The Investment Game Is Changing — And Old Rules Are Starting to Fade Away

Here’s why this market rally will continue, and the broken link that's Wall Street's new reality.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

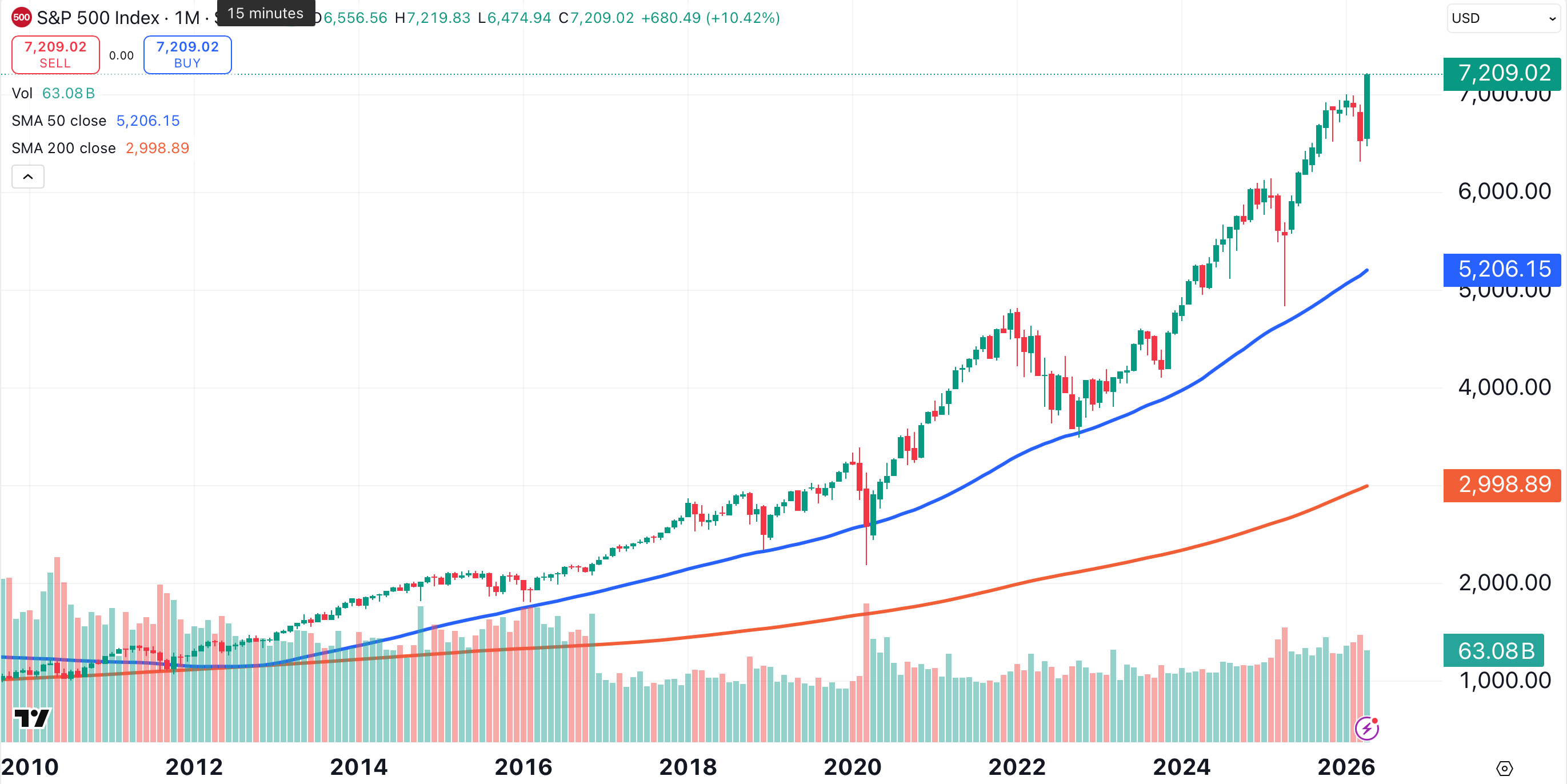

The S&P 500 just had its best month in five years.

