Boockvar's Succinct Summation of the Week's Events

From Peter Boockvar:

Positives,

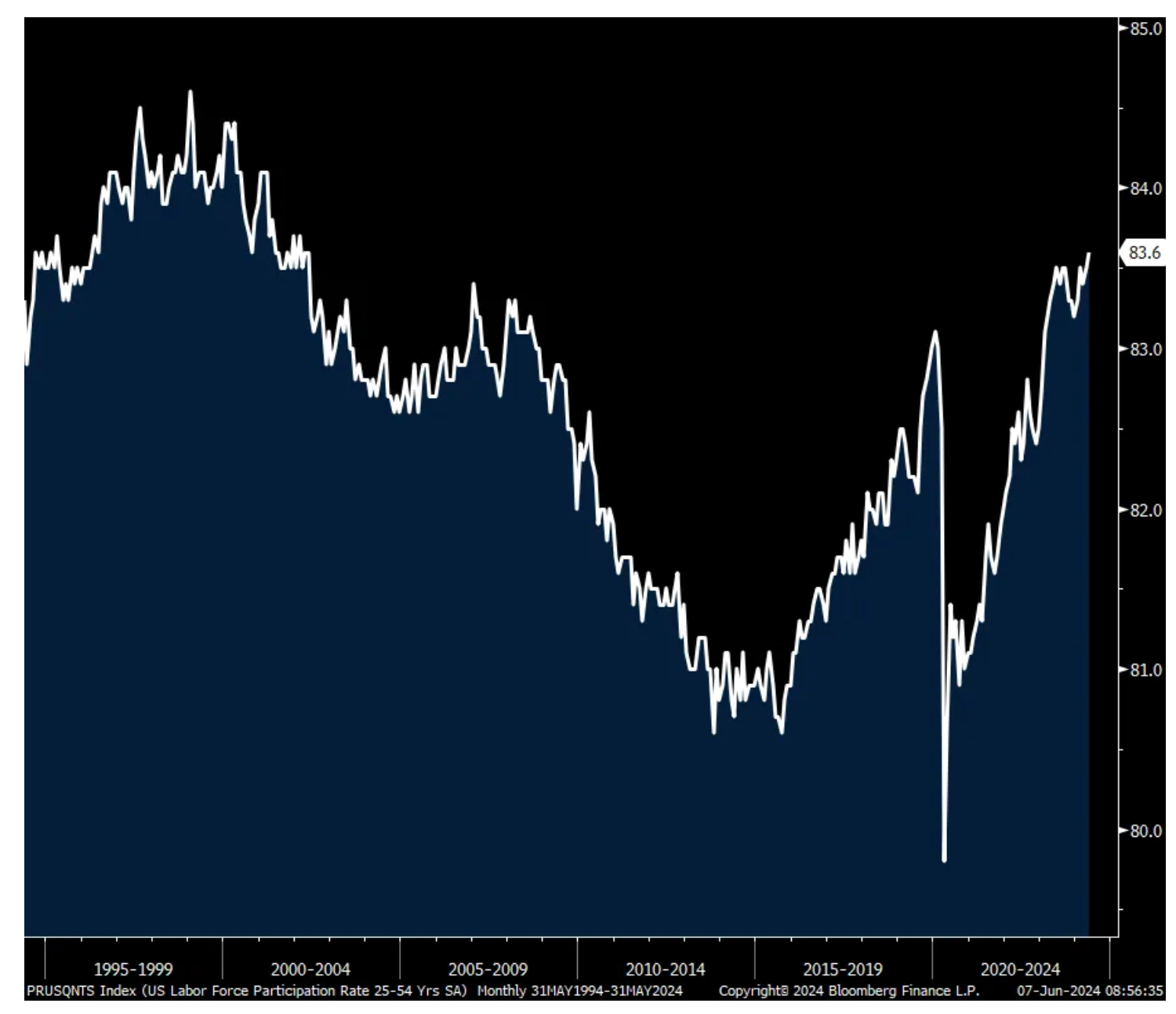

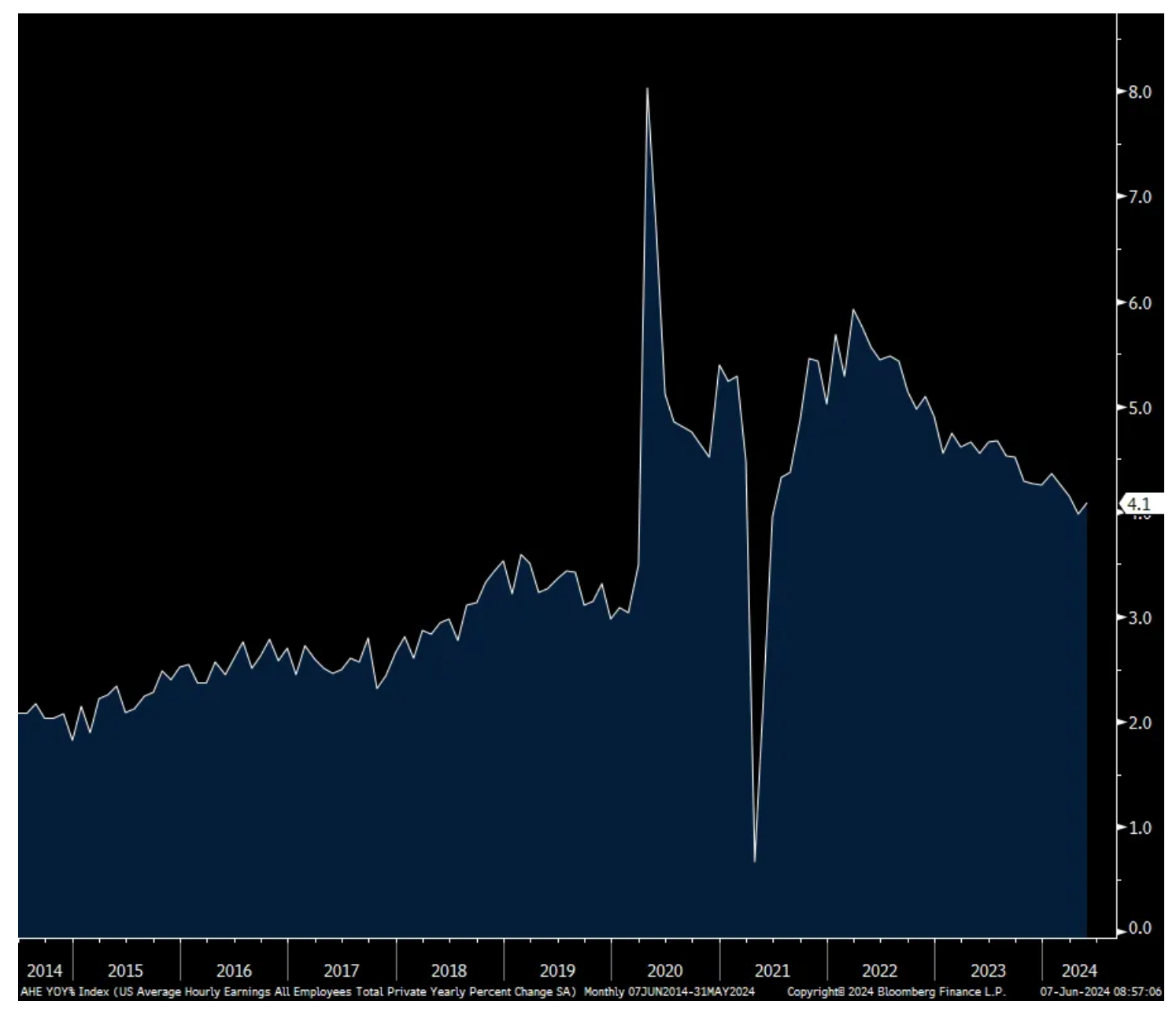

1)Payrolls grew by 272k, almost 100k above the estimate of 180k. The private sector contributed 229k of this vs the forecast of 165k. Revisions to the two prior months were down a combined 15k. Average hourly earnings rose .4% m/o/m, one tenth more than consensus and the y/o/y pace is up 4.1%. For perspective, this averaged 2.5% per annum in the 20 years leading up to Covid. Hours worked were as expected at 34.3 which is where it was in February 2020. Combine this with the hourly earnings figure and weekly earnings grew by .4% m/o/m and 3.8% y/o/y. The 25-54 yr old age group saw its participation rate rise to 83.6% from 83.5% and that is the highest in 22 years.

2)The May ISM services index rose to 53.8 from 49.4 and that was better than the estimate of 51. The internals were quite mixed though. The breadth was a touch better as 13 industries of 18 asked saw growth vs 12 in April while 5 saw a contraction vs 6 in the month before. The bottom line from ISM reflects the mixed picture, and was goosed by the supplier delivery component. “Survey respondents indicated that overall business is increasing, with growth rates continuing to vary by company and industry. Employment challenges remain, primarily attributed to difficulties in backfilling positions and controlling labor expenses. The majority of respondents indicate that inflation and the current interest rates are an impediment to improving business conditions.”

