Weekly Roundup: Portfolio Extends Lead, Adds Firepower Ahead of Earnings Season

We locked in gains on three holdings, giving our cash levels a boost as the Q2 earnings season heats up.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The first full week of trading for the new quarter had a little of everything: a geopolitical shock, a hawkish turn in Fed expectations, a marquee IPO, and another leg up in the AI trade. By Friday’s close, the S&P 500 and Nasdaq had both notched gains of roughly 1% to 2% on the week, and the Dow squeezed out a fresh record close near 53,000. That came in the face of one the market’s worst single sessions of the summer on Wednesday.

One factor that pushed the market and the Pro Portfolio higher week over week was the AI and chip stocks. Broadcom (AVGO) extended its custom-chip partnership with Apple (AAPL) through 2031, and Applied Materials’ (AMAT) CEO talked up multi-year visibility into chip demand — comments that sent the stock sharply higher and drew multiple price-target increases. Meta’s (META) custom AI silicon chip plans added to our positive stance on AVGO shares.

Shares of SK Hynix (SKHYV) made their Nasdaq debut with the ADRs pricing at $149 and opening around $170. Late Friday, SK Hynix CEO Kwak Noh-Jung said that he sees the memory chip shortage persisting beyond 2030. That keeps us bullish on our AI and data center chip positions and brings another layer of support for AMAT shares.

Other positives this week included preliminary North American net orders for Class 8 heavy duty trucks surging in June. That makes us increasingly bullish on Paccar (PCAR) one of our newer positions. Boeing’s (BA) June aircraft deliveries do the same for our view on BA shares as does the expectation for the FAA to approve its 737 MAX 7 aircraft in the coming weeks.

Wednesday was the week’s clear stress test. President Trump declared the Iran ceasefire “over” after the U.S. launched fresh strikes, and the market reaction was immediate: oil jumped roughly 5%, and the Dow fell 1.5% on the day. While fighting continued on Thursday, on Friday no attacks were reported and that is giving the market some cautious optimism that peace talks may get back on track. Our focus will remain on the volume of ships passing through the strait and what that means for energy prices and supply chain disruptions. So far, the full reopening of the strait has been delayed.

Tariffs remained a persistent, if lower-grade, overhang. The current 10% global baseline tariff is set to expire July 24, with the administration threatening to raise it to 15%, and Trump added a fresh threat of a 35% tariff on Canada on Friday. Layered on top of that, midweek FOMC minutes showed a more hawkish tilt than some may have expected. However, we’ve seen June inflation data since that meeting start to trend lower indicating May was the likely peak.

We continue to think that if upcoming inflation data for June, July and August continue that trend, the market may need to revisit expectations for multiple rate hikes in coming quarters. As of Friday, the CME FedWatch Tool shows the market currently sees two rate hikes between now and Q1 2027. In our view, such a reset would be a tailwind for the market, provided a rollover in the jobs market doesn’t accompany it.

And as the market trended higher this week, by Friday, the Volatility Index (VIX) fell to one of its lowest levels so far this year. We are likely to see volatility return to the market as the Q2 2026 earnings season heats up next week and even more so in the following ones. We raised some cash this week by doing some opportunistic register ringing, and below we’ve updated our Portfolio shopping list.

We will remain prudent but on the lookout for favorable risk-to-reward opportunities should they present themselves. As the earnings season heats up, we’ll continue to watch key support levels for the S&P 500, the Nasdaq Composite and the Portfolio’s holdings. And with that in mind, we’ll be sharing an updated table of relative strength index levels, checkpoints and pick-up points early next week.

Enjoy your weekend, and we’ll see you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

The Pro Portfolio put in another positive week, extending its early lead over the S&P 500 for the current quarter, and continuing the outperformance against that market index on a year-to-date basis. Several holdings powered that aggregate month-to-date move, including Meta (META), Arista Networks (ANET), Palantir (PLTR), Morgan Stanley (MS), Apple (AAPL) and Broadcom (AVGO).

