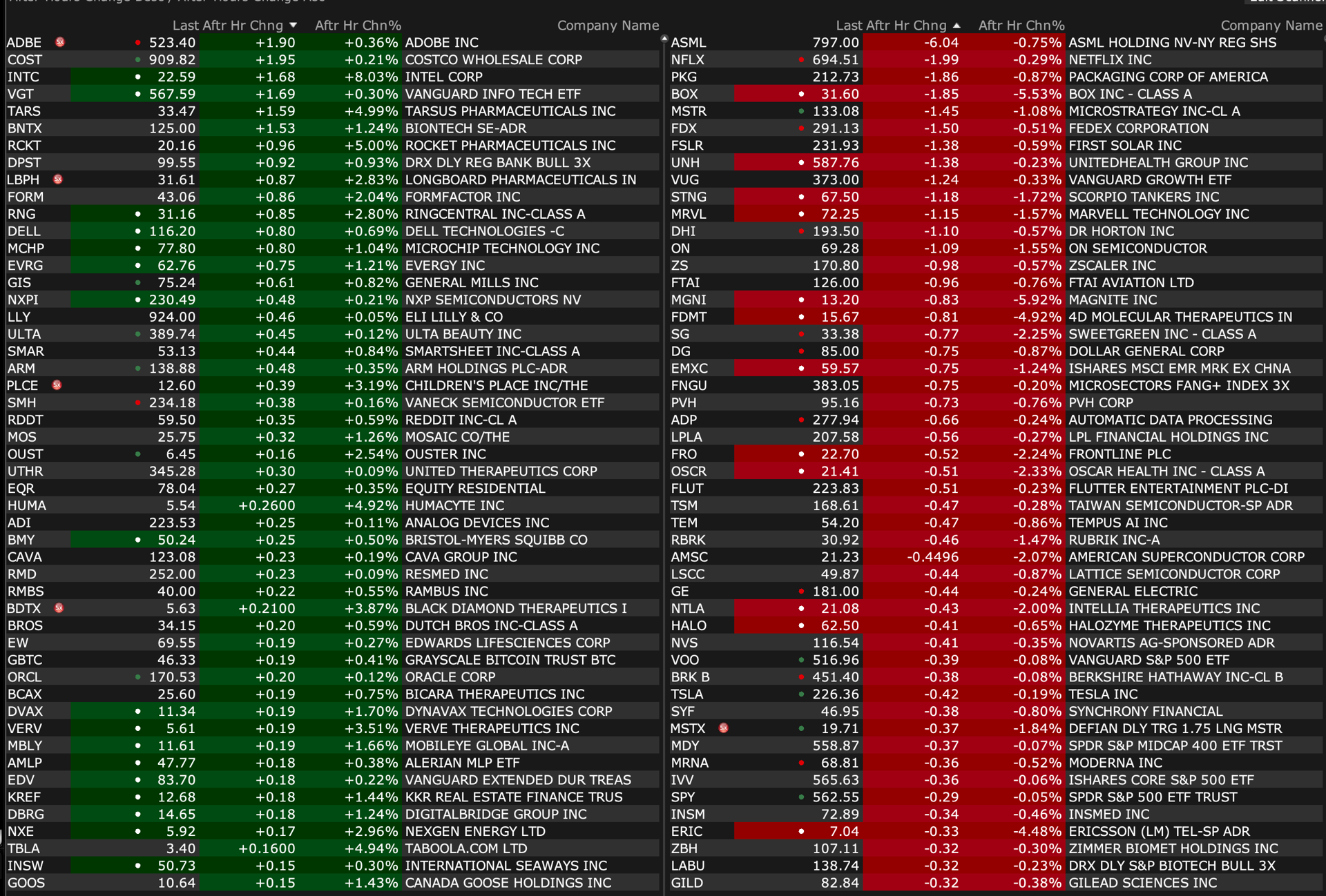

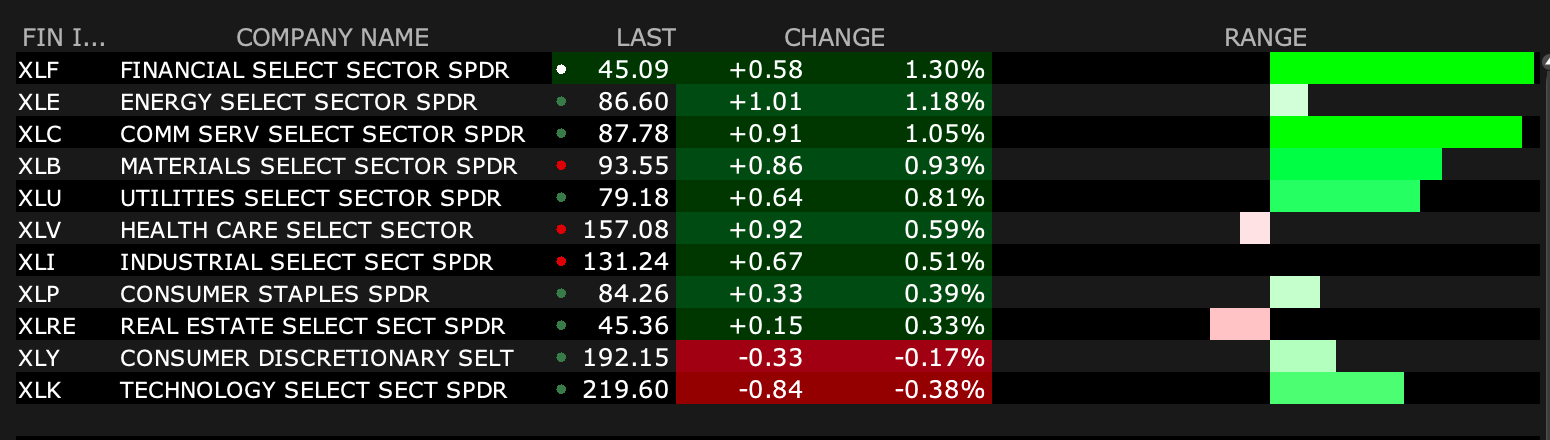

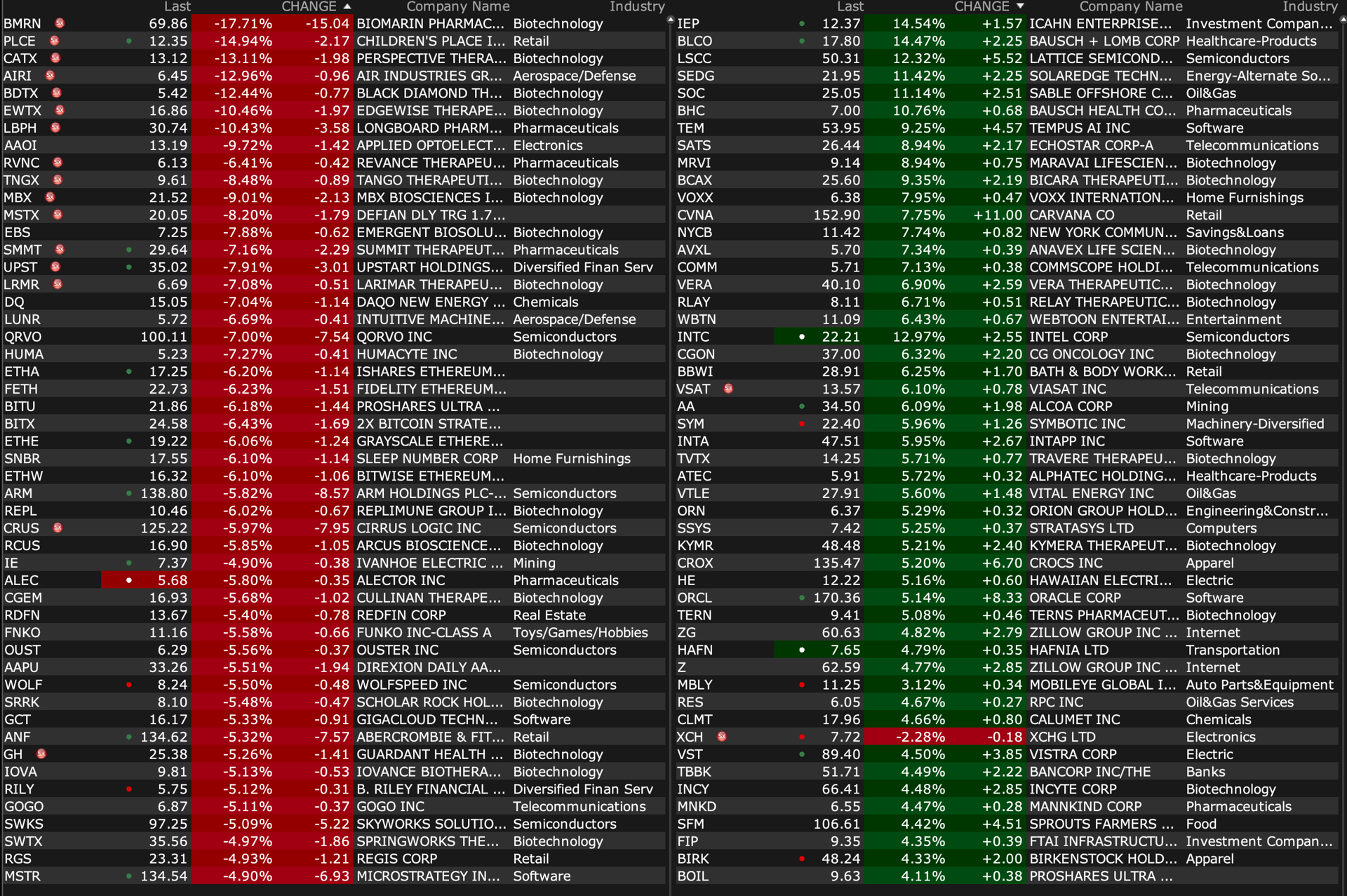

After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Sep 16, 2024, 5:20 PM EDT

