Weekly Roundup: Bucking Trend, September Is Lifting the Portfolio Higher

And why we will continue to focus on uncovering new Bullpen candidates in an overbought and valuation-stretched market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Coming into September, the month’s historical underperformance had many, including us, bracing for what could have been a turbulent month. While that was indeed how the month started, the last three weeks pulled all of the major market indices into positive territory for the month. The effect reverberated through the Portfolio as well.

With one trading day left in September, barring anything catastrophic on Monday, it appears September 2024 will go down in the market history books as bucking the trend. While we’ve enjoyed that, the S&P 500 has made a string of new highs lately and moved into short-term overbought territory. The Fear & Greed Index is back in Greed territory and the S&P 500’s P/E valuation as we close out the week is a lofty 23.6-times expected 2024 EPS.

That’s modestly higher than last Friday, meaning the market is incrementally more expensive, and that has us treading the same water. By that we mean that finding well-positioned companies with superior earnings growth prospects at favorable to compelling risk-to-reward tradeoffs is challenging.

Our preference is not to put capital to work just to say we are doing something. That would be foolish, given the backdrop of the market. Next week’s economic data, if rate-cut friendly, could see the market stretch itself a tad further, but between the 2024 presidential election, the potential port strike and still-lofty 2025 EPS expectations for the S&P 500, it’s possible October could be the challenging month that many expected September to be.

We’ll continue to look for fresh opportunities for the Portfolio and, given our comments above, that likely means seeding the Bullpen so we are ready to take advantage of the right set of circumstances. Below, we discuss some prudent Portfolio actions we took this week, and if the market continues to melt up, we may be doing more of that ahead of the September quarter earnings season.

Catching Up on the Portfolio This Week

As we noted above, with one trading day left in September, it looks like the month was a very positive one for the market and the Portfolio. More than a dozen of our positions are tracking ahead of the S&P 500 for the ninth month of the year with standouts being Builders FirstSource BLDR, United Rentals URI, Axon AXON, Meta META and Eaton ETN, to name a handful. Laggards include Marvell MRVL and Qualcomm QCOM, but this week’s earnings and guidance from Marvell keep us bullish.

With the market hitting new highs and the S&P 500’s P/E valuation stretched, we made no additions to the Portfolio this week. On Wednesday, we locked in some big gains on some shares of Trade Desk TTD and Universal Display OLED.

We also made several price-target adjustments this week. Adding KB Home’s KBH double-digit delivery outlook for 2H 2024 to Lennar’s LEN robust 2H 2024 delivery guidance, we upped our price targets for Builders FirstSource, United Rentals and Waste Management WM. We continue to think those positions as well as Vulcan Materials VMC and Eaton will benefit as the Fed delivers more rate cuts over the coming quarters. During the week JPMorgan increased its URI price target to $940 from $780.

On Thursday, we upped our price target on Meta shares and discussed where we would be interested in picking up more shares. Later that day, we boosted our rating on Bank of America BAC shares to a One rating following quarterly results and guidance from Jefferies JEF. We see Bank of America’s business as well as One-rated Morgan Stanley’s MS benefitting from lower rates. On Friday, we noticed MNTN, the connected TV advertising platform operator whose Chief Creative Officer is Hollywood star Ryan Reynolds, has selected Morgan Stanley to work on an initial public offering and is considering going public as soon as in early 2025.

On Thursday, we also explained why Micron’s quarterly results and guidance were supportive of our positions in Nvidia NVDA, Marvell, Qualcomm and others. As it relates to Qualcomm, we discussed the positive AI PC forecast issued by Canalys this week and why we expect folks will begin to re-think how they value QCOM shares before too long.

Over the weekend, be sure to read the latest batch of ripped-from-the-headline signals for our holdings.

Next week sees a busy week for the Portfolio as we close the books on September and 3Q 2024. We have Office Hours on Tuesday and Thursday in the Forum. Wednesday will be our Quarterly Members Only Call and Friday brings our next installment of the Monthly Roundtable.

