Weekly Roundup: Stocks Are Up for September and So Is the Portfolio

The Fed has started to cut rates, but these items could make for challenging weeks ahead.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We had another positive move in the market this week, ushered in by market expectations for the Fed to deliver a 50 basis point rate cut. While we and many others foresaw a more modest rate cut move, the Fed delivered what the market expected and signaled that more rate cuts are on the horizon.

Despite Friday’s triple-witching event, the Volatility Index (VIX) closed the week lower while all the major market indices finished higher. That move brought the S&P 500 and Nasdaq back into positive territory over the last month, showing that, so far at least, September’s market reputation may not play out this year. And, so far, the Portfolio has been humming along over the last several weeks.

While we are enjoying that, we recognize the market’s condition remains overbought and the S&P 500’s valuation is stretched. In addition to the September quarter earnings season kicking off soon, there are other items that will probably grab the market’s attention in the coming weeks. These include the potential longshoreman strike that could hobble eastern and Gulf Coast ports, a potential government shutdown, the 2024 presidential election and continued geopolitical tensions. We’ll also want to keep a close watch on incoming economic data to gauge the Fed’s potential cadence of rate cuts.

So, while the first three weeks of September have all the major market indices in positive territory, we have to keep our eye on the road ahead and continue to position the Portfolio as needed. As we’ve discussed before, falling in love with one’s holdings is a trap that plagues many investors. Another is becoming lax and slipping into a fix-it-and-forget-it mentality, something we refer to as “crockpot investing.”

The moves we’ve made over the last several months, and especially those in August, are paying off because we positioned ourselves for what was coming. As it stands today, the Portfolio is well-positioned as the Fed moves deeper into its rate-cut cycle. However, we won’t rest on our laurels or become complacent. We still have some cash to put to work and we also recognize the landscape can shift if you’re not paying attention.

While the Portfolio has made great strides over the last several months, we’ll continue to roll up our sleeves, do the work and look for well-positioned companies, with superior EPS growth prospects, and shares that offer a favorable or compelling risk-to-reward entry point. Our glass-half-full view is that market pullbacks bring opportunities and that means that, following this week’s move in the market, we’ll be updating our shopping list and sharing it with you as we kick off next week.

Catching Up on the Portfolio This Week

Above, we noted the market’s continued melt up this week and the positive impact it had on our holdings. Outsized performers this week included our more interest-rate-sensitive positions, including Builders FirstSource BLDR, United Rentals URI and Vulcan Materials VMC. Following the Fed’s rate cut and updated set of projections, our shares of Eaton ETN, ServiceNow NOW and Meta META were also strong performers. Late in the week, PepsiCo PEP shares traded off, joining Waste Management WM, Elevance Health ELV and Costco COST in finishing the week lower.

Early in the week, Microsoft approved a new $60 billion stock buyback program and boosted its quarterly dividend by 10% to $0.83 per share. The first of this new dividend will be paid on December 23, 2024, to shareholders of record on November 21, 2024. Our take on both is that they support the company’s expected growth path as cloud, AI and the PC upgrade cycle ramp. Ahead of the Fed’s policy meeting on Wednesday, we discussed several real estate investment trust (REIT) stocks we’re taking a closer look at.

On Thursday we picked up some additional shares of Morgan Stanley MS and Bank of America BAC, whose businesses should benefit from the Fed’s rate-cutting efforts. That left us with just over 11% of the Portfolio’s assets in cash. Friday’s modest retreat in the S&P 500 means that market barometer is just off fresh highs, remains overbought in the short term, and has a stretched P/E valuation near 23.5x based on consensus 2024 EPS. We will continue to look for opportunities to put capital to work but we will remain disciplined and common-sense investors.

In terms of upcoming calendar items, we’re watching Apple’s new iPhone, Apple Watch, and AirPods products hitting shelves on Friday; early next week, we’ll be looking for indications of how demand for those products fared following their opening weekend. Next week also brings quarterly results from Costco COST as well as Bank of America’s Financials CEO Conference.

With some travel early in the week, our next set of Office Hours will be on Thursday, September 26 between 12 p.m. and 1 p.m. ET in the Forum.

Other dates we’re marking in our calendar include PepsiCo’s earnings on October 8, and Amazon’s Prime Big Deal Days on October 8 and 9. We think this event will market the early start of the 2024 holiday shopping season, one that we and Deloitte think will benefit digital shopping. In addition to Apple targeting an October release for iOS 18.1 that will formally unveil initial Apple Intelligence features, we are also hearing that Apple may hold an October event to unveil new M4 Macs and an updated iPad mini.