As of 4:22 p.m.:

BY Doug Kass · Sep 16, 2024, 5:20 PM EDT

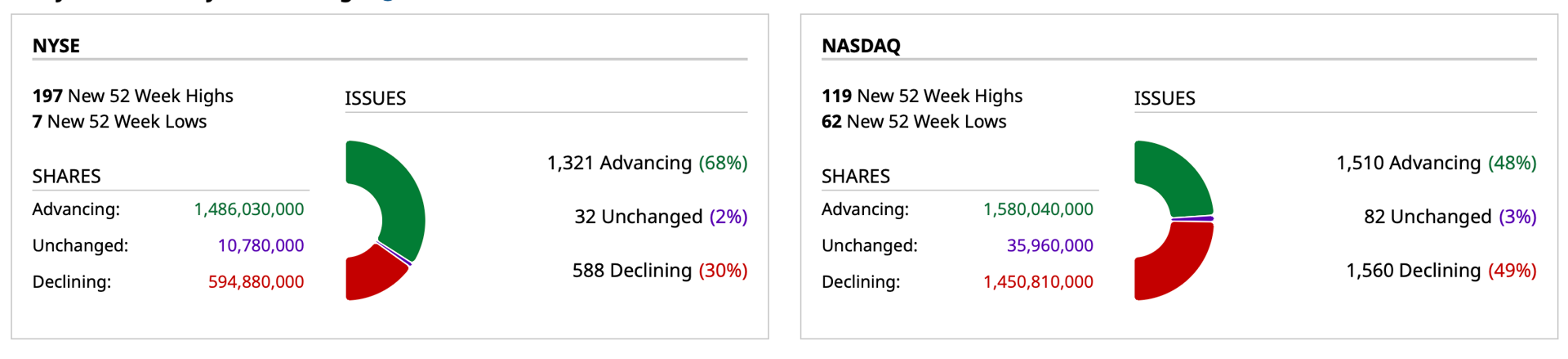

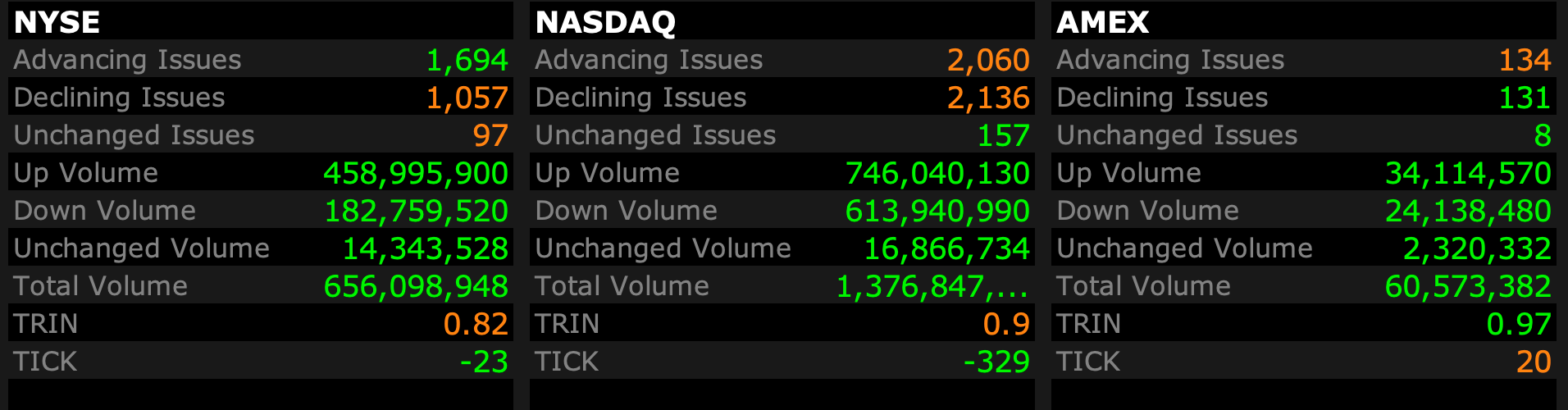

- NYSE volume flat to its one-month average.

- NASDAQ volume 11% below its one-month average.

- VIX up 3.62% to 17.16.

BY Doug Kass · Sep 16, 2024, 5:00 PM EDT

* But first my response!

TechNova asked an interesting question this afternoon.

I will give you my answer even before reposting his question (!):

I don’t know what is left of the carry trade but continued strength in yen and other currencies vs the US dollar could lead to foreign selling of US assets. It could also lead to a rebound in import prices and commodity prices if sustained.

So here is TN's question:

TechNova

Let's talk Japan:

It's interesting to me that nobody is talking about the Japan Carry Trade unwind anymore.

For the unwind to stop, the US cannot cut rates as cutting rates exacerbates the unwind.

If we cut rates soon, and at a rate of 50bps, thus furthering the unwind, will we not then see again a sell off in equities (although a bit more diminished than the first one)?

Which would play into the them that Markets tend to drop initially after large rate cuts start.

Am I missing something?

BY Doug Kass · Sep 16, 2024, 4:20 PM EDT

* For a change it was a quiet trading day and a narrow, range-bound market.

I came into the day small net long and ended the day the same in net exposure.

I was quiet on the trading/investing front — with very few trades:

* In premarket trading I added to a very small SPY ($562.55)/QQQ ($475.39) Later in the day, as the S&P Index rallied to about breakeven. I initiated a very small short call position in the Indices.

* I added to SLB long $40.07. Frankly I was disappointed in my energy holdings (save OIH, which was a standout at nearly +$5/share) after crude oil rose by about $1.50/barrel. That said, as I write this column the shares are beginning to rebound.

* I added to SBUX short at $98.41. Late last week the shares rose by about +$4 (after hitting recent lows) for no apparent reason.

* I shorted Apple AAPL in premarket trading.

* I was bidding for more cannabis equities, but my bid wasn't hit on any of the individual names.

Overall the market did well (with 50 minutes to go!), especially after the magnitude of the recent rally from the early September weakness. RSP (Equal weighted S&P ETF) was +0.70% at 3 p.m. after Friday's strong performance. Continued strength in bond prices were a favorable influence on certain sectors of the market.

BY Doug Kass · Sep 16, 2024, 3:36 PM EDT

I pressed some shorts throughout the rally from the lows this afternoon...

BY Doug Kass · Sep 16, 2024, 3:00 PM EDT

BY Doug Kass · Sep 16, 2024, 2:55 PM EDT

I added further to Schlumberger SLB at $40.07.

BY Doug Kass · Sep 16, 2024, 2:07 PM EDT

BY Doug Kass · Sep 16, 2024, 2:00 PM EDT

With S&P cash +1, I am adding on a scale (and slowly) to my SPY/QQQ short calls.

BY Doug Kass · Sep 16, 2024, 1:48 PM EDT

Polymarket sees an 83% probability of Amendment 3 passage in November.

BY Doug Kass · Sep 16, 2024, 1:35 PM EDT

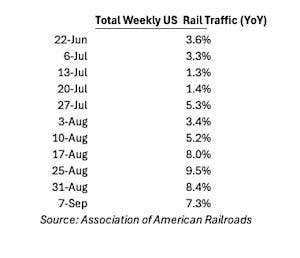

ChrisVersace

Dougie Kass (and others), wondering if you're coming to a similar thought that the rebound and strength in weekly railcar traffic pushes back on the hard landing narrative that seems to have goosed Fed rate cut expectations.

BY Doug Kass · Sep 16, 2024, 12:40 PM EDT

Back shorting some SPY and QQQ calls (for October and deep in the money).

BY Doug Kass · Sep 16, 2024, 12:25 PM EDT

Barron's featured Schlumberger SLB over the weekend.

BY Doug Kass · Sep 16, 2024, 11:05 AM EDT

At 10:30 a.m.

