Post Script

Super Micro's SMCI margins were awful and the stock is getting schmeissed.

Dell DELL just announced layoffs.

So much for the prosperity of AI.

For now it's just a license to lose money.

BY Doug Kass · Aug 6, 2024, 7:23 PM EDT

Super Micro's SMCI margins were awful and the stock is getting schmeissed.

Dell DELL just announced layoffs.

So much for the prosperity of AI.

For now it's just a license to lose money.

BY Doug Kass · Aug 6, 2024, 7:23 PM EDT

I briefly looked at Super Mocro Computer's SMCI earnings release — margins were horrific and I don't understand why the stock gapped higher.

I expect the post-market strength in semis to reverse and put pressure on the indices tonite.

BY Doug Kass · Aug 6, 2024, 6:27 PM EDT

As of 4:24 p.m.

BY Doug Kass · Aug 6, 2024, 4:45 PM EDT

Break in!

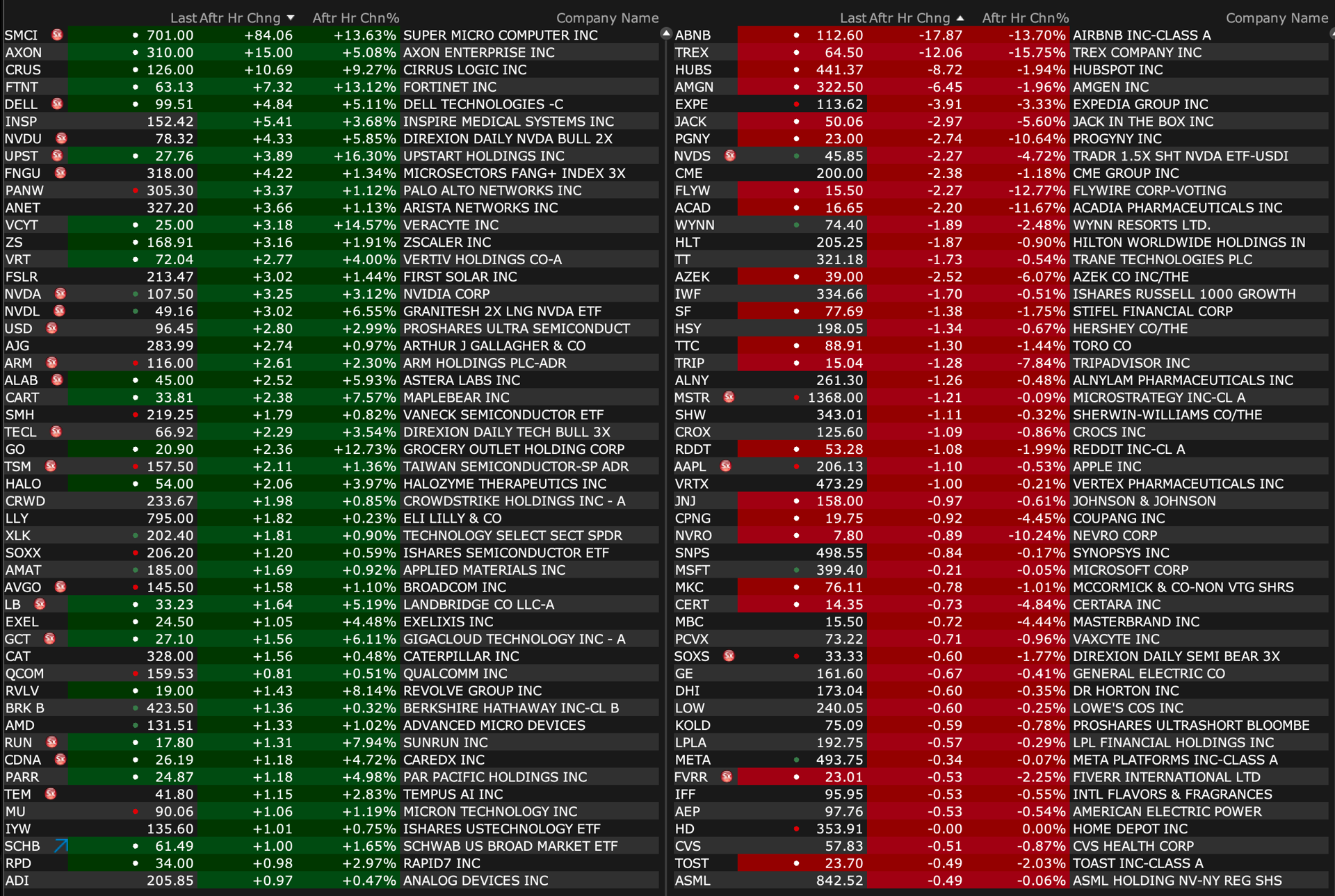

Semis higher after Super Micro SMCI numbers.

NVDA, AMD, DELL... all trading up.

BY Doug Kass · Aug 6, 2024, 4:30 PM EDT

Wolf Street howls about reverse repos.

BY Doug Kass · Aug 6, 2024, 4:15 PM EDT

Poor execution on the SPY/QQQ trades.

Right idea (that the market was a sale on strength) — but impatient in process.

Made some money but left too much on the table.

Next time.

BY Doug Kass · Aug 6, 2024, 4:07 PM EDT

* "Just in case" and I am prepared to rip them up!