Drags on the Portfolio included Applied Materials (AMAT and Marvell (MRVL), and Neostellar (NSLR). To that we can also added the recently reconstituted EPS All-Stars, which after seven trading days for the new basket is in the red. While these positions have moved against us in the short-term, our focus remains on the medium to longer-term. For Applied, we are seeing increasing capex levels from key customer such as Samsung (SSNLF), SK Hynix (SKHYV), and Micron (MU). For Marvell, ramping custom AI silicon programs and demand for networking chips keep us bullish on the shares. As for the EPS All-Stars, the upcoming earnings season should be a catalyst for multiple holdings in the basket, including Ciena (CIEN), Micron, Lumentum (LITE) and others.

In terms of trades, things were relatively quiet with the Portfolio for the first few days of the week but on Wednesday, following renewed tension in the Middle East between the U.S. and Iran, and President Trump declaring the ceasefire over, we opted to do some opportunistic profit taking. That led us to shed some shares of Axon (AXON), Bank of America (BAC), and Labcorp (LH). That profitable move increased the Portfolio’s cash position to roughly 9.5% of its assets, lifting our firepower as we move into the Q2 2026 earnings season.

Later in the week we indicated that Costco (COST), Neostellar (NSLR), Bank of America, Boeing (BA), and Paccar (PCAR) are among a select list of positions on our radar screen. We’ll add Marvell to that list as well following the 28% drop in the shares over the last few weeks. That decline reaffirms the Portfolio’s decision to lock in some massive gains on the shares in June. As we move into the busy hiring season, we will continue to look out for fresh opportunities for both the Portfolio and the Bullpen.

In Friday’s Portfolio video we also indicated that we are aware that shares of Apple, Arista Networks, the First Trust NASDAQ Cybersecurity ETF (CIBR) and Welltower (WELL) are at or above our existing price targets. In our view, the next few weeks should bring sufficient fresh information that will allow us to revisit those targets, most likely with an upward bias.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday, July 6 – Applied Materials received a big price target increase at Morgan Stanley to $647, up from $502. Arista Networks fetched two price target increases to $200 from BofA and KeyBanc, while Morgan Stanley reiterated its $190 target. Evercore ISI increased its American Express target to $380 from $345 and took its Morgan Stanley target to $233 from $210. Goldman Sachs also lifted its Morgan Stanley target to $233 from $211. Wolfe Research established a new Microsoft target at $525, and Citi pushed its United Rentals (URI) target to $1,210 from $1,130.

Tuesday, July 7 – Barclays boosted its Amex target to $364 from $322, while UBS hiked its to $386 from $340. Shares of Morgan Stanley received two price target increases, one from BofA to $250 from $225, the other from UBS to $255 from $214. CIBC upgraded its rating on the shares of Waste Management (WM) to Outperform from Neutral, resetting its target at $244.

Wednesday, July 8 – TD Cowen initiated coverage on Amazon with a $340 target.

Thursday, July 9 – JPMorgan Chase trimmed its Costco (COST) price target by $10 to $1,100 but maintained its Outperform rating.

Friday, July 10 – Stifel lifted it price target for Applied Materials to $650 from $530. KeyCorp reset its Google (GOOGL) target at $445, and Morgan Stanley nudged its Nvidia (NVDA) target by $3 to $288.

