Weekly Roundup: Dueling Factors Lead to Mixed Results Ahead of the Fed

With the market flashing oversold, we have cash to put to work but we will be mindful of next week's Fed meeting.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market put in a mixed performance this week, with the S&P 500 and the Dow trading off while the Nasdaq Composite eked out a modest gain. The difference was largely tied to gains in the Tech sector, which helped shore up the portfolio’s performance this week against more interest rate-sensitive positions that moved lower.

Even though the market’s expectation for the Fed to deliver another 25-basis point rate cut next week jumped following the less-than-feared November CPI report, the market is coming to terms with the likelihood the Fed may deliver another round of sobering comments about the pace of future rate cuts. Appearing at the recent DealBook Summit, Fed Chair Powell said the economy was performing better than expected back in September and data to that point indicated inflation was sticky. That combination, according to Powell, means the Fed can be more cautious. After that appearance, we received this week’s November CPI and PPI reports, which confirmed that stickiness.

Our view is the Fed is likely to deliver another 25-basis point rate cut next week but signal it will take a more measured approach to rate cuts in 2025. As of now, the market sees two more rate cuts next year, one in March and the other in September. But with five Fed meetings in the first seven months of 2025, the central bank can adjust policy as more data on the speed of the economy and inflation is had.

In the Fed’s September set of economic projections, the median forecast had the Fed funds rate at 4.4% exiting this year and 3.4% next year. That implies a December cut and four more 25-basis point cuts next year. However, more recent comments from Powell concede the economy is stronger than the Fed expected at the time of those projections and inflation has remained sticky. This suggests we will see some adjustments in the Fed’s 2025 and 2026 Fed funds rate forecast as well as other components of its economic projections.

Similar to this week’s market reaction to the November CPI data, a better-than-feared set of comments by Powell and updated Fed economic projections would be welcomed, especially if the market is short-term oversold heading into that Fed meeting. So long as the Fed does not telegraph fewer rate cuts next year than the two expected by the market, the likelihood of a Santa Claus rally emerging this year is good.

Closing the books on Friday, the week’s move lower has the market flashing oversold per the McClellan Oscillators. Subject to weekend developments, should Monday’s Flash December PMI show some progress on inflation, we may take advantage of the market’s oversold condition. Rest assured we will stick to our discipline and keep our eyes on the medium-to long term as we do so.

Catching Up on the Portfolio This Week

The portfolio this week felt the impact of declines in Builders First Source BLDR, Dutch Bros BROS, Elastic ESTC, Nvidia NVDA, The Trade Desk TTD and United Rentals URI. Minimized the impact on the portfolio were week-over-week gains in Alphabet GOOGL, Marvell MRVL, Universal Display OLED, Apple AAPL, and Amazon AMZN. Despite the week’s setback for the portfolio, quarter to date it is still outperforming the S&P 500.

On Monday we increased our price targets for Bank of America BAC and Morgan Stanley MS to $53 and $140, respectively. Later that day we also adjusted our ServiceNow NOW target to $1,200 following positive data points found in a new National Bureau of Economic Research working paper about AI adoption.

Wednesday was a busy day for the portfolio as we picked up more shares of Applied Materials AMAT, Builders FirstSource, Lockheed Martin LMT, United Rentals, and Universal Display following the “sigh of relief” November CPI report. Later that day, the data we found in the November FAO Food Price Index led us to downgrade PepsiCo PEP to a Four rating and rescind our price target. Our plan with PEP shares is to use near-term market strength to unwind the portfolio’s position in the coming days.

While that action could lift our cash position, with the market flashing oversold, we may have an opportunity to scoop up some additional shares of names on our shopping list. Still on that list are BLDR and URI, and following this week’s move lower we have some room for LMT shares as well following its bout with some fake news. Others on that list are Eaton ETN, Meta META, and Waste Management WM, but we’re inclined to be disciplined buyers, especially as we continue our work in fleshing out new candidates for the Bullpen and the portfolio.

Now let’s turn to what the Wall Street community said and did about our holdings this week:

Amazon shares saw a price target bump to $260 from $220 at Baird given the firm’s December-quarter channel checks. This move followed TD Cowen upping its target to $265 from $240. Our view has been Amazon would benefit as consumers embraced digital shopping to extend their disposable shopping dollars. Indications are that is what is happening. Following next week’s November Retail Sales report, we will revisit our AMZN price target of $250.

Goldman reiterated its $210 price target and Buy rating for Alphabet shares saying it sees the company well positioned against the “rise of AI.”

Morgan Stanley named Apple shares its Top Pick heading into 2025 with a $273 price target. As we get monthly revenue reports for December and January from Taiwan Semi (TSM) and Foxconn, we will revisit our $250 target.

Costco COST received several price target increases following Thursday night’s quarterly earnings report. Morgan Stanley bumped its target to $1,150 from $950 while BMO Capital upped its to $1,175 and Loop Capital reset its at $1,095.