As we get ready for those events, let’s catch up with what others on Wall Street said about our holdings this week:

BMO Capital boosted its price target for Costco COST to $980 from $950 while DA Davidson upped its to $880 from $780 and Truist lifted its to $909 from $873. We maintained our $950 target following Costco’s earnings report this week.

Lockheed Martin LMT was awarded more than $550 million in Navy contracts this week, adding further to its multi-year backlog. LMT shares are above our $575 target, but as we reminded folks during Thursday’s Office Hours, when we boosted our price target to $575 we shared that when Lockheed shares its 2025 and beyond delivery schedules, which will be updated for the F35 being back on track, we'll revisit our price target.

Tigress Financial raised its price target on Alphabet GOOGL to $220 from $210 and reiterated its Strong Buy rating on the shares. The firm argues ongoing strength in Search and Cloud, combined with the company's increasing ability to leverage its Gemini generative AI, will continue to drive revenue and cash flow growth. That sure sounds like our thinking on the shares. We continue to have a $210 target and a One rating on GOOGL shares.

Evercore ISI lowered its price target on Labcorp LH to $240 from $250, while Jefferies upped its target to $265 from $245 citing continued robust volume levels at diagnostic lab companies. In our August Monthly Roundup, we shared an uptick in COVID cases as well as the WHO’s naming mpox a global health emergency could stoke testing volumes. Our price target continues to be $235.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, September 23: We Don't See Qualcomm Acquiring Intel

Tuesday, September 24: Here's What to Watch for in Meta’s Connect Event

Wednesday, September 25: Why We're Increasing Price Targets on These Positions

Friday, September 27: Fed Rate Cut Odds Improve But This Disruption Looms

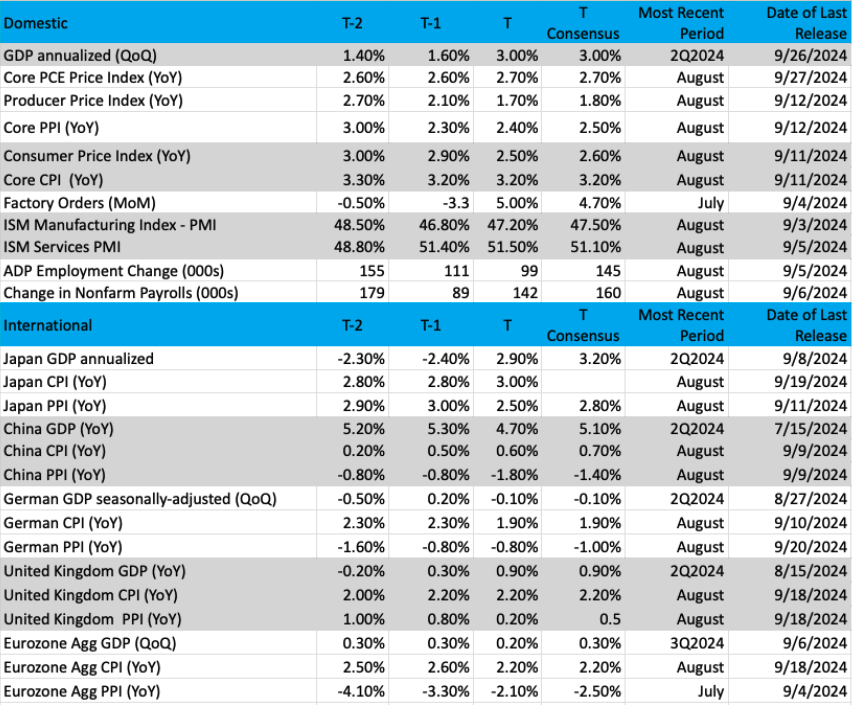

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: Invesco S&P 500 Equal Weight ETF

With the S&P 500 hitting its 43rd all-time high this week, we thought it was time to compare how the index is faring overall versus the "vaunted" Magnificent 7 stocks and their widespread influence.

