AI Giants Begin to Appear Defenseless

As I look out to the major artificial intelligence names, I see something missing: a moat.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

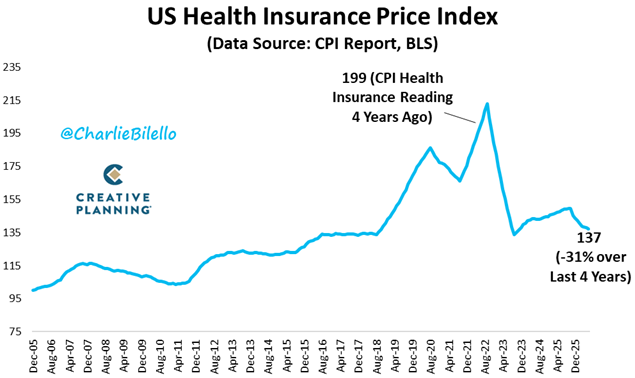

The market has benefited from lower-than-expected June consumer price index and producer price index readings this week. But there are a couple of caveats with these readings. First, statistics such as the monthly jobs numbers put out by the Bureau of Labor Statistics have been notoriously unreliable in recent years. I would also take any reading that includes the preposterous take that health care premiums have fallen 31% over the past four years with a grain of salt. Second, energy prices have rallied higher this week as the conflict with Iran has erupted again this week, cutting traffic through the Strait of Hormuz. No long term solution to restoring transit through this critical global choke point seems on the near-term horizon. The fall in inflation levels might prove to be temporary.

Tech spending around the build-out of AI infrastructure continues to be the primary driver of both the U.S. economy and equity markets. Without this surge in this spending, both fixed capital investment and construction spending would be at levels typical in recessions. The AI Revolution, however, does have some downsides. The need to embrace AI is cannibalizing other parts of company’s tech budgets.

This was on full display this week within the dismal quarterly results from IBM Corporation (IBM) that sparked an approximate 25% selloff in the shares. Management attributed the disappointing numbers to “slower software spending, delayed large deals, and softer mainframe demand as enterprise customers prioritize AI infrastructure investments.”

Surging prices on computer memory, thanks to hyperscaler demand, have forced Apple (AAPL) to raise prices across their product portfolio significantly and Goldman Sachs to cut its global PC shipments forecast.

Hyperscalers like Amazon (AMZN) and Alphabet (GOOG) in the early years of the AI infrastructure, funded their capital budgets from the cash on their balance sheets and free cash flow. And both have fallen dramatically in recent quarters as capital expenditure budgets have ballooned, they are turning more and more to the equity and debt issuance to fund this spending. Oracle’s (ORCL) long-term debt surged over 40% in its just concluded fiscal year to just north of $120 billion.

And the markets appear to be starting to choke on all this issuance. You can see this around Space Exploration Technologies Corp. (SPCX). The stock has now round tripped and trades at the same level as where the company raised $85 billion worth of proceeds just over a month ago. During the decline from its post IPO highs, the stock has eviscerated just over $1 trillion of valuation. The $25 billion of bonds SpaceX floated less than two weeks after its IPO are not behaving well recently either.

And roughly half of the capacity the hyperscalers are building is for just two companies; Anthropic and OpenAI. Anthropic is looking to go public sometime this fall at roughly a $1 trillion valuation. OpenAI is speculated to be targeting early 2027 for a similar move. Both companies are far from profitable and OpenAI has burned through more money and faster than any startup in history.

The bigger problem for both AI language model enterprises is this: Since both names move their frontier AI models from a subscription-pricing model to a usage-priced model, it is becoming more obvious that neither OpenAI or Anthropic may have much of a moat to their businesses. Much cheaper Chinese models from the likes of Deep Seek have rapidly gained market share in powering AI token use. And it is easy to see why, given these Chinese models can provide most of the capability of the newest frontier models at 10 cents on the dollar.

In addition, both Grok and Muse Spark 1.1 from Meta Platform (META) are also offering much lower priced AI models. Unlike enterprise software from the likes of Salesforce (CRM), there is little cost or effort involved for companies moving from one AI model to another.

And there here Is the $64,000 question for the markets: How are Anthropic and OpenAI going to meet the massive commitments they have made to the hyperscalers for future compute power given the lack of longer-term moats to the businesses? How will they ever become profitable? I don’t see positive answers to those questions, so my portfolio remains positioned quite conservatively.

At the time of publication, Jensen was long AMZN.