I am buying call options on OXY for Friday (out of the money)... just in case an additional filing of more Berkshire Hathaway BRK.A BRK.B purchases are made tonite.

BY Doug Kass · Aug 6, 2024, 3:41 PM EDT

BY Doug Kass · Aug 6, 2024, 3:35 PM EDT

Covers:

* SPY $525.85

* QQQ $443.33

From earlier:

With S&P cash +108 handles I have shorted a small position in the indices:

* (SPY) $527.81

* (QQQ) $445.75

Position: Short SPY (VS), QQQ (VS)

BY DOUG KASS AUG 6, 2024 1:42 PM EDT

BY Doug Kass · Aug 6, 2024, 3:19 PM EDT

* The Google Antitrust Case was a focus for me nine months ago...

From my 10 Surprises for 2024:

Surprise #5. The biggest and most popular stock in the world, Apple, suffers a large percentage loss in 2024 as trade tensions with China escalate. With China supporting Huawei, Apple loses substantial market share in that country and overall revenues decline again in 2024 (over 2023). Meanwhile, as a result of the Google Anti-Trust case, Google undefined stops paying Apple $18 billion in search fees.

From yesterday:

Google's (GOOGL) adverse court decision hurts Apple (AAPL) (and we can see the swift decline in the shares).

From Morgan Stanley:

"GOOGL would likely need to see 15%+ search traffic losses in order to make TAC reductions NPV negative. Given the high utility and continued innovation of GOOGL's products, differentiation of the logged in ecosystem, etc, this to us seems like a low probability risk.

For Apple, in a worst-case scenario (total TAC elimination globally), we see 15% EPS downside risk (~$1.20 FY25 EPS), but there are a number of other potential less severe outcomes that are possible, and we would ascribe a low probability to this worst-case scenario playing out."