- NYSE volume 9% above its one-month average;

- NASDAQ volume 11% below its one-month average

- VIX up 5.80% to 17.52

BY Doug Kass · Sep 16, 2024, 10:49 AM EDT

Occidental Petroleum price target lowered to $71 from $74 at Morgan Stanley Morgan Stanley lowered the firm's price target on Occidental Petroleum to $71 from $74 and keeps an Overweight rating on the shares. In Q3, the energy group has lagged the market by 10% as softening oil prices, slowing inflation, and potential interest rate cuts "all present headwinds for performance," the analyst tells investors. In this backdrop, the firm remains selective and continues to prefer defensive sub-sector positioning among midstream and majors. Morgan Stanley favors gas over oil in exploration and production. It made price target and rating changes in the group after revisiting the setup across the North American energy sector.

Occidental Petroleum price target lowered to $72 from $76 at Mizuho Mizuho lowered the firm's price target on Occidental Petroleum to $72 from $76 and keeps a Neutral rating on the shares. The firm reduced its commodity price outlook for the second half of 2024 to 2027 and reduced net asset value-based price targets by 7% across the oil and gas exploration group. The analyst remains constructive on the U.S. oil and gas sector fundamentals despite lowering 2024 and 2025 EBITDA estimates. While growing macroeconomic fears, resilient U.S. demand, potential for resumption of OPEC+ production and delays on key projects have led to drops in oil prices over the last month, "micro" fundamentals for the sector remain strong with operating efficiencies improving, capital discipline holding and stocks offering above-market cash returns, the analyst tells investors in a research note.

BY Doug Kass · Sep 16, 2024, 10:25 AM EDT

I will be on a research call from 10 a.m. to 11 a.m.

Radio silence.

BY Doug Kass · Sep 16, 2024, 10:11 AM EDT

BY Doug Kass · Sep 16, 2024, 9:48 AM EDT

From Peter Boockvar:

