Peter Boockvar's succinct summary of the week’s events:

Positives,

1)While I do believe reasons are adding up for a move lower in interest rates, I also understand Powell’s reticence to commit yet as sustainability of lower inflation is what he needs next.

2)The May CPI was flat headline and higher by .2% core, both one tenth below expectations. This brings the y/o/y change to 3.3% and 3.4% respectively from 3.4% and 3.6% in April.

3)Wholesale prices in May surprised to the downside with a .2% drop vs the estimate of up .1%. The core rate saw no change m/o/m vs the estimate of up .3%. The y/o/y increases slowed a touch to 2.2% and 2.3% respectively vs 2.3% and 2.5% in April.

4)After jumping in April, import prices fell in May, leaving the y/o/y change not much changed. The headline fall was .4% vs the April rise of .9%. The estimate was for a one tenth drop. Ex petro saw a 3 tenths fall after rising by 6 tenths last month. The estimate was for another .2% rise. Versus last year, headline import prices are up 1.1% and was up just .1% ex food and fuel.

5)In the Fed’s NY Consumer Expectations survey: "Perceptions about households' current financial situations improved, with more respondents reporting being better off than a year ago and fewer respondents reporting being worse off. Year ahead expectations also improved."

6)While mortgage rates didn't move much w/o/w, down 5 bps, refi's exploded higher by 28.4% w/o/w. Again, assume most are cash outs. After falling in 10 out of the last 12 weeks, purchase applications rebounded by 8.6% w/o/w.

7)The May NFIB Small Business Optimism index rose to 90.5 from 89.7. While still well below the 50 yr average of 98 and bouncing along 10 yr+ lows, that is the best read since it was at 91.9 in December. The 6 month average is 90. The internals were very mixed. Notwithstanding the modest lift in confidence, the bottom line from the chief economist at the NFIB was still downbeat. Highlighting the small business sector contribution to GDP and employment of over 40%, "for 29 consecutive months, small business owners have expressed historically low optimism and their views about future business conditions are at the worst levels seen in 50 years. Small business owners need relief as inflation has not eased much on Main Street."

8)From Casey’s General Store: "we're seeing pretty consistent behavior with the upper income consumers. They're continuing to buy as they normally have.

9)Broadcom’s AI party continues, Oracle celebrated too.

10)The Bank of Taiwan and Bank of Thailand each left rates unchanged as expected.

11)China's inflation data, both CPI and PPI were about as expected. The former saw a .6% rise y/o/y ex food and energy, staying on trend and reflecting actual price stability. PPI decline of 1.4% was the slowest decline since February 2023 in part due to the comp of -4.6% in May 2023.

12)In the UK in April its economy was flat from March which was one tenth better than anticipated. Again, services outperformed manufacturing and the industrial side of their economy.

13)The Eurozone June Sentix Investor Confidence index rose back to positive territory at .3, a bit better than the estimate of -1.7. Sentix said the internals were mixed as the current situation was -9, "while the expectations component rose by 2.2 pts to +10 pts."

14)Congratulations to Tom Brady for your entrance into the New England Patriots Hall of Fame and thanks for this very motivational speech for many, particularly my son. Wise words indeed,

Negatives,

1)Initial jobless claims popped to 242k which was much greater than the estimate of 225k and up from 229k last week. That’s the biggest one week count of unemployment benefit filers since August 2023 and puts the 4 week average at 227k from 222k, the highest since September 2023. Also of note, continuing claims rose back above 1.8mm at 1.82mm, 25k more than expected and still hovering around the highest since November 2021.

