Weekly Roundup: A Lack of Fear Is Concerning as the Market Melts Up

We’re following Buffett’s advice for an increasingly heady market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Despite a flattish start, the S&P 500 and the Nasdaq notched another positive week, hitting fresh record highs along the way. That is in keeping with the typical seasonal pattern of December, but we’ve noted investor sentiment across a variety of metrics points to the market becoming a bit frothy. To that end, we find the Nasdaq Composite back in overbought territory as we close out the week with its relative strength index (RSI) near 72. While the RSI for the S&P 500 didn’t cross over 70 as we closed out the week, at just under 69, it’s pretty close.

The week’s climb in the market came in the face of November economic data that showed the economy remains on firm footing overall with job creation still at respectable levels but inflation data continuing to inch higher. If one were to suggest the market ignored Fed Chair Powell’s comments on Wednesday, we’d be inclined to agree, especially given Friday’s move higher in December rate-cut expectations despite the week’s data.

Looking at the Volatility Index above, we see its quarter-to-date fall of more than 20% has it back at levels we haven’t seen since mid-July. One thing to know about the VIX, the higher the reading, the greater the fear in the market. That also means the lower the VIX, the lower the fear and the more complacent the market. That has us reflecting on Warren Buffett’s words that it’s wise for investors “to be fearful when others are greedy and to be greedy only when others are fearful.”

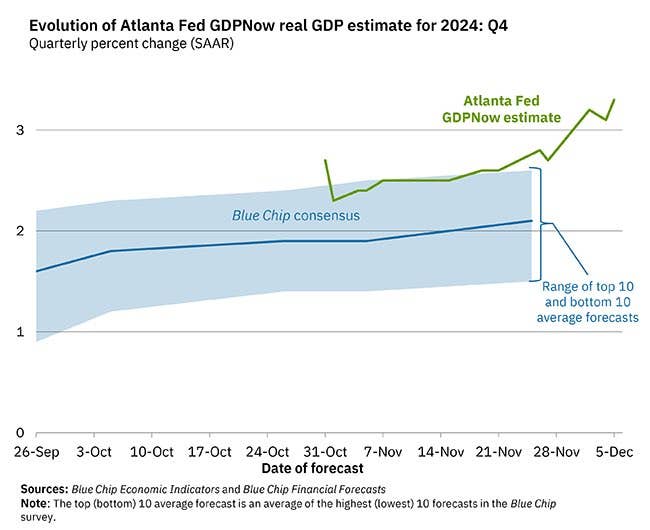

Per the VIX there is little fear in a market that is extended, and while we’re not fearful, it means we’re proceeding cautiously ahead of more November data next week that could challenge the market's preconceived notion of a December rate cut. Considering the lift recent data have given to the Atlanta Fed’s GDP Now model, the market could also be in for a surprise when the Fed updates its set of economic projections on December 18.

Moves we made this week have the portfolio’s cash position back at 12% of its assets, which offers us some cushion should a market pullback emerge as that upcoming inflation data is reported. It also gives us ample firepower to take advantage of that pullback as well as other opportunities we are seeing with existing portfolio positions.

As we plot those next moves, we have some fine-tuning and updating to do with price targets, including those for Trade Desk TTD, ServiceNow NOW, and a few others early next week. When we do that, we’ll make any needed adjustments to panic points as well. Next week, we’ll also continue the work we started this week to refresh the Portfolio’s Bullpen.

Be sure to check your emails over the weekend for our next batch of portfolio signals, and a healthy bowl of Sunday Soup!

Catching Up on the Portfolio This Week

On Monday, we locked in big profits on shares of Dutch Bros BROS and Elastic ESTC as they moved even deeper into overbought territory. As we explained in the trade Alert, that move took advantage of the current condition of the shares but we see further upside ahead for both holdings. After Marvell reported a beat-and-raise quarter, we boosted our price target but also locked in another very profitable slice as well as downgraded them to a Two rating. We also lifted our Costco COST price target following the company’s favorable November sales report and we expect more good news when the company reports its quarterly results next week.

The net effect of this week’s moves added to our cash position, but that didn’t deter the portfolio from gaining additional ground this week. Shares of Marvell MRVL were the standout performers this week, rising more than 20% following its quarterly earnings. ServiceNow NOW, Trade Desk TTD, Amazon AMZN and Meta Platforms META were also strong outperformers. Laggards for the week included a few positions on our shopping list, namely Lockheed Martin LMT, Qualcomm QCOM, and Universal Display OLED, one that we discussed in Friday’s video.