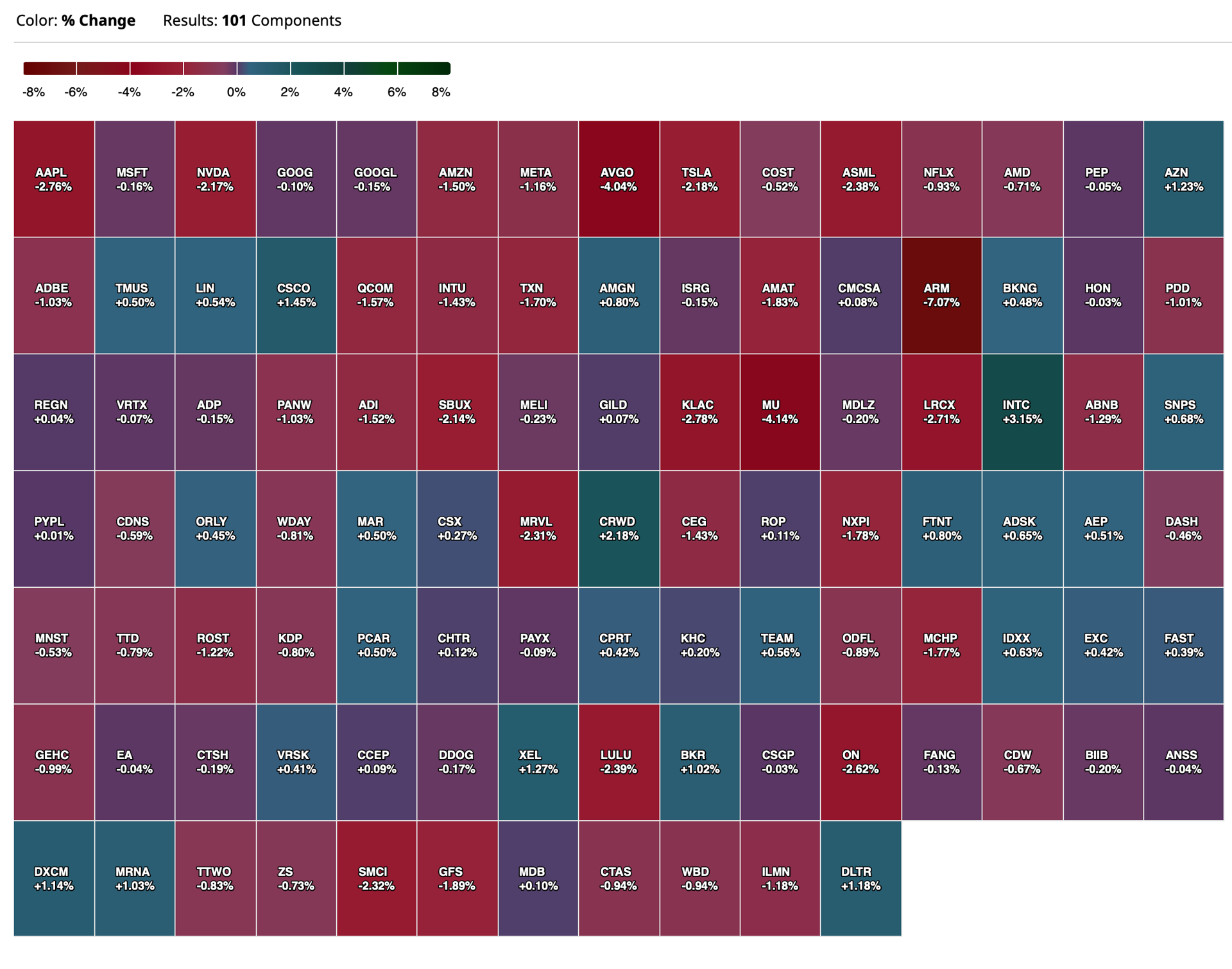

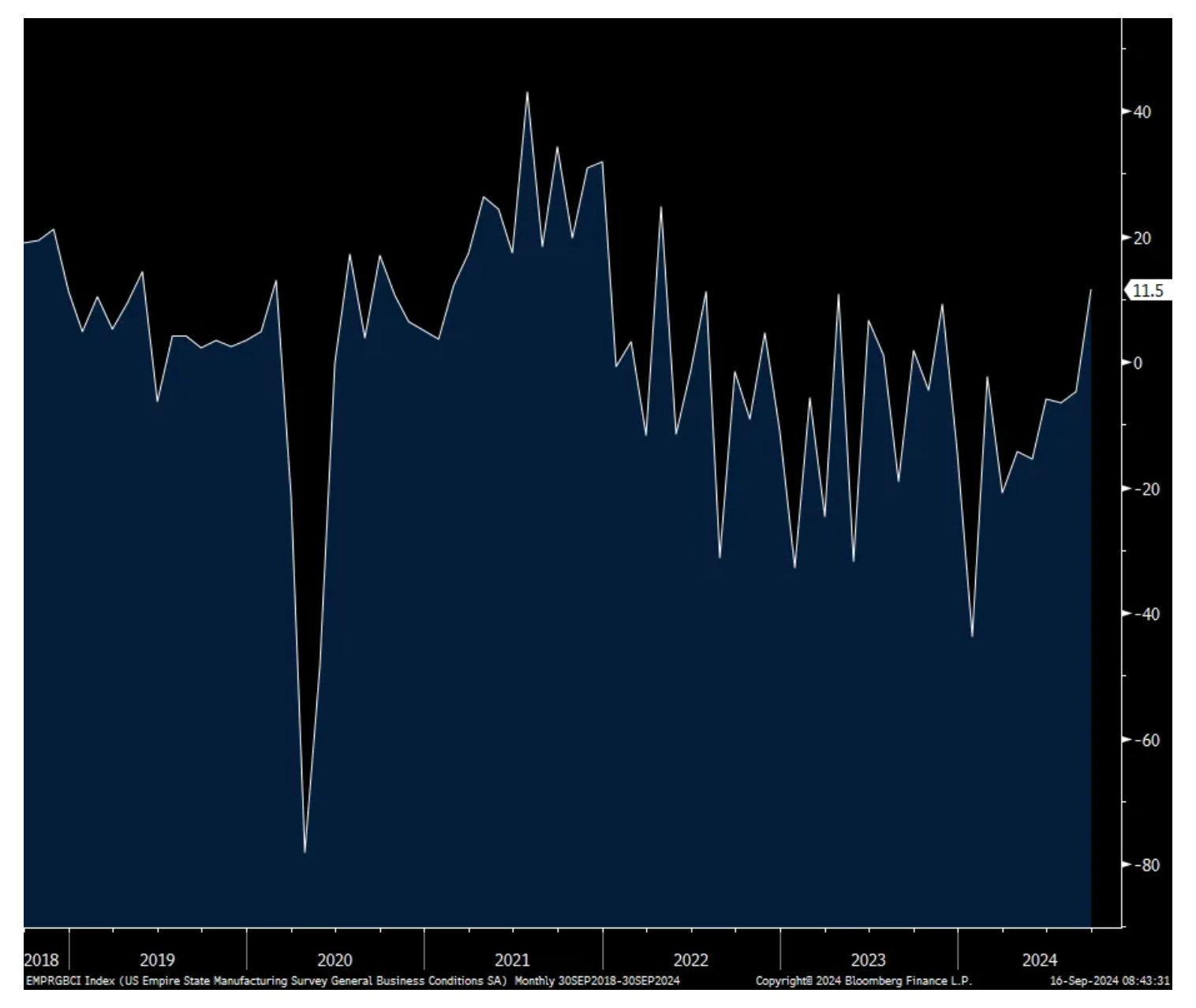

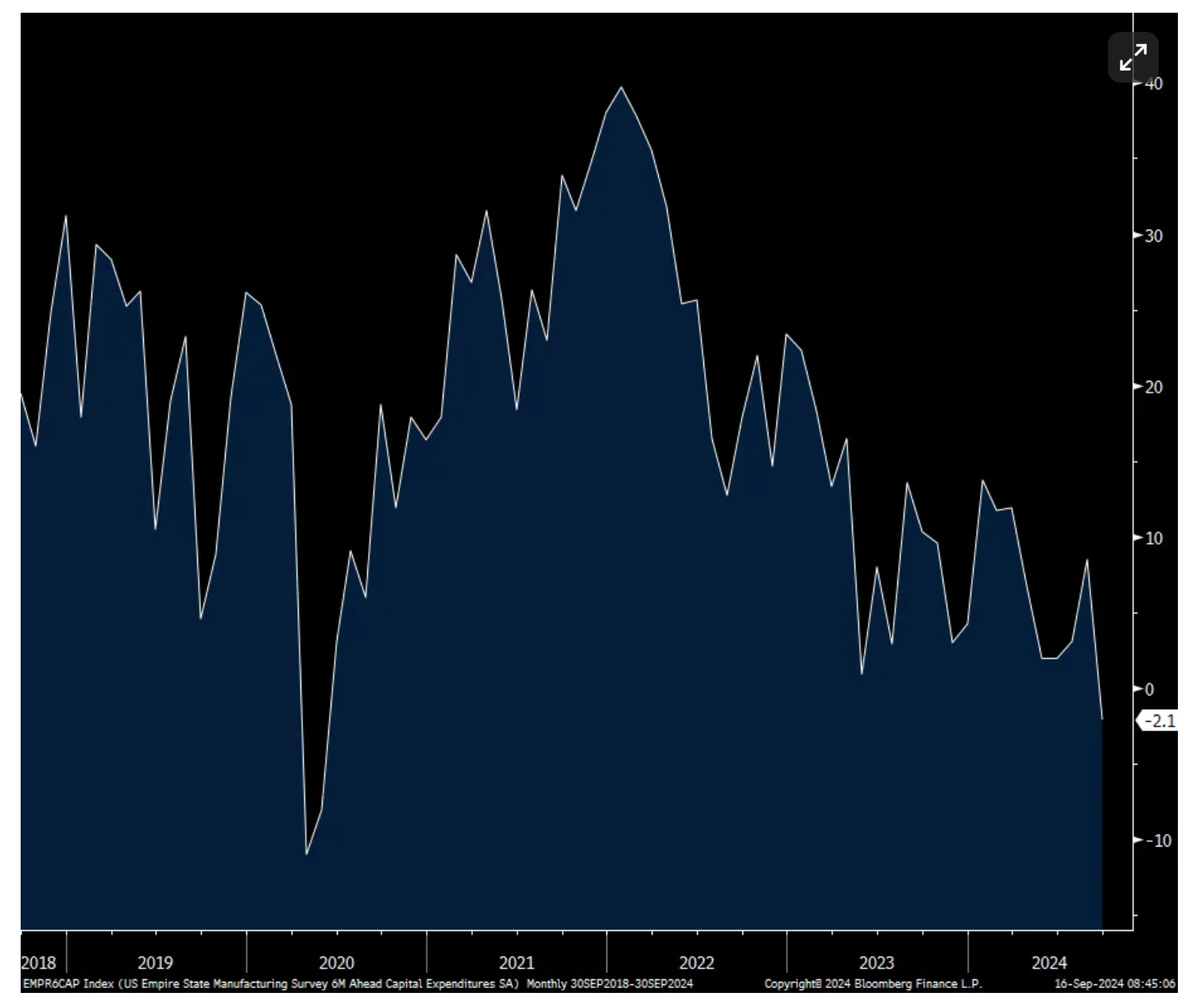

The September NY manufacturing index, the first September industrial number to be seen, surprised to the upside with a print of +11.5 versus -4.7 in August and versus the estimate of -4.0.

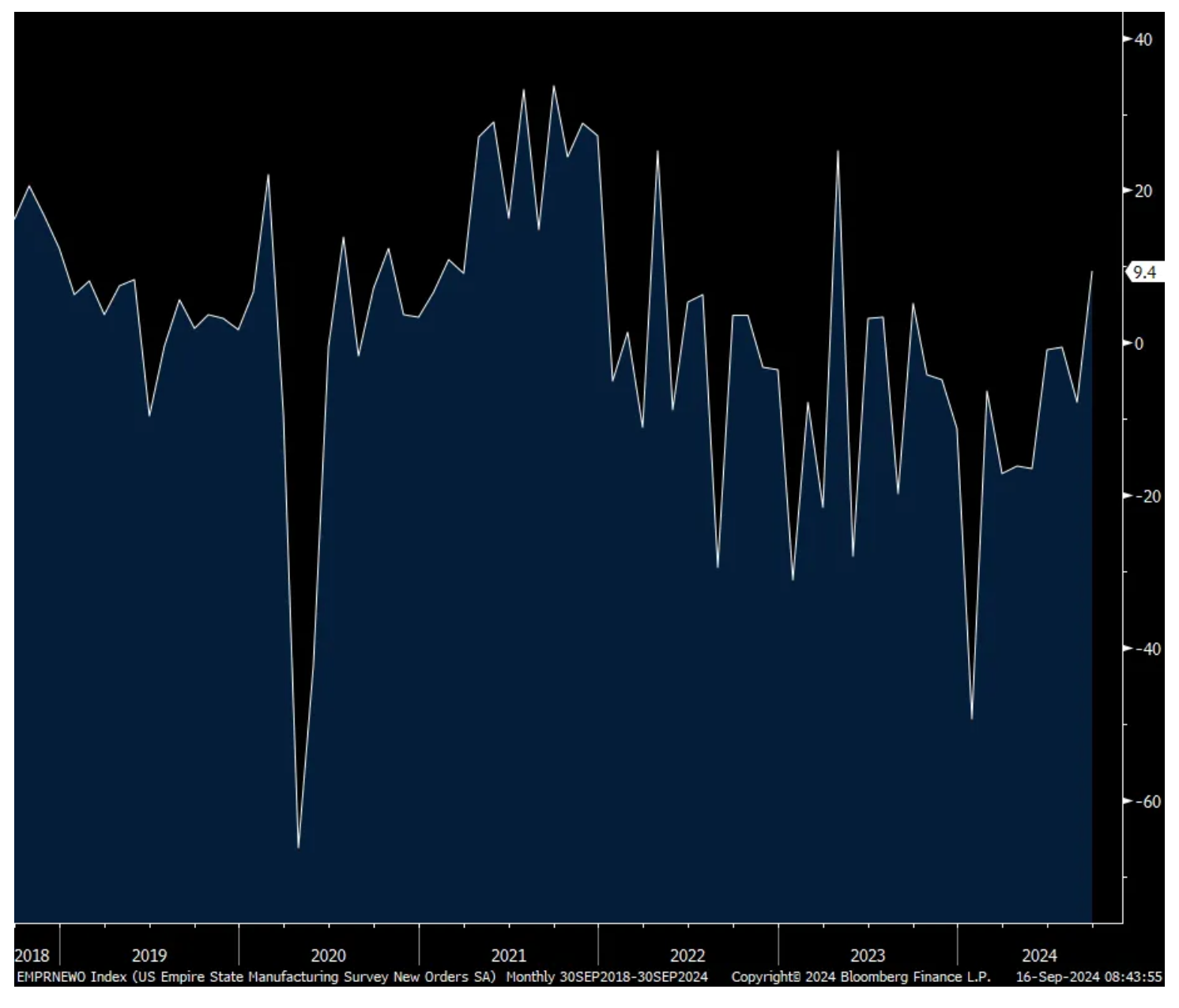

Keeping in mind the volatile nature of this data, new orders rebounded to +9.4 from -7.9 and versus -.6 in the month before and that led the way. Backlogs, too, got back above zero at 2.1 from -7.4. Inventories were exactly at zero and compares with the six-month average of -1.7. Prices paid and those received fell a touch month over month. Employment remained weak at -5.7 versus -6.7 in the month before. The workweek though did bounce to +2.9 from -17.8.

