We're Boosting Price Targets on 3 Portfolio Holdings

Improving housing construction prospects and elevated non-residential construction are the catalysts for these moves.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* We are upping our price target and panic point on Builders FirstSource.

* We are also raising our price target and panic point for United Rentals.

* We are revising higher our target for Waste Management, while maintaining our target for Vulcan Materials.

Following several positive data points for the housing market that point to stronger construction activity, we are lifting our price target for Builders FirstSource BLDR. August single-family housing starts hit their highest level since April and Lennar’s LEN second-half 2024 home deliveries are expected to be 21% higher compared to the first half of the year.

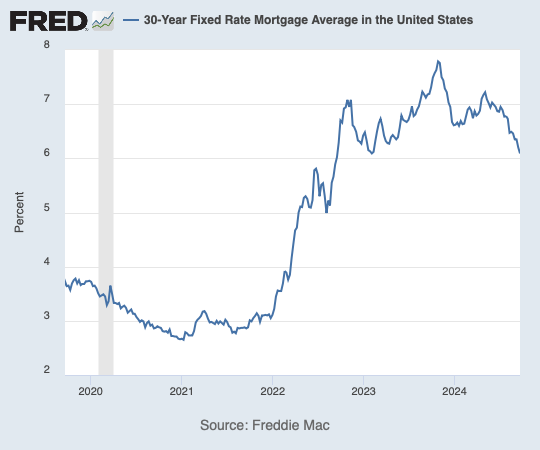

To that, we can add homebuilder KB Home’s KBH H2 2024 home deliveries, which are forecasted to be up around 15% compared to H1 2024. As the Fed moves further down the rate-cutting curve and mortgage rates continue to fall, we should see the housing market continue to improve.

At the same time, the latest data point to the U.S. housing shortage totaling 4.5 million homes, something that should be chipped away at as mortgage rates and housing affordability improve. With Fed rate cuts continuing into 2025, we see this as another factor that should help drive housing construction in 2025 and 2026.

For now, we’ll lift our BLDR price target to $235 from $205, but should data over the coming months point to a quicker pick-up in home construction activity we may need to revisit that new target. In terms of our BLDR rating, at current levels we see more than enough upside to keep our One rating intact, but should BLDR move above $210 or so, a re-think on that rating could occur. We will also lift our BLDR panic point to $160 from $135.

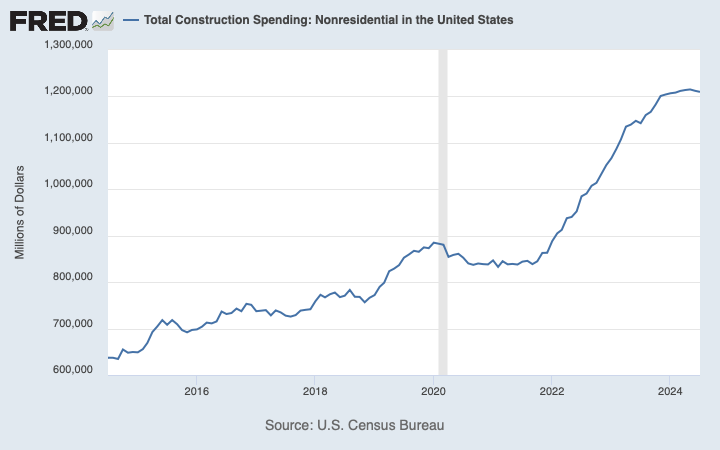

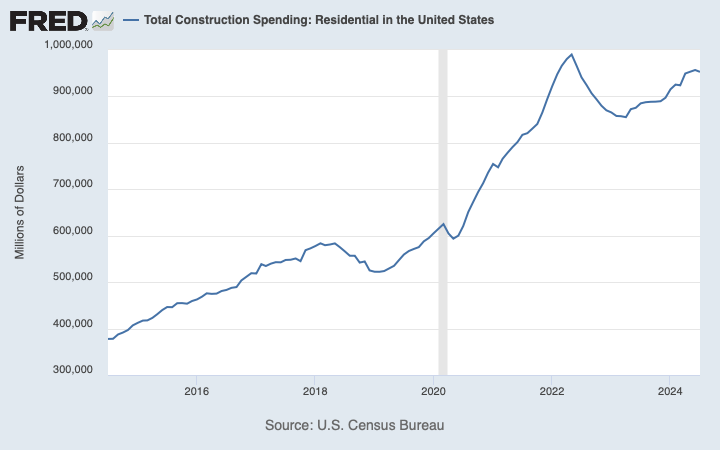

Turning our other construction-related holdings, United Rentals URI, Vulcan Materials VMC, and to a lesser extent Waste Management WM, their exposure to home construction is meaningful but less so than for Builder’s FirstSource. And unlike Builders, their businesses also benefit from non-residential construction activity, which is being driven by infrastructure and related stimulus spending programs out of Washington.

As we move further down the curve of those programs, we expect to see more difficult year-over-year comparisons emerge in the monthly Construction Spending reports for non-residential construction. However, because residential construction accounts for 40%-45% of total construction spending over the last decade, a pick-up in that market while non-residential construction spending remains at elevated levels should boost overall construction spending levels in 2025 and into 2026.

That prospect is leading us to make the following adjustments:

We'll lift our URI price target to $875 from $775 and our panic point to $650 from $585. Despite the price target boost, with less than 10% upside we will maintain our Two rating. Should URI shares pull back below $750, that would give us enough upside to revisit a potential One rating.

We'll maintain our above-consensus price target of $300 for VMC shares, and for now, keep our panic point at $225. With almost 20% upside to our target, our rating remains One. Should we see concrete and aggregate pricing firm further in the coming months, it would be a reason for us to revisit our price target.

With WM shares, we are boosting our target to $225 from $220 and keeping our $183 panic point and Two rating intact. As WM completes its pending acquisition of Stericycle, and management details its integration and cost savings plans, we’ll revisit our target and rating as needed.

As we make these changes, one of the risks we will continue to monitor will be the health of the overall U.S. economy. Recent data support the soft-landing narrative, and the prospects for Fed policy look to support that, extending the current economic cycle. That should be supportive of the thinking we outlined above. However, should data in the coming months or quarters signal a greater downturn in the economy, we may need to revisit our thinking on these holdings. As of now, that probability seems minimal, but as you know we will continue to let the data talk to us.

At the time of publication, TheStreet Pro Portfolio was long BLDR, URI, VMC and WM.