Weekly Roundup: Chip Rout Tests the Market, but Here’s How We Aim to Capitalize

We raised a few price targets, added to three holdings, and locked in big gains in another.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Stocks finished the week lower, with the Nasdaq Composite bearing the brunt of the damage. The S&P 500 slipped more than 1%, but the Nasdaq tumbled more than 2.5% as a chip-stock rout and renewed Middle East tensions combined to weigh on investor sentiment. Those developments did not leave the Pro Portfolio unscathed, but despite the setback, we remain nicely ahead of the S&P 500 so far this year.

Geopolitics set the tone early in the week. Fighting between the U.S. and Iran flared back up around the Strait of Hormuz, with U.S. forces striking targets inside Iran and Iran’s Revolutionary Guard retaliating against tankers and U.S. military assets in the Gulf. The clash reversed a weeks-long ceasefire and immediately rattled energy markets, since roughly a fifth of the world’s oil flows through the strait.

That escalation pushed oil prices to a one-month high, with Brent crude jumping as much as 3.8% at one point to trade near $86 a barrel — about 19% above where it stood before the conflict first erupted earlier this year. Higher energy costs add a fresh headwind for consumers and businesses just as broader inflation had been showing signs of cooling.

On that front, June’s inflation data came in better than expected. The Consumer Price Index fell 0.4% for the month, pulling annual inflation down to 3.5% from 4.2% in May — the first monthly decline since April 2020. The primary driver was the fall in gasoline and energy prices before the latest Iran flare-up. Core CPI, which strips out food and energy, rose just 2.6% year over year in June, also below forecasts. The Producer Price Index told a similar story, falling 0.3% in June on the back of a sharp drop in energy costs, though wholesale prices remained up 5.5% from a year ago.

The encouraging inflation print gave new Fed Chair Kevin Warsh a stage to make his case to Congress this week. In testimony before the House and Senate, Warsh pledged a “regime change” in Fed policy, criticized the central bank’s 2020 shift to flexible inflation targeting as a mistake, and promised the inflation surge of recent years would become “a thing of the past.” He cautioned that one good CPI report doesn’t mean “mission accomplished,” and pointed to the ongoing AI infrastructure buildout as a major force reshaping the economy — while insisting he’ll keep the Fed independent of White House pressure.

To us, the duration of this renewed conflict between the U.S. and Iran, its impact on energy prices and the potential for it to spur another round of output price increases is firmly on our radar. The same goes for the number of vessels crossing the Strait of Hormuz and the risk that poses to global supply chains.

In addition to those renewed market pressures, it was the tech sector that dominated the headlines late in the week. We saw a steep selloff in semiconductors, the worst stretch for the group since last year’s tariff-driven meltdown, which dragged the Philadelphia Semiconductor Index into bear-market territory as investors grew nervous that AI-related chip spending has gotten ahead of itself.

We saw this nervous market mood firsthand with the steep selloff in IBM (IBM) shares that followed the company’s Q2 2026 earnings pre-announcement that showed a relatively modest miss relative to market expectations. It reared its head again on Friday, with the double-digit fall in Netflix (NFLX) shares after the streaming giant guided current-quarter EPS to $0.82, $0.02 below the market forecast. As we called out in our Alert discussing the quarter, the market seemed to miss that $0.82 figure would be up ~39% year over year.

When we’ve faced periods of rising anxiety in the market, the strategy that has served us well has been to slow things down, take stock of what we own in the Portfolio, double and even triple check the underlying thesis and focus on the medium to longer-term horizon. In particular, the next two weeks will give us a tremendous amount to think about as hundreds of companies report their latest quarterly results and update their guidance for the back half of the year.

Odds are there will be some bumps along the way, but we will look for helpful data points across the Portfolio’s holdings. Given the pressures on the tech sector, we will be especially tuned into comments about AI adoption and usage. Not to steal any thunder from Saturday’s signals Alert, but for those of us that have our ear to the ground, we continue to see favorable developments not only for AI adoption and usage but for the other strategies powering the Portfolio’s holdings.

Against that backdrop, we will continue to look for compelling opportunities to put capital to work in our existing positions at favorable risk-to-reward trade-offs, as well as new opportunities for the road ahead.

Enjoy your weekend. We’ll see you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

As we discussed, it was a rough week for the market and the Pro Portfolio, but even after the battering delivered over the last several trading days, the Portfolio remains well ahead of the S&P 500 on a year-to-date basis.