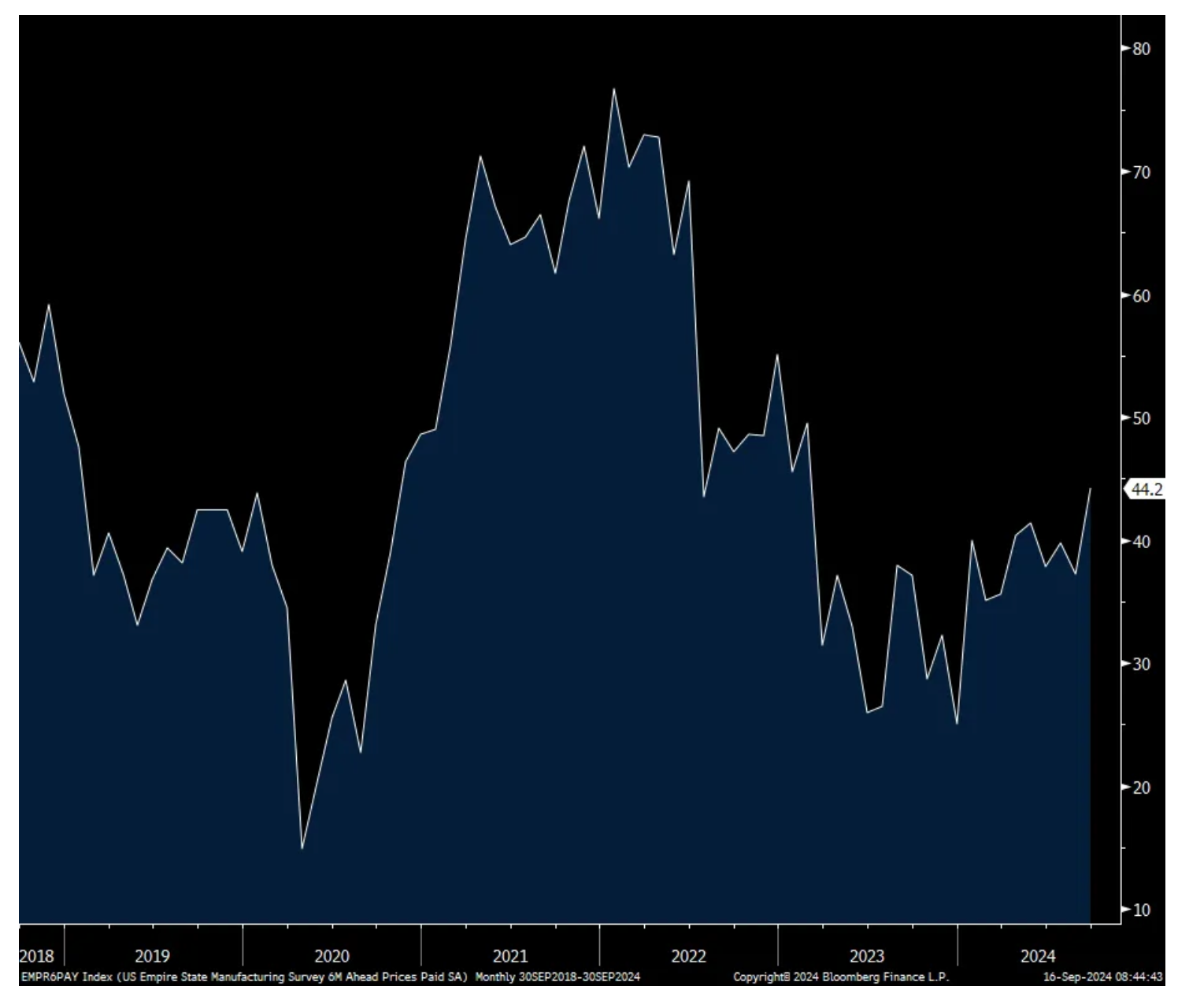

The six-month business outlook bounced too to 30.6 from 22.9 and that is the best since March 2022 (which ended up being badly wrong unfortunately at the time). Of note, the six0month outlook for prices paid rose to the highest since February 2023 and let’s hope they are wrong here, too. The negative was the expectation for a drop in capital spending as it went to -2.1 from +8.5 and that is the lowest since May 2020.

Bottom line, while always volatile month to month as stated, this is the best manufacturing read since April 2022, remembering this is measuring the direction, not degree, of sentiment. As end consumer demand remains very squishy and uncertain, I’m guessing this is more to do with hopes for some inventory replenishment. That said, we’ll need to see more regional surveys to draw any definitive conclusions. The treasury market is waiting too as it didn’t respond to the upside surprise, as it rarely does with this data point and is more focused on the Fed right now.

NY Manufacturing:

New Orders:

Prices Paid Six-Month Outlook:

Capital Spending Six-Month Outlook:

BY Doug Kass · Sep 16, 2024, 9:37 AM EDT

Chart from 8:39 a.m ET.

BY Doug Kass · Sep 16, 2024, 9:25 AM EDT

Upside:

-ZNTL +37% (FDA lifts hold on Azenosertib Studies; on track to present data from key clinical studies of Azenosertib in Q4)

-APVO +34% (Aptevo Therapeutics and Alligator Bioscience announce data from Phase 1 ALG.APV-527 Monotherapy Trial showing 60% of evaluable patients achieved stable disease in solid tumor study)

-VRAX +30% (announces extension of existing Exclusive Distribution Agreement to market Mpox Virus Real-Time PCR Detection Kits with Cosmos Health for GCC countries)

-ASND +20% (announces topline data from the pivotal double-blind placebo-controlled ApproaCH Trial of TransCon CNP (navepegritide), which included 84 children with achondroplasia)

-BLCO +20% (reportedly has hired advisers to consider a sale to end its messy spin off from its indebted parent company)

-REE +9.0% (announces Global Manufacturing Agreement with leading automotive supplier Motherson Group making strategic investment in a $45.4M registered direct offering led by M&G)

-SATS +6.7% (reportedly AT&T and JV partner TPG Inc. are in talks to combine their DirecTV service with Dish)

-COSM +5.1% (secures Exclusivity Agreement with Virax Biolabs to Distribute mpox PCR Kits across the GCC, including the UAE, Saudi Arabia, Bahrain, Kuwait, Oman, and Qatar)

-GTLS +3.8% (Morgan Stanley Raised GTLS to Overweight from Equal Weight, price target: $175)

-ZG +3.6% (Wedbush, Inc. Raised ZG to Outperform from Neutral, price target: $80)

-RLAY +3.0% (hearing positive comments from Stifel)

-BLDR +2.6% (Truist Raised BLDR to Buy from Hold, price target: $220)

Downside:

-SBT -9.4% (sells Sterling Bank and Trust, F.S.B. to EverBank Financial Corp for $261M in cash; announces Adoption of Plan of Dissolution)

-BMRN -9.3% (lower in sympathy with ASND)

-MU -3.4% (Tier1 firm Reiterates MU with Buy, cuts price target: $110 from $170)

-AAPL -2.5% (Tier1 analysts citing early pre-order data for iPhone 16)

-LTRX -2.5% (CFO Jeremy Whitaker resigns, effective immediately)

-MOS -2.4% (potash and phosphate operations sustained operational challenges that are expected to reduce production volumes and shipments in Q3 2024 by 200-300K tons)

-ALOT -2.0% (earnings, guidance)

-APO -2.0% (confirms to purchase ~$1.0B non-controlling stake in bp Pipelines TAP Limited)

