Rising AI Adoption Prompts a Price Target Boost for This Software Holding

Findings from the NY Fed mean we’ll also be looking at this name.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We are reading two reports — one from the New York Federal Reserve and the other a working paper on AI adoption — that underscore our bullish stance for several of the portfolio’s holdings. As we discussed last week and touched on again in today’s Daily Rundown video, the market has gotten somewhat extended, but we continue to see further upside ahead for our holdings. Remember, we don’t buy the market, we buy companies positioned to benefit from multi-year tailwinds and generate superior earnings growth.

National Bureau of Economic Research Working Paper 32966 – The Rapid Adoption of Generative AI

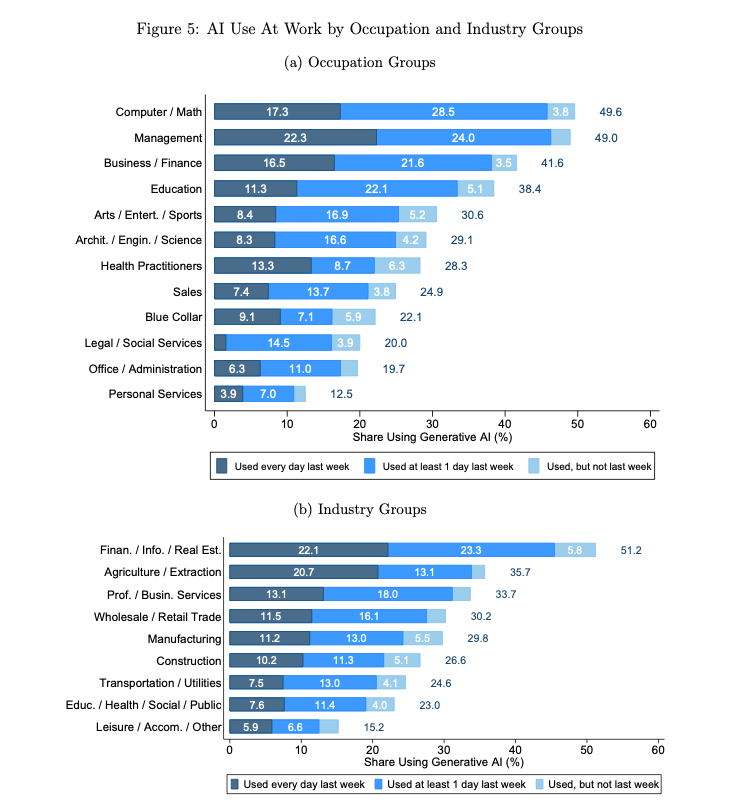

This working paper is chock full of figures and charts that point out the faster pace of AI adoption compared to the adoption of other technologies, including the PC and the internet.

“Generative AI has been adopted at a faster pace than PCs or the internet. Generative AI has a 39.5 percent adoption rate after two years, compared with 20 percent for the internet after two years and 20 percent for PCs after three years (the earliest we can measure it). This is driven by faster adoption of generative AI at home compared with the PC, likely because of differences in portability and cost. We find similar adoption rates at work for PCs and for generative AI.”

The working paper also shows wider adoption of AI across occupation groups and industry groups, which keeps us bullish on Microsoft MSFT, Alphabet GOOGL, ServiceNow NOW, and Elastic ESTC.

As it relates to ServiceNow shares, despite all of the comments and data points revealed during the September-quarter earnings season, we have seen no movement in consensus 2025 EPS estimates for the company in the last three months. This suggests we will be seeing some Wall Street analysts catch up in January. We’ll get ahead of that now by lifting our NOW price target to $1,200 from $1,100 and resetting our panic point to $860 from $800.

The New York Fed’s November 2024 Survey of Consumer Expectations

Three findings in this report stood out to us:

“Perceptions about households’ current financial situations compared to a year ago were mostly unchanged but year-ahead expectations about households’ financial situations improved considerably in November. The share of households expecting a better financial situation one year from now rose to its highest level since February 2020, while the share expecting a worse financial situation fell to its lowest level since May 2021.

“Year-ahead commodity price expectations declined by 0.5 percentage point for gas to 2.7%, 0.5 percentage point for food to 3.8%, and 0.2 percentage point for rent to 5.7%. The expected change in the cost of medical care increased by 0.2 percentage points to 6.0% and the expected change in the cost of a college education increased by 1.0 percentage points to 6.7%.

“The average perceived probability of missing a minimum debt payment over the next three months decreased by 0.7 percentage point to 13.2%, the lowest reading since June 2024.”

Taken together these findings signal consumers are feeling more optimistic about their disposable income prospects, a positive for consumer spending as we finish up the 2024 holiday shopping season and head into 2025. Those data points mesh well with the wage data we saw last week in ADP’s November Employment Change report and Friday’s November Employment Report.

While we are well situated with our positions in Amazon AMZN, Costco COST, Dutch Bros BROS, and Mastercard MA, we will revisit other consumer spending-related companies. One that we plan on digging deeper into is American Express AXP, in part because like Costco we appreciate its differentiated business that is based on membership. Roughly two-thirds of Amex’s pre-tax income is derived from net card fees. And much like Costco, Amex has been growing its membership base, which stood at 145.5 million cards in force at the end of September, up 10 million year over year.

The expected EPS growth for AXP next year is less than 10%, but we have also seen the company lift its 2024 EPS target multiple times this year. Between a humming economy and an improving consumer outlook, there are reasons to think Amex may do that again.

More Pro Portfolio:

- We're Locking In a Triple-Digit Gain for This Deeply-Overbought Name

- Weekly Roundup: A Lack of Fear Is Concerning as the Market Melts Up

- Half of U.S. Living Paycheck to Paycheck — and More Headlines You Might Have Missed

At the time of publication, TheStreet Pro Portfolio was long MSFT, GOOGL, NOW, ESTC, AMZN, COST, BROS and MA.