While our positions in Applied Materials (AMAT), Axon (AXON), Marvell (MRVL), Neostellar (NSLR), and the EPS All-Stars basket weighed on the Portfolio performance this week, as did Broadcom (AVGO) and Arista Networks (ANET), that impact was blunted by gains in positions outside the tech sector. Those included Welltower (WELL), Waste Management (WM), Paccar (PCAR), TJX (TJX), Costco (COST) and Bank of America (BAC).

Turning to some of the moves we made this week with the Portfolio, on Monday, we increased our Apple (AAPL) price target. Tuesday, we not only picked up additional shares of Neostellar, Marvell and Boeing (BA), we also bumped up our price target for First Trust Nasdaq Cybersecurity ETF (CIBR). Our decision for the latter was reaffirmed by the late-week announcement by Coca-Cola (KO) that its Fair Life operation was impacted by a cyber-attack, one that was hobbled production levels.

Thursday, despite the bump up earlier in the week for our Apple price target, we prudently took advantage of the strong move in the shares and the newfound overbought condition to lock in some gains and funnel the proceeds into the shares of TJX. As we made that move, we also lifted our rating on TJX to One from Two. On Friday, after digesting the quarterly results and guidance from Netflix (NFLX), we downgraded the shares to a Three rating and reduced our price target to $85 from $115. We explained the rationale behind both of these moves in our post-earnings Alert, which also touched on the upcoming catalysts that could lead us, as well as others on Wall Street, to revisit the stock and their newfound “show me” state.

Exiting the week the Portfolio’s cash position stood at around 8.5% and that gives us a decent amount of firepower to be opportunistic in the coming days and weeks as we move through the current earnings season. When we shared our updated Portfolio table of key metrics on Thursday, we called out some of the cheap PEG ratio valuations across our chip holdings.

In Friday’s video we discussed that there are likely those across Wall Street who are seeing these valuations as well. That leads us to think that we could see value buyers stepping into the names before too long, and we would look to be among them subject to two things. One is what we learn when Google (GOOGL) and the other hyperscalers report next week and the following one. The other is the technical setup and support levels for the S&P 500 and Nasdaq Composite discussed in Friday’s video and further up in this edition of the Weekly Roundup.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday, July 13: KeyBanc raised its Nvidia (NVDA) target to $330 from $310 following a channel check trip to Asia that found strong AI data center chip demand. KeyBanc also boosted its Marvell target to $400 from $385. Citi increased its United Rentals (URI) target to $1,270 from $1,210 following strong construction and related end markets.

Tuesday, July 14: Jefferies raised its Bank of America target to $75 from $70.

Wednesday, July 15: Keefe Bruyette upped its Bank of America target to $70 from $67, while Wells Fargo nudged its BAC target to $69 from $67 and Baird took its to $62. Wells Fargo also trimmed its Microsoft (MSFT) target to $625 from $650. Evercore ISI lifted its Microsoft target to $525 from $510.UBS lifted its Applied Materials target to $705 from $570.

Thursday, July 16: Goldman Sachs increased its target price for Morgan Stanley (MS) shares to $241 from $233, while Keefe Bruyette upped its to $250 from $225. Barclays took its MS target to $262 from $230. Wedbush resumed coverage of Alphabet with an Outperform rating and $445 price target, an gave an Outperform rating on Amazon (AMZN) with a $293 target, and a $671 target for Meta (META). KeyBanc nudged its AMZN target to $335 from $330. Wells Fargo bumped up its target for Arista Networks to $200 from $185. Scotiabank raised its Waste Management target to $260 from $250.

Friday, July 17: Alongside our price target cut and rating downgrade for Netflix shares, others across Wall Street cut their targets to $83-$95 from $100-$130. Citi upped its Morgan Stanley target to $235 price target from $220, and HSBC upgraded Apple shares to Buy and took its price target to $366 from $260. Ahead of next week’s earnings report, BMO Capital raised its Alphabet target to $455 from $435. Rounding out the day, Morgan Stanley bumped up its United Rentals target to $1,165 from $1,030, also ahead of URI’s earnings report next week.

