Weekly Roundup: The Pro Portfolio Is Winning, Even as Markets Turn Overbought

We had a strong April, but remain focused on what’s ahead. Here's what drove our outperformance during the month.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As we foreshadowed in our April Monthly Roundup, April was a good month for the market, and that continued into the final days of the month with the S&P 500 setting a fresh high. While questions and uncertainties over the Iran conflict remained, the final days of trading brought confirmation for what some refer to as the “AI-trade.”

Another leg up in hyperscaler spending this year suggests we should see favorable follow-through as key suppliers and beneficiaries of that spending report. With that in mind, we’ll be going over revised consensus EPS figures for the S&P 500 this weekend and next, reviewing their implied growth expectations against the S&P 500’s P/E ratio. Heading into this weekend, that figure looks to be around 22.3x, but that’s using the consensus 2026 EPS figure before this week’s hyperscaler earnings.

Odds are the flow through of those earnings and the ones we’ll get next week will lift EPS growth rate expectations for the S&P 500, nudging that P/E multiple lower. However, as we discussed in Friday’s opening missive, both the S&P 500 and Nasdaq Composite were back in overbought territory exiting April, and the first day of May trading only extended that condition.

Normally, this would have us sitting on the sidelines. However, we are also listening intently for what’s next between the U.S. and Iran, and what that means for energy prices and the opening of the Strait of Hormuz. Inflation data points toward escalating pressures, and that means we are likely to hear more from companies on pricing actions.

I kid you not, Starbucks (SBUX) CEO Brian Niccol is defending a $9 cup of coffee at the company, billing it as a “special experience.” My take is that is not in sync with consumers these days, and I’ll also share that based on a few visits to Starbucks of late, it’s hard to argue it is a “premium” experience. I’ll stick to buying the Costco Kirkland Signature Coffee, a much cheaper way to get my caffeine.

While the market is focused on tech this week and next, soon the kinds of companies reporting quarterly results will shift to retail and related names. Based on what we’re seeing and hearing, that could be more of a challenge than what we heard this week. But that’s part of what our job is as investors, to look around corners for opportunities as well as those events that could upset the market, so we can act accordingly. Efforts made over the last few months are treating us well, and should continue to do so, but now is not the time to take our eye off the ball.

Enjoy your weekend! I’ll be unpacking more boxes, but I will see you back here, bright and early on Monday.

Catching Up on the Portfolio This Week

Following last week’s earlier-than-usual April Monthly Roundup, we can confirm the Pro Portfolio bested the S&P 500 in April, bringing its year-to-date return through April to 7.24%, compared to 5.3% for the market index. Updating our comments for the final four trading days of April and quarterly results from the major hyperscalers, outperformers for the Portfolio in April were Marvell Technology (MRVL) , Arista Networks (ANET) , Alphabet (GOOGL) , Broadcom (AVGO) , SuRo Capital (SSSS) , and United Rentals (URI) . Those positions were up between 20% and nearly 67% in the case of Marvell.

The other powerhouse in the Portfolio was the EPS Diplomats basket, which returned more than 36% in April. That outsized gain was powered by shares of Bloom Energy (BE) as well as by Credo Technology (CRDO) , Micron (MU) , and Lumentum (LITE) . Talk about a good time to increase our exposure to the strategy! And all things considered, it may be smarter to refer to it as "EPS All-Stars." We’ll think on that and come back to you.

Laggards that dragged on the Portfolio’s performance were the market-hedging, inverse ETF positions, as well as Axon Enterprise (AXON) , Labcorp (LH) , Netflix (NFLX) , Palantir (PLTR) , and TJX Companies (TJX) . Axon and Palantir report early next week, as do several other holdings. We’ll update our collected opinions as we digest those learnings.

With the stock market in or near an overbought condition this week, we did not make any trades.

On Friday, the first day of trading for May, both the Portfolio and the market climbed further. For the S&P 500 and the Nasdaq Composite, that good news pushed their respective relative strength index (RSI) levels further into an overbought condition. The same goes for the Technology Select Sector SPDR Fund (XLK) as well as the shares of Google and Amazon (AMZN) . We recently trimmed our exposure to AMZN, locking in a gain of more than 240%. With GOOGL pushing past a 4.4% position size for us, some prudent trimming could be in the offing if we see the shares push into an even deeper overbought condition.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday: Erste Group upgraded Morgan Stanley (MS) shares to a Buy rating and made the same move with the shares of Applied Materials (AMAT) .

Tuesday: Goldman Sachs upped its price target for American Express (AXP) to $400 from $360, BofA boosted its Applied Materials target to $465 from $420, and UBS increased its target for Apple (AAPL) to $287.

Wednesday: Evercore ISI nudged its American Express target up to $345 from $330.

Thursday: JPMorgan downgraded Meta (META) to Neutral from Overweight and trimmed its price target to $725 from $825, while Barclays upped its META target to $830 from $800. Barclays also lifted its Waste Management (WM) target to $270. Oppenheimer initiated coverage of Palantir shares with an Outperform rating and a $200 target. Citi, Barclays, and TD Cowen upped their Amazon price targets to $320-$350 from $285-$300. BofA jacked its Alphabet target to $430 from $370, while Stifel reset its target at $420 from $387. Piper Sandler lifted its Microsoft (MSFT) target to $540 from $500, while Citi took its target to $620.

Friday: Baird, BofA, TD Cowen, Wells Fargo, and Morgan Stanley all boosted their Apple price targets to $310-$335 from $285-$300.