UBS increased its Eaton price target to $431 from $330, reiterating its Buy rating along the way. The catalyst for the move is expected strong order growth for Eaton’s Electrical America segment. We concur and would be interested in picking up some additional ETN shares for the portfolio.

Citi goosed its price targets for Eaton and United Rentals early this week, lifting them to $440 and $985, respectively.

Jefferies re-initiated coverage on Labcorp LH shares with a Buy rating and a $275 target. Bank of America lifted its LH target to $271 from $262 citing encouraging signs for the Life Sciences Tools sector. We’ll do some digging on this and determine if we need to make any adjustments to our $260 target for LH shares.

Mizuho delivered a pair of price target increases, for Microsoft MSFT to $510 from $480, and for ServiceNow to $1,210 from $1,070. Truist also raised its NOW price target to $1,100 from $900, while TD Cowen boosted its NOW price target to $1,300 from $1,025. We started the week off by lifting our NOW target to $1,200 from $1,100.

Deutsche Bank raised its Waste Management price target to $238 from $234 based on a brighter macro environment for 2025 compared to prior expectations. That was the same rationale cited by Jefferies when it upped its Mastercard MA price target to $640 from $590.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, December 9: Our Next Steps for This Semiconductor Name

Tuesday, December 10: Why Shares of This Equipment Rental Holding Are Under Pressure

Wednesday, December 11: Apple’s New Release Can Kickstart the Real Upgrade Cycle

Thursday, December 12: Fake News Pressures Our Shares, Presenting Opportunity

Friday, December 13: Will the Market Match Its Historical Friday the 13th Performance?

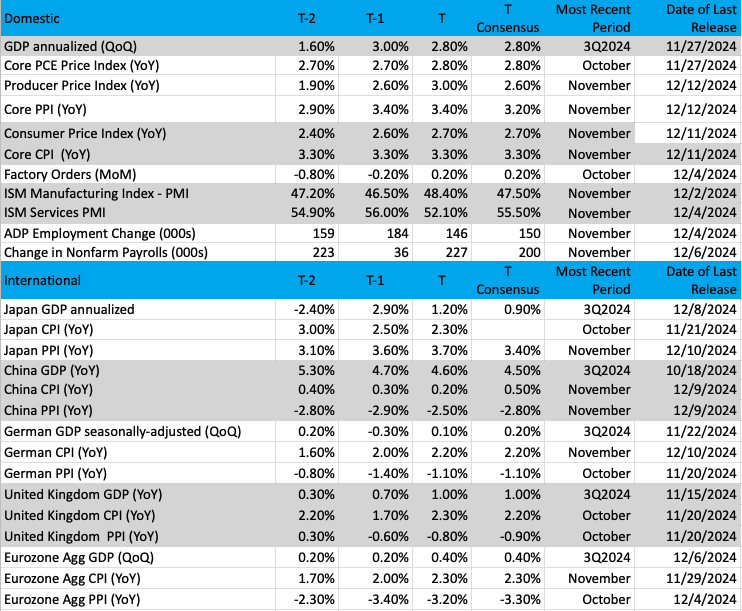

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: VanEck Semiconductor ETF (SMH)

We defy you to find any sector more important than the semiconductors in the technology space. But with the heaviest weight coming from Nvidia NVDA the group tends to be led by this all-star leader, up and down. Hence, why we have experienced mostly sideways action in the VanEck Semiconductor ETF SMH. This ETF has performed poorly versus the overall stock market since October, the divide.

Still, some other components are doing very well. Take Marvell MRVL, for instance, which is in TheStreet Pro Portfolio. This upstart name just hit all-time highs and is looking for more, while Bullpen name Broadcom AVGO had an outstanding quarter, boosted guidance, and talked about the AI revolution. But even with these strong names and a few others, the heavy weighting of Nvidia on the SMH is influential.

Perhaps that may change down the road as we often see rebalancing efforts in other indexes that carry Apple AAPL or Microsoft MSFT. Regardless, the semiconductor group is vital and the lifeblood of success for all technology names. This is the exact reason we hold some of these important names in the portfolio.

The chart of the SMH shows a sideways consolidation that seems to have been going on forever. But the ETF is building a nice base, and the longer it runs the better chance for much higher prices down the road. The indicators are somewhat bearish but notice in pane 4 that the stochastics are turning up. That means momentum is starting to return to this group, but we don’t want to get too excited about it because money flow is just starting to rise, and the MACD is still not showing us a buy signal.

Buying the SMH ETF is not a bad move, but in a stock picker’s market, your success might be in choosing the names that will be winners. While that is challenging to do, we find the exercise of picking the right companies much more fulfilling in this case than just buying them all. Certainly, the returns of semiconductor-related names in our portfolio bear that out.

