We're Rescinding Our Price Target for This Holding Amid Rising Input Costs

Here’s our plan for converting the position into cash for the Portfolio.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

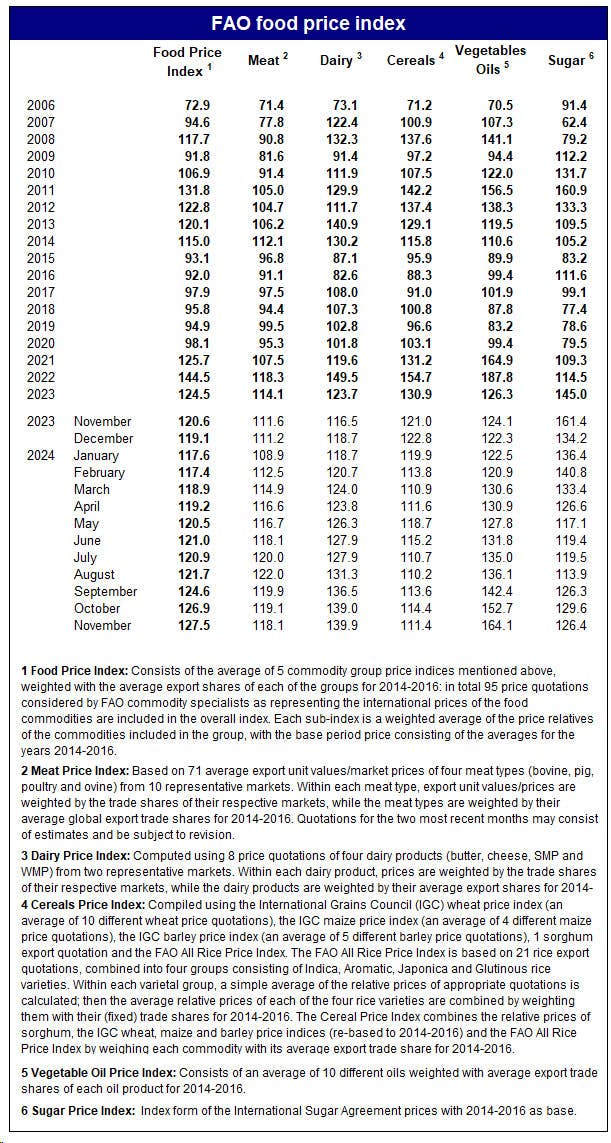

As we finish reviewing the November Consumer Price Index and get ready for Thursday's November Producer Price Index, we’ve noticed food prices have been back on the rise due to gains in protein prices, with those for beef and eggs being notable standouts. This led us to take a closer look at food prices by examining recent FAO Food Price Index data from the United Nations.

When we look at that data in the chart above, we can see the upward climb in the Food Price Index over the last few months, and the higher year-over-year prices in November. Across the five-food commodity baskets that comprise the overall index, meat, dairy and vegetable oil prices are higher compared to year-ago levels, while cereals and sugar are lower, especially sugar. However, when we look at how those five are performing compared to their Q3 average, the indices for meat, dairy, vegetable oils and sugar are noticeably higher quarter to date. Cereals, which include wheat, corn and rice, are little changed compared to Q3.

As we think about those moves, we have to consider the implications for input costs at PepsiCo PEP, which include acesulfame potassium, aspartame, corn, corn sweeteners, flavorings, flour, juice concentrates, oats, potatoes, raw milk, rice, seasonings, sucralose, sugar, vegetable and essential oils, and wheat. We’re also seeing upward pressure in recent months for aspartame as more companies reformulate their products amid the growing demand for less sugar.

Despite these developments, we haven’t seen any shift in Wall Street consensus EPS expectations for the current quarter, nor for the March one in over two months. While we’ve been inclined to hold onto PEP shares as we move through the seasonally strongest quarter of the year, the trend in input prices suggests margin pressure could be ramping up when PepsiCo is focused on stimulating demand. Management shared that comment about its Frito Lay business on its September earnings call, but we’ve noticed an uptick in promotional pricing for its beverage lineup as well.

Putting all of that together, we see potential downside risk to current Wall Street consensus EPS forecasts for the current quarter and for the implied sub-6% EPS growth in 2025 compared to this year. Our thinking is that, as we review candidates for the Bullpen and Portfolio, we will find better uses for the Portfolio’s cash.

That is leading us to downgrade PEP shares to a Four rating. In keeping with that, we will rescind our PEP price target and look to use near-term strength in the shares to reduce the Portfolio’s exposure. As we move into December’s seasonal strength, we’d note that PEP shares have resistance near $165, and unwinding the position near that level and very close to our cost basis would reduce the position’s drag on the Portfolio. Should we see the shares trade sideways over the next few weeks, if we don’t see any improvement in the December FAO Food Price Index data when it’s published in early January, our preference would be not to own PEP shares heading into its December quarter earnings.

More Pro Portfolio

- We're Locking In a Triple-Digit Gain for This Deeply-Overbought Name

- Weekly Roundup: A Lack of Fear Is Concerning as the Market Melts Up

- Half of U.S. Living Paycheck to Paycheck — and More Headlines You Might Have Missed

At the time of publication, TheStreet Pro Portfolio was long PEP.