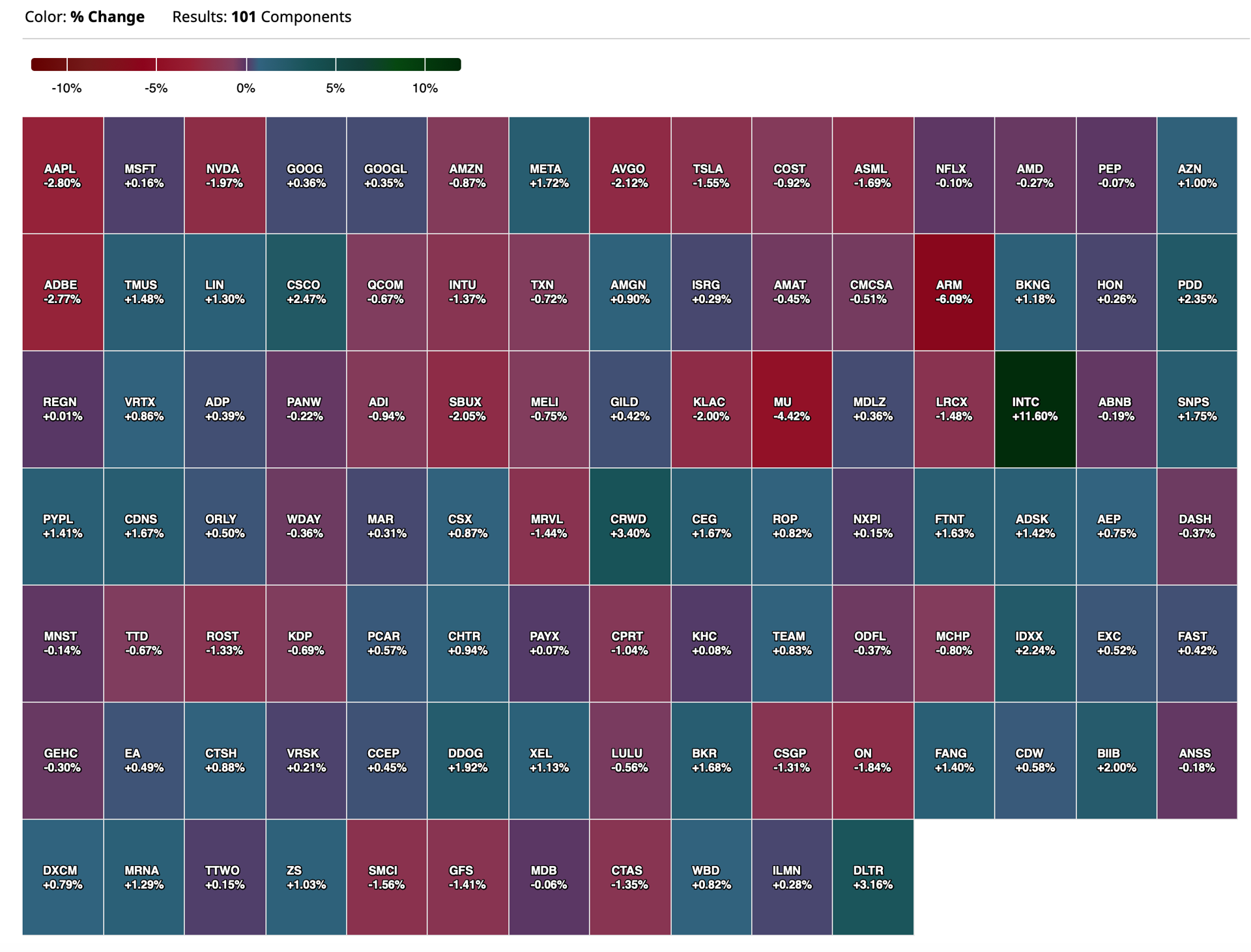

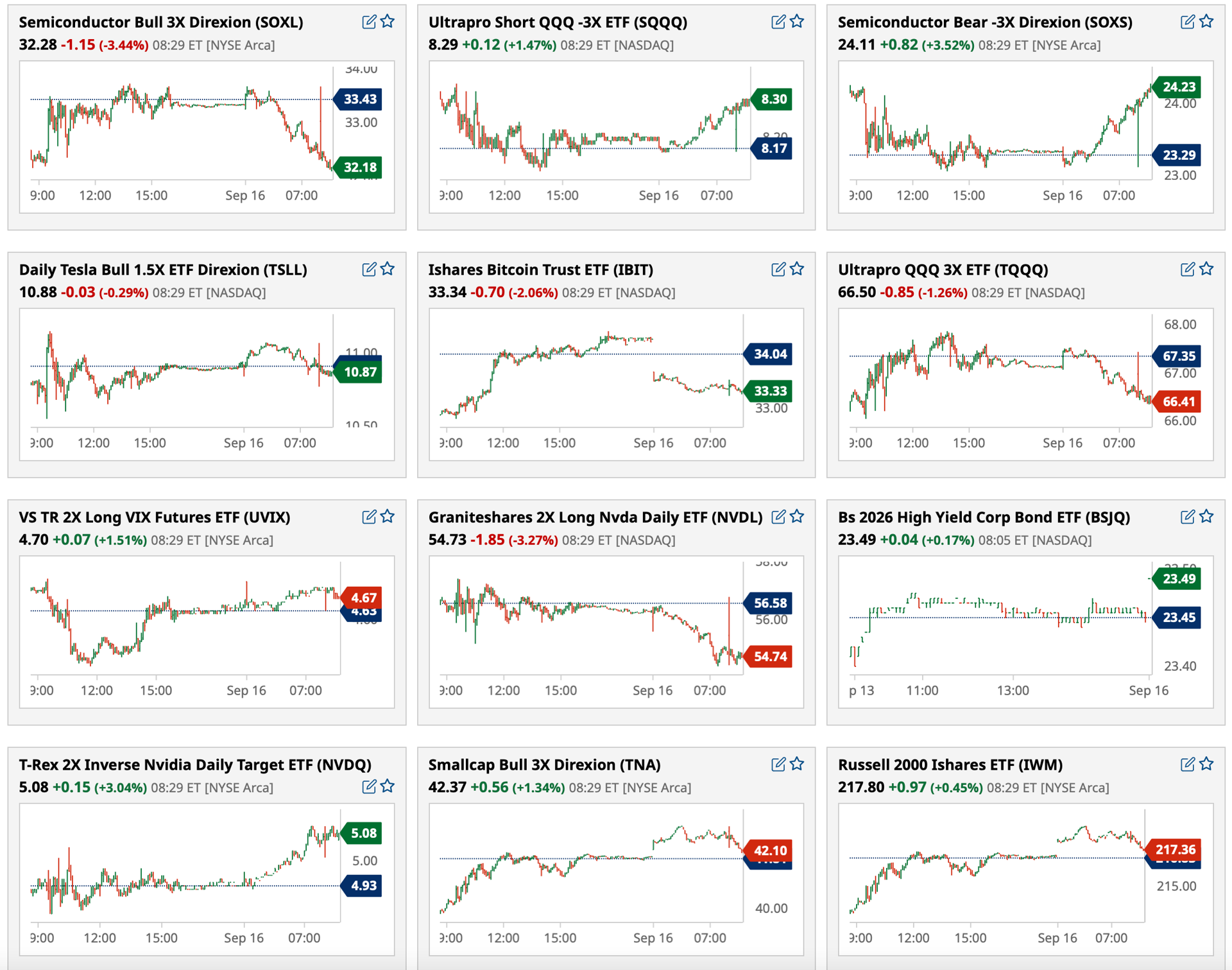

BY Doug Kass · Sep 16, 2024, 9:17 AM EDT

Chart from 8:55 a.m. ET:

BY Doug Kass · Sep 16, 2024, 9:10 AM EDT

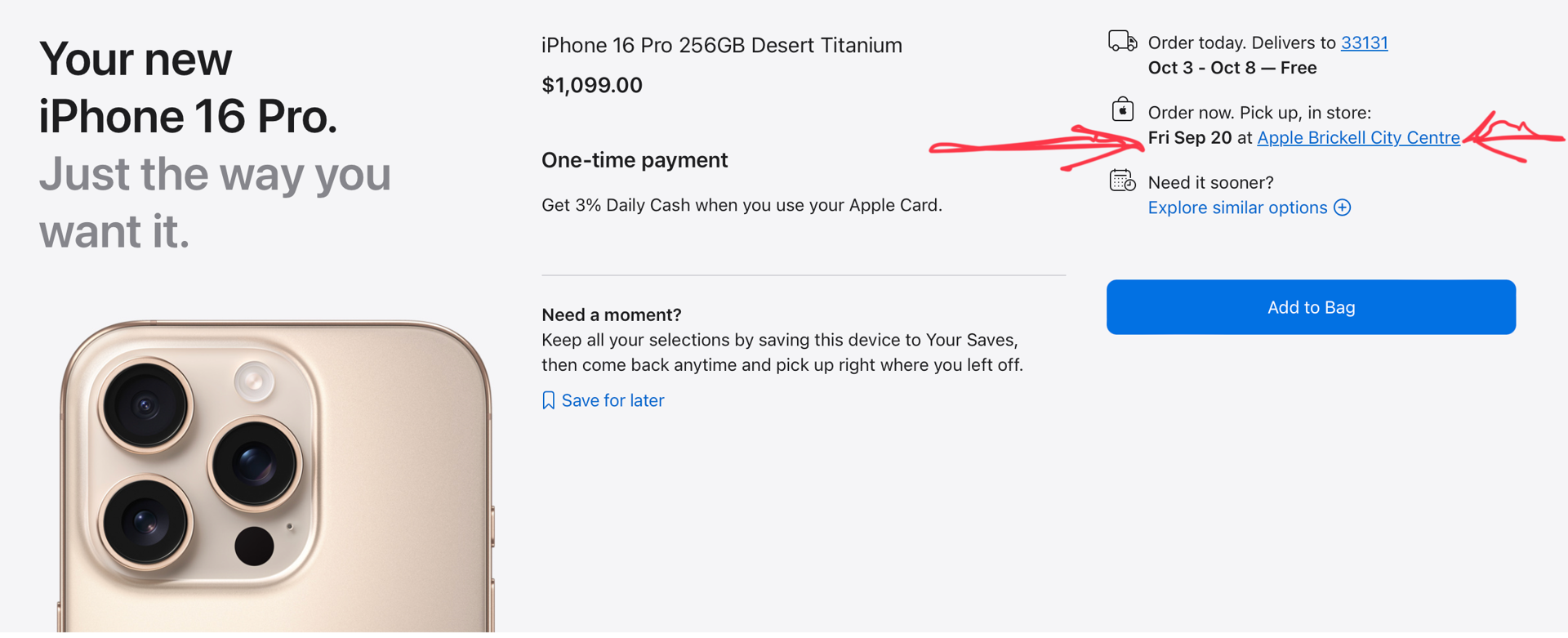

* Consistent with my previous comments on early demand metrics....

* Order now and pick up on Friday!

I went on the Apple website and inquired about iPhone 16 availability:

BY Doug Kass · Sep 16, 2024, 9:00 AM EDT

I am adding to my SBUX short in the premarket at $98.41.