AUG 5, 2024 3:15 PM EDT

BY Doug Kass · Aug 6, 2024, 3:05 PM EDT

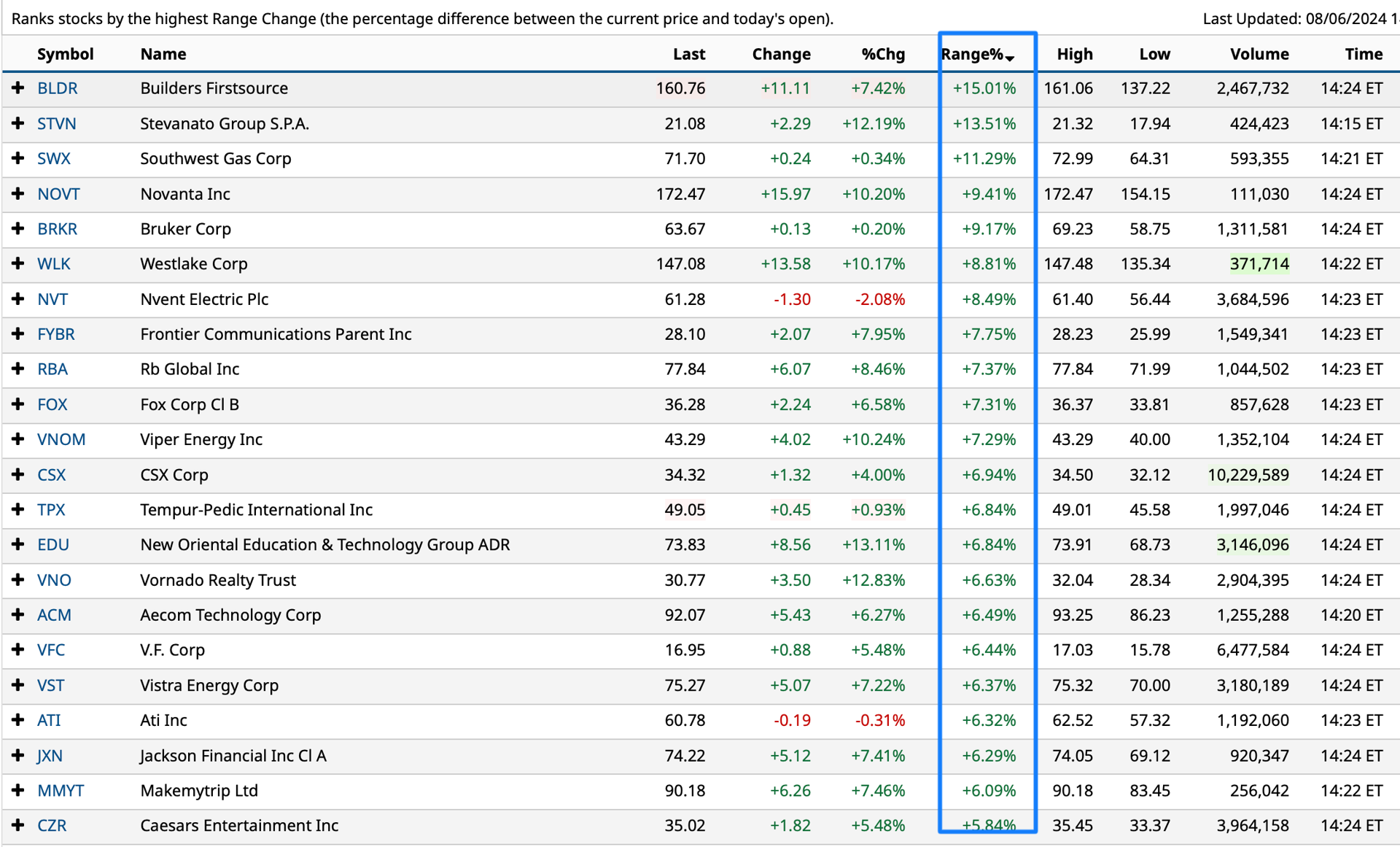

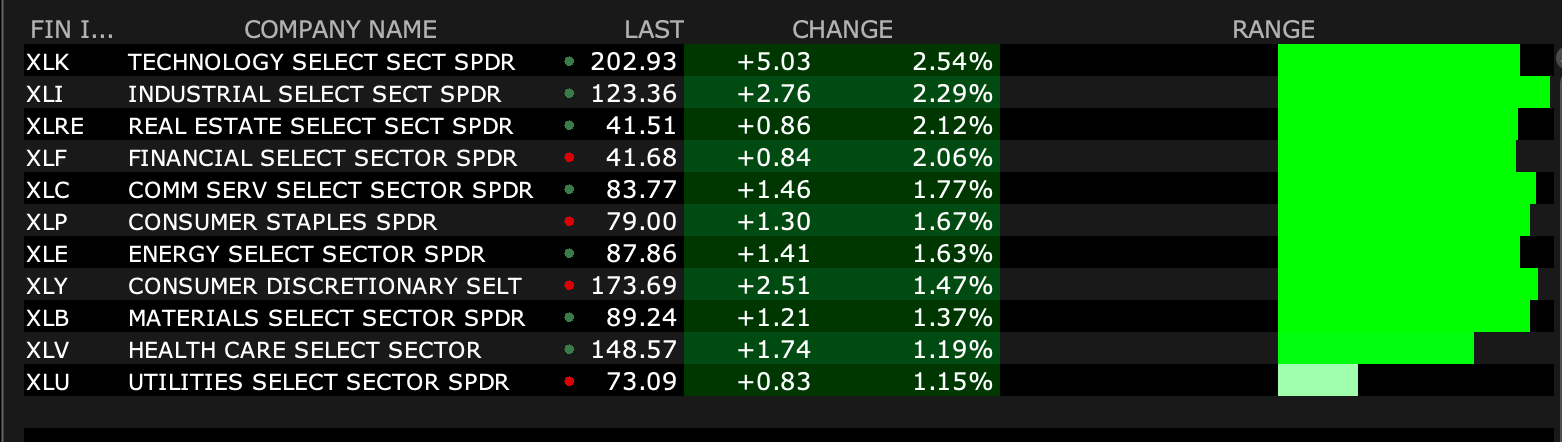

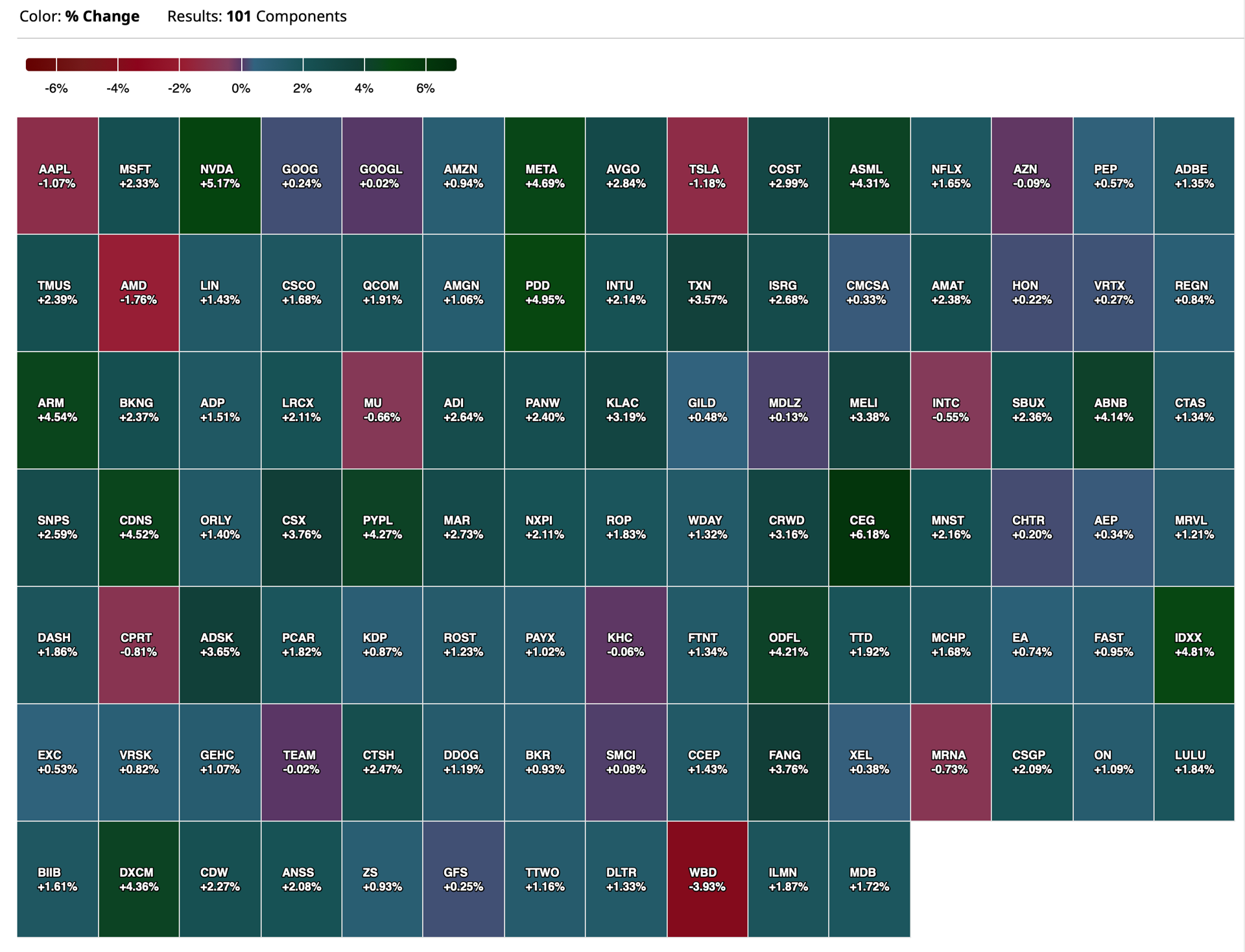

ADVANCING Large-Cap Stocks With Widest % Range on Day

DECLINING Large-Cap Stocks With Widest % Range on Day

BY Doug Kass · Aug 6, 2024, 2:50 PM EDT

Back near the high in the S&P Index in mid-June this strategist raised his S&P target from 4750 to 6000.

Wall Street’s new top S&P target is 6,000. Here’s why. - MarketWatch

His arguments for such a massive increase in price target were specious to me.

At the time I said moving from the lowest S&P target to the highest tells us a lot more about the forecaster than his forecast.

Which gets me to my tweet this morning:

BY Doug Kass · Aug 6, 2024, 2:30 PM EDT

From Dr. Deemer:

BY Doug Kass · Aug 6, 2024, 2:18 PM EDT

With S&P cash +108 handles I have shorted a small position in the indices:

* SPY $527.81

* QQQ $445.75

BY Doug Kass · Aug 6, 2024, 1:42 PM EDT

BY Doug Kass · Aug 6, 2024, 1:25 PM EDT

What follows is a compilation of some of my Diary entries and recent communiques with my Limited Partners in my hedge fund (Seabreeze Partners):

I am just a poor boy

Though my story's seldom told

I have squandered my resistance

For a pocketful of mumbles

Such are promises

All lies and jest

Still a man hears what he wants to hear

And disregards the rest

- Simon & Garfunkel, The Boxer (1969)

Thus far in 2024 market participants have embraced the idea of an economic "Goldilocks" — a domestic economy that was not too cold and not too hot.

I have argued otherwise — citing a host of political, geopolitical, fundamental (economic and corporate profit growth), market structure, valuation and other concerns. I have been particularly mystified by how expensive stocks were relative to interest rates — with the equity risk premium at a two-decade low and with short-term Treasury returns nearly 4x the S&P dividend yield.

Until recently the market has paid little heed to my apprehensiveness. Though earnings estimates for the S&P 500 Index have been reduced for both 2024 and 2025, "animal spirits" and the fear of missing out (FOMO) coupled with buying from momentum-based systematic products and strategies stoked higher stock prices.