Now, let’s turn and recap some of the moves Wall Street firms made this week pertaining to our holdings:

Loop Capital lifted its BLDR price target to $230 from $190, Oppenheimer took its to $225 from $205, while BofA upped its to $198 from $165. Truist also upgraded Builders FirstSource to Buy from Hold with a price target of $220, up from $165. Truist’s rationale should sound rather familiar to you — falling interest rates should spark single-family housing activity in 2025 and Builders FirstSource's size and continued push into value-added products and digital offerings should drive faster than market growth. In Friday’s video, we discussed our plan when it comes to our BLDR price target.

Citing "robust" data center power demand growth and prospects for "outsized' earnings growth over the next several years, Citi initiated coverage of Eaton with a Buy rating and a $348 price target.

Evercore increased its Amazon price target to $240 from $225 and Lab Corp LH saw its target over at Baird inched up to $282 from $278.

Even though Morgan Stanley kept its PepsiCo price target at $185, the same as ours, the firm downgraded its rating to Equal Weight from Overweight. We see that matching our Two rating on the shares.

In addition to an expanded partnership with Salesforce CRM that should help drive enterprise adoption of AI, Nvidia fetched a fresh Outperform rating at William Blair.

BofA raised its price target on MasterCard to $509 from $480, keeping a Neutral rating on the shares. Our price target clocks in at $490, and our plan is to review it once we have digested next week’s August Personal Income & Spending data, and what it says about real wage growth.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, September 16: Data Doesn’t Support Big Action by Fed

Tuesday, September 17: Why We’re Convinced the Fed Will Deliver Less Than Expected

Wednesday, September 18: Despite Favorable Print, Don’t Chase This Holding

Thursday, September 19: Downside Guidance Could Be a Positive for This Holding

Friday, September 20: What We're Watching as Apple’s New Models Hit Shelves

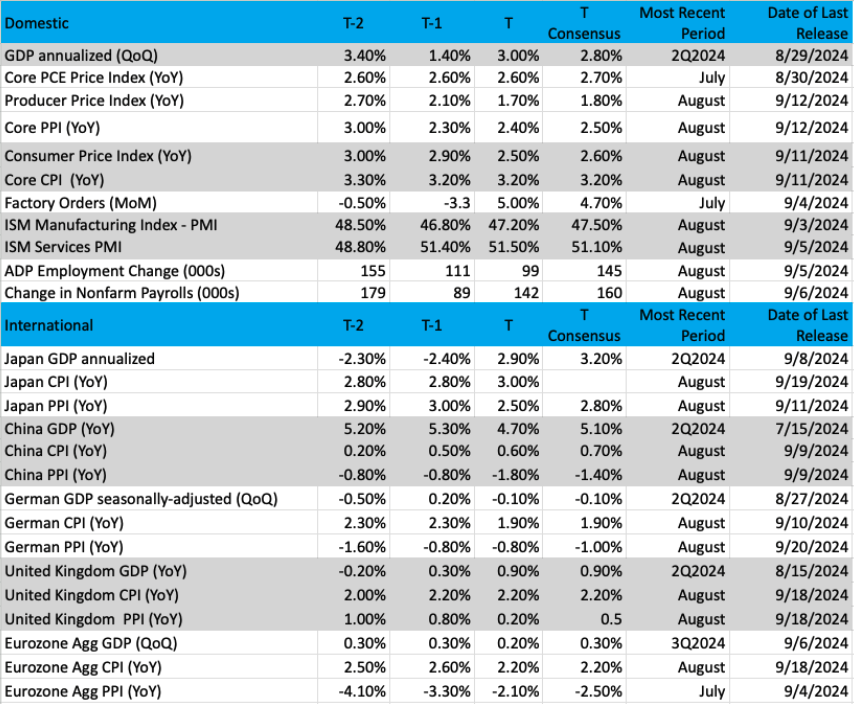

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: iShares Russell 2000 ETF

Small-cap stocks seem to love lower interest rates. After all, lowering those borrowing costs makes it easier for small companies to attain financing for their business. It also means the lower rates are trying to stimulate economic growth. The small-cap stocks are largely represented by the Russell 2000, or the IWM ETF as a proxy. As a technician, the chart of the IWM explains market moves, which gives us a read-on direction.

Remember, breadth is an important component when evaluating market conditions. It is hard to dismiss 2000 stocks that are moving in waves, they can move the rest of the market in a big way.