Earlier in the year, we noted a stark divergence between the S&P 500 proxy SPY and the equal-weight S&P proxy, the Invesco S&P 500 Equal Weight ETF RSP. The simple difference is the SPY is weighted towards the highest capitalization stocks (hence, influenced heavily by the Mag 7) against the RSP, which weighs each member equally and not by market cap.

Why is it important to compare? A strong bull market (S&P 500) depends on all its members performing well, not just a handful. The index can certainly rise on the back of only a handful of stocks, but the rise is not considered healthy. In strong markets we see the RSP moving higher, at least in line with the SPY.

Earlier this year, a divergence between the two was quite apparent. The RSP was lagging while the SPY was performing well, as was the case in 2023. But in the summer, there was a notable shift, the 493 (names outside of the Mag 7) were suddenly performing at a high level and the RSP started to outperform the SPY. We see that as a sign of a healthy market.

Today, we see the SPY and RSP basically in the same spot (see the chart comparison). As for the technical condition of the RSP, momentum is strong with the stochastics in bull mode, moving average convergence/divergence (MACD) is on a strong buy signal and rising while the candles in the price chart are teal (after recently being blue). This represents a bullish condition in the GoNoGo composite of indicators.

If the RSP continues to perform well, we see a stock-picking environment continuing and thriving into the new year.

Other charts we shared with you this week were:

Monday, September 23: S&P 500 - S&P 500 Embarks on New Ground

Monday, September 24: Amazon AMZN - Amazon Takes Another Step Towards New Highs

Tuesday, September 25: Costco COST - Costco Flexes in Front of Earnings

Wednesday, September 26: The Trade Desk TTD - This Holding Hits Resistance

Thursday, September 27: Elevance Health ELV - This Health Care Position Is Due for a Bounce Soon

The Coming Week

Next week, we close the books on not only September but 3Q 2024 as well. With all of one trading day left in September, barring any major swings on Monday, the S&P 500 and Nasdaq are on pace to climb almost 5% and 2%, respectively, during the quarter.

That’s certainly better than many expected heading into what has typically been one of the most challenging months for the market. The other surprise, if we look at the final 2Q 2024 GDP figure of 3.0% from this week and the latest Atlanta Fed GDPNow figure of 3.1% for the current quarter, is how well the economy is performing. Looking at those figures, it suggests that concerns for a hard economic landing should be fading and the conversation shifting to something between a no-landing for the economy and a soft one.

We know, however, that next week begins the flow of September economic data that could reshape the GDPNow model. We also know the Fed is closely watching the employment market, and that means we will be paying attention to what is gleaned from the September PMI reports and ADP’s September Employment Change report.

More than likely, bad or disappointing economic news next week will be positive for rate cuts. The reason comes down to the cadence of potential rate cuts. Given the next wave of Fed speakers, including Fed Chair Powell on Monday, we expect that the topic will be a hot one next week. How the rate-cut wind blows is likely to impact the market. Powell’s appearance is on Monday and he’s likely to reiterate his recent comments but could acknowledge the continued inflation progress found in the August PCE data.

While Powell’s word carries the most weight, we’ll be more interested in Fed speaker comments between Tuesday and Friday as fresh September data is had. As we enter the quartet of data days, we’ll also have our eyes on the looming longshoreman port strike. As we discussed in Friday’s video, should a strike be called, the degree of its impact will hinge on the length of its duration. The longer it goes on, the more likely things could get difficult for retail companies this holiday shopping season.

We will also be focusing more on the 2024 presidential election as we move into next week. So far, swing states appear to be close, and we suspect that means over the next 38 days we will see a barrage of campaign marketing. We’re positioned for that with our shares of Alphabet, Meta and Trade Desk. And while we’re on the topic of digital advertising, we read this week that Amazon topped its $1.8 billion in targeted up-front ad commitments.