In addition to the previously discussed headwinds, I continue to hold to several non-consensus viewpoints:

1. A few interest rate cuts will likely fail to stabilize/improve the U.S. economy.

2. Just as the lag of monetary tightening was longer than expected (it was different that time (2022-24)!), so may the easing have a lengthier impact (and be different this time (2024-26)!)

3. The Fed may be ultimately forced to more aggressively ease next year, raising fears of a resurgence of inflation "down the road."

4. The herd/consensus — acting like Pavlov's dogs — may again be wrong in its bullish thesis.

Open market interest rates have slipped over the last two weeks — coincident with lower economic readings and market participants' expectations that the Federal Reserve might lower the Fed Funds more aggressively this year.

As a direct result (and until late last week), equities continued to firm.

A reminder: Buying stocks in October 2007 when the Fed first cut rates was a poor idea — as it was when the Fed (under Greenspan) cut rates in 2000.

Despite the magnitude and rapidity of the recent market decline I think that economic (and stock market) optimism is still overdone for some of the following reasons:

* The U.S. economy is far less interest-rate sensitive than previously assumed.

* It took the Fed undertaking the most rapid increase in interest rates in decades to slowly dull domestic economic growth — it follows that it will likely take a rapid decline in interest rates to stabilize/improve economic growth in the U.S.

* It has taken more and more debt and money creation to generate a unit of production over the last decade.

* The stacked inflation (since 2020) is unique to the last few decades and remains a headwind to the consumer — and no rate cut changes its cumulative impact.

* Also unique is the U.S. deficit and burgeoning debt load which acts, increasingly, as a governor to economic growth.

* A large swath of disadvantaged U.S. consumers ("the have nots") may not have access to lower-cost credit. Underwriting standards will tighten further as the economy moves lower. Moreover, it is unlikely that credit-card rates will be lowered commensurate with reduced open market rates.