3)In the May Challenger Jobs Report, they said announced job cuts fell 1.5% m/o/m and lower by 20% y/o/y. Year to date thru May, firing’s are down 7.6% and tech continues to lead the way in cuts.

4)The May Logistics Managers Index rose 2.7 pts m/o/m to 55.6. They said "this increase was largely a function of positive movements in the transportation market and warehousing utilization. This expansion faced headwinds in the 2nd half of the month however, particularly from inventory levels, which moved from expansion to contraction." Also of note was pricing as they are rising again "and are mildly above capacity." Their transportation price index jumped 13.7 pts at 57.8 from a contracting 44.1 in April. That's the highest since June 2022.

5)Auto sales in May totaled 15.9mm at a seasonally adjusted annualized rate (SAAR). That is vs 15.74mm in April, just above the 15.8mm estimate and vs 15.05mm in May 2023. Wards yesterday said "Further confirming as a theme for 2024, growth in May largely was centered in the most affordable CUV (crossover utility vehicle) and car segments. Other sectors during the first five months of 2024 have either recorded sporadic gains or fell into steady decline, including some, such as fullsize pickups, that are coming off lengthy periods of strong results. So far in 2024, market strength is with more affordable small and midsize CUVs and small sedans."

6)The Atlanta Fed’s GDPNow is back above 3% for Q2 from 1.8% earlier in the week.