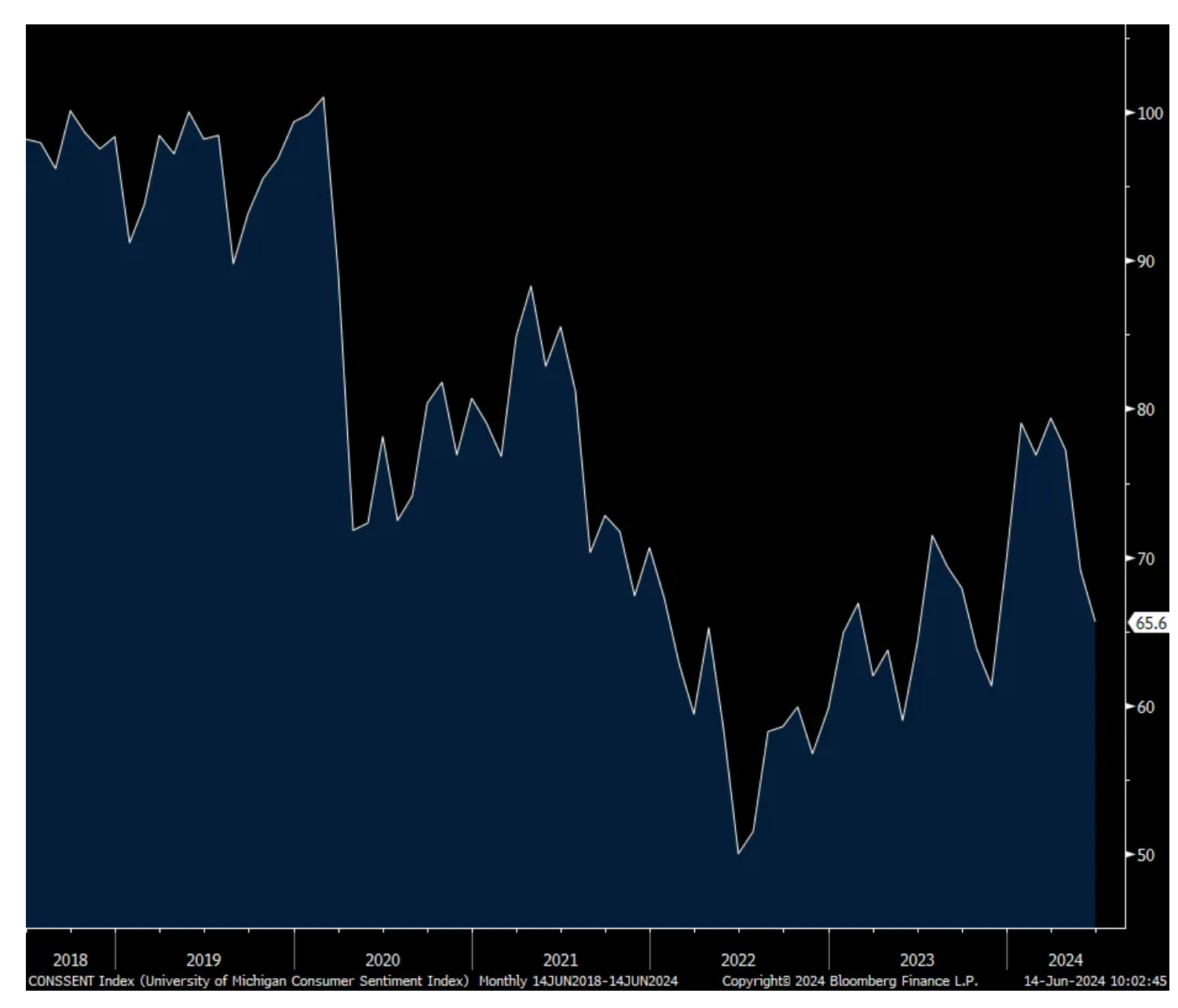

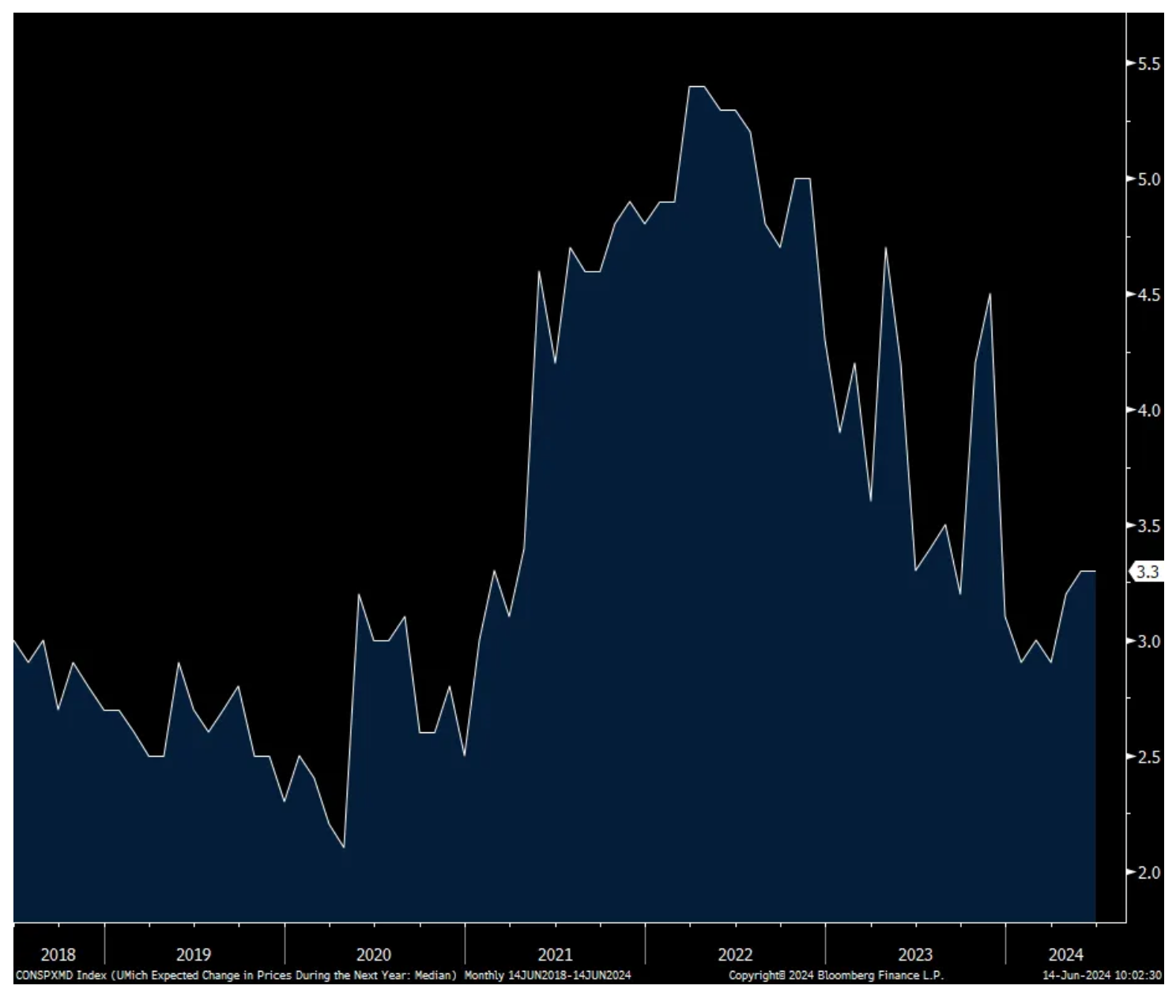

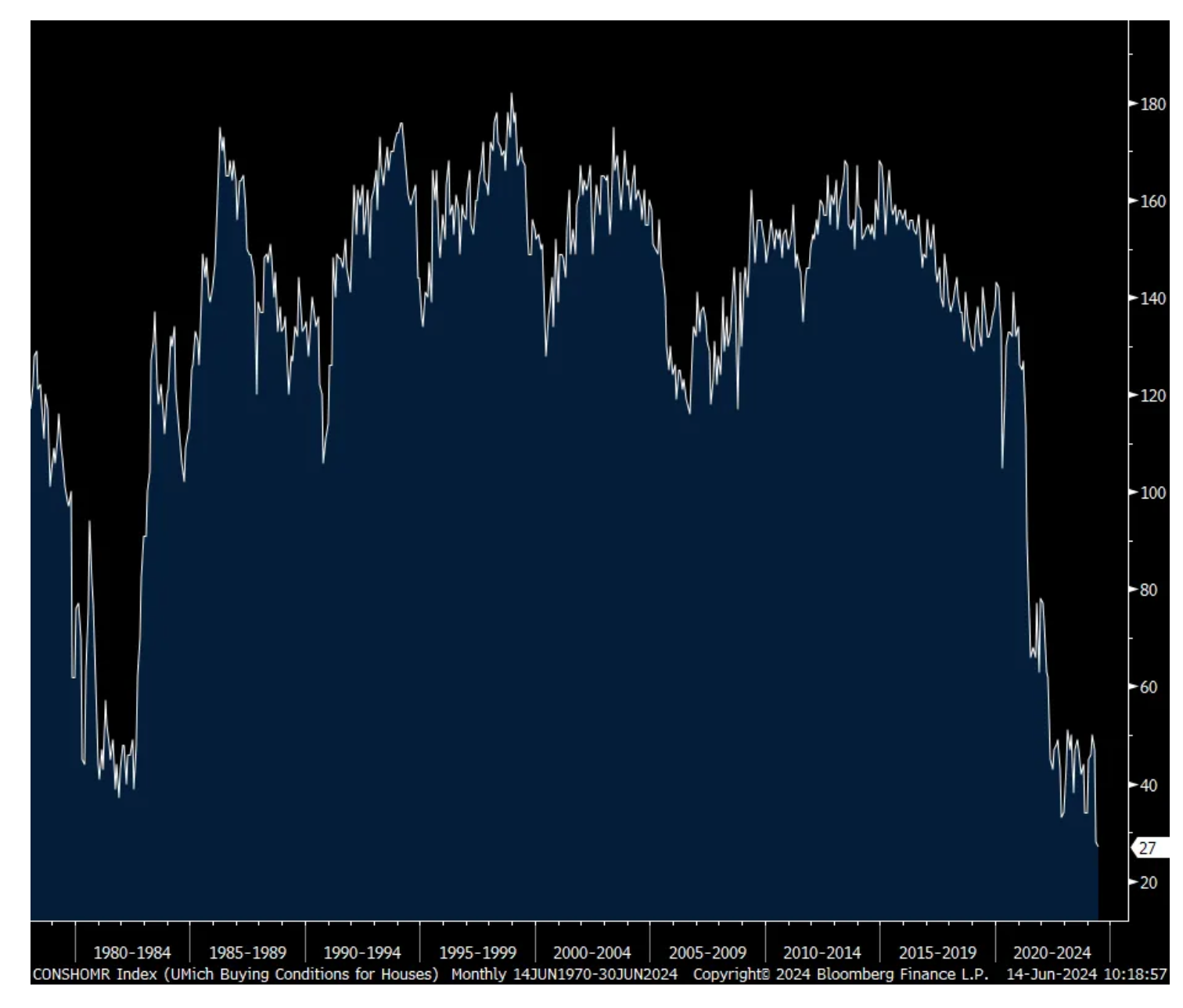

2)The preliminary UoM June consumer confidence index unexpectedly fell to 65.6 from 69.1 and that is well below the estimate of 72. It’s now down almost 14 pts over the past 3 months. Most of the decline came from the Current Conditions component which declined by 7.1 pts m/o/m while Expectations slid just 1.2 pts. One yr inflation expectations held at 3.3%, the highest since November and the 5-10 yr guess ticked up by one tenth to 3.1%. Spending intentions continue to deteriorate. From the UoM, “Although high price complaints have generally fallen since 2022 for higher-income consumers, these complaints have continued largely unabated during this period for those with lower incomes. While lower-income families have, as a group, seen notable wage gains in a strong labor market, their budgets remain tight amid continued high prices even as inflation has slowed. The views of middle-income consumers resemble those of their lower-income counterparts, a departure from historical patterns in which their mentions are squarely in between those of higher- and lower-income consumers.”