BY Doug Kass · Sep 16, 2024, 8:43 AM EDT

BY Doug Kass · Sep 16, 2024, 8:34 AM EDT

From Peter Boockvar:

The debate here on the Fed doesn't have to be binary. It's not 25 or 50 bps in cuts, take it or leave it. I say that because the signaling by Jay Powell in the press conference will likely be just as important. For example, the Fed might cut 25 bps but maybe Powell says they will be ready to cut 50 bps at one of the following few meetings if the data warrants it. Or, they might cut 50 bps but Powell will say don't get used to that cadence and they were more interested in front loading the first cut, thus implying only 25 bps cuts come next. Bottom line, what they announce at 2pm est Wednesday could be enhanced or blunted by what Powell says at 2:30pm.

If my chips were on the table, I'd say Powell does the latter and goes 50 bps but warns markets (in his own way) that for now this is a rate 'tweaking' cycle, not the beginning of something pronounced that the market is currently pricing in. The reality of circumstances can of course change that as events unfold but that's how I think he'll stage it at least on Wednesday.

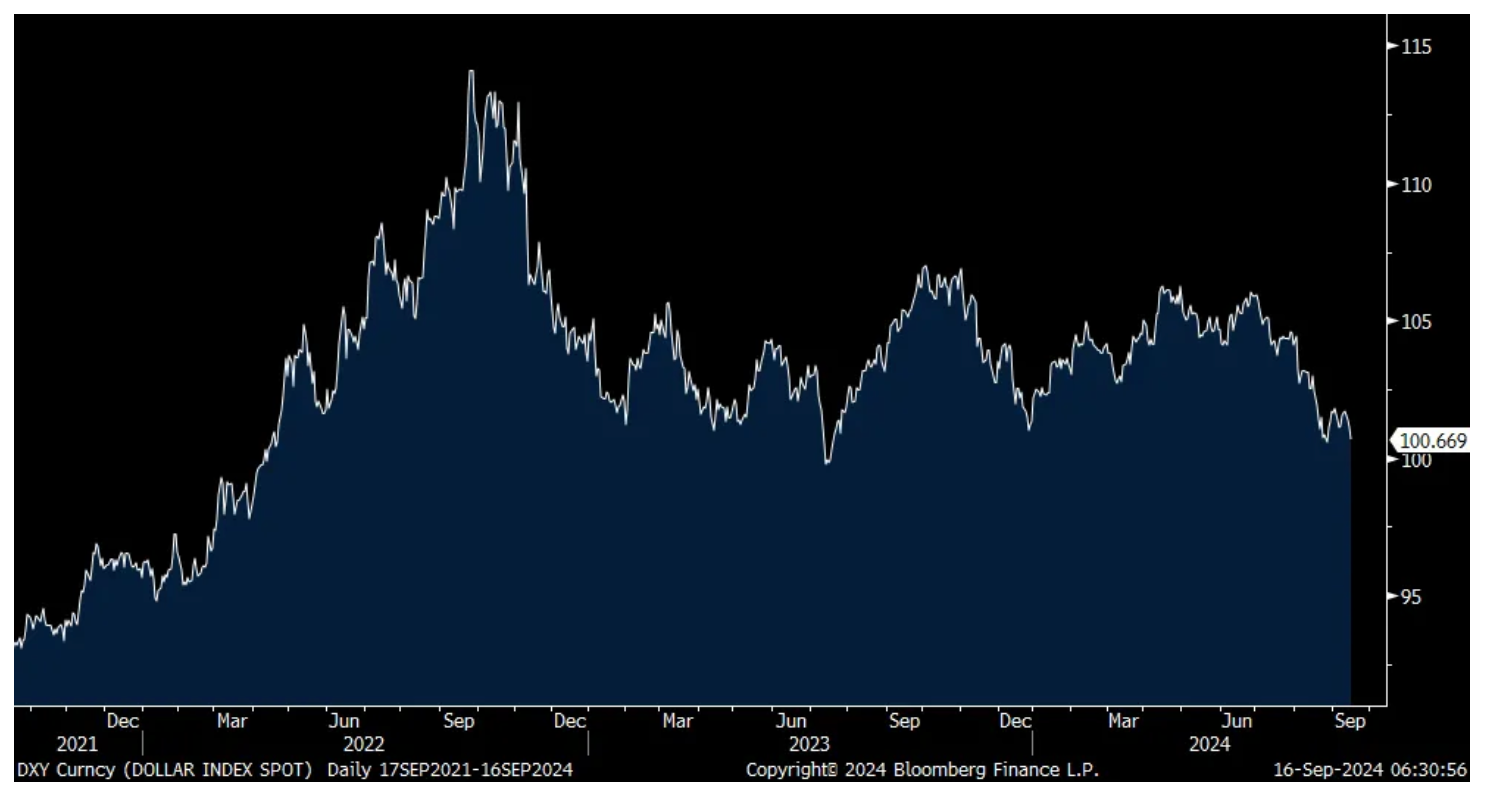

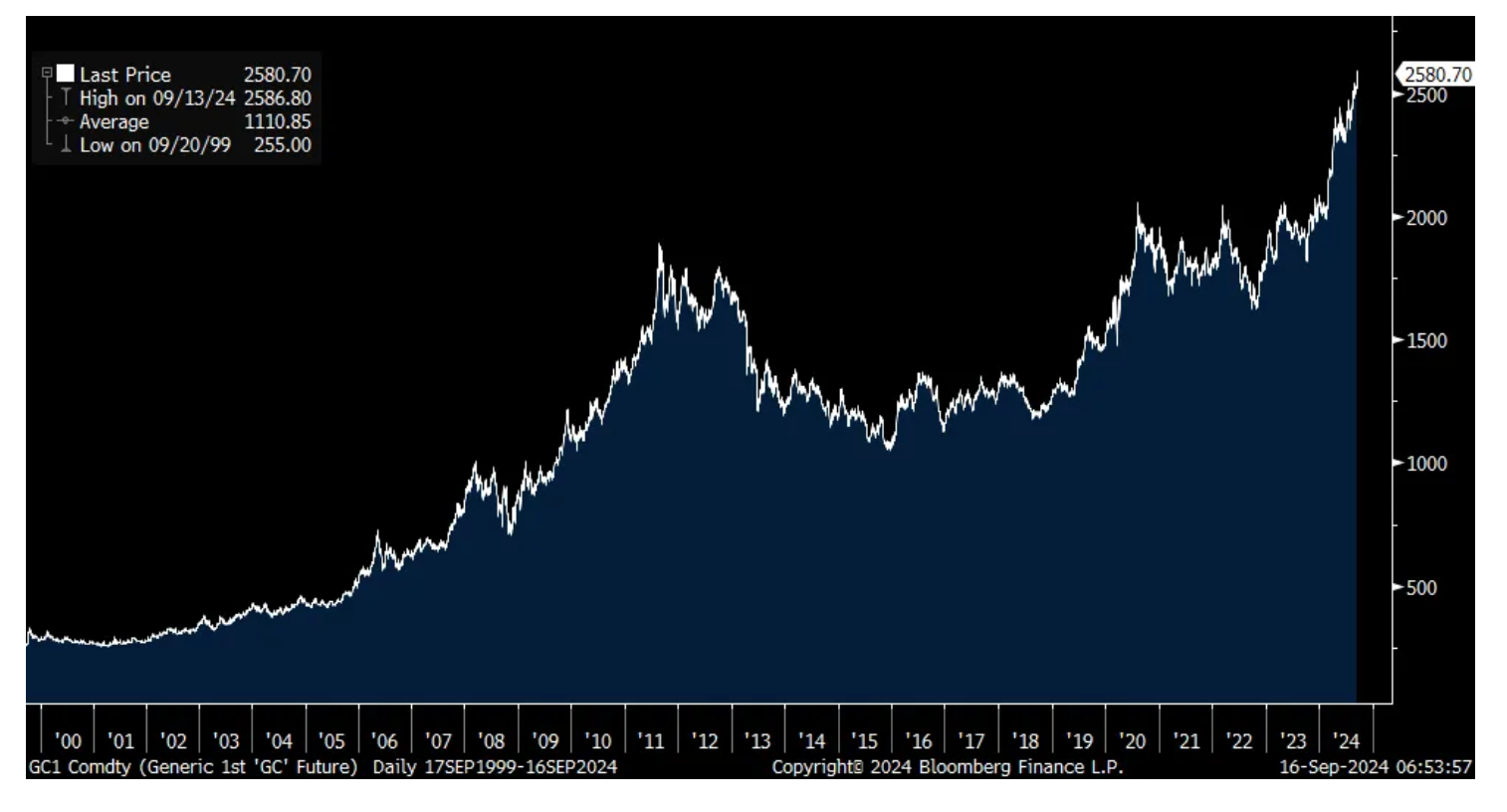

Ahead of the meeting, the euro/yen heavy US dollar index is knocking on 100 again as it retests the last August lows. If it breaks below 100, go back to July 2023 the last time it did and if it closes below 99.77, go back to April 2022 the last time it was weaker. Yes, the Fed is about to start cutting interest rates, helping to explain some of the weakness. I say 'some' because other central banks, outside of the BoJ, are cutting too and just maybe there is something else going on. Like worries about US debts and deficits reaching a point of no return. We'll see but the ever rising price of gold is quite the sign that something is up, particularly with foreign central bank desires to diversify away from their holdings of the US dollar and into other things like that shiny yellow metal.