Other charts we shared with you this week were:

Monday, December 9: S&P 500 - S&P 500 Within Reach of a New Milestone

Monday, December 9: Waste Management (WM) - This Holding Reaches Prime Spot to Add More Shares

Tuesday, December 10: Alphabet (GOOGL) - Google Breaks Resistance With Quantum Chip

Wednesday, December 11: The Trade Desk (TTD) - The Trade Desk Tests Key Trendline

Thursday, December 12: Labcorp (LH) - This Holding Is Heading Toward a Major Support Level

The Week Ahead

For the last full week of trading in 2024, we will be watching the market’s technical setup to see if it becomes short-term oversold, a condition that could set up a Santa Claus rally as we close out the year. In doing that, we will be mindful of next week’s economic data, including the November Retail Sales and Housing Starts reports and December Flash PMI data that will be released before the Fed concludes its policy meeting on Wednesday afternoon.

The November Retail Sales report will reveal not only the degree to which consumers opened their wallets during the month, which included the bulk of the Black Friday-Cyber Monday shopping weekend, but also where they did that spending. Based on findings from Adobe (ADBE), we should see a strong print for digital shopping, and that will lead us to revisit our Amazon AMZN price target. That same report should also bring the next round of consumer wallet share gain confirmation for Costco COST.

With the November Housing Starts report, we’ll be focused on findings for single-family construction given our positions in Builders FirstSource BLDR, United Rentals URI, Vulcan Materials VMC, and to a lesser extent Waste Management WM. After rebounding to 6.93% in mid-November, 30-year mortgage rates backed off in the balance of November, ending the month at lower levels compared to the end of October. We’ll look to see if that activity spurred incremental activity in the housing market, but we’ll balance what we see in this data with upcoming New and Existing Home Sales data.

Those two reports will bring some additional adjustments to rolling GDP expectations for the current quarter. The last update on December 9 from the Atlanta Fed put its GDPNow model at 3.3% and given this week’s data as well as what we’ll get early next week, we will be interested to see where its next update lands on December 17. That’s the same day the Fed kicks off its policy meeting.

The other piece of data will be Monday’s December Flash PMI figures from S&P Global. With the sticky inflation data found in this week’s November CPI and PPI reports, we suspect the Flash December data will be picked over more than usual. Should its comments on input and output prices as well as wages point to that stickiness continuing in December, it would increase the odds of Fed Chair Powell’s comments being more hawkish than not about the pace of future rate cuts.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, December 16

· S&P Global Flash PMI – December (9:45 AM ET)

Tuesday, December 17

· Retail Sales – November (8:30 AM ET)

· Industrial Production & Capacity Utilization – November (9:15 AM ET)

· Business Inventories – October (10:00 AM ET)

· NAHB Housing Market Index – December (10:00 AM ET)

Wednesday, December 18

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Housing Starts & Building Permits – November (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· FOMC Rate Decision (2 PM ET)

Thursday, December 19

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· GDP (Third Estimate) – 3Q 2024 (8:30 AM ET)

· Existing Home Sales – November (10:00 AM ET)

· Leading Indicators – November (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, December 20

· Personal Income & Spending – November (8:30 AM ET)

· PCE Price Index – November (8:30 AM ET)

· University of Michigan Consumer Sentiment Index (Final) – December (10:00 AM ET)

International

Monday, December 16

· Japan: Jibun Bank Flash PMI – December

· China: Industrial Production, Retail Sales – November

· Eurozone: HCOB Flash PMI – December

· UK: S&P Global Flash PMI - December

Tuesday, December 17

· Germany: Ifo Business Climate and Expectations – December

· Eurozone: ZEW Economic Sentiment Index - December

Wednesday, December 18

· UK: Inflation Rate – November

· Eurozone: Inflation Rate (Final) - November

Thursday, December 19

· Eurozone: New Car Registrations – November

· Germany: GfK Consumer Confidence – November

· UK: Bank of England Interest Rate Decision

Friday, December 20

· Germany: Producer Price Index – November

· UK: Retail Sales - November

As you can see below, the crop of earnings reports next week is small. However, there will be several we’ll want to focus on. Lennar (LEN) and its home delivery forecast, AI and cloud adoption comments from Accenture (ACN), and a check on consumer spending by cross-referencing results from General Mills (GIS), Conagra (CAG) and Darden Restaurants (DRI).

Meanwhile, comments from FedEx (FDX) about the holiday shopping season and the global economy will be of interest to us. The same goes for what Nike (NKE) has to say about the consumer, especially in China, and the dollar. Currency may be a topic we hear more about when Micron (MU) reports, but its color on AI, data center, PC, and smartphone markets as well as its capital spending outlook will be our areas of focus.

What we learn on these fronts could influence our actions next week, especially if the market becomes short-term oversold early in the week.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, December 17

· Close: Heico (HEI).

Wednesday, December 18

· Open: General Mills (GIS), Jabil (JBL).

· Close: Lennar (LEN), Micron (MU).

Thursday, December 19

· Open: Accenture (ACN), CarMax (KMX), Conagra (CAG), Darden Restaurants (DRI).

· Close: FedEx (FDX), Nike (NKE).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.