3)In the NY Fed’s Consumer Expectations Survey, price expectations for the necessities remain high. For gas, 4.8%, food, 5.3%, rent, 9.1%, medical care, 9.1% and college at 8.4%. As for home prices, they were unchanged at 3.3%. The job market results were mixed. Spending expectations did slip by two tenths to 5% but has been steady between 5-5.2% over the last 6 months. Expectations for future credit access "deteriorated, with a larger share of respondents expecting tighter credit conditions a year from now, and a smaller share expecting easier conditions."

4)The Shanghai to Rotterdam trip rose another $145 w/o/w to $6,177 for a 40 ft shipping container. It's doubled since May 2nd and is up almost 4x off the late 2023 lows. The route to LA rose $50 w/o/w to $6,025.

5)Last Friday the WorldACD Market Data on air cargo rates said "Rate surge continues throughout May from Middle East & South Asia (MESA)...Amid continuing strong demand, and disruptions to ocean freight services caused by the attacks on container shipping, average air cargo rates in May of US $2.78 per kilo from MESA to worldwide destinations were up 47% y/o/y with tonnages up 17% higher, based on the more than 450,000 weekly transactions covered by WorldACD's data. And from MESA origins to Europe, May's average spot rate of around $3.35 per kilo was more than double the level in May last year, with the average spot rate in week 22 (27 May to 2 June) up by 128% y/o/y."

6)The May Fannie Mae Home Purchase Sentiment Index fell 2.5 pts m/o/m "as the component measuring consumer attitudes toward homebuying conditions fell markedly, reaching an all-time survey low…This month, only 14% of consumers indicated that it's a good time to buy a home, down from 20% last month, while the share believing it's a good time to sell fell from 67% to 64%."

7)From RH: "Demand was up 3% in the quarter, slightly below our guidance, as growth softened when interest rates once again exceeded 7% post the hawkish Fed commentary throughout April…We do expect the constantly changing outlook regarding monetary policy will continue to weigh on the housing market through the 2nd half of 2024 and possibly into 2025…I don't think that there's a meaningful sustained move in the home market. I think you've got little ticks up here and there and kind of bouncing around the bottom. And I think it will be until we have a meaningful move in interest rates."

8)From Signet Jewelers: "This continues to be a challenging environment with macro pressure on the consumer and heightened discount activity among many jewelry participants…So we've continued to see a highly promotional category.”

9)From Casey’s General Store: “The lower end consumers, which is only about a quarter of our guest base, they're still continuing to buy. They're just moving around the store a little bit. A simple example is our fountain soft drink business has been really strong this last year and that's especially so among our lower income consumers. And that on a price per ounce basis, is a lot more affordable than buying the bottle and can version inside the store. So they're still purchasing. They're just making different decisions and those flow back and forth between categories."

10)From Daver & Buster’s: "it's a complex macro environment and it's been challenging. There was more weakness within lower income consumers versus moderate income and higher income, and we saw some strengthening in the higher income last quarter. Those trends continued into Q1…While some restaurants are likely to slow the pace of price increases, they are looking to raise prices further as "we have realized significantly less price compared to our peers and believe there's an opportunity for us to optimize our prices and menu mix in order to close this gap."

11)From Academy Sports & Outdoors: "As we expected, our customer remains challenged by the current macroeconomic environment. Inflation is keeping prices at elevated levels, while personal savings have been depleted, causing our customers to be tight with their discretionary spending. The trends we've cited in previous calls in terms of customer shopping patterns held true in the first quarter, with customers shopping episodically while gravitating towards the value offerings in our assortment along with new and innovative items."

12)From Korn Ferry: "This environment we're in, every company is in an incredibly difficult environment. There is a fight for growth, there is a fight for relevancy...We think the labor market in the United States is not going to change materially. I don't think there's going to be huge adjustments to interest rates. Costs for most Americans have gone up 35% to 40%. Wages have not gone up that much. And so I think realistically, if you're only looking a quarter, which is quite myopic, I think it's going to be kind of the environment we're in."

13)MSC Industrial lowered guidance: "Today we announced softer than expected preliminary 3rd quarter results and are lowering our full year 2024 outlook, primarily driven by two factors. First, while average daily sales improved sequentially, ongoing heavy manufacturing softness and a slower anticipated ramp in our Core Consumer resulted in a lower sequential revenue improvement than anticipated. Second, gross margins were approximately 60 bps below our expectations."

14)Nucor did too: “The largest driver for the expected decrease in earnings in the 2nd quarter of 2024 as compared to the 1st quarter of 2024 is the decreased earnings of the steel mills segment, due primarily to lower average selling prices, and, to a lesser extent, lower volumes.”

15)While Broadcom’s AI business is rocking, they still see “continued cyclical weakness in semiconductor revenue from enterprises and telcos."

16)The BoJ did nothing but at least laid the groundwork for another change in policy in July.