DXY

Gold over the past 25 years

One thing helping the euro today was the Peter Kazimir comments today, a Governing Council member of the ECB. "We will almost surely need to wait until December for a clearer picture before making our next move. I would require a significant shift, a powerful signal, concerning the outlook to consider backing another cut in October. But the fact is that very little new information is in the pipeline...Last week's decision definitely doesn't mean we're on a path to cut rates every time we meet. We stay open minded, but from my perspective, there is still more risk that inflation will be higher over the medium term than we currently project." He is typically on the hawkish side of the spectrum.

The China growth worries continue as on late Friday est time they reported a continuation of falling home prices in August and data misses with retail sales, industrial production, fixed asset investment and property investment. The jobless rate also ticked up by one tenth to 5.3%. Notwithstanding this, the yuan is higher and the Hang Seng closed up by .3% as other Chinese markets were closed as they were in some other Asian markets. Weakness in the Chinese economy is no longer new news and hasn't been for a while.

BY Doug Kass · Sep 16, 2024, 8:17 AM EDT

From Green Thumb's CEO:

BY Doug Kass · Sep 16, 2024, 8:00 AM EDT

Green Thumb announces a $50 million share buyback this morning: "Green Thumb Industries Announces $50 Million Share" (globenewswire.com)

GTBIF is my largest individual equity holding in the cannabis space.

BY Doug Kass · Sep 16, 2024, 7:45 AM EDT

BY Doug Kass · Sep 16, 2024, 7:28 AM EDT

From Ming-Chi Kuo, the negative TF International Securities analyst on Apple AAPL:

* First Weekend pre-order sales: estimated based on each model’s delivery time and production plans for that period.

* Average delivery time: results from Apple’s official websites in major iPhone markets 48 hours after pre-orders opened.

* Shipments before pre-order: Production volume before pre-orders.

His specific analysis and conclusions:

1. iPhone 16 series first-weekend pre-order sales are estimated at about 37 million units, down about 12.7% YoY from last year’s iPhone 15 series first-weekend sales. The key factor is the lower-than-expected demand for the iPhone 16 Pro series.

2. The delivery times of the iPhone 16 Pro series are significantly shorter than those of the 15 Pro series. In addition to the shipment increase before the pre-order, the key is that demand is lower than expected, as evidenced by the YoY decline in first-weekend sales.

3. The significant YoY growth in shipments before pre-order for iPhone 16 Pro Max is due to improved tetraprism camera production yields and Apple’s optimistic outlook for demand for this model.

4. One of the key factors for the lower-than-expected demand for the iPhone 16 Pro series is that the major selling point, Apple Intelligence, is not available at launch alongside the iPhone 16 release. Additionally, intense competition in the Chinese market continues to impact iPhone demand.

5. While first-weekend sales of the iPhone 16 Plus and standard version were up YoY, their impact on total iPhone shipments is limited.

6. Despite the YoY decline in first-weekend pre-order sales of the iPhone 16 Pro series, the supply chain’s production plans are unlikely to change significantly in the near term. Apple still has opportunities to improve sales through the release of Apple Intelligence and peak season promotions (year-end holiday season in America and Europe and Double 11 in China). These factors will be key points to watch for changes in iPhone demand.

7. Strategies such as adding a tetraprism camera to the 16 Pro and maintaining iPhone 16 series pricing have had a limited help to iPhone 16 first-weekend pre-order sales. Suppose Apple Intelligence releases in 4Q24 and peak season promotions have a limited effect on iPhone 16 shipments. In that case, I believe that Apple will implement more aggressive iPhone product strategies in 2025 to stimulate market demand.

BY Doug Kass · Sep 16, 2024, 7:11 AM EDT

Newly released tapes indicate President Nixon dud not think cannabis was "particularly dangerous":

BY Doug Kass · Sep 16, 2024, 7:05 AM EDT

Bonus - Here are some great links:

BY Doug Kass · Sep 16, 2024, 6:50 AM EDT

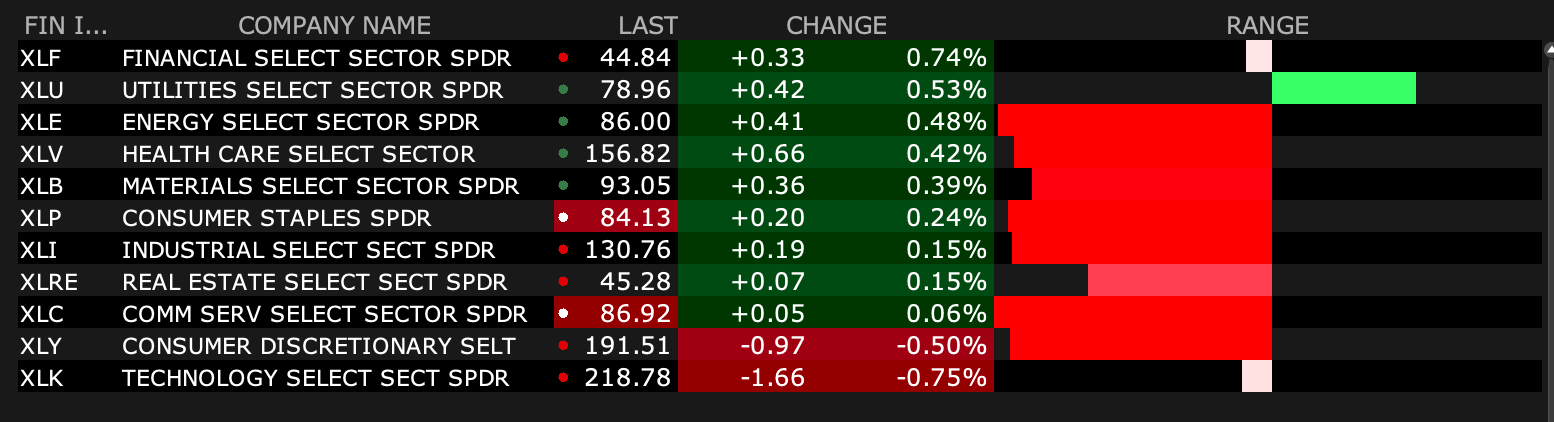

Into extreme sector weakness:

I substantially increased my long exposure to energy stocks late last week:

BY Doug Kass · Sep 16, 2024, 6:40 AM EDT

A prominent analyst in Asia is saying that the company's 16 launch is underwhelming so far.

BY Doug Kass · Sep 16, 2024, 6:30 AM EDT

This is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Sep 16, 2024, 6:27 AM EDT

From JPMorgan:

US: Futs are up small-caps outperforming, following a trend from late last week. Pre-mkt, Mag7 names are mixed with Semis lagging; let’s see if last week’s bid returns. Bond yields are down as the curve bull steepens, pressuring USD. Cmdtys are higher with Energy and Metals boosting the index. Today is a light macro day ahead of tmrw’s Retail Sales and Weds’ Fed Mtg where the market remains split on 25 or 50bps.

and...

EQUITY AND MACRO NARRATIVE: What a difference a week makes! After the worst performing week of the year for SPX, it follows that up with the best performing week of the year, +4.0%. Both NDX and RTY outperformed, adding 5.9% and 4.4% respectively, as we saw a combination of the resumption of the AI/Mag7 trade and Cyclicals/Value as part of a broadening rally; proponents of the barbell trade were rewarded with 10 of 11 sectors higher. Energy Equities were down WoW despite WTI rebounding 1.5%, or $0.98. This performance occurred against a backdrop of still declining inflation which, according to Blackstone’s CFO, is already below the Fed’s target (he sees 1.7% headline inflation if shelter components are marked-to-market vs. 2.5% official print). Further, rate cut bets of 50bps increased with the market now pricing in 37bps of cuts this week helping the yield curve bull steepen, which was supportive of the outperformance of Cyclicals/Value. The USD has fallen in 9 of the last 11 weeks, which has fueled demand for EM Equities.

This week, the two biggest questions is what does the beginning of the easing cycle means for the economy & risk assets and whether we see a return of negative seasonality. The key may be in Retail Sales rather than the Fed decision; the balance of this note is focused on understanding why that is the case and the various outcomes. From a seasonality perspective, if we are right on the economy then would buy any dips due to seasonality. In terms of monetization, we like the barbell trade but with a tilt towards the Cyclicals/Value side of the barbell.

BY Doug Kass · Sep 16, 2024, 6:17 AM EDT

I have expanded my short hedges modestly in premarket trading (but still remain small-sized):

* SPY $562.55

* QQQ $475.39

BY Doug Kass · Sep 16, 2024, 6:07 AM EDT

* Vote Yes on Amendment 3 Florida Amendment 3, Marijuana Legalization Initiative (2024) - Ballotpedia

BY Doug Kass · Sep 16, 2024, 6:02 AM EDT

BY Doug Kass · Sep 16, 2024, 5:54 AM EDT