growth in China lost further momentum amid weaker consumption as well as the continued downturn in the real estate sector. This affected the overall sales volume in China including sales in the Top-End segment."

5) From FedEx: "Our results reflect a challenging Q1 demand environment which was weaker than we expected, particularly in the U.S. domestic package market. Looking at our performance on a year-over-year basis, there are several factors at play. Weakness in the industrial economy pressure our B2B volumes, particularly in the U.S. We saw increasing demand for our lower-yielding services and some of this demand increase was driven by a shift in customer preference worldwide from priority to deferred services."

6) From Darden Restaurants: What's going on in Fine Dining? "Same restaurant sales at both Capital Grille and Eddie Vs were negative, as the Fine Dining category as a whole continues to be challenged." The CFO said, "It seems like there were other places where the luxury consumer was spending dollars on, especially the summer months. So, we do expect a gradual build back. I don't know that we have an exact timing of when that's going to happen, but there is a clear difference between suburban markets and urban markets. We are still operating close to that mid-70s of pre-Covid levels in the urban markets, while suburban markets are in the more of the 90s in terms of retention of pre-Covid… and then when we look at income, people all the way up to $200,000 and below we're seeing pull back. And so that's the other part of the Fine Dining impact. And they did get a lot of people, more aspirational guests maybe, and those we are really losing them pretty fast. And that's part of the reason why you saw Fine Dining decline."

7) From Sysco: "We haven't quoted August and we'll save that for our earnings call. But Q1, the quarter we're currently in is softer than the prior quarter. It softened a bit, not a major shift, but it has softened a bit. We're seeing it across all sectors. It's not just QSR, a sector that's being written about the most because of the lower income consumer being the most strained right now. Yes, QSR is being impacted, but we're seeing it across the industry right now."

8) From General Mills: "We did see a slight uptick in food consumption at home in the quarter. We did anticipate that might be the case as we see consumers seeking value. And the fact is that now food at home is four times less expensive than food eating out on average. And so, eating at home is a great value for consumers. And consumers are still economically stressed."

9) Japan's August trade data missed expectations as exports grew by 5.6%, about half the estimated increase of 10.6%. Imports were up by just 2.3%, well below the estimate of 15% growth. A typhoon in August definitely disrupted shipments but tough to say by what extent. Exports to Japan's Asian trading partners led the growth as they were little changed to the U.S. Product wise, machinery, semis, chemicals and electrical machinery drove the gains.

10) Non-oil exports from Singapore in August fell by 4.7% month over month after a strong 12.2% rise in July. The estimate was for a 2.7% fall. Versus last year, though, they are still up 10.7% with particular strength in electronic products. Taking out the influence of electronic products saw exports rise 3.7% year over year. Exports to China rose 19% and were strong to other Southeast Asian countries like Indonesia and Malaysia. They were up 6.4% to the U.S. but fell by 21% to the EU.

11) The German September ZEW investor confidence index on the German economy fell to 3.6 from 19.2 and that was well under the estimate of 17. The Current Conditions component weakened to -84.5 from -77.3 and that is the worst since the Covid shutdowns. The ZEW said, "The optimism in economic expectations that has been evident since November 2023 has thus almost completely dwindled."

12) Late last Friday China reported disappointing August retail sales, industrial production, fixed asset investment and property investment data. The jobless rate also ticked up by one-tenth to 5.3%.

Boockvar on the Yield Curve, BoJ and Important Earnings

From Peter Boockvar:

Where on the curve are you borrowing off? Plus, that other big central bank and important earnings comments

With a two-week high in the U.S. 10-year yield post FOMC, the beneficiaries of a lower fed funds rate will depend on where on the yield curve one can borrow.

Is it SOFR+ or further out? At least right now, the former is more excited than the latter, with the latter more influential to commercial real estate. There is no free lunch on what the Fed is embarking on post a 40-year high in inflation and the quickest response of "recalibration" off zero rate policy and epic QE.

The other major central bank met overnight and reverted back to its typically dovish self but with a door open to another hike by year's end, not in October though. As expected, the BoJ left policy unchanged but I expect one more hike maybe in December. At the same time, they continue to shrink the pace of asset purchases and will do so through March 2026 and something no one is seemingly paying attention to in terms of shrinking what has been a massive liquidity spigot.