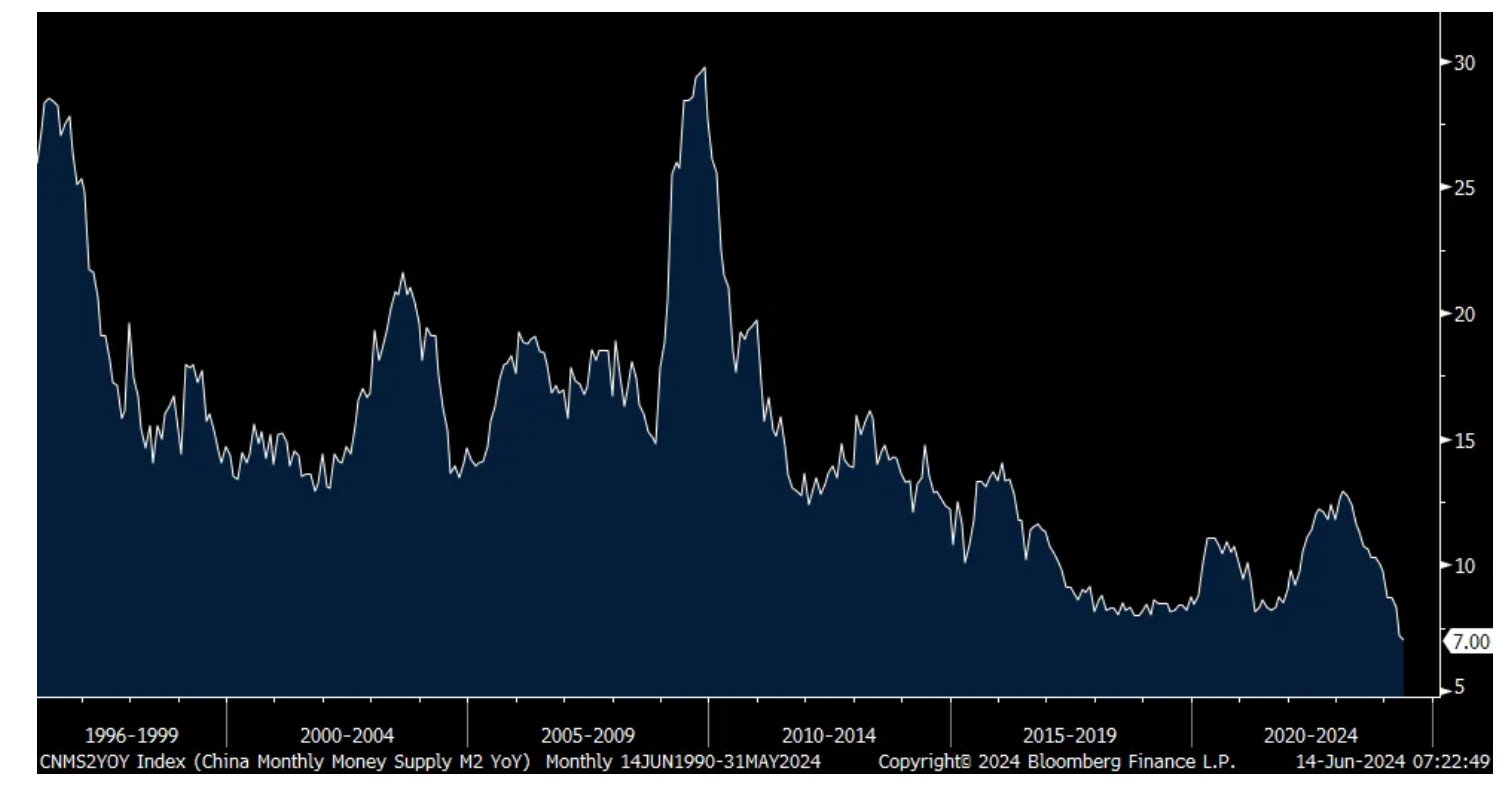

17)China reported its May aggregate loan data and it was a bit under expectations, though still up 8.4% y/o/y (mostly driven by government borrowing) and M2 money supply growth slowed to 7% growth from 7.2% in April. That happens to be the slowest rate of gain since I have data going back to 1996.

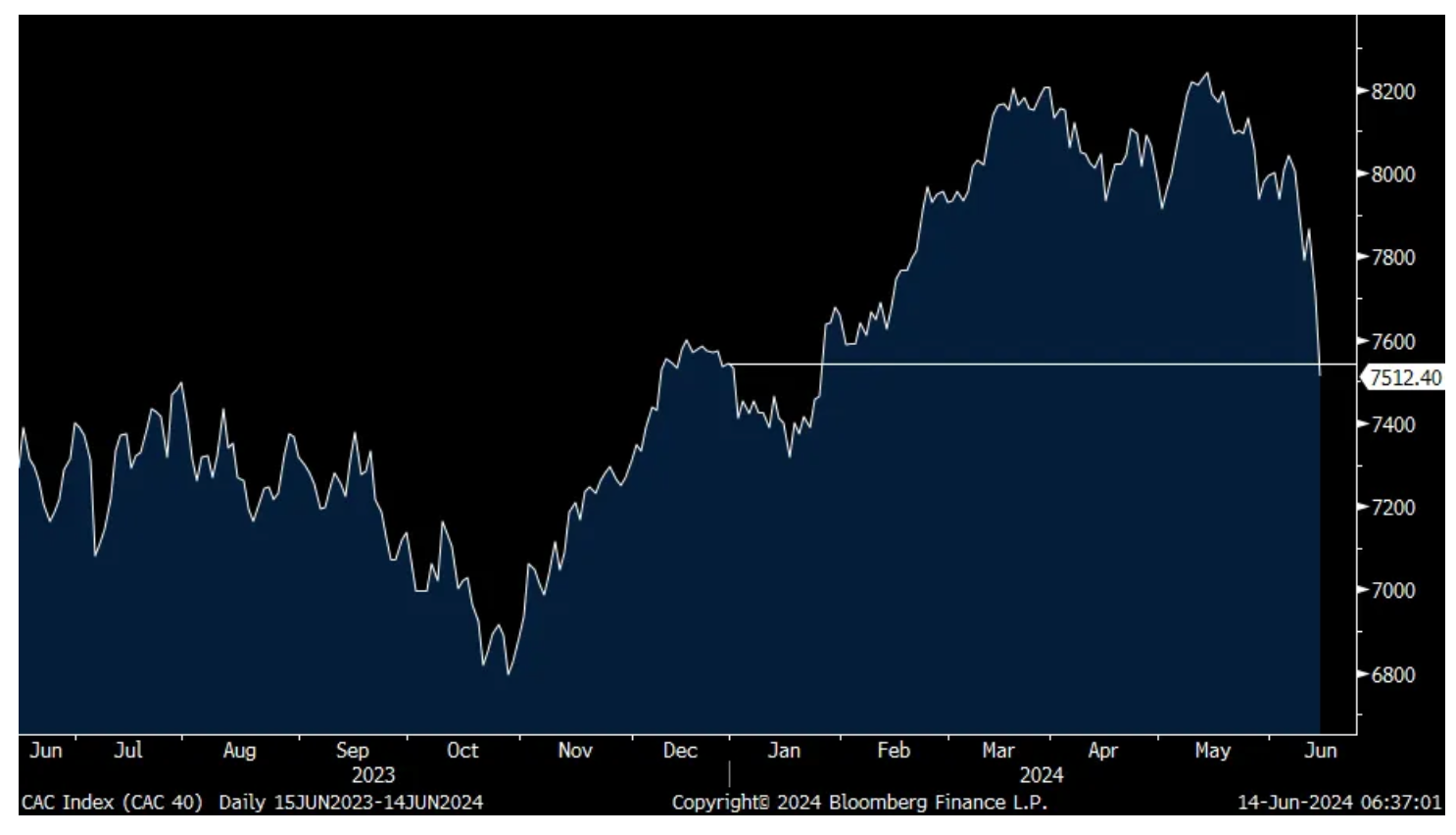

18)Turmoil in French markets as the CAC loses its year to date gains but I just can’t get too worked up over chaotic European politics.

19)UK employment weakened more than expected in the 3 months ended April as their unemployment rate rose to 4.4% from 4.3% where no change was forecasted. And, there was a reduction of 139k in the number of those employed vs the estimate of a drop of 98k. Also, there was a large 50.4k person increase in those filing for jobless claims in May. That's the biggest one month increase since February 2021.

* As I mentioned yesterday the reward vs. risk in the cannabis sector has never been better.

* Singalong!

… Would you believe in a love at first sight? Yes, I'm certain that it happens all the time What do you see when you turn out the light? I can't tell you, but I know it's mine

Import prices/It's the cumulative rise in inflation, stupid

After jumping in April, import prices fell in May, leaving the y/o/y change not much changed. The headline fall was .4% vs the April rise of .9%. The estimate was for a one tenth drop. Ex petro saw a 3 tenths fall after rising by 6 tenths last month. The estimate was for another .2% rise. Versus last year, headline import prices are up 1.1% mostly because of a 9.8% rise in petro prices and 5.6% gain in food/beverages. Offsetting this are more muted gains in consumer goods which are unchanged y/o/y, capital goods prices lower by .2%, industrial supplies up by 2% and auto/parts import prices higher by 2.3% y/o/y.

Bottom line, overall still pretty benign on the import price data for goods, which squares with the CPI goods data which is flattish too y/o/y, which happens to be the pre Covid trend. Question now is whether it’s sustainable and stays at current trends. We hope so but I question it.