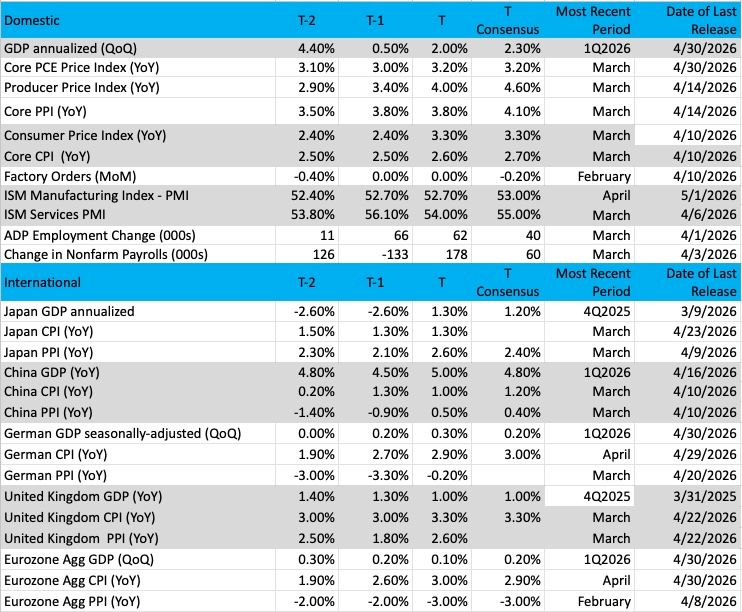

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading, and T-2 is two periods back, the intent being to illustrate any trends.)

Chart of the Week: S&P 500 – Market Cap vs. Equal Weighted

After some brief separation, the equal-weighted S&P 500 ETF (RSP) and the weighted S&P 500 ETF (SPY) have teamed up and started advancing simultaneously. It represents a strong bullish case when both the RSP and SPY are moving up together, and while the RSP is just under all-time highs (it printed a high last week), the SPY is strong enough to carry the rest of the indexes higher.

The SPY, which had been the laggard for weeks finally got its act together, no question helped by the big Magnificent Seven names rising towards all-time high territory. These stocks have enormous influence on market performance and can certainly push many tech names in their direction. Alphabet (GOOGL) , Amazon (AMZN) and Nvidia (NVDA) recently hit historical highs and with it the SPY also reached a new milestone (along with the Nasdaq).

However, the RSP is not quite there yet. These big names only have one vote in this ETF no matter how strong they perform. Yet, the RSP has found a way to rise, spreading the wealth to other groups and sectors like retail, discretionary, gold/silver miners, oil/gas, financials and industrials.

Notice on the chart, the late high made in February by the RSP did not have the SPY moving with it. That created a divergence and led to a sharp down move, so when the two move separately again we will know how to prepare for it. Currently, the RSP and SPY are very tight and in sync.

After falling sharply in late March both the RSP and SPY managed to rise on strong volume trends and solid breadth (not seen here). As we know, price action matters most and when secondary indicators support the trend, we look for that move to continue. It is hard to believe more upside is in store, but we are not going to fight the tape.

Other charts we shared with you this week were:

Monday, April 27: S&P 500 - Tech Stocks Lead the Way as Big Earnings Loom

Monday, April 27: Microsoft (MSFT) - Microsoft May Be in a Good Spot

Tuesday, April 28: Alphabet (GOOGL) - Alphabet Punishes the Non-Believers

Wednesday, April 29: Amazon (AMZN) - Did Amazon Rise Up Before a Strong Quarter?

Thursday, April 30: Waste Management (WM) - Waste Management Sets Stage for Potential Move Higher

The Week Ahead

You know the drill, as we close out one month and begin the next, a wave of fresh economic data is coming at us next week, bringing with it a fresh look at the speed of job creation and inflation pressures. Following Friday’s step up in the Prices sub-index in ISM’s April Manufacturing Index to 84.6 from 78.3 in March and 59 back in January, it’s safe to say the duration and follow-through of the U.S.-Iran conflict and higher energy prices are being felt.

We’ll have another view on that next week with ISM’s Non-Manufacturing Index for April and its Price sub-index. As a primer, that sub-index hit 70.7 in March, its highest level since October 2022.

We will also get multiple vantage points on job creation, including the one from ISM, but also S&P Global, ADP, the latest Challenger Job Cuts report, and of course, the April Employment Report. As of Friday, the April Employment Report is expected to show 73,000 jobs created, down from 178,000 in March. Those expectations will be adjusted as other job-facing data is published next week, but we will also want to review any revised job creation figures for February and March when we get the April report next Friday.

Next week will also bring some catch-up economic data for Construction Spending, and while it's a bit backward-looking at this point, we’ll give the data a going over with an eye toward our position in United Rentals (URI) .

Given growing concerns over consumer spending, next week brings us the Fed’s latest Senior Loan Officer Opinion Survey on Bank Lending Practices, widely referred to as the SLOOS report. This will provide insights into credit availability, whether lending standards are loosening or tightening, and other aspects of commercial and consumer lending. We’ll be looking for commentary on economic uncertainty and other factors that could signal a slowing economy.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, May 4

Factory Orders – March (10:00 AM ET)

The Senior Loan Officer Opinion Survey on Bank Lending Practices (2 PM ET)

Tuesday, May 5

LMI Logistics Managers Index – April (6 AM ET)

Trade Balance – March (8:30 AM ET)

S&P Global US Services PMI (Final) – April (9:45 