One vivid example of a changing rate/economy relationship can be seen in the housing market, which was mis-forecast by the Federal Reserve and by economists. After 15 years of zero interest rates, consumers had materially reduced their mortgage rates (through new mortgages and refinancings) — rendering a reluctance to substitute a 3% mortgage rate with a 7% mortgage rate. As a result, the supply of homes for sale contracted and home prices remained firm.

Lower interest rates may have the opposite intended effect (especially when it coincides with higher unemployment) — by finally increasing the supply of homes for sale, serving to pressure home prices.

The boxer in Simon & Garfunkel's song is a metaphor: Despite having a strong memory for each and every defeat and setback he has endured ("carries the reminder of every glove that laid him down or cut him til he cried out"), he will not give up but will persevere ("the fighter still remains").

Though wrong in market view (and being modestly net short) I have persevered too — reporting a modestly profitable investment return throughout the heady market advance. To this end I recall one of Warren Buffett's most important quotes:

Speaking of Buffett (as noted previously) I have shared his negative market view, which came to the fore on this news over the past weekend:

While stocks have recently slipped, Goldilocks remains a well-embedded narrative.

In contrast to the consensus, it is my view that the U.S. economy has already entered a downturn:

As a result, I am growing more confident that stocks will ultimately decline to a level in which I will want to participate on the long side.

While a good entry point may lie ahead — it may come from still lower levels.

To emphasize... when justified, my (and Seabreeze's) approach is that of a contrarian and not a perma anything.

I fully recognize that positioning of the short side helps to preserve capital but that long positioning generates capital.

Through the course of the market's cycles, I have eschewed the crowd's emotion which has been so conspicuous in 2024's market advance (that has been based on a reset higher in valuations but, arguably, not in an improvement in the fundamental outlook).

Rather, I evaluate equities dispassionately with a calculator in hand — seeking value and a "margin of safety" based on the calculus of an upside/downside analysis.

That said, already some equities (that have fallen far more precipitously than the Indices) are already approaching a point of presenting a more favorable reward vs. risk ratio.

As (or if) stocks continue to fall. I plan to transition from a defensive pairs strategy into a modestly more bullish (and opportunistic) longer positioning.

BY Doug Kass · Aug 6, 2024, 12:20 PM EDT

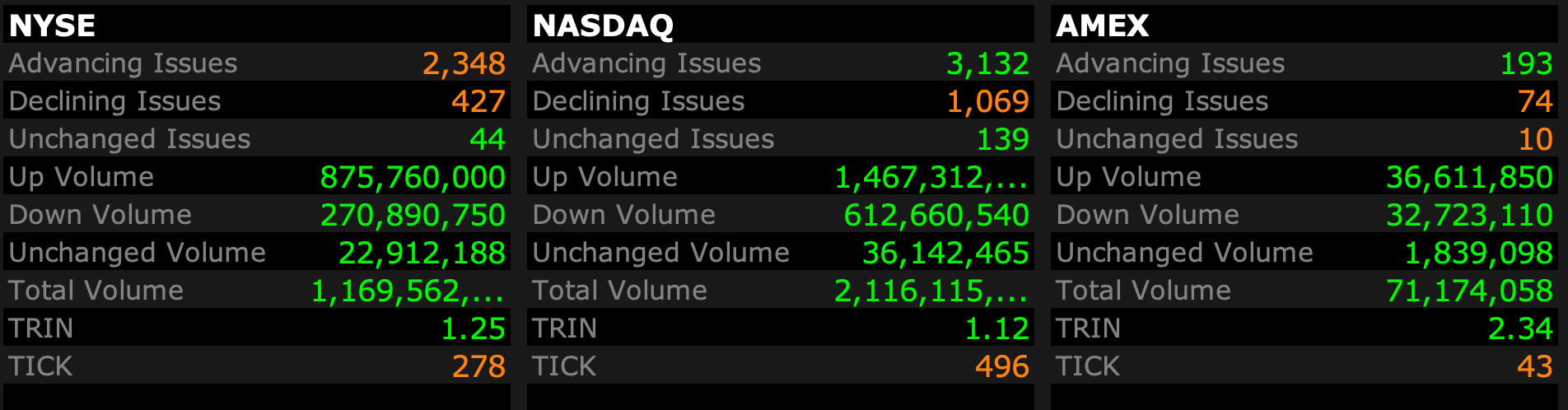

At 10:50 a.m.:

- NYSE volume 167M shares, 17% above its one-month average;

- NASDAQ volume 1.76B shares, 2% above its one-month average;

BY Doug Kass · Aug 6, 2024, 11:15 AM EDT

The action is volatile and unpredictable.

Size accordingly.

BY Doug Kass · Aug 6, 2024, 11:00 AM EDT

From Peter Boockvar:

The cry for the inter-meeting cut/Other interesting things

The only reason why I keep hearing people cry for an inter-meeting Fed rate cut is because the Fed over the past few decades has bailed out markets so many times. People have been trained all too well to expect it. I think former Dallas Fed President Richard Fisher yesterday on CNBC laid it out well when he said "The Fed will always act if something occurs that threatens the credit system or the economy and it is not yet clear what has happened the last few days, including today with the Dow off over 1,000, that is going to threaten the economy or the credit system. If it does, then they would move." He also highlighted that the Fed has the Jackson Hole meeting in two weeks that they can use to signal to the markets.