Here's a closer look at the economic data coming at us next week:

U.S.

Tuesday, October 1

- S&P Global Final Manufacturing PMI - September (9:45 a.m. ET)

- ISM Manufacturing PMI – September (10:00 a.m. ET)

- JOLTs Job Openings & Quits – September (10:00 a.m. ET)

- Construction Spending – August (10:00 a.m. ET)

Wednesday, October 2

- MBA Mortgage Applications Index – Weekly (7:00 a.m. ET)

- ADP Employment Change Report – September (8:15 a.m. ET)

- EIA Crude Oil Inventories – Weekly (10:30 a.m. ET)

Thursday, October 3

- Challenger Job Cuts – September (7:30 a.m. ET)

- Initial & Continuing Jobless Claims – Weekly (8:30 a.m. ET)

- S&P Global Final Services PMI – September (9:45 a.m. ET)

- ISM Services PMI – September (10:00 a.m. ET)

- Factory Orders – August (10:00 a.m. ET)

- EIA Natural Gas Inventories – Weekly (10:30 a.m. ET)

Friday, October 4

- Employment Report – August (8:30 a.m. ET)

International

Monday, September 30

- Japan: Industrial Production, Retail Sales, Housing Starts - August

- China: NBS Manufacturing & Non-Manufacturing PMI – September

- China: Caixin Manufacturing and Services PMI – September

- U.K.: GDP – 2Q 2024 (Final)

- U.K.: Consumer Credit - August

Tuesday, October 1

- Japan: Jibun Bank Final Manufacturing PMI – September

- Eurozone: HCOB Final Manufacturing PMI – September

- Eurozone: Flash Inflation Rate – September

- UK: S&P Global Final Manufacturing PMI - September

Wednesday, October 2

- Eurozone: Unemployment Rate - August

Thursday, October 3

- Japan: Jibun Bank Final Services PMI – September

- Eurozone: HCOB Final Services PMI – September

- Eurozone: Producer Price Index - August

- U.K.: S&P Global Final Services PMI - September

Friday, October 4

- U.K.: New Car Sales - September

Late this week and early next, companies have entered their pre-earnings quiet period and that means only a modest number of earnings report next week and the week after.

As we digest the reports coming at us from the likes of Nike NKE and ConAgra CAG, we’ll keep our eyes and ears open for any and all earnings’ pre-announcements. Should we see any across competitors, customers or suppliers for the Portfolio’s holdings, we’ll be sure to share potential implications with you.

We will also continue to collect data points for Apple’s new iPhone models.

Here's a closer look at the earnings reports coming at us next week:

Monday, September 30

- Open: Carnival CCL

Tuesday, October 1

- Open: Acuity Brands AYI, McCormick & Co. MKC

- Close: Lamb Weston LW, Nike NKE.

Wednesday, October 2

- Open: ConAgra CAG

- Close: Levi Strauss LEVI

Thursday, October 3

- Open: Constellation Brands STZ

Portfolio Investor Resource Guide

- Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

- Investing Terminology: 16 Key Terms Club Members Should Know

- 10-Ks: Want to Know About a Stock? Read the Company's Reports

- 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

- Income Statement -Our Cheat Sheet to Understanding This Financial Document

- Balance sheet, Cash Flow Statements, and Dividends - How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

- Valuation Metrics - Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

More Pro Portfolio

- Locking in Big Gains on These Two Positions

- Weekly Roundup: Stocks Are Up for September and So Is the Portfolio

- While the Market Focused on the Fed, We Collected the Latest Signals

At the time of publication, TheStreet Pro Portfolio was long BLDR, URI, AXON, META, ETN, MRVL, QCOM, TTD, OLED, WM, VMC, BAC, MS, NVDA, COST, LMT, GOOGL, LH, AMZN and ELV.