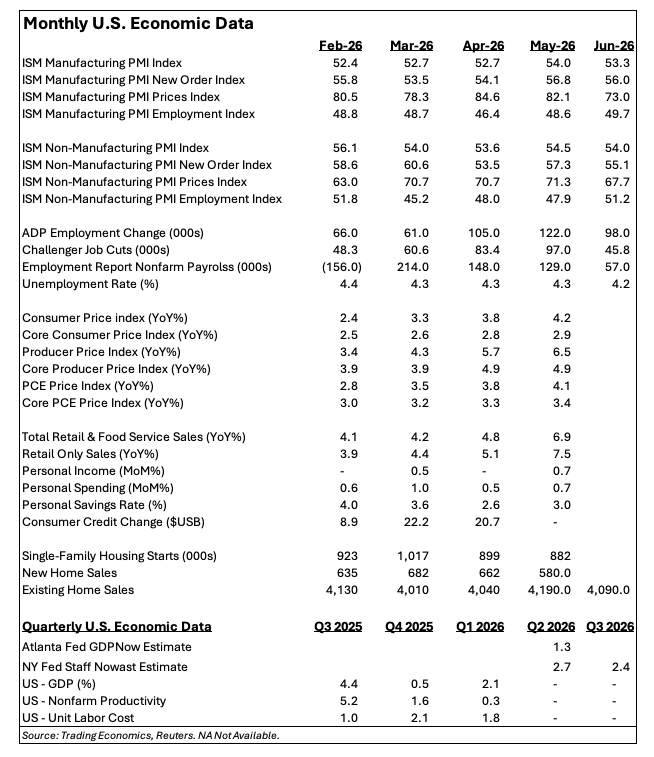

Key Global Economic Readings

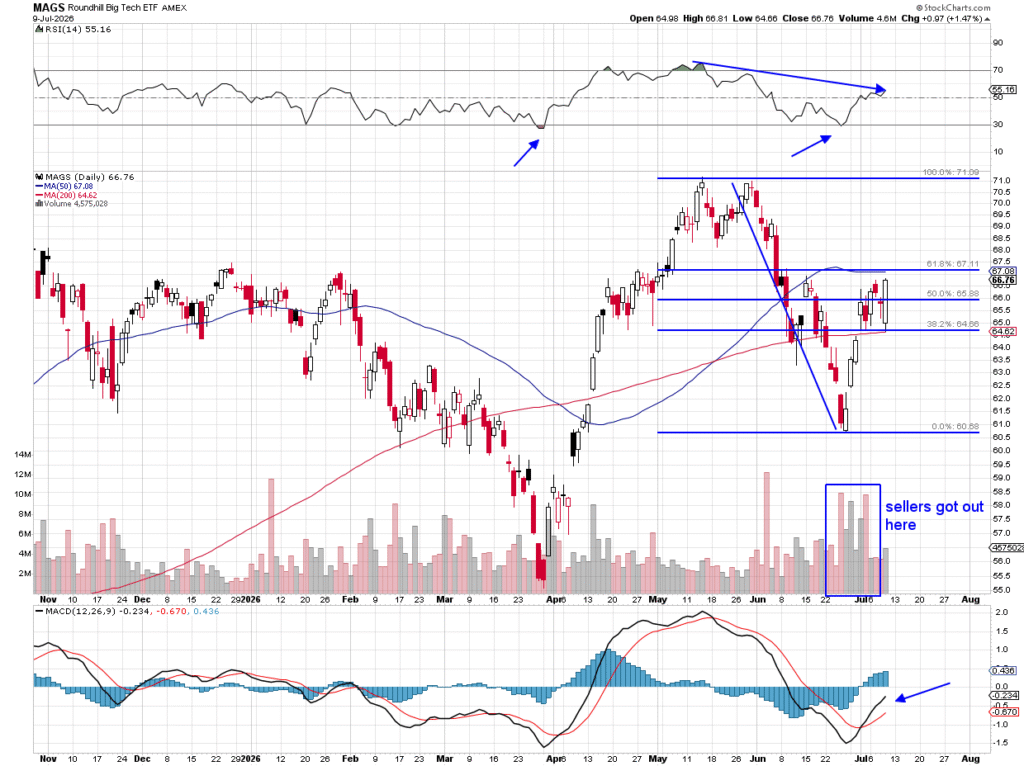

Chart of the Week: The Roundhill Big Tech ETF

With all the talk about the wild semiconductor names and the hot IPO market, can you believe the biggest group of all is being ignored? That’s right, the Magnificent Seven, representing the seven biggest stocks on the planet and contained in the Roundhill Big Tech ETF (MAGS). This group had been lagging badly since a massive breakdown that started in mid-May. That swoon saw the MAGS fall a staggering 15% in just a over a month. To put that into perspective, the Mag 7 names lost about 4 trillion dollars in value during that timeframe, which is roughly the GDP of India, England or Japan. Stunning!

Well, just as stocks can easily fall, they can easily rebound. Nobody ever said these stocks would grow to the sky, nor did anyone say they would fail. But a few of these names are knocking on the door of new highs while others are close to a breakout. No doubt with earnings season coming around the likes of Apple (AAPL), Microsoft (MSFT), Meta (META), Alphabet (GOOGL) and Amazon (AMZN) are going to be in demand.