Governor Ueda got spooked in July and said, "The outlook for overseas economic development is highly uncertain. Markets remain unstable. We need to scrutinize such developments carefully for the time being." The yen rally has certainly given him a bit more time and he said to this, "As such, we can afford to spend some time in making a policy decision."

Leaving open the possibility of another rate increase at one of their last few meetings, but with a caveat, Ueda said, "Looking at consumption and other data, Japan's economy is on track and moving in line with our forecasts. But, uncertainty on the U.S. economic outlook has heightened. That is offsetting some of our optimism on inflation expectations."

Keeping pressure on Ueda to, at some point, tighten policy again is the persistent pace of inflation there. Headline CPI in August rose 3% year over year with an ex. food figure of 2.8% and core/core rate of 2%, all as expected. That the BoJ still has its overnight rate at just .25% and completely missed the rate hiking cycle which has now given other central banks the ability to cut was a terribly missed opportunity. Inflation breakevens are unchanged in response to the in-line figures.

The two things to respond to what Ueda said is the yen, which is weaker, and the Nikkei, which was stronger. JGB yields were little changed. We remain bullish and long Japanese stocks.

On the economic ground, we were reminded again yesterday that there are continued pockets of softness and challenges.

Mercedes stock is down 7% as after their market close yesterday said, "Overall, the sales mix in the second half of 2024 is expected to remain unchanged versus the first half, and therefore weaker than originally expected." They mostly blamed China, "This was triggered by a further deterioration of the macroeconomic environment, mainly in China. GDP growth in China lost further momentum amid weaker consumption as well as the continued downturn in the real estate sector. This affected the overall sales volume in China including sales in the top-end segment."

Skechers, speaking at the Wells Fargo consumer conference, said, "We've definitely seen worse conditions unfold in China than we expected for the back half of the year, so I would expect the back of the year's going to be more disappointing than what we had originally thought. I think that's a market that's still re-forming itself post Covid."

From FedEx, a stock we own:

"Our results reflect a challenging Q1 demand environment which was weaker than we expected, particularly in the U.S. domestic package market. Looking at our performance on a year-over-year basis, there are several factors at play. Weakness in the industrial economy pressure our B2B volumes, particularly in the U.S. We saw increasing demand for our lower-yielding services and some of this demand increase was driven by a shift in customer preference worldwide from priority to deferred services."

From Lennar's press release and where the discounting, impacting margins, is likely why the stock is down, along with a miss in orders:

"Although affordability continued to be tested during the quarter, purchasers remained responsive to increased sales incentives, resulting in a 16% increase in our deliveries and a 5% increase in our new orders year over year."

They also said, "This week, the Fed decreased interest rates which should start to enhance affordability and accelerate the already strong demand for both new and existing homes." As I said, though ,in the first sentence of this piece, the benefit from the rate cuts has already been fully priced in and long rates have now ticked higher again.

From Darden Restaurants, owning everything from Olive Garden, Yard House, LongHorn Steak, Ruth's Chris, Cheddar's, The Capital Grille, Season 52 and Eddie V's:

"Last quarter earnings results were lower than our expectations as a result of the sales softness that impacted the industry in July. June same restaurant sales trends were in line with our fiscal 2024 fourth quarter results, and we were surprised by the significant step down in traffic, beginning with the Fourth of July holiday. However, sales trends rebounded in August, resulting in flat same restaurant sales for the month."

Also, "The first three weeks of September have further improved, resulting in positive same restaurant sales quarter to date for all of our segments except Fine Dining."

What's going on in Fine Dining?

"Same restaurant sales at both Capital Grille and Eddie Vs were negative, as the Fine Dining category as a whole continues to be challenged," The CFO said. "It seems like there were other places where the luxury consumer was spending dollars on, especially the summer months. So, we do expect a gradual build back. I don't know that we have an exact timing of when that's going to happen, but there is a clear difference between suburban markets and urban markets. We are still operating close to that mid-70s of pre Covid levels in the urban markets, while suburban markets are in the more of the 90s in terms of retention of pre-Covid."

Not everyone back to work five days a week in urban markets has broad economic consequences in these areas for sure.

Also, "and then when we look at income, people all the way up to $200,000 and below we're seeing pull back. And so that's the other part of the Fine Dining impact. And they did get a lot of people, more aspirational guests maybe, and those we are really losing them pretty fast. And that's part of the reason why you saw Fine Dining decline."