7)From HP Enterprises: "Enterprise customer interest in AI is rapidly growing and our sellers are seeing a higher level of engagement." Similar to Dell however, "This year's mix shift from networking to AI systems should weigh on our gross margins…As we capitalize on the AI growth opportunity, we also see indications of the market recovery in traditional and cloud infrastructure markets. Orders for traditional service grew sequentially and y/o/y, driven by enterprise public sector and SMB customers in North America and Europe."

8)I’ll give the ECB the benefit of the doubt with its interest rate cut because they made it a point that at least for now it’s more of a tweak rather than a tip off to a consistent rate cutting cycle. They don’t want to give up on the inflation fight and consider the cut more being less restrictive rather than easy. Also the same with the BoC.

9)China said its exports in May rose 7.6% y/o/y, above the estimate of 5.7%.

10)The private sector Caixin services index for China rose to 54 from 52.5 and they said "Business activity and total new orders both grew for the 17th month in a row, increasing at the fastest pace since July and May last year, respectively. Notably, growth in total new orders recorded its fourth consecutive month of acceleration, reflecting a strong recovery in demand...Employment expanded following three months of contraction." As for the Chinese service outlook, "Market sentiment remained optimistic. Surveyed companies were generally confident about future market prospects, although they expressed concerns over the global economic landscape and growing costs of raw materials."