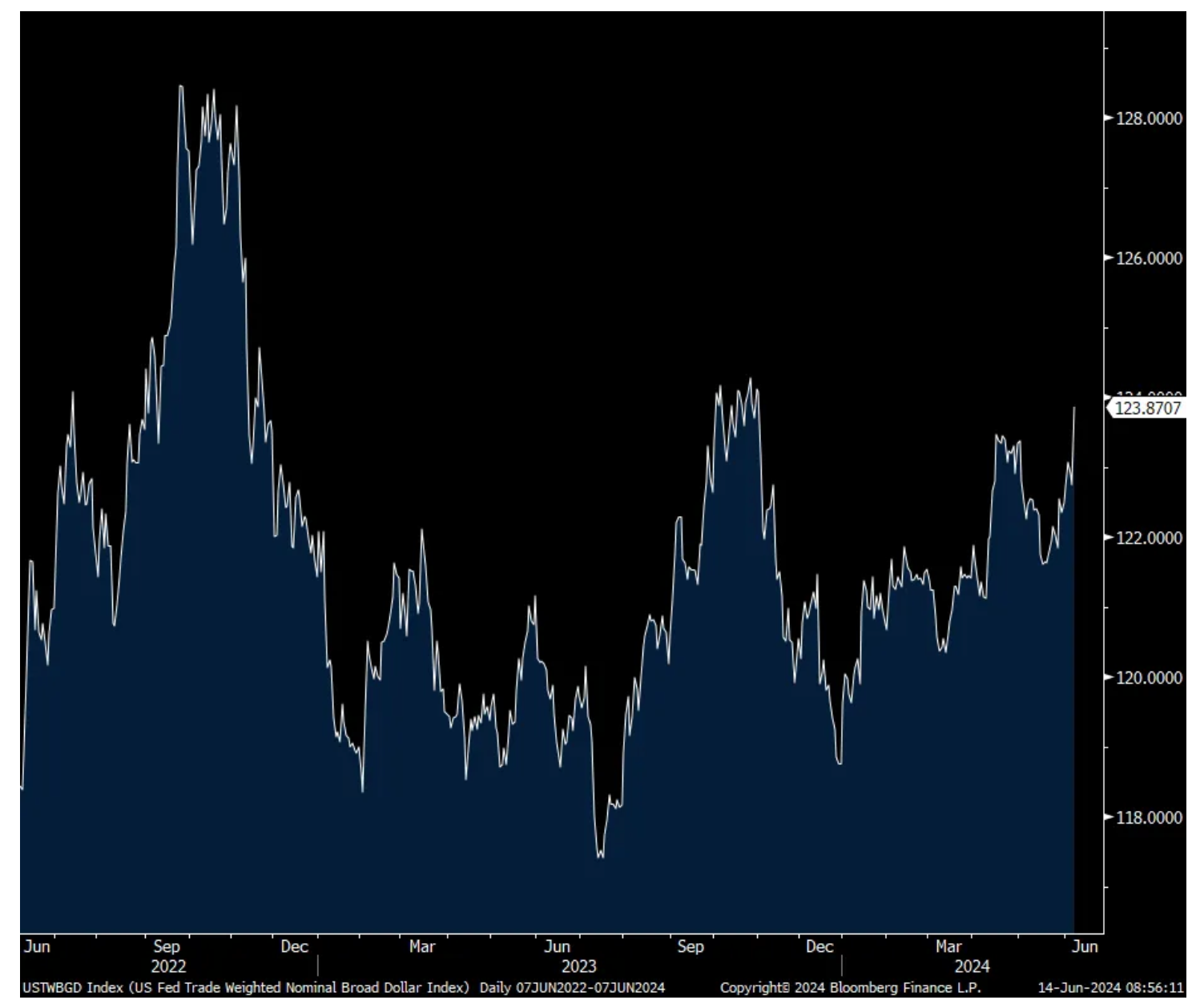

As for the influence of the dollar on import prices, the trade weighted dollar index from the Fed is only slightly above the 2 yr average and with some of this gain coming just over the past few weeks as the Mexican peso fell sharply after their election. https://www.federalreserve.gov/releases/h10/current/

Fed’s Trade Weighted Dollar Index

The preliminary UoM June consumer confidence index unexpectedly fell to 65.6 from 69.1 and that is well below the estimate of 72. It’s now down almost 14 pts over the past 3 months. Most of the decline came from the Current Conditions component which declined by 7.1 pts m/o/m while Expectations slid just 1.2 pts. One yr inflation expectations held at 3.3%, the highest since November and the 5-10 yr guess ticked up by one tenth to 3.1%.

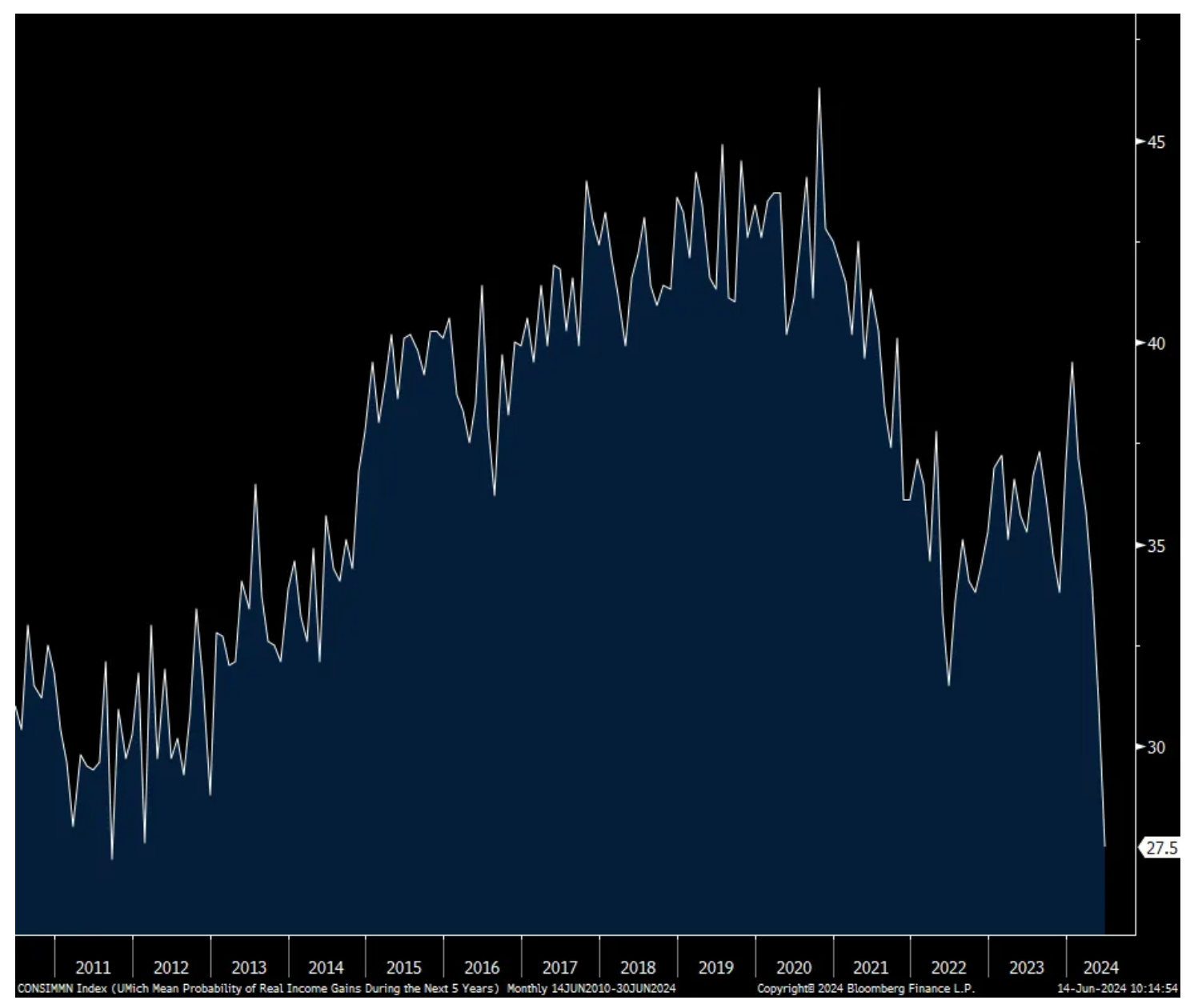

After falling by 10 pts in May to the lowest since last June, the employment component rose 2 pts. Of particular note, those seeing ‘Higher Income’ fell 7 pts to the lowest since November 2013. Combine this with still high inflation expectations, the mean % of those ‘expecting family income will beat inflation over next 5 yrs’ fell to just 27.5%, the worst read since 2011.