That more cautious "aspirational" buyer is something we've heard from all the luxury goods markets too.

From Cracker Barrel:

They saw a .4% rise in comp store restaurant sales that included a 4.2% rise in pricing, similar to what CPI told us for out of home dining. They saw commodity inflation of about 1% and "hourly wage inflation of approximately 5%, and higher workers' compensation expense."

With guidance, they see pricing up about 5%, commodity inflation of 2% to 3% and hourly restaurant wage inflation of 3% to 4%.

In terms of their customer, "We've seen a little uptick in our 65 plus group, which is positive because they had been down prior... But other than that, the demographics have stayed pretty, pretty similar. We have seen a decline among the under $60,000 a year cohort and spending. So we're just kind of keeping our eye on that."

In order to drive traffic, they also are focused on providing value and broadening their loyalty program. As an example, "We introduced a new Sunrise Pancake Special for $7.99. It's an incredible value. It includes two fluffy, delicious buttermilk pancakes, two eggs, and your choice of bacon or sausage." Yum.

Likely driving that increase in traffic for the 65-plus cohort, "We're continuing to highlight our early dinner deals. These offerings are an exceptional value." Nothing like the early bird special.

Overseas, French business confidence in September rose one point month over month to 98, but still remains well below its pre-Covid level. A lift in retail and employment led the way as both the manufacturing and services components were unchanged. Nothing market moving here today.

French Business Confidence

August retail sales in the U.K. ex-auto fuel surprised to the upside with a 1.1% month-over-month gain, about double the estimate of up .5%. July was also revised upward. The chief economist at the ONS said, "Retail sales rose in August as warmer weather and end of season promotions helped to boost sales, most notably for clothing and food shops. Retail sales have also increased across the three-month and annual period, following strong growth from online retailers."

The U.K. economy has really hung in there and we remain bullish and long some U.K. stocks where some of the cheapest in the world reside.

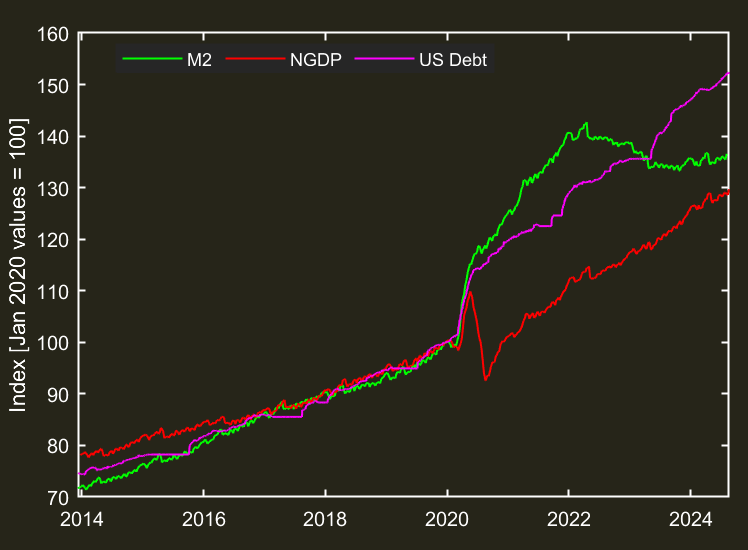

"Doug, I loved your 'post Fed Rant' post. It really puts things into perspective for myself as to the past year. Dollars added to the debt are not adding equal but fractional value to the GDP (as expected) but the money supply (M2) picked up in 2023 and while it was trending to the GDP line is now not converging further. Many thanks."