For the month of April, the large-cap index gained 10.5%. That’s close to the index’s average annual return since its inception in 1957.

That spectacular gain occurred despite a Middle East war that has no end in sight. It happened despite sharply higher energy prices, with U.S. crude oil gaining over 80% since the start of this year.

The monthly chart of the S&P 500 reveals a bullish long-term trend that shows no signs of slowing down.

The Warsh Factor

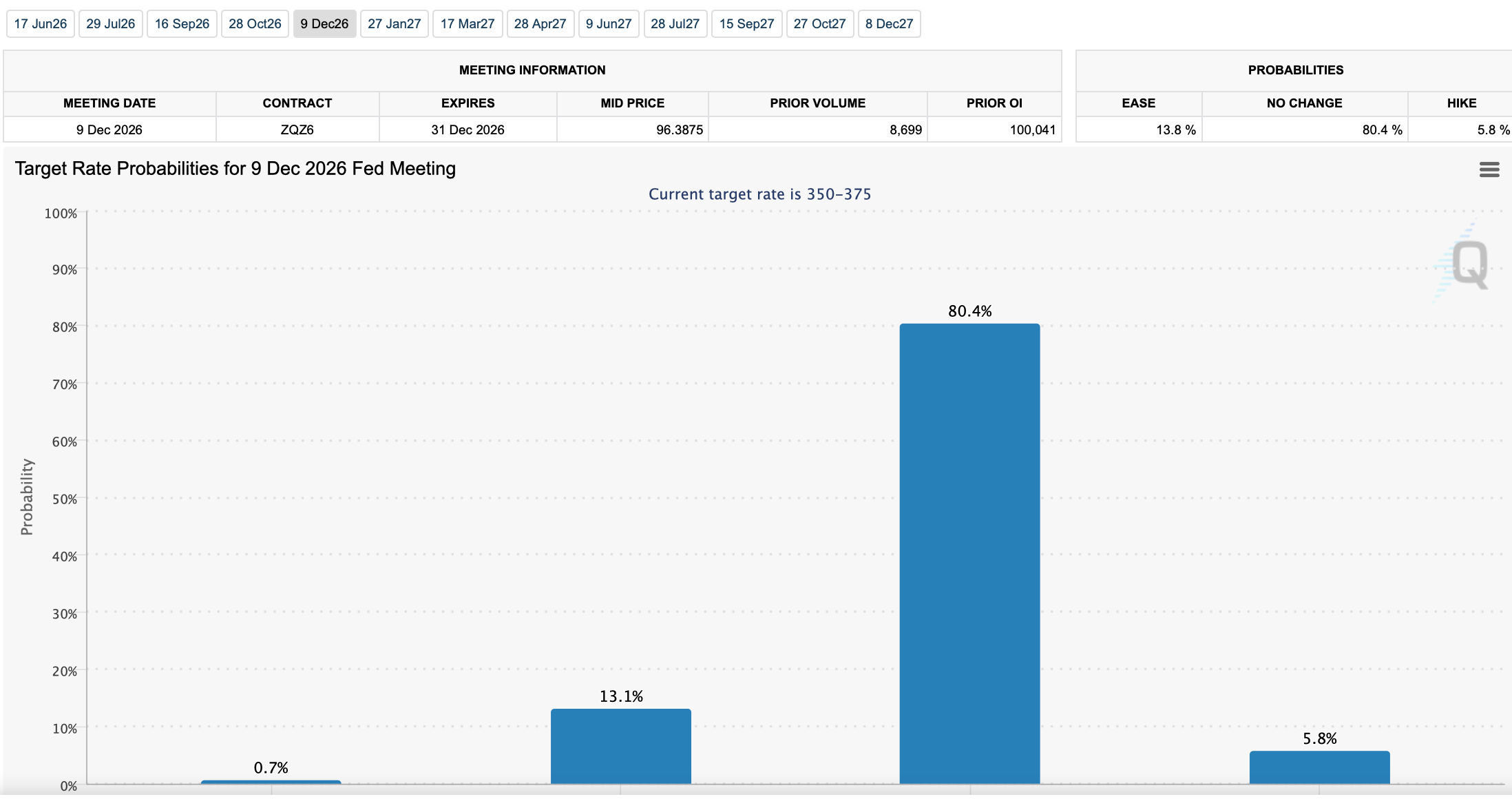

Is the market reacting to Kevin Warsh’s apparent ascent to Fed Chair? Earlier this week, the Senate Banking Committee voted to advance Warsh’s nomination as Jerome Powell’s replacement.

Warsh’s critics have labeled him a “sock puppet” for President Trump, who has made no secret of his strong desire for interest rate cuts. While reductions in the Fed Funds rate could potentially spur inflation (more on that here), lower interest rates also tend to have a positive effect on stocks, by making bonds less attractive in comparison.

While this line of reasoning seems feasible, interest rate futures disagree. According to the CME’s FedWatch Tool, there is only a 14% chance for a Fed Funds rate cut this year — and a 6% chance of a rate hike. There is an 80% chance that the Fed Funds rate will end the year where it is now, in a range between 3.5% and 3.75%.

Earnings Are Strong...

The reason for the market’s persistent climb is economic strength, as reflected by corporate earnings.

According to FactSet, 84% of the companies reporting have beaten earnings expectations for Q1 2026. Seventy-six percent of companies have exceeded estimates for both earnings and revenue. We are on track for the sixth consecutive quarter of double-digit earnings growth.

Those corporate gains are being driven by technology, specifically the adoption of AI.