11)Base pay in Japan rose 2.3% y/o/y in April, reflecting the Shunto negotiations, and up from 1.7% in the two prior months. That is the fastest pace of wage growth in 30 years, yes, since 1994.

12)Singapore's PMI rose to 54.2 from 52.6. S&P Global said, "Improvements in demand and output spurred a renewed rise in employment levels, while overall confidence levels also rose." For Thailand it was 50.3 from 48.6 and Malaysia it's at 50.2 from 49.

13)India saw its service PMI remain strong at 60.2 vs 61.4 in April and combined with manufacturing, a composite print of 60.5, outperforming most places in the world.

14)Some stabilization in other manufacturing PMI’s too in Asia: South Korea 51.6 vs 49.4, Taiwan 50.9 vs 50.2, Indonesia 52.1 vs 52.9, Philippines 51.9 vs 52.2, India 57.5 vs 58.4, Japan 50.4 vs 49.6, Australia 49.7 vs 49.6 and the private sector focused Caixin China mfr'g PMI at 51.7 vs 51.4 (in contrast to the drop seen in the state weighted one).

15)The May Eurozone manufacturing PMI was revised a touch to 47.3 vs the initial read of 47.4 but up from 45.7 in April and the best read since February 2023. The final figure for the UK was 51.2 vs 49.1 in the month before.

16)German exports in April were a bit better than expected, rising 1.6% m/o/m vs the estimate of 1.1%.

17)The revision to the Eurozone services PMI was 53.2, little changed with the initial read of 53.3 and vs 53.3 in April and 51.5 in March. This is where Germany is well outperforming France with a services PMI of 54.2 vs 49.3 in France. Italy and Spain, via their tourist industries, are also doing better.

18)The UK services PMI was 52.9, left unrevised and compares with 55 in April and 53.1 in March.

Negatives,

1)In stark contrast to the establishment survey, the household survey said 408k jobs were lost in May and joined with the 250k person drop in the labor force saw the unemployment rate rise by one tenth to 4.0%, matching the highest since November 2021 though historically very low as we know. The all in U6 rate held at 7.4%. The big thing though with the household survey is that about ALL of the jobs lost were in the 20 to 24 yr age cohort, totaling a fall of 474k. Those aged 25-54 saw job gains of 87k and the 55 and older crowd saw only a modest drop of 31k. The participation rate fell 2 tenths and back down to 62.5%. This was 63.3% in February 2020.

2)ADP said 152k private sector jobs were added in May, 23k below the estimate and April was revised down by 4k to 188k.

3)Initial jobless claims rose to 229k from 221k and that was 9k more than expected. As a 232k print dropped out, the 4 week average fell by 1k to 222k. Of note, continuing claims remained elevated at 1.792mm, up slightly w/o/w.

4)Challenger also said “hiring announcements are at their lowest level in a decade. The typical churn in a healthy labor market appears to be stalling.”

5)April Job Openings totaled 8.059mm vs 8.488mm in March and about 300k under the estimate. The hiring rate held at 3.6% which is one tenth from matching the lowest since 2014 not including Covid. The quit rate also was unchanged m/o/m at 2.2%, matching the lowest since 2018, also not including Covid.

6)The May ISM manufacturing index stayed below 50 at 48.7 vs 49.2 in April and below the estimate of 49.5. In terms of overall breadth, 7 of 18 industries surveyed saw growth, down from 9 in the two prior months and that is the least since January. Those seeing growth in new orders shrunk to just 4 from 8 in April and 12 in March. The bottom line from the ISM, “Demand remains elusive as companies demonstrate an unwillingness to invest due to current monetary policy and other conditions.”