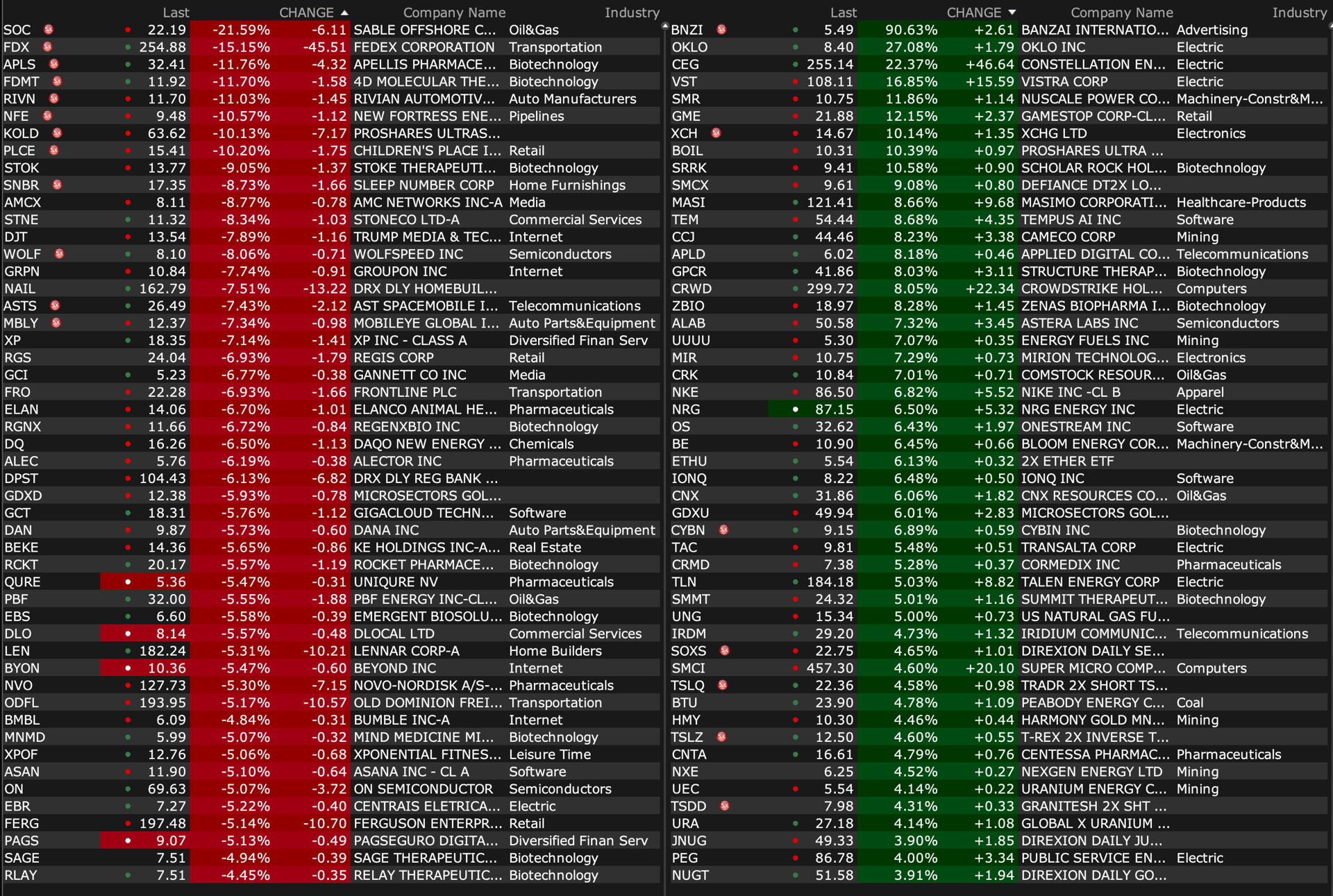

-BATL +120% (announces amendment to Merger Agreement with Fury Resources, Inc.)

-BNZI +63% (files to sell 25M in Class A shares)