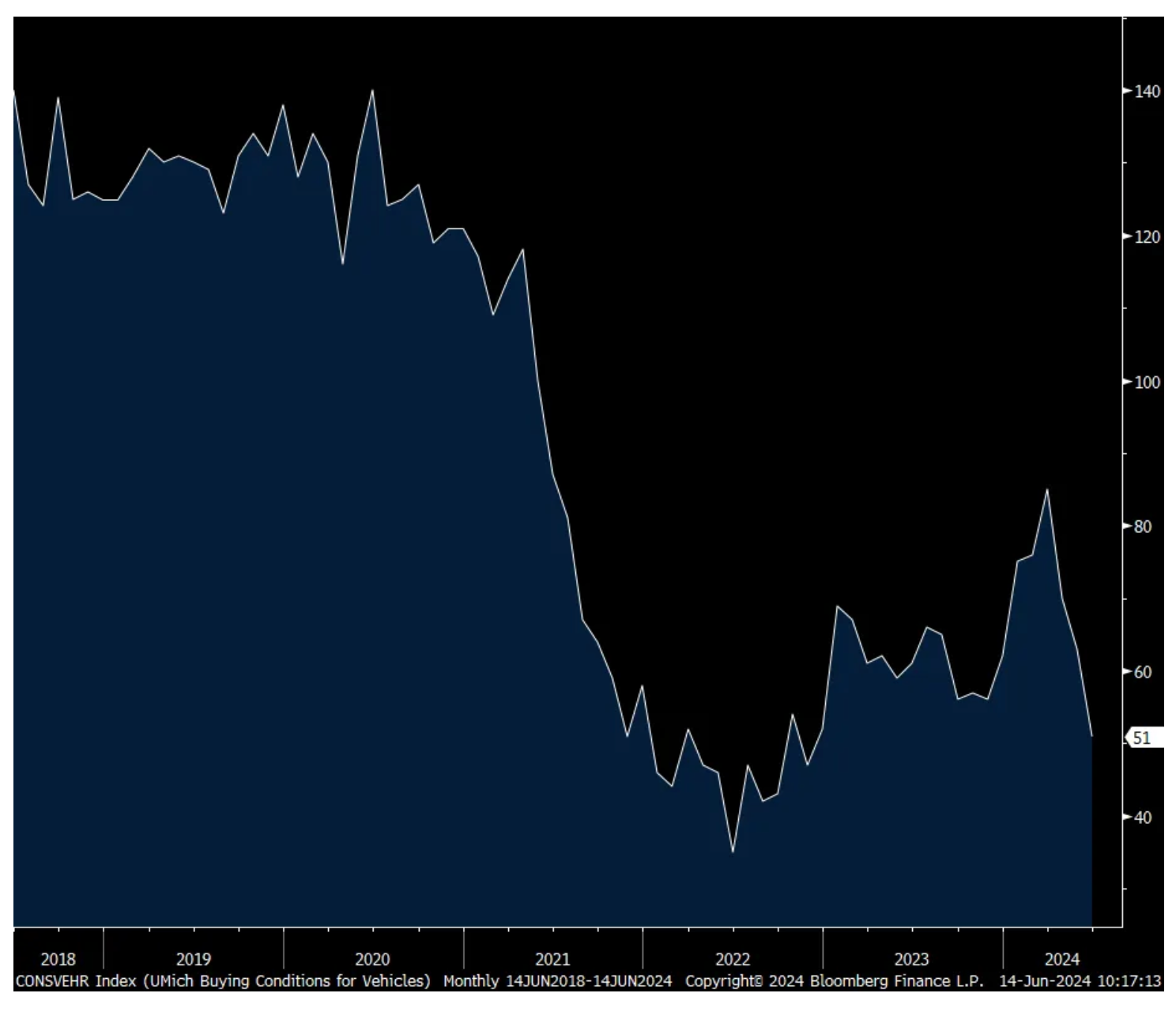

Spending intentions continue to deteriorate, both because of the cumulative rise in inflation and pared with the high cost of funding high ticket purchases. Plans to buy a car fell 15 pts in April, another 7 pts in May and 12 pts in June. At 51 that is the lowest since November 2022. Plans to buy a home plummeted by 19 pts in May and fell 1 pt in June to 27, the lowest on record dating back to 1978.

We have to understand that a mortgage rate of around 7% today is not an apples to apples comparison to what rates were in the 1970’s because the home price to income ratio is dramatically higher today.

With respect to a major appliance, intentions to buy dropped 7 pts and by 28 pts in two months.

While we on Wall Street obsess about the inflation rate of change, many consumers could care less and are still struggling with the cumulative rise relative to their wage growth.

The bottom line is simply the inflation squeeze that lower and middle income consumers are feeling. From the UoM, “Although high price complaints have generally fallen since 2022 for higher-income consumers, these complaints have continued largely unabated during this period for those with lower incomes. While lower-income families have, as a group, seen notable wage gains in a strong labor market, their budgets remain tight amid continued high prices even as inflation has slowed. The views of middle-income consumers resemble those of their lower-income counterparts, a departure from historical patterns in which their mentions are squarely in between those of higher- and lower-income consumers.”

Not quite what James Carville once 30 something years ago said but now it’s the cumulative rise in inflation, stupid.

-BITF +8.2% (Riot Platforms, Inc. reports Beneficial Ownership of 14% in Bitfarms Ltd.)

-ENZ +6.9% (earnings)

-CATX +6.0% (CEO Johan Spoor buys $117K in common stock)

-HAS +3.9% (Tier1 firm Raised HAS to Buy from Neutral, price target: $80 from $70)

-NEXT +3.0% (reportedly Hanwha Aerospace to acquire shares in NextDecade)

Downside:

-GANX -26% (prices 7.11M share equity offering at $1.35/share)

-RZLT -19% (prices 11.3M shares at $4/share)

-MSM -13% (reports prelim Q3, cuts FY guidance)

-RH -12% (earnings, guidance)

-RARE -4.1% (prices 7.4M share equity offering at $39/share)

-IRON -3.0% (priced 4.94M share offering at $36.00)

-PINS -3.0% (recent notable premarket weakness being attributed to Piper Sandler analysts noted Pinterest-Amazon traffic was up 83% y/y in May, a deceleration from +147% in April)

-NUE -2.4% (guides Q2, cites lower average selling prices at steel mills segment)

-DDOG -2.0% (Monness Crespi Cuts DDOG to Sell from Hold, price target: $98)

BoJ being even more patient but.../CAC back to flat/Gary Friedman comments and more