After that catastrophic failure from the highs in May the MAGS fell through good support of the 50- and 200-day moving averages. A bottom was put in place when the RSI reached an extreme oversold level of 30. Last time this happened the MAGS went on an historic run higher. Bargain hunters came in and started picking at Nvidia (NVDA), Meta, Microsoft and Tesla (TSLA).

MACD is now on a buy signal crossover, and the action on July 9 was very positive, with a very long candle, outside day, bouncing off the 200-day moving average and finishing at the highs of the session. Better volume as well.

With earnings out for most of these names in the back half of July, keep a close eye here on this ETF. It’s already gained back half the losses and could make a run to those highs by the end of the month and before MAGS gets overbought.

Other charts we shared with you this week were:

Monday, July 6: S&P 500 – Index Continues to Grind, but Money Is Moving

Monday, July 6: Marvell (MRVL) – Marvell Is Taking a Breather

Tuesday, July 7: Bank of America (BAC) – A Close Look at Bank of America as Earnings Approach

Wednesday, July 8: Rocket Companies (RKT) – This All-Star Is Waiting for a Catalyst

Thursday, July 9: Bloom Energy (BE) – Bloom Energy’s Pullback Could Be Just What the Bulls Needed

The Week Ahead

The pace picks up next week with second-quarter 2026 earnings season getting underway, several key pieces of June data, and an appearance by Fed Chair Kevin Warsh. Yeah, it’s going to be a busy few days and while we dig through all of that, we’ll continue to keep a watchful eye over key technical levels for the S&P 500, the Nasdaq Composite, and the Pro Portfolio’s holdings.

To be clear, we are not expecting Warsh to say very much about the future of monetary policy on Tuesday. More likely he is going to reiterate his view that folks should be following the data, the way we do here at the Pro Portfolio. With that in mind we will want to scour the June Consumer Price Index report that will be published earlier on Tuesday and ahead of Warsh’s testimony.

As we close out this week, the market’s expectations for headline CPI are for it to dip to around 3.9% on a year-over-year basis compared to the May reading of 4.2%. Looking at core inflation, that is expected to hold steady at 2.9%. Given the fall in gas prices and related ones, we could see the headline CPI dip a little more than the market is expecting. If so, that would be welcome news for the market and could lead to another rethink on the number of rate hikes the Fed is expected to deliver over the coming quarters. With that in mind we will want to see what Warsh has to say about the data if asked.

On Wednesday we will get the June Producer Price Index data. The consensus forecast for that shows headline PPI dipping modestly compared to the 6.5% year-over-year figure posted in May. The core figure, however, is expected to remain flat at 4.9%. Based on what we saw in the price components for the June ISM manufacturing and services PMIs, there is reason to think those June PPI figures could come in softer than the market expects. With the lag time between PPI data and CPI data, we will continue to track PPI data closely as we revisit inflation expectations and monetary policy.

Next week also brings the June Retail Sales figure, which should benefit from Amazon’s Prime Day 2026 that ran from June 23 through the 26th. The greatest impact will be on the non-store retail sales figure, but we will also be taking note of other categories and what they tell us about various category spending in the second quarter as we get ready for companies to report over the ensuing weeks. We also have the latest housing starts and building permits data coming at us and when we parse that data for June, we will continue to focus on single-family housing data. That includes housing starts data but also the number of units authorized but not started and the number of units under construction at the end of the month compared to prior ones.

Here’s a closer look at the economic data coming at us next week:

U.S.

Tuesday, July 14

NFIB Business Optimism Index – June (6:00 AM ET)

ADP Employment Change Report – Weekly (8:15 AM ET)

Consumer Price Index – June (8:30 AM ET)

Fed Chair Warsh Testimony (10:00 AM ET)

Wednesday, July 15

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Producer Price Index – June (8:30 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Fed Beige Book (2 PM ET)

Thursday, July 16

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Retail Sales – June (8:30 AM ET)

NY Fed Services Activity Index – July (8:30 AM ET)

Philly Fed Index – July (8:30 AM ET)

Pending Home Sales – June (10:00 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, July 17

Housing Starts & Building Permits – June (8:30 AM ET)

Import/Export Prices – June (8:30 AM ET)

Industrial Production – June (9:15 AM ET)

Michigan Consumer Sentiment (Prelim.) – July (10:00 AM ET)