We saw back in July a violent move higher in the IWM ETF, this happened after a positive CPI number was printed for June. Yields plunged at the time and, of course, when that happens investors clamor for small caps. The IWM moved up more than 10% over the course of ten sessions, a remarkable move in a relatively short period.

So, this past week saw the Federal Reserve drop the funds rate by 50 basis points (BPS), a bit of a shocking move as many were only expecting half as much. But leading up to this move bond yields had already fallen sharply, the two-year, for instance, fell below the key 4% level and still hovers under it today.

Of course, the market rallied sharply this week, and small caps rose along with the other indices, but the IWM is not anywhere near an all-time high. For reference, the Industrials and S&P 500 have both hit new highs recently and continue to move. For its part, the Russell 2K is about 4% away from all-time highs, and if rates stay low or continue moving down that only strengthens the argument for the IWM to make a new high sooner rather than later.

To the chart, the IWM shows a buy signal with the MACD indicator, a strong signal for more upward movement. This indicator shows a change in trajectory before it actually happens. The recent pullback (in the top pane) shows a higher low on the chart, our textbook uptrend condition. But we also see resistance at recent highs around the $224 to $226 area, which could be problematic if the IWM can’t muster enough energy to penetrate those levels.

We think any pullback here in the IWM is worthy of a buy if the $204 level holds in place. Small caps, when they participate in the market rally are a powerful energy source for the rest of the stock market. If only rates could keep falling...

Other charts we shared with you this week were:

Monday, September 16: S&P 500 - Powerful Reversal Will Lift S&P 500 to New All-time High

Monday, September 16: Microsoft MSFT - A Magnificent Seven Name Is Making a Bullish Move

Tuesday, September 17: Mastercard MA - Mastercard's Moves ... Priceless

Wednesday, September 18: Dutch Bros BROS - This 'Upstart' Holding Is Making a Steady Move Above Resistance

Thursday, September 19: Vulcan Materials VMC - This Holding Is About to Make an Important Move

The Coming Week

Exiting this week, the Atlanta Fed’s GDPNow model for the current quarter stood at 2.9% and its next update will come on Friday, September 27, better known as the end of next week. We’ll start next week with the first hard look at how the economy performed in September and conclude with the latest look at Personal Income and Spending as well as the Fed’s preferred gauge of inflation, the Personal Consumption Expenditure (PCE) Price Index. In between, we’ll get more data on how the housing and industrial markets performed in August.

Across Flash September PMI reports on Monday from S&P Global, we’ll be looking to see if the manufacturing economy strengthened given the upturn in weekly rail traffic. We’ll also be looking to see if the service sector continues to carry the overall economy. Given the Fed’s focus on both inflation and job creation, we’ll be parsing the data for both of those items and comparing them up against other recent data.

While the August PCE Price Index data is somewhat rear-view mirror-ish compared to the Flash September data, we’ll still be looking for continued progress toward the Fed’s 2% inflation target. Alongside those figures, we’ll be interested in what the data shows for real wage growth compared to the last few months.

Next week also brings a dozen engagements for Fed speakers, including one by Fed Chair Powell on Thursday, September 26. Because we will only have a modicum of fresh data coming off this week’s Fed policy action, we’re not expecting those speakers will break much new ground. While some may show their dovish or hawkish hand, we suspect the overriding message is the Fed is recalibrating policy and the pace for that will hinge on incoming data. In other words, a re-delivery of Powell’s message this week. As more data is published, we are likely to see the market hang more on Fed speaker comments, especially as we approach the November policy decision.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, September 23

- S&P Global Manufacturing and Services Flash PMI – September (9:45 a.m. ET)

Tuesday, September 24

- FHFA Housing Price Index – July (9:00 a.m. ET)

- S&P Case Shiller Home Price Index – July (9:00 a.m. ET)

- Consumer Confidence – September (10:00 a.m. ET)

Wednesday, September 25

- MBA Mortgage Applications Index – Weekly (7:00 a.m. ET)

- New Home Sales – August (10:00 a.m. ET)

- EIA Crude Oil Inventories – Weekly (10:30 a.m. ET)

Thursday, September 26

- Initial & Continuing Jobless Claims – Weekly (8:30 a.m. ET)

- Durable Orders – August (8:30 a.m. ET)

- GDP – 2Q 2024 (third estimate) – (8:30 a.m. ET)

- Pending Home Sales – August (10:00 a.m. ET)

- EIA Natural Gas Inventories – Weekly (10:30 a.m. ET)