And while I do believe the Fed had reason to definitely cut last week in order to start taking the edge off interest rates in a lackluster economy, slowing labor market and cooling inflation for now, the bond market has clearly cut rates notably for them already and there is institutional credibility at stake if they respond to every single market hissy fit, especially inter-meeting. And while there have been economic/earnings fundamental, technical and market sentiment reasons to question the sustainability of the stock and credit market rallies, the Fed is not going to respond to a leveraged unwind in an FX carry trade, however huge it appears to have been.

Japan is not just The Land of the Rising Sun. It became The Land of Easy Money and keep in mind that the BoJ's first rate hike in March 2024 that took them out of negative rate policy, finally, was a full two years AFTER developed countries started to hike and almost three years after emerging market central banks started to. It was the last place on earth that provided cheap money. This leveraged carry trade has been building for a while and I still have no idea how big it got in terms of dollars. And I'm sure it has more unwind to go but it will stop at some point. The question then is whether it's an all clear or we will shift our focus back to the economic and earnings fundamentals that I believe are shifting to a more challenged time. I thus believe in the latter.

By the way, I did see a strategist at JPM who thinks the yen carry trade unwind is about half done.

The Nikkei bounced back by 10%, the yen is a bit weaker and the 10 yr JGB yield rebounded by 11 bps after falling by 16 bps yesterday. We still like Japanese stocks and a lower beta way of playing is Seven & I Holdings, the owner of 7-11. Higher rates in Japan, and also in the rest of the world, after years of around zero with mountains of QE, was never going to be a smooth process but one that needed to take place.

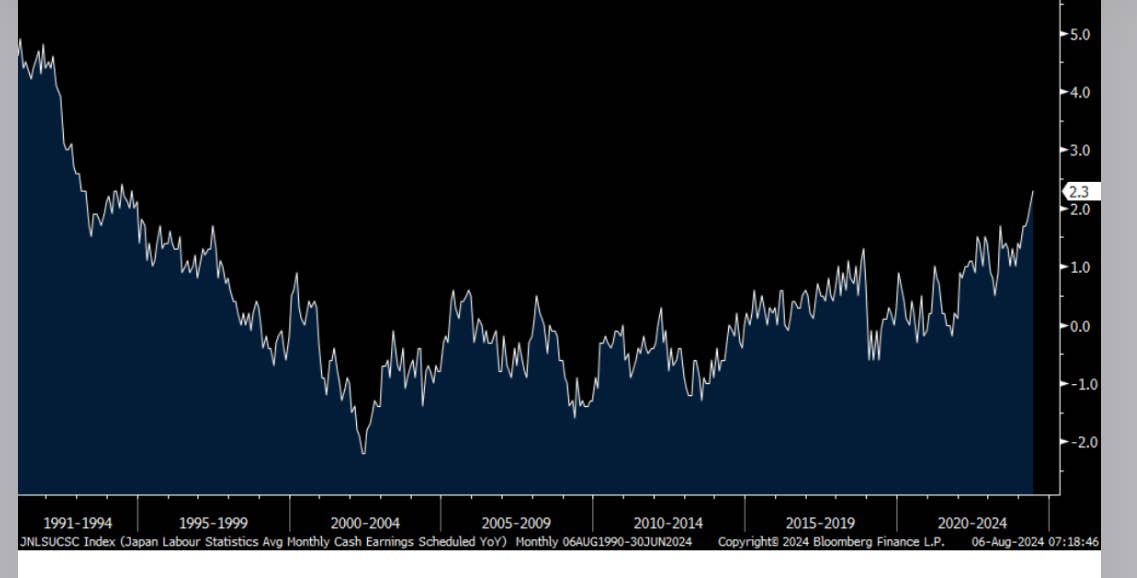

Japan did get great news on the wage front as in June base pay rose 2.3% y/o/y, up from 2.1% in May, 1.8% in April and 1.7% in the two prior months. That is the fastest pace since 1994 and is finally catching up to the rate of inflation.

Base Pay y/o/y in Japan

Here are some earnings comments.

From Sonic Automotive:

They talked about the rising inventories they are experiencing where they ended the quarter at 59 days of supply, up from 50 days at the end of the first quarter. "This increase was driven in part by slower sales rate in the last 12 days of the quarter, as well as certain models that were subject to top sale order from the manufacturer." In response, "our team continues to work closely with our manufacturer partners to manage new vehicle inventory levels." They said Toyota inventories are lean because sales of their products are good, along with Honda, Hyundai, Subaru and BMW. They are seeing too much inventory from Stellantis and Nissan, and among others like Mercedes. And, "with day supply going up, price is going to come down, incentives are going to get better."

"In the used vehicle market, wholesale auction prices for three year old vehicles decreased 5% during the 2nd quarter, while our franchise dealerships average retail used pricing was flat compared to the first quarter...Elevated used retail prices remain a challenge for consumers, contributing to affordability concerns amid the current interest rate environment. However, the return to normal seasonal trends in the used vehicle wholesale pricing are positive for our business outlook and should benefit affordability and used vehicle sales volume going forward."