International

Tuesday, July 14

China: Imports/Exports – June

Japan: Industrial Production – May

Wednesday, July 15

China: GDP – Q2 2026

China: Industrial Production, Retail Sales, Fixed Asset Investment, Loan Growth – June

Eurozone: Industrial Production – May

Thursday, July 16

China: Foreign Direct Investment – June

UK: Industrial Production, GDP – May

Friday, July 17

Eurozone: Consumer Price Index – June

As we discussed in Friday’s Portfolio video, earnings season indeed heats up next week and we have three companies in the Portfolio reporting — Bank of America (BAC), Morgan Stanley (MS) and Netflix (NFLX). Based on the level of investment banking activity and volatility during Q2 2026, we should see solid prints from both Bank of America and Morgan Stanley. When they report, we will be interested in updated comments about net interest income expectations for 2026 as well as comments about their investment banking backlog levels and how they see that activity unfolding in the back half of the year. We will be cross-referencing those findings against those from JP Morgan Chase (JPM), Goldman Sachs (GS), and others reporting next week

With Bank of America in particular, we will be looking to see if the company delivers more on its dividend following the successful completion of the Fed’s latest annual stress test. Shortly after those test results were announced Morgan Stanley increased its quarterly dividend while Bank of America said it would be making more news on that front following an upcoming board meeting.

Turning to Netflix, our view following the company’s Q1 2026 results was that its guidance for the current quarter was skewed conservative given its latest subscription price increase. We’ll be looking to see if the company plans to extend that price increase to markets outside the U.S. but also will be interested in any comments about the growing influence of advertising revenue across its total revenue stream. And it goes without saying that because content is king, we will be looking for more insight on the company’s second-half slate of programming.

In addition to those three quarterly earnings reports, we will also be closely following what is reported by Taiwan Semiconductor (TSM), considering its role in the semiconductor ecosystem. To us, the composition of Taiwan Semi’s revenues across its various segments and what they tell us about the different categories of chip demand, including AI and data center, smartphone, other connected device markets will be one of our areas of focus. The same goes for the outlook ahead and what that tells us about demand and revenue prospects for our various chip holdings in the Portfolio.

Turning to the Portfolio’s position in Applied Materials (AMAT), with rumblings of companies discussing available capacity with Intel (INTC) and Samsung (SSNLF), we will be very interested in what Taiwan Semiconductor has to say about its near-term and longer-term capital spending plans. Should we see Taiwan Semi increase its capital spending budget, on the back of higher capital spending levels at Micron (MU), Samsung, and SK Hynix (SKHYV), it would be yet another positive data point for our AMAT shares.

We will also continue to roll up our sleeves and connect learnings from other companies reporting back to the Portfolio while we keep an eye out for earnings pre-announcements and what they may tell us. For example, during Friday’s earnings conference call from Delta Air Lines (DAL), the management team had a number of positive things to say about its relationship with American Express (AXP). The Delta team said that card spend for its Amex-branded cards has grown double digits for seven straight quarters, with particular strength among premium cardholders.

Here’s a closer look at the earnings reports coming at us next week:

Monday, July 13

Open: Fastenal (FAST)

Tuesday, July 14

Open: Bank of America (BAC), Citigroup (C), Ericsson (ERIC), Goldman Sachs (GS), JPMorgan Chase (JPM), Wells Fargo (WFC)

Wednesday, July 15

Open: ASML (ASML), BlackRock (BLK), BNY Mellon (BNY), Cintas (CTAS), Conagra (CAG), Johnson & Johnson (JNJ), Morgan Stanley (MS), PNC (PNC)

Close: JB Hunt (JBHT), United Airlines (UAL)

Thursday, July 16

Open: Abbot Labs (ABT), GE Aerospace (GE), Manpower (MAN), UnitedHealth (UNH)

Close: Alcoa (AA), Netflix (NFLX)

Friday, July 17

Open: Autoliv (ALV), Fifth Third Bank (FITB), Travelers (TRV)

Portfolio Investor Resource Guide

Economic Data: Here’s a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company’s Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends – How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics – Everyone Wants a Value. Here’s How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 – Buy Now (BN): Stocks that look compelling to buy right now.

2 – Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 – Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 – Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.