Friday, September 27

- Personal Income & Spending, PCE Price Index – August (8:30 a.m. ET)

- Advanced Inventories – August (8:30 a.m. ET)

- The University of Michigan Consumer Sentiment Index (Final) – September (10:00 a.m. ET)

International

Monday, September 23

- Eurozone: HCOB Manufacturing and Services Flash PMI – September

- UK: S&P Global Manufacturing and Services Flash PMI - September

Tuesday, September 24

- Japan: Jibun Bank Manufacturing and Services Flash PMI - September

Wednesday, September 25

- Eurozone: European Central Bank Non-Monetary Policy Meeting

Friday, September 27

- China: Industrial Profits – August

- Japan: Leading Economic Index – July

- Eurozone: Economic Sentiment and Consumer Confidence – September

As we near the end of September, the majority of companies reporting in the coming weeks will be entering their quiet period. Similar to the Fed’s blackout period ahead of its policy meetings, quiet periods typically see companies go quiet as they start rolling up their books for the quarter and begin prepping for the earnings report and conference call.

When we enter these periods, our eyes and ears go on alert for earnings pre-announcements across the continuum of companies that represent the competitors, suppliers, and customers of the Portfolio’s holdings as well as the holdings themselves. Should we see any such reports, good or bad, they may lead us to tweak some of our thinking as it relates to the Portfolio.

Even though it’s just a trickle, there will be a few earnings reports we want to dig into next week. Following Lennar’s LEN positive outlook for housing deliveries, we’ll look to see if KB Home KBH also offers an upbeat outlook. If it does, it will suggest a more widespread rebound in the housing market has begun and should accelerate as the Fed moves down its rate-cutting curve and mortgage rates move in a similar fashion. That will be a catalyst for us to revisit not only our price target for Builders FirstSource but potentially its rating as well.

Uniform and supply company Cintas CTAS will provide another look at the economy while Jefferies JEF does the same for the investment banking landscape. Following the start of the Fed’s rate-cutting cycle, odds are Jefferies will give an upbeat lookout for deal flow and the IPO market. That expectation was part of our adding to Bank of America and Morgan Stanley on Thursday.

Wednesday also brings quarterly results and guidance from Micron MU. Many will be focusing on the memory market. We will be too, but our greater interest will be in its comments about the PC, smartphone and data center markets. Those comments are the next known data point to watch for the rebounding that is unfolding in the smartphone and PC markets, which means we’ll be factoring what is said into our thinking for Apple AAPL, Qualcomm QCOM and Universal Display OLED. We’ll be tracking Micron’s data center comments with an eye toward Nvidia NVDA, Marvell MRVL and Eaton shares but also United Rentals and Vulcan Materials.

Accenture ACN reports on Thursday and, in that report, it will be AI adoption in the enterprise that we focus on most. Costco also reports on Thursday and comparing its monthly sales reports against monthly Retail Sales reports suggest it should be a good report. Starting September 1, Costco’s new membership fee went into effect and that could lead to some on Wall Street having to recast their EPS projections. Over the last 90 days, consensus EPS expectations have moved up somewhat, but our thinking is there is more to go to accurately reflect the full impact of that recent price hike across the company’s entire membership. Based on what we learn, we’ll revisit our above consensus COST price target of $950 as needed.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, September 24

- Open: AutoZone AZO,

- Close: KB Home KBH, Progress Software PRGS

Wednesday, September 25

- Open: Cintas CTAS

- Close: Jefferies JEF, Micron MU

Thursday, September 26

- Open: Accenture ACN, CarMax KMX

- Close: Costco COST

Portfolio Investor Resource Guide

- Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

- Investing Terminology: 16 Key Terms Club Members Should Know

- 10-Ks: Want to Know About a Stock? Read the Company's Reports

- 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

- Income Statement -Our Cheat Sheet to Understanding This Financial Document

- Balance sheet, Cash Flow Statements, and Dividends - How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

- Valuation Metrics - Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

More Pro Portfolio

- Buying More Stock of This Semi-Cap Equipment Position

- Weekly Roundup: Is the Market Setting Up for an April Repeat?

- The AI Conundrum, Cyber Threats, and Our Digital World: More News on Our Strategies

At the time of publication, TheStreet Pro Portfolio was long BLDR, BAC, URI, VMC, ETN, PEP, WM, ELV, COST, MS, LH, MA, META, MSFT, NOW, BROS, AAPL, QCOM, OLED, NVDA and MRVL.