Now let’s see what Wall Street had to say about the Portfolio’s holdings this week:

Bank of America BAC and Morgan Stanley MS shares both received new price targets of $57 and $138, respectively, up from $50 and $121, at Keefe Bruyette. The firm sees a post-election pick up in investment banking, trading, and watered-down regulatory environment benefiting both financial firms. We agree and plan on revisiting our price targets for both as IPO and investment banking activity picks up.

Costco COST caught several price target increases with Stifel landing at $1,000 up from $935, while Jefferies bumped its target to $1,145 from $$1,050. Baird hoisted its target to $1,075 from $975.

UBS boosted its Dutch Bros BROS price target to $65 from $44, reiterating its Buy rating given favorable comp sales prospects for 2025 and 2026. We recently shared Dutch Bros aims to expand its food offering, mimicking a successful strategy at Starbucks (SBUX) more than a decade ago. We expect more details on this move in early 2025, but we’re already revisiting our price target.

Eaton Corp ETN saw its price target lifted at Jefferies to $440 from $400, which is where our target still resides for now. Much like we do, Jefferies sees Eaton as a “play on the electrification of everything.”

Marvell MRVL saw multiple price target increases, following our own move to $130 from $105, after this week’s earnings report. BofA, TD Cowen, Oppenheimer, and Susquehanna lifted their targets to $125, while Benchmark and Cantor Fitzgerald reset theirs at $135. Wells Fargo joined us at $130 as did JPMorgan.

Goldman Sachs lowered its price target on Mastercard MA to $557 from $563 even though it sees the larger fintech space benefiting from a stronger economy.

Jefferies upped its ServiceNow NOW price target to $1,250 from $1,000 this week while Barclays boosted its to $1,200 from $1,000. We’d note that consensus estimates for the company have not moved up despite the continued data points for AI adoption in the enterprise. We’re in the process of reworking our price target for this Two-rated company.

Shares of Vulcan Materials VMC saw their target at Argus boosted to $315 from $290 to reflect the improving outlook in the construction industry.

CIBC increased its Waste Management WM target to $235 from $228 as the company benefits from the strong price environment and easing inflation.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, December 2: Here's Our Game Plan as This Semiconductor Name Reports

Tuesday, December 3: How This Market Breather Might Spiral into a Bigger Tradeoff

Wednesday, December 4: Why Powell Could Upset a Market That Is Nearing Overbought Levels

Thursday, December 5: Why We're Focused on This Specific Data Point in Friday's Job Report

Friday, December 6: AI Chip and Software Positions Get Good News

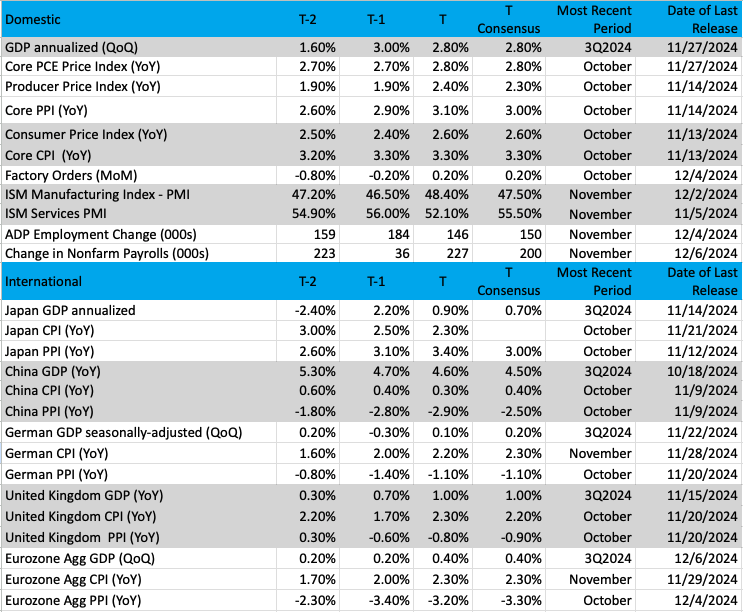

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: Financial Select Sector SPDR Fund

Following the election results we noticed some relative strength in the banks and financials. To see this, we can look closely at the Financial Select Sector SPDR Fund XLF daily chart to find just how strong the financials truly are. We can take it back to July when the money flow really started to expand. This was the month when the names in the XLF, such as JPMorgan Chase JPM, Morgan Stanley MS, and others really started to make a move. Naturally, this group thrives in a low-interest rate environment, and when markets were starting to price in rate cuts during the summer it was the banks that started to outperform.

The XLF shows a strong pattern of higher lows and higher highs, our textbook definition of an uptrend. When overbought, the ETF retreats a bit and simply pulls back to support. The dip buyers are into this "game" of cat/mouse, preferring to let the stock come in before piling in on some heavy buy orders.