From Simon Property, the owner of many high end malls but also has an outlet business:

"I think we've been pretty consistent for well over a year that the lower income consumer has been under pressure for quite some time, primarily because of the inflation that's affected them. So that continues to be the case, they are very focused on managing their bills and discretionary expenditures have been obviously not where we'd like to see them."

Also, "We haven't seen a slowdown in the higher end consumer. Obviously, the market is in an interesting point. We have not seen the wealth impact at all impact the higher end consumer. So we're still pretty sanguine about it. I think, as you know, we kind of budgeted at the beginning of the year flat sales. We're a little bit above that."

From Builders FirstSource, "the largest US supplier of building products, prefabricated components, and value added services to the professional market segment for new residential construction and repair and remodeling":

"we continue to see weaker than expected Single-Family starts, slowing Multi-Family, and broader housing affordability challenges."

The Reserve Bank of Australia kept interest rates unchanged as expected at 4.35%. Governor Michele Bullock is turning out to be a clear hawk. She said "Make no mistake, inflation is still too high" and "near-term interest rate cuts are not on the agenda...What I'm trying to tell the markets today is that I think probably expectations for interest rate cuts are a little bit ahead of themselves."

In their statement, "Policy will need to be sufficiently restrictive until the board is confident that inflation is moving sustainably towards the target range."

She even chimed in on the selloff around the world, and in the US. "I think everyone felt that perhaps it was a bit rich valuations in the equity markets, particularly in the United States" and it was an "overreaction" to a weak jobs report.

Notwithstanding the hawkishness, Aussie yields are lower as is the currency while the ASX bounced by just .4% after the 3.7% selloff yesterday.

German factory orders in June jumped 3.9% m/o/m, well more than the estimate of up .5% and was due to a surge in autos and aircraft. Domestic orders too the led the way as they fell by .3% m/o/m to the rest of the Eurozone and rose just .9% in non-Eurozone countries after a 4.8% drop in May. Because of the lumpiness of autos and aircraft, we need to see more broadening in order to believe that the German economy is in the clear.

BY Doug Kass · Aug 6, 2024, 9:45 AM EDT

I have long cited geopolitical risks as a stock market headwind - "the other" Dougie agrees:

douglas cassel

1 hour ago

The Japan debacle seems to have distracted people from the Mideast caldron. Iran has delayed their response, but appears to have done so just in order to finish preparations. This time, I think it is unlikely Israel will sit back and take it, especially if Hezbollah is involved or real damage is done. Potential Israeli targets include nuclear facilities and oil refineries in Iran. The present snap back rally, and the talking heads on CNBC, seem oblivious to this impending crisis, which perplexes me. Additionally, it is hard for me to imagine some hedge funds will not go belly up on the Japan reversal, which has to have repercussions.

I have cut back exposure significantly, which helped some yesterday, but was still hurt by crypto's dump. As much as some inner voices are telling me to buy, I am resisting until some of these issues play out.

BY Doug Kass · Aug 6, 2024, 9:25 AM EDT

After the close, Green Thumb GTBIF crushed it! Green Thumb Industries Inc. - Green Thumb Industries Reports Second Quarter 2024 Results (gtigrows.com)

This should augur well for the cannabis sector.

I added yesterday.

BY Doug Kass · Aug 6, 2024, 9:11 AM EDT

Masterhedge

51 minutes ago

"If you don't do macro, macro does you" I think is still very appropriate. However, since 2008 many active public equity managers have gone overboard. The current generation see everything in terms of 2008 which we all know was very very bad. Calling 10 corrections and getting people "out" may seem good until you realize virtually ALL corrections have been buying opportunities, except 2008 and even that in the long run was too. Add in the systematic, automated and index funds and we will always have a degree of volatility. The good macro guys like Hedgeye may very well get you "out" unlike Tom Lee but the real BIG money is getting back in or staying IN via hedging and there they are somewhat questionable in process. Also the genuine great stock pickers are very few and far between because it is such hard work and requires extensive time and resources. Stock market part timers are very vulnerable to these macro research "fly tippers" (a British saying where a person illegally leaves waste in an unauthorized space).

For me the analogue for this correction remains 1998 and the Russian Debt crisis and the blow up of LTCM. At this stage if no significant financial institution has been fatally hurt then the correction is over. A pod shop blowing up can be dealt with in a day or two, Citadel maybe in a week.

BY Doug Kass · Aug 6, 2024, 8:23 AM EDT

Kdog88

18 minutes ago

Dougie…..would really appreciate your best guess on a range for the S&P for the balance of this year. Thanks.

Reply

DK

Dougie Kass

STAFF

Just Now

4800-5300 a guess.

poor reward v risk imho.

BY Doug Kass · Aug 6, 2024, 8:10 AM EDT

The S&P Short Range Oscillator has shifted to a small oversold (at -2.47% vs. 1.37%).