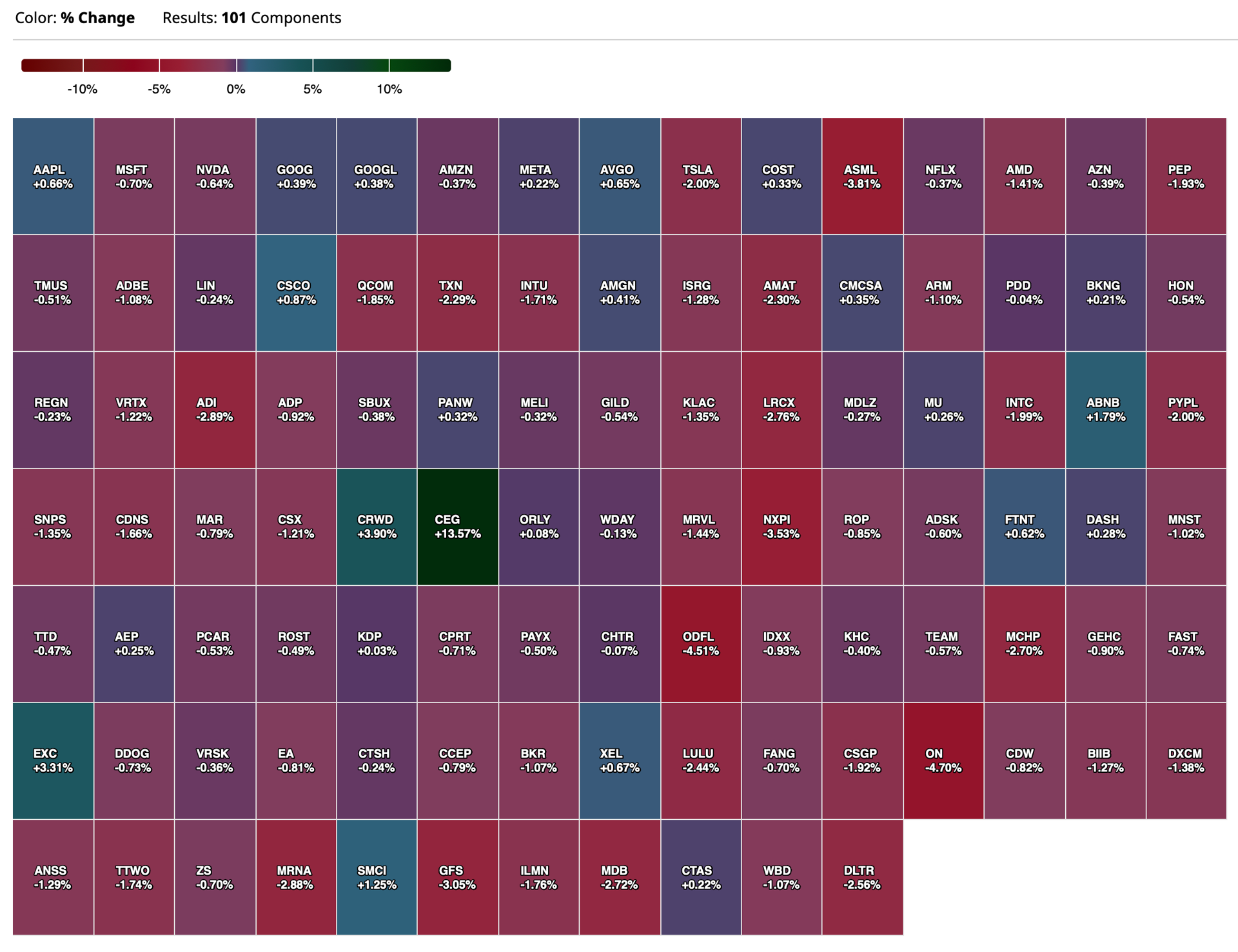

-CEG +9.3% (signs 20-yrs power purchase agreement with Microsoft, to restore Three Miles Island (TMI) Nuclear Unit 1 in Pennsylvania to service and keep it online for decades)

-NKE +8.0% (Nike veteran Elliott Hill to return as President/CEO; John Donahoe to retire, effective Nov 14th)

-SLI +5.6% (subsidiary SWA Lithium LLC selected for up to $225M award negotiation from U.S. Department of Energy (DOE) for a critical minerals project, part of the Infrastructure Investment and Jobs Act)

-OPTT +4.5% (files to sell up to $3.0M shares)

-ATNM +3.7% (announces publication of results from the Phase 3 SIERRA Trial of Iomab-B in the Journal of Clinical Oncology)

-UEC +3.6% (strength off restoration plan for Three Miles Island)

Downside:

-KOPN -30% (prices 37.5M shares at $0.65/shr)

-FDX -13% (earnings, guidance)

-APLS -6.6% (receives negative CHMP opinion for Pegcetacoplan for Geographic Atrophy (GA) in the EU following re-examination)

-DJT -5.8% (Former President Trump permitted to begin selling shares following lockup expiration)

-MLKN -5.7% (earnings, guidance)

-FRO -5.0% (multiple broker downgrades)

-LEN -4.0% (earnings, guidance)

-CHWY -3.2% (prices 16.67M shares at $30/share; announces concurrent $300M stock buyback from selling holder)

-RPD -2.2% (RBC Cuts RPD to Sector Perform from Outperform, price target: $40 from $50)

Below are two simple and interesting charts to consider after the Federal Reserve cut rates by 50 basis points.