Portfolio Videos

Monday, July 13 – Our Roadmap for Big Bank Earnings

Tuesday, July 14 – Stocks & Markets Podcast: Regenerative Medicine’s Next Leap with Conexeu Sciences CEO

Wednesday, July 15 – Assessing the Pressure on 2 Portfolio Holdings

Friday, July 17 – Our Game Plan for a Nervous Stock Market

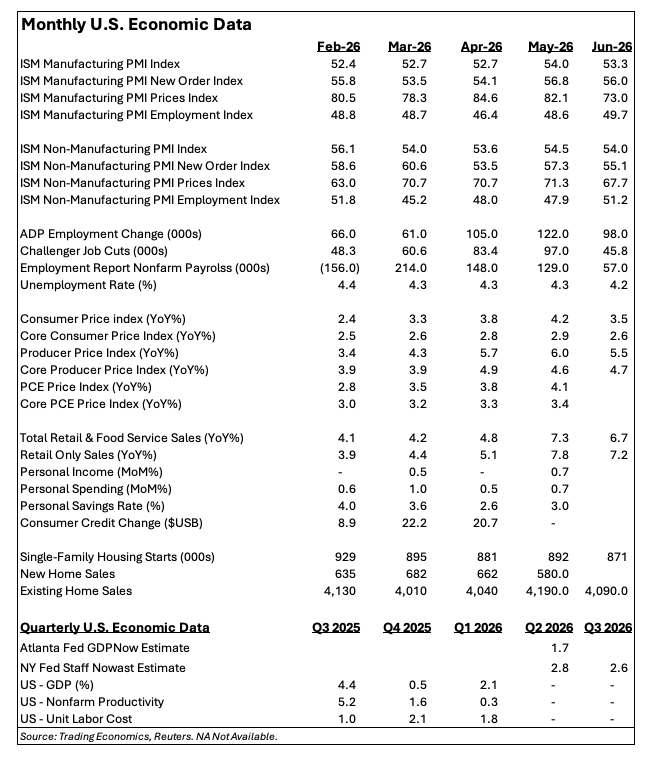

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period’s reading, and T-2 is two periods back, the intent being to illustrate any trends.)

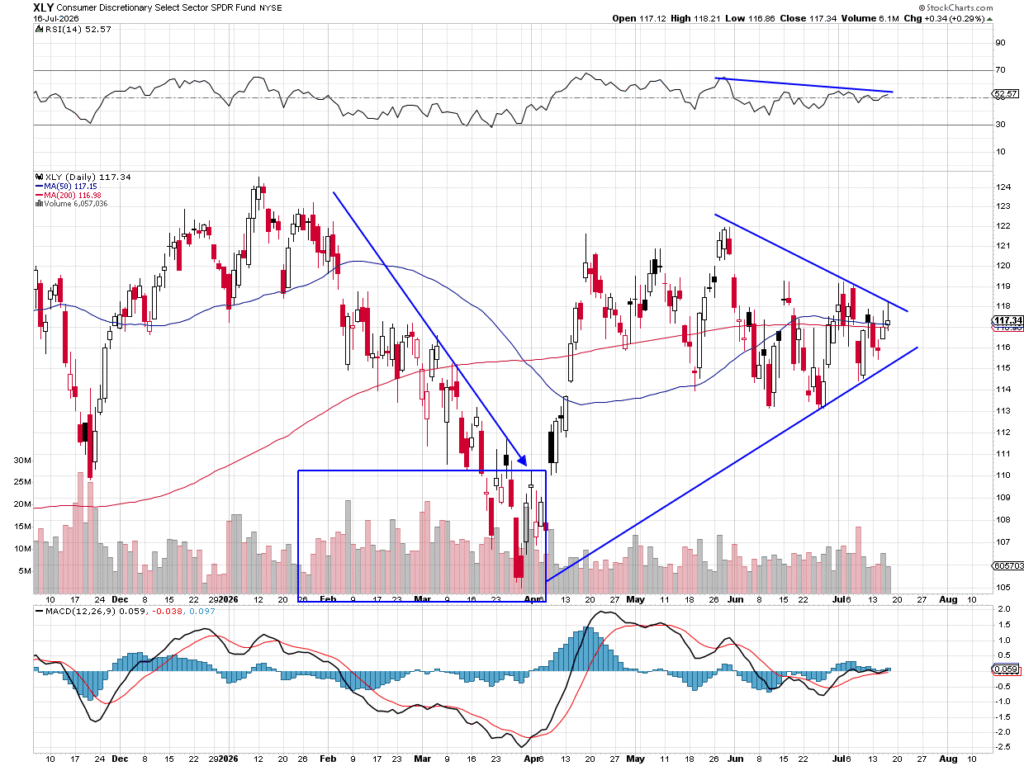

Chart of the Week: Consumer Discretionary Select Sector SPDR Fund ETF (XLY)

Consumer discretionary names have started to make some noise. With some weakness in markets there is a chance this group pulls back, but all signs point to that move lower being a buying opportunity.