BY Doug Kass · Aug 6, 2024, 7:50 AM EDT

BY Doug Kass · Aug 6, 2024, 7:46 AM EDT

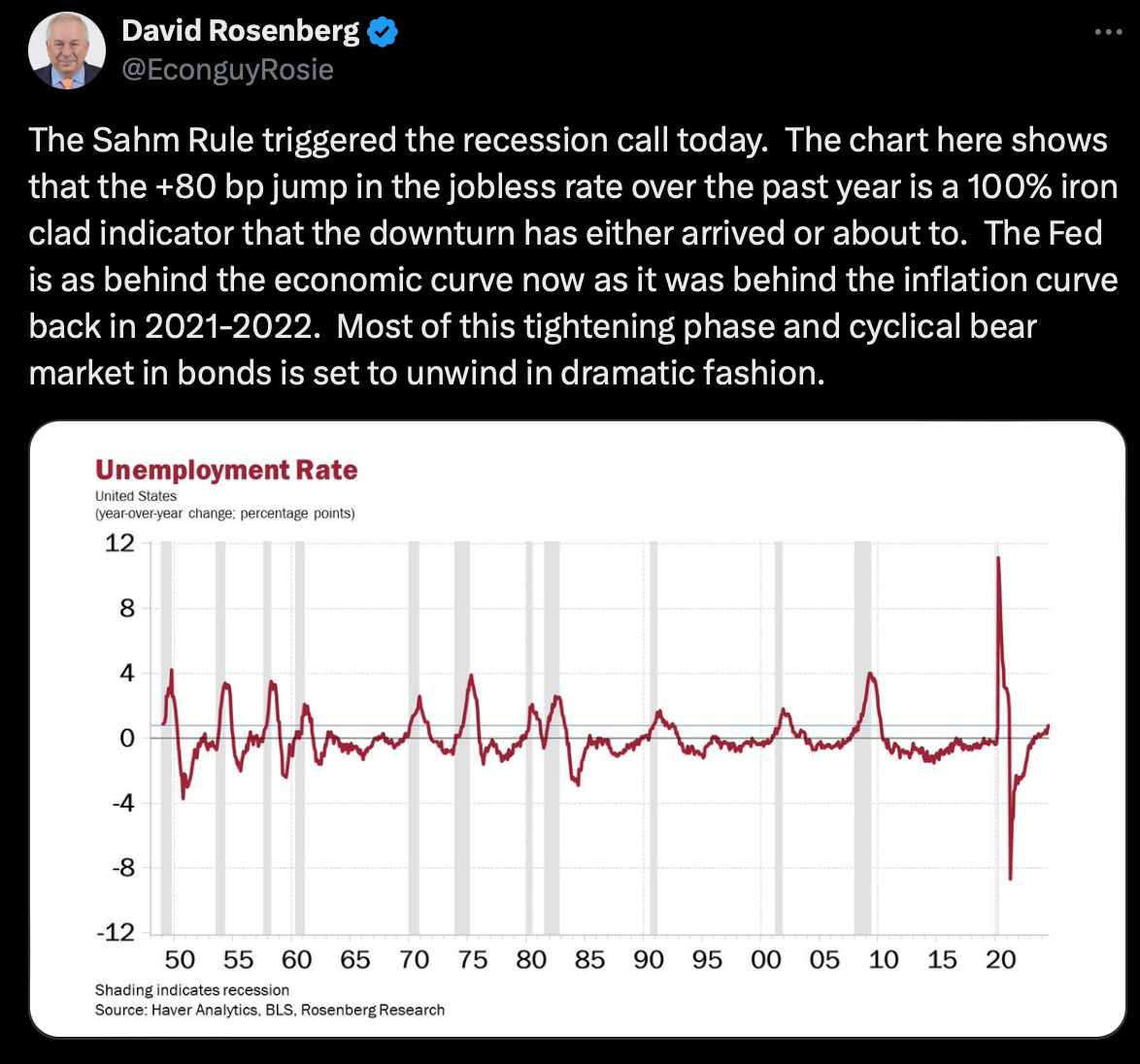

Some important observations from Rosie (David Rosenberg):

* Keep an eye on the credit market — high yield spreads gapped out an additional +16 basis points yesterday to 373 basis points (highest in eight months) and have widened +70 basis points in the past month.

* CCC-BB corporate spreads soared +30 basis points and are nearly up +230 basis points from the nearby lows to 8 percentage points for the first time since April 2023 — watch these “quality spreads” as they are typically canaries in the coal mine for other risk asset classes.

BY Doug Kass · Aug 6, 2024, 7:30 AM EDT

“I would like to see more volatility in the markets. Small shocks remind us that a bigger shock might occur. And, we protect ourselves to some extent.”

- Myron Scholes

Bonus — Here are some great links:

BY Doug Kass · Aug 6, 2024, 7:15 AM EDT

Investment short Chegg CHGG spit the bit again — making a new 52-week low (and -18% in premarket trading).

BY Doug Kass · Aug 6, 2024, 6:50 AM EDT

I went to sleep and the S&P futures were +67 handles.

I was very close to reshorting SPYs, but I wanted to watch the Olympics with "peace of mind."

They are now up by less than 20 handles.

As Grandma Koufax used to say, "Dougie, the only certainty in this market is that there is no certainty."

Especially in a leveraged financial system that has been underestimated by the business media, strategists and retai/institutionall investors.

Just look at the leveraged ETFs that typically are premarket leaders in volume (I highlight these daily for a reason!).

The movie is now in reverse (from leveraging to deleveraging).

Ten cuidado.

BY Doug Kass · Aug 6, 2024, 6:21 AM EDT

BY Doug Kass · Aug 6, 2024, 6:08 AM EDT