7)World container prices continue to spike higher and the problem is not just the lengthier trips but also the lack of containers in China as empty ones don't come back to them as fast as they did. The Shanghai to Rotterdam trip was up 15% w/o/w to $6,032, higher by $762 on the week. It's doubled since late April and is up from $1,667 at year end. That's also triple where it was in February 2020, though still well below the panic peak in 2021 of $14,807. The Shanghai to LA trip was higher by 11% w/o/w to $5,975.

8)Mortgage apps were down 5.2% w/o/w with purchases lower by 4.4% and refis declining by 6.8% w/o/w. The purchase index in particular is just shy of the lowest since 1995.

9)Commercial real estate bank loans saw its biggest one week drop outstanding for the week ended 5/22 since March 2023, when SVB blew up, to $2.99 trillion.

10)From ABM Industries: On why Class B office buildings will continue to bleed, "if tenants are taking less space and they can afford to pay the same amount of rent, you can move to Class A. And that's why Class A has been so resilient, because Class B tenants can move to Class A now."

11)From JM Smucker: "just acknowledging that the consumer is behaving a bit more cautiously. There's been some trade around, if you will, up and down in the category. The cautiousness of the consumer seems to have activated a bit more competitive intensity in the category…The coffee category continues to experience commodity volatility and overall meaningful inflation. In response to recent higher green coffee costs that we will begin to incur during the first quarter, we are taking a list price increase across parts of our portfolio in early June."

12)From Dollar Tree: "In both segments, comp growth was driven by traffic gains that were partially offset by lower average tickets. The average ticket declines reflected weaker discretionary demand, particularly in the Dollar Tree segment."

13)From Five Below: They reported a 2.3% drop in comp store sales and "These results fell short of our expectations as we experienced a meaningful slowdown in sales during the back half of the quarter." And why? "First, our negative comp results were driven by a decline in comp transactions. Second, consumers were more discerning with their dollars, increasingly buying to need. We saw this in the types of products they purchased, choosing more items in our version of consumable categories, such as candy, food and beverage, beauty...Additionally, declining sales and older merchandise trends presented greater comp headwinds than planned."

14)From Lulu: With regards to the US, "As we mentioned on our last call, we've seen a slower start to the year due to several internal factors, including missed opportunity in women's and bags, which we are actively addressing, and some ongoing choppiness in the consumer environment. Our men's business has maintained its momentum."

15)From Ollies Bargain Outlet: "Consumers clearly remain under pressure and are seeking value in making their purchases...Everyone loves a bargain and Bargain is our middle name."

16)From Thor Industries: "In our fiscal 3rd quarter, our independent dealers experienced increased retail activity during the Spring selling season; however, conversion to sales remained difficult in light of the economic pressures on retail buyers. Faced with elevated floor plan interest rates, our independent dealers remain understandably cautious with their ordering patterns; consequently, our independent dealer inventory levels remain suppressed."

17)From Bath & Body Work: they referred a few times to the "dynamic consumer spending environment" and "are taking a prudent approach to our guidance."

18)China May Imports were softer than anticipated, rising by 1.8% y/o/y vs the forecast of 4.3% growth.

19)Taiwan also reported its trade data for May. Exports rose 3.5% y/o/y, well below the estimate of a rise of 9.8%. Likely helped by Taiwan Semi shipments, thanks to Nvidia, exports to the US were up 36% y/o/y while falling by 5.3% to Hong Kong/Mainland China. Imports were almost flat, up by .6% vs the consensus gain of 4.5%.

20)Germany reported soft industrial production and factory order activity in April.

21)The number of unemployed in May in Germany jumped by 25k and that was well more than the estimate of up 7k and compares with 11k in April. Their unemployment rate did hold at 5.9% as expected and the head of the statistics agency there said "The spring recovery hasn't really taken off this year."

22)Modi lost some momentum with his governing mandate.

BY Doug Kass · Jun 7, 2024, 4:45 PM EDT