We can see as well that each time the XLF touches the 20-day moving average the buyers step in. We are sitting on that 20-day right now, which may be a spot for dip buyers to once again add more shares.

While the MACD (moving average convergence/divergence) is falling and crossing over it is simply resting here until the other moving averages catch up to it. Momentum has slowed down; the stochastics are rolling over while the ADX (pane 3) is also rolling over from a high level.

What might be next for the XLF? A little sideways consolidation in a low-volatility market, waiting until the new year rolls around for some bank earnings just after the calendar turns.

Other charts we shared with you this week were:

Monday, December 2: Nasdaq 100 (NDZ) - Nasdaq 100 Is in a Good Spot for a Year-End Run

Monday, December 2: Morgan Stanley (MS) - This Bank Holding Is Leading the Pack

Tuesday, December 3: Microsoft (MSFT) - Bullish Microsoft Could Power Up Soon

Wednesday, December 4: Alphabet (GOOGL) - A Glimmer of Hope for a Frustrating Holding?

Thursday, December 5: Dutch Bros (BROS) - Resting at the Highs Is Nothing New for This Portfolio Holding

The Week Ahead

Next week could be a bit of a battleground for the stock market. On the one hand, the stocks remains in heady territory and the CME FedWatch Tool indicates the market sees a high probability, near 85%, for a December Fed rate cut. On the other hand, we have what we saw in the November Employment Report, the upward climb in ISM Service price data, and Friday’s revision for the Atlanta Fed’s GDPNow model that puts GDP for the current quarter at 3.3%.

In Friday’s video, we discussed why next week’s November CPI and PPI reports are likely to show core inflation remains at least sticky and has the potential to tick higher compared to recent figures. The inflation findings in those reports will be among the last pieces of key November data we get before the Fed’s next policy decision on December 18. What could make those findings a tad more challenging for some to interpret will be their being published during the Fed’s next pre-meeting blackout period.

We’ll be sure to put the data through its paces and share what it says with members. Given what we’ve seen so far, we’re inclined to interpret this week’s data as supporting Fed Chair Powell’s Wednesday comments that the economy is stronger than previously expected, inflation is running higher, and the Fed can afford to be more cautious in finding the neutral level of monetary policy. That suggests that even though we are in a seasonally strong period for the market, caution is warranted near-term.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, December 9

· Wholesale Inventories – October (10:00 AM ET)

Tuesday, December 10

· Productivity & Unit Labor Cost (Revised) – 3Q 2024 (8:30 AM ET)

Wednesday, December 11

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Consumer Price Index – November (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

· Treasury Budget – November (2 PM ET)

Thursday, December 12

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Producer Price Index – November (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, December 13

· Import/Export Prices – November (8:30 AM ET)

International

Monday, December 9

· China: Inflation Rate, Producer Price Index - November

Tuesday, December 10

· Japan: Eco Watchers Survey – November

· Germany: Inflation Rate (Final) – November

Thursday, December 12

· UK: GDP, Industrial Production, Manufacturing Production – October

· Eurozone: European Central Bank Interest Rate Decision

Costco COST will be reporting next week, and that will be a primary focus for us. We will also be interested in what Ciena (CIEN) has to say about tightening digital infrastructure and what that means for Marvell’s Enterprise Networking and Carrier Infrastructure businesses. With Broadcom (AVGO) our main interests will be what is discussed relating to its smartphone, connected devices, and data center businesses. When it comes to Adobe (ADBE), comments on cloud and AI adoption will be what we’re digging into and what that means for ServiceNow NOW, Elastic ESTC, and Microsoft MSFT.

The other Tech item we’ll be keeping our eyes open for next week will be Taiwan Semiconductor’s (TSM) November revenue report. As you’ve likely come to realize that report will help us track not only AI and data center chip demand, but it will also tell us about smartphone demand during its traditionally strongest quarter of the year. That means the report will have implications for Nvidia NVDA and Marvell MRVL but also Apple AAPL, Qualcomm QCOM, and Universal Display OLED.

Outside of Tech, quarterly results and guidance from homebuilder Toll Brothers (TOL) are what we’ll be watching next when it comes to our position in Builders FirstSource BLDR.

Here's a closer look at the earnings reports coming at us next week:

Monday, December 9

· Close: Casey’s General Store (CASY), Toll Brothers (TOL)

Tuesday, December 10

· Open: AutoZone (AZO) Ollie’s Bargain Outlet (OLLI), United Natural Foods (UNFI)

· Close: Dave & Buster’s (PLAY), GameStop (GME)

Wednesday, December 11

· Close: Adobe (ADBE)

Thursday, December 12

· Open: Ciena (CIEN)

· Close: Broadcom (AVGO), Costco (COST)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.