What is consumer discretionary? We look at the XLY, the State Street Consumer Discretionary Select Sector SPDR Fund ETF, to determine the health of the consumer, and after the positive reading in June retail sales it seems the consumer remains resilient and is spending.

The two biggest weightings in the XLY are Amazon (AMZN) and Tesla (TSLA), which make up a whopping 41% of the ETF. That is huge, but other stocks in the ETF are also big consumer names like Home Depot (HD), McDonald’s (MCD), TJX Companies (TJX), Lowe’s (LOW), Starbucks (SBUX) and several hotel and travel companies. Collectively, these discretionary names tell us how strong the economy is from a retail view, considering about 70% of GDP is personal consumption expenditures.

We may learn more about consumer spending patterns when these companies release earnings over the next six weeks.

Of course, when oil/gas prices were elevated in the spring due to the Iran war many consumers were strapped for spending. We see on the chart during that time the XLY had a devastating move down, dropping some 15% lower on heavy turnover. It seemed obvious, at the time, the consumer was going to struggle, but those concerns were allayed quickly and the XLY rebounded.

Currently, the XLY is in a tough spot to predict upside or downside. We call this a “no man’s land,” where you don’t want to buy or sell the ETF. Eventually the XLY will break, and the longer it stays above important support such as the 50- and 200-day moving averages, the better chance that next move will be higher.

Notice how strong turnover was in the spring but now it currently is a fraction of those levels. With price levels now about neutral it tells us the market believes the XLY is fairly priced.

MACD is on a tepid buy signal, while relative strength is neutral. The chart shows a series of lower highs and higher lows, which is no trend. The range between $113 and $122 is firm, so we’ll be watching to see which direction the XLY moves.

Other charts we shared with you this week were:

Monday, July 13: S&P 500 – New Highs Are Very Close as Bulls Regain Control

Monday, July 13: Morgan Stanley (MS) – Morgan Stanley is Ready for Prime Time

Tuesday, July 14: Lumentum (LITE) – ‘All-Star’ Gets Caught Up in Sector Selling Storm

Wednesday, July 15: Apple (AAPL) – Can Apple Get Some Praise?

Thursday, July 16: Amazon (AMZN) – Don’t Look Now, But Amazon Is Making Its Move

The Week Ahead

We have another frenetic week ahead of us, one that will primarily driven by another notch up in the volume of quarterly earnings reports. We say that because, over the weekend, the Federal Reserve enters its quiet period ahead of its next monetary policy meeting that will conclude on July 29. As of now the market expectation is that the Fed will leave interest rates unchanged following that meeting, a thought that was furthered by comments this week from Fed Chair Kevin Warsh.

During the week we shared with you the reasons for our concerns about what’s next for inflation-facing data, given the re-escalation of military strikes between the U.S. and Iran, the rebound in oil, diesel, gas and other petrochemical prices, and the decline in vessels crossing the Strait of Hormuz. That is why among the various data points for the economy that will be published next week, we will be focusing on what is revealed in the Flash July PMI data published by S&P Global.

In addition to what the Flash PMI report says about input prices and output prices, it will also help frame initial GDP expectations for the current quarter as well as upcoming July employment figures. Those insights should be helpful as we get ready for that July 29 Fed policy meeting, but also as we prepare for the initial Q2 2026 GDP reading.

Here’s a closer look at the economic data coming at us next week:

Monday, July 20

U.S.

