November Services PMI Reports Conflicting, But Could Catch Fed's Eye

Upward trend in ISM price data will no doubt get noticed by Powell and Co.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The back-to-back November services purchasing managers' index reports from S&P Global SPGI and ISM are once again providing a conflicting set of findings.

The S&P Global found the Services sector perking up in November, with “marked increases in business activity and new orders,” but the ISM’s findings pointed to slower activity in the sector and more subdued order growth compared to the last few months.

On the jobs front, both showed a slower pace of job creation in the Service sector, which jibes with the month-over-month findings in ADP’s November National Employment Report. The key here is the jobs market is still growing, albeit at a slower pace, but not one that should spur the Fed into action.

We’ve seen these two PMI sources conflict in the past. This is important because the data is an input into GDP calculations, including the Atlanta Fed’s GDPNow model. Given the headline miss relative to expectations for ISM’s November Services PMI, which came in at 52.1 vs. the 55.5 consensus and the October figure of 56.0, we should expect to see the rolling GDPNow model be revised lower.

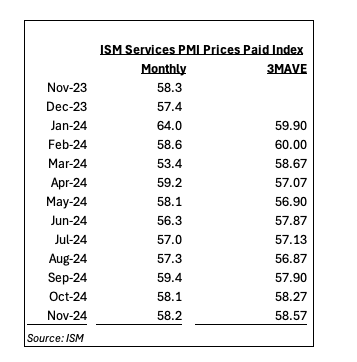

While that will be viewed as a positive tick in the December rate-cut column, adding to the upward move in wage data found in today’s ADP November National Employment Report, as we suspected the price component in ISM’s November Service PMI ticked higher to 58.2 from October’s 58.1.

Examining that price data on a three-month moving average, a perspective Fed Chair Powell shared the Fed uses to examine data, in the table above, we see a clear upward trend over the past few months. This is another indication inflation remains sticky and given the Fed’s focus on inflation in the Service sector we rather doubt this trend will be missed by the Fed. That has us expect less dovish comments from Fed Chair Powell this afternoon, assuming he makes any.

A quick check of relative strength index (RSI) levels shows both the S&P 500 and Nasdaq Composite are once again nearing overbought conditions (RSI>70). That along with other indicators suggests the market is in a heady mindset, especially coming off last night’s quarterly results from Salesforce CRM, Okta OKTA, and our own Marvell MRVL. This suggests that should Powell’s early afternoon comments lean more toward a December policy skip than a rate cut, we are likely to see some market softness emerge ahead of Friday’s November Employment Report.

Coming up we’ll share our thoughts on Marvell’s quarterly results last night, sharing an updated price target as we do so.

The Pro Portfolio is long MRVL.