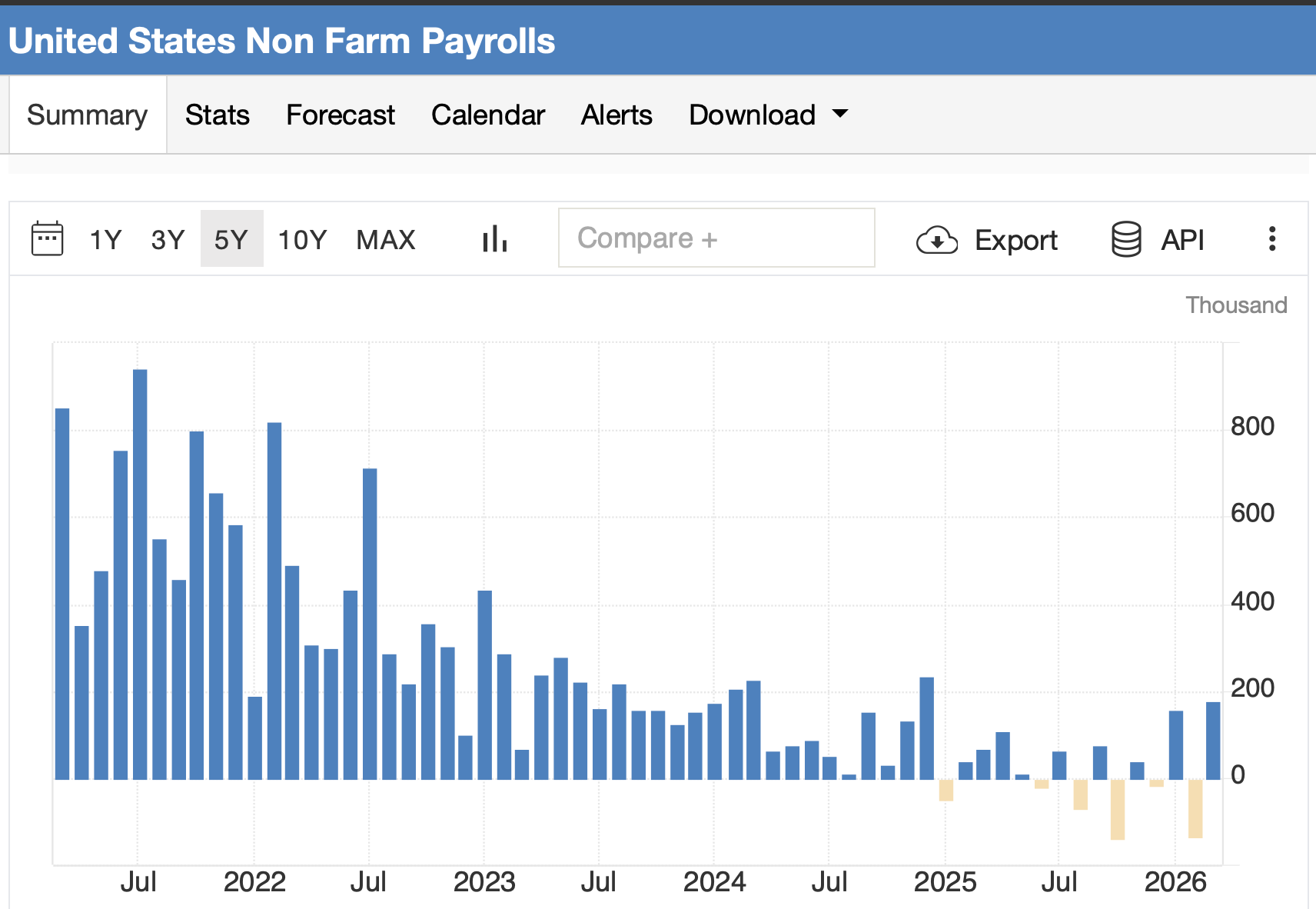

Job Creation Is Weak

If the economy is so strong, why isn’t that reflected in job creation?

According to the Bureau of Labor Statistics, U.S. non-farm employment has increased by a total of just 337,000 since August of last year. That’s an average monthly increase of just over 42,000 per month.

In a healthy economy, one might expect job creation of 200,000 or more per month. Meanwhile, employment actually declined in six of the past f15 months.

Weakness in employment is often cited as proof of a stalling economy, and therefore a reason to reduce interest rates. However, as explained above, rate cuts are not likely to occur this year.

Skeleton Crew

The economy is less dependent on human interaction every day.

Klarna (KLAR) has 118 million active users. In recent years, the "buy now, pay later" service reduced its staff from over 5,000 to 3,000.

Block (XYZ) , owner of Cash App, has over 60 million monthly users. The company recently announced a reduction in headcount from 10,000 to 6,000.

Duolingo (DUOL) has about 12 million subscribers that are serviced by about 1,000 full-time employees.

We’ve reached a point where companies are now being forced to adopt AI — and potentially reduce headcount — in order to compete effectively.

Future Shock

Alvin Tofler’s Future Shock was released in 1970. The author opined that in the 21st century, disruptive changes would occur so quickly that the human mind, accustomed to a slower rate of change, may become overwhelmed.

Here in the 21st century, certain skill sets are quickly becoming outdated. The long-time correlation between job creation and economic strength is falling apart in real time. Interactions with AI customer service agents, which until recently were something of a joke, have improved noticeably over just the past few months.

Bottom Line

Soon, less emphasis will be placed on employment data. Earnings can continue to improve, and stocks can continue to rise, without strong job creation, and without an easy monetary policy.

We are still in the early stages of this process. As it continues to unfold and accelerate, fewer of the old rules will apply. While some things will never change, for investors, it could be dangerous to adhere too tightly to old ways of thinking.

Related: When Is Low Price an Opportunity? When Is It a Risk?

At the time of publication, Ponsi had no positions in any securities mentioned.