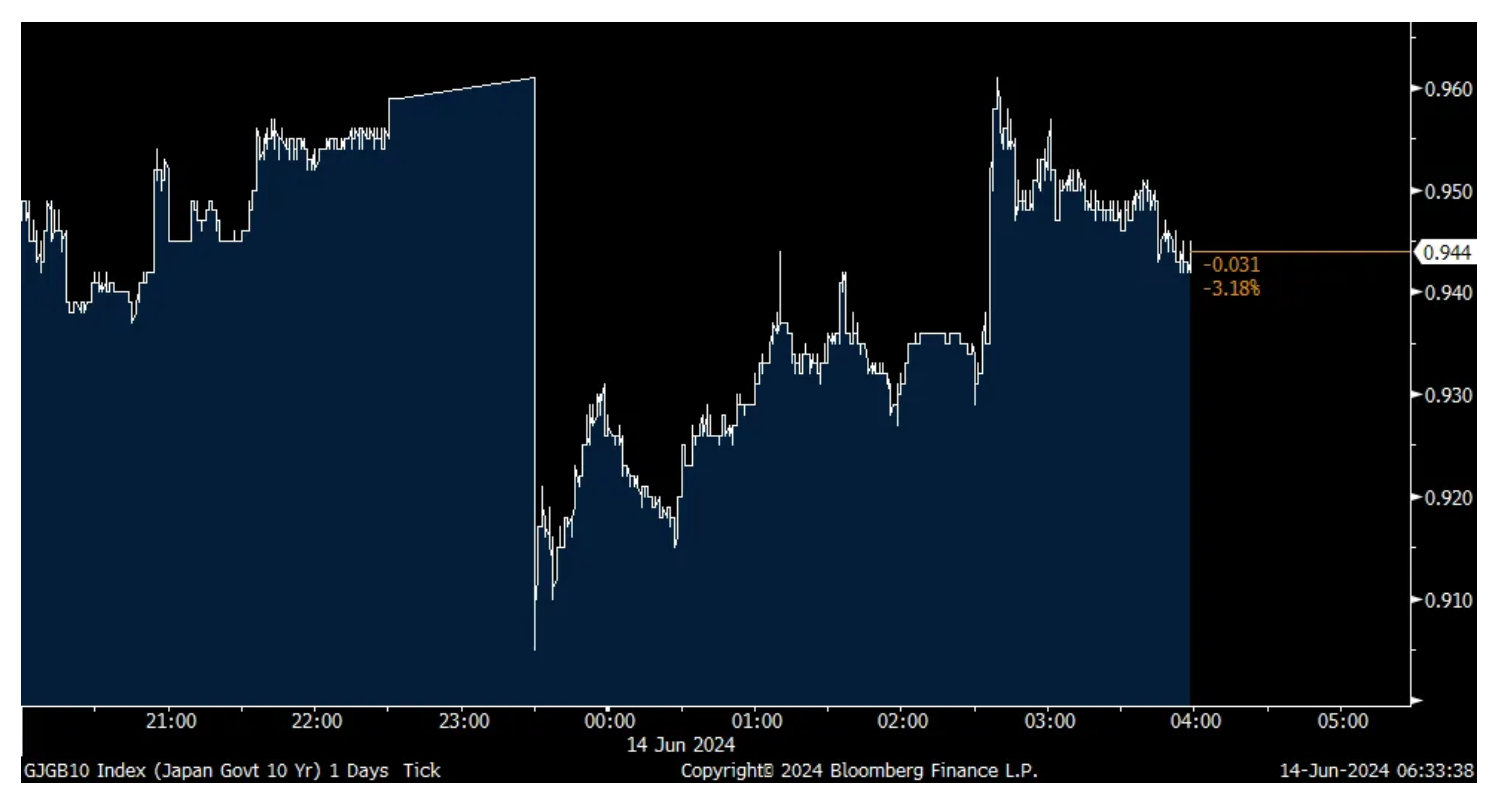

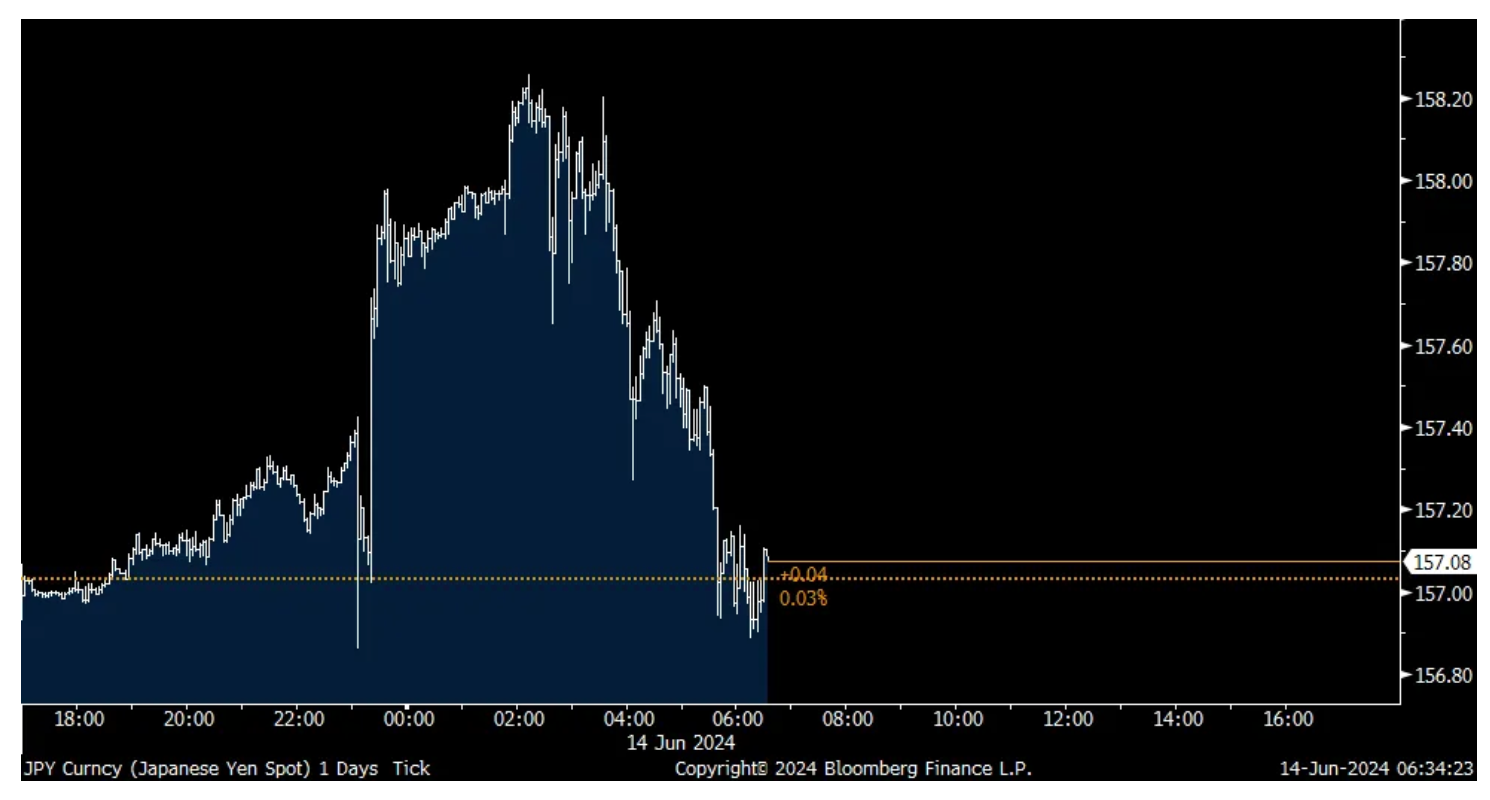

Open Webster's Dictionary under the word 'patient' and the Bank of Japan is still listed there. Just as we thought overnight there would be an announcement on cutting QE, Governor Ueda said we have to wait until July. On the flip side, he also said that when it comes it could be big and a rate increase could come next month too.