CB Leading Index – June (10:00 AM ET)

Tuesday, July 21

ADP Employment Change Report – Weekly (8:15 AM ET)

Wednesday, July 22

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, July 23

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Chicago Fed National Activity Index – June (8:30 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, July 24

S&P Global Flash PMI – July (9:45 AM ET)

New Home Sales – June (10:00 AM ET)

International

Tuesday, July 21

UK: Unemployment Rate, Employment Change – May

Eurozone: ZEW Economic Sentiment Index – July

Wednesday, July 22

Japan: Imports/Exports – June

UK: Inflation Rate – June

Thursday, July 23

UK: CBI Business Optimism Index – Q3 2026

UK: CIB Industrial Trends Orders – July

Eurozone: European Central Bank Interest Rate Decision

Eurozone: Consumer Confidence Flash – July

Friday, July 24

Japan: S&P Global Flash PMI – July

Eurozone: S&P Global Flash PMI – July

UK: S&P Global Flash PMI – July

UK: Retail Sales – June

Nearly 500 companies are expected to report next week, including 86 S&P 500 constituents. So far, roughly 10% of S&P 500 companies have reported and generally speaking we’ve seen positive EPS and revenue surprises. There have also been examples where modest shortfalls relative to consensus expectations have sent stocks tumbling. Included among those were IBM (IBM) and Pro Portfolio holding Netflix (NFLX).

By the time we wrap up next week, approximately 27% of the S&P 500 will have reported. While that is still quite a bit from the halfway mark, what we see should give us an indication whether the market’s expectation for nearly 25% year-over-year EPS growth for the S&P in Q2 2026 is likely. As we field those earnings reports and conference call comments, we will continue to tie back our learnings to the Portfolio’s positions and, if needed, make any adjustments necessary. Because the three Portfolio companies that are reporting next week — Alphabet (GOOGL), United Rentals (URI) and American Express (AXP) — are doing so in the back half of the week, we aim to do quite a bit of that dot-connecting on Monday and Tuesday.

In Friday’s Portfolio video we explained why quarterly results and guidance from Alphabet will be a big moment for the market next week. We will once again focus on the various line items in the report, what they tell us about the Search and Advertising business, but we expect the market’s focus will be on Google Cloud, its conversion of backlog to revenue, margins, and capital spending plans. We would not be surprised if, given the current market mood, Alphabet opts to simply reiterate its existing 2026 capital spending plans. Normally the market would cheer another leg up in that spending, however, this time around our thinking is the company would get more kudos for showing it will be disciplined in adding AI and data center capacity.

In terms of United Rentals, project activity and weather improved in Q2 2026 compared to Q1 2026, and that bodes well for rental demand and equipment uptime. Over at American Express, consumer spending has remained robust and indications late in the quarter from management signaled favorable developments on the Platinum Card Refresh. When we dig into Amex’s earnings, once again, one of our key areas of focus will be on the growth in the number of cards in force and average fee per card, as well as management’s comments on both for the second half of the year.

Here’s a closer look at the earnings reports coming at us next week:

Monday, July 20

Open: Domino’s Pizza (DPZ)

Close: Steel Dynamics (STLD)

Tuesday, July 21

Open: 3M (MMM), Charles Schwab (SCHW), DR Horton (DHI), Danaher (DHR), Hasbro (HAS), Northrop Grumman (NOC), Synchrony Financial (SYF)

Close: Alaska Air (ALK), Interactive Brokers (IBKR)

Wednesday, July 22

Open: AT&T (T), Cal-Maine Foods (CALM), GE Vernova (GEV), Philip Morris International (PM), Pulte Group (PHM)

Close: Alphabet (GOOGL), CSX (CSX), IBM (IBM), Packaging Corp. (PKG), ServiceNow (NOW), Tesla (TSLA), Texas Instruments (TXN), Waste Connections (WCN)

Thursday, July 23

Open: Albertsons (ACI), Ameriprise Financial (AMP), Comcast (CMCSA), Dow (DOW), Honeywell (HON), Lazard (LAZ), Lockheed Martin (LMT), Mobileye Global (MBLY), Quest Diagnostics (DGX), ST Microelectronics (STM), Union Pacific (UNP)

Close: Boston Beer (SAM), Digital Realty Trust (DLR), Imax (IMAX), Intel (INTC), SAP SE (SAP), United Rentals (URI)

Friday, July 24

Open: American Express (AXP), Booz Allen Hamilton (BAH), Lamb Weston (LW), NextEra Energy (NEE)

Portfolio Investor Resource Guide

Economic Data: Here’s a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company’s Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here’s How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 – Buy Now (BN): Stocks that look compelling to buy right now.

2 – Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 – Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 – Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.