* M2 is still well above trendline and you could easily argue the growth in money supply from 2014-2020 was higher than it needed to be.

* M2 is now growing again, banks are lending again and velocity is also increasing (in part due to all the government spending).

* A healthy mature economy should grow at roughly +3%, have +2% inflation, so GDP growth should be +5%. We are currently about 6%+ (from deficit spending) and M2 is increasing -- so it is not like things have really cooled off.

* Whatever inflation is, it is understated.

As the wise woman, Grandma Koufax once said, "we shall see what we shall see"...

JPMorgan on the most popular equity, Federal Express (company specific or economy specific?):

2Q Commentary / 2H Ramp (off the call, still ongoing) – would not give an explicit guide for 2Q but messaged to expect lower than normal seasonality in Q2 (historically, normal seasonality is +L-MSD% 1Q to 2Q) given USPS contract termination that will be a headwind as well as negative effect from timing of cyberweek which will push into 3Q, but then was pressed further to get color on 2Q expectation and said “definitely see the opportunity for sequential q/q profit improvement” so think most are thinking that flat EPS q/q is on the table. To be clear, flat q/q ($3.60) would still put implied 2Q guide well below street ($4.46), and lets say its flat q/q, it puts a lot of pressure to ramp earnings 1H to 2H. FDX is expecting better than normal seasonality in 2H (when asked why confident in that, said driven by revenue actions and ramping up DRIVE), but in order to hit even low end of guide would need to see a big step up, which is a large source of negative feedback on the print/call so far as people feel that further cuts to FY could be on the table. Mgmt emphasizing DRIVE and recovery in volumes (as well as help from GRI and demand surcharges) as giving them confidence in being able to step up to hit that 2H guide but so far feedback suggest investors are not going to give benefit of the doubt believing in the 2H step up after such a negative surprise tonight w/ 1Q disappointment. FDX -11%, after starting the call down just shy of -10%. Haven’t heard anyone pitching a bull angle on anyone from this print or call so far, and mgmt will not comment any further on Freight strategic review beyond the statement that the assessment is well underway and on track to complete it & communicate the outcome by end of calendar yr – the SOTP angle is the main bull case that seems to be keeping the stock from getting pressed much below this mid $260s level despite no one seeming to want to buy on this weakness.

US: Futs are lower across the board. In MegaCap Tech, TSLA (-3.6%) is the top mover, followed by META (-1.8%) and AAPL (-1.7%). Yields are mostly higher, and USD is largely unchanged; 5-, 10-yr yields are 5bp, 10bp higher. Commodities are mixed with oil and metals higher, while ags are mostly lower. FDX is down -13% after its earnings release yesterday; UPS -2.4%. BOJ announced no hike to its policy rate, in line with expectation, and further signaled the gradualist approach to its rate hikes. USDJPY +0.8% to 143.8; NKY +1.5%. PBOC left loan prime rates unchanged.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, we saw aglobal risk-on rally since Asia markets open on Wednesday night. We saw both short-covering and buying in Mag 7 and Cyclicals. Matt Reiner from cash trading desk tells us that: “we’re seeing LO demand in Mega-Tech, and not so much in small/mid cap yet. I would have though the LO bid would be showing up in higher leverage, riskier assets but thus far that bid is absent at this point.” Large-Cap banks outperformed credit card companies as both V and MA fell on WMT’s instant bank payments announcement. Catalysts yesterday remain muted, but Initial Jobless Claims suggests some improvement in the labor market.

I have been called out of the office for all of the morning so my posts will be less frequent and shorter.

This post was published late yesterday - I will expand upon it on Monday:

Short Home Builders (Part Trois)

I suspect, under normal conditions, Lennar's (LEN) results augur poorly for home builders tomorrow.

From the Comments Section:

STAFF

34 minutes ago

Lennar lower backlogs on bottom end of unit deliveries, more tomorrow... Gross margin came in at 22.5% v 23% estimate and forecast 4Q margins flat (22.5%) v. 24.5% consensus estimates)