On QE, "In trimming bond buying, it's important to leave flexibility to ensure market stability, while doing so in a predictable form." Interestingly he did say the cut in purchases would be "significant." On a possible rate hike, "Depending on economic and price data that become available at the time, of course there is a possibility we could decide to raise interest rates and adjust the degree of monetary support in July."

Governor Ueda also gave notice to the FX market, likely encouraged by the Finance Ministry, and said "Exchange rate moves would have a big impact on the economy and prices. Recent yen falls have an effect of pushing up prices, so we are closely watching the moves in guiding policy."

The market's reaction was immediately a plunge in JGB yields and drop in the yen but when markets realized that Ueda is setting us up for a possible notable move at the end of July, the moves reversed.

Intraday 10 yr JGB move

Intraday Yen move

Notable today too overseas was the French CAC which is down almost 3% and has given back its entire 2024 stock market rally ahead of the early parliamentary elections in late June/early July.

CAC

Before I get to the earnings comments of note yesterday, particularly RH and will include an interesting one from Casey's, we got another insurance quote within the inflation stats yesterday that will show up in PCE in a few weeks. That being 'property, casualty insurance' seen in yesterday's PPI that was up .7% m/o/m and 7.3% y/o/y.

From Gary Friedman at RH:

"Demand was up 3% in the quarter, slightly below our guidance, as growth softened when interest rates once again exceeded 7% post the hawkish Fed commentary throughout April."

"We do expect the constantly changing outlook regarding monetary policy will continue to weigh on the housing market through the 2nd half of 2024 and possibly into 2025."

"I don't think that there's a meaningful sustained move in the home market. I think you've got little ticks up here and there and kind of bouncing around the bottom. And I think it will be until we have a meaningful move in interest rates."

"I think the Fed is going to be massively data dependent, which means the Fed will be behind the curve, right? And so they were behind the curve on seeing inflation. I think they'll be behind the curve as it relates to assessing, is inflation under control? And I think they'll be behind the curve as it relates to it's time to cut interest rates. So our view is probably a little bit more negative than it was a quarter ago. I think a quarter ago, we were feeling a little bit more optimistic that there'd by rate cuts and the housing market would begin to meaningfully move in a sustained manner. I think it may not be until '25 or 2nd quarter '25, maybe. So I don't think there's going to be a sustained inflection in luxury home sales at these interest rates." He went on to say that it's not just interest rates that are high but "home prices up roughly 50%, 60%...I mean, it's just simple affordability now."

From Signet Jewelers:

"This continues to be a challenging environment with macro pressure on the consumer and heightened discount activity among many jewelry participants."

"So we've continued to see a highly promotional category. Independent jewelers were significantly over-inventoried for the last 18 months. That has been now getting back to a more normalized level. So we'd hope to see the competitive environment get back to a level of normalcy potentially in Q2 and Q3, although we haven't accounted for that in our plans."

They talked about the demand for natural diamonds vs lab produced. "So in engagement, we still are seeing far and away a choice of natural diamonds by customers for engagement. Lab created has been a good choice for more price conscious customers. We've had a challenged consumer environment for a while now. And so, I think that it has been a good innovation in that context for people who can't afford to get the size and clarity of stone they'd like in natural." And price of course has fallen with lab diamonds because of "significant availability."

This was from Casey's General Store a few days ago:

"we're seeing pretty consistent behavior with the upper income consumers. They're continuing to buy as they normally have. The lower end consumers, which is only about a quarter of our guest base, they're still continuing to buy. They're just moving around the store a little bit. A simple example is our fountain soft drink business has been really strong this last year and that's especially so among our lower income consumers. And that on a price per ounce basis, is a lot more affordable than buying the bottle and can version inside the store. So they're still purchasing. They're just making different decisions and those flow back and forth between categories."

From Korn Ferry, the executive job search firm:

"This environment we're in, every company is in an incredibly difficult environment. There is a fight for growth, there is a fight for relevancy...We think the labor market in the United States is not going to change materially. I don't think there's going to be huge adjustments to interest rates. Costs for most Americans have gone up 35% to 40%. Wages have not gone up that much. And so I think realistically, if you're only looking a quarter, which is quite myopic, I think it's going to be kind of the environment we're in."

Finally, MSC Industrial, a major distributor of important supplies to the manufacturing/industrial sector, lowered guidance last night and the stock is down sharply pre market.

"Today we announced softer than expected preliminary 3rd quarter results and are lowering our full year 2024 outlook, primarily driven by two factors. First, while average daily sales improved sequentially, ongoing heavy manufacturing softness and a slower anticipated ramp in our Core Consumer resulted in a lower sequential revenue improvement than anticipated. Second, gross margins were approximately 60 bps below our expectations."

China reported its May aggregate loan data and it was a bit under expectations, though still up 8.4% y/o/y (mostly driven by government borrowing) and M2 money supply growth slowed to 7% growth from 7.2% in April. That happens to be the slowest rate of gain since I have data going back to 1996. Bottom line, the country continues to delever, particularly its developers in the residential real estate market and consumers focus their spend on services rather than goods.

Households are also lacking enthusiasm for the U.S. economy’s prospects. What differs compared to players interfacing with consumers is the rapidity with which households’ sentiment has shifted. To wit, the CivicScience U.S. economy index, a component of the headline Economic Sentiment Index, abruptly collapsed in the latest two-week period ended June 4th (yellow line). Sudden moves in macro data tend to occur around cyclical turning points - and come out of left field. The eventual snapback in other consumer sentiment gauges is sure to be accompanied by the same in corporate bond credit spreads (light blue line). Perhaps sandpaper would be best suited to scrub performance in one year’s time.

While I don't have a dog in the hunt, over the last few weeks, in my Tales of Nvidiaseries, I have raised questions whether investors are blind to the risks that the company might face.

The near unprecedented and continuing rise in the shares (and results) for Nvidia are something to behold and are the chief contributing factor to the increasingly bifurcated market — with a diminishing amount of stocks contributing an abnormal portion of the market's overall returns.

In the fullness of time, it will end badly (FOMO, OHNO?) though I have no idea of the timing. But I am reasonably certain that the correction in the shares of NVDA are likely to occur well before there is evidence of an inflection point in the company's currently strong fundamentals:

Here are some more of Bob's lessons that might bear reading:

Lesson 3 There are no new eras – excesses are never permanent.

Translation: There will be a hot group of stocks every few years, but speculation fads do not last forever. In fact, over the last 100 years, we have seen speculative bubbles involving various stock groups. Autos, radio, and electricity powered the roaring 20s. The nifty-fifty powered the bull market in the early 70s. Biotechs bubble up every 10 years or so and there was the dot-com bubble in the late 90s. “This time it is different” is perhaps the most dangerous phrase in investing. As Jesse Livermore puts it:

"A lesson I learned early is that there is nothing new in Wall Street. There can't be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again."

Lesson 4 Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways.

Lesson 5 The public buys the most at the top and the least at the bottom.

Translation: The average individual investor is most bullish at market tops and most bearish at market bottoms. The survey from the American Association of Individual Investors is often cited as a barometer for investor sentiment. In theory, excessively bullish sentiment warns of a market top, while excessively bearish sentiment warns of a market bottom.

Tesla Inc. (TSLA): Implications from shareholder meeting and likely higher tariffs

13 June 2024 | 11:11PM EDT

In this note we frame implications from recent events, including: 1) Tesla's 2024 shareholder meeting on 6/13, where proposals to re-approve Elon Musk's 2018 performance award and to reincorporate in Texas both passed; 2) The US government announced in May 2024 that it will likely increase tariffs on vehicles and lithium-ion batteries made in China, and on June 12th the EU announced an increase in tariffs starting from July 5th for EVs made in China. We also share our latest views on Tesla's 2Q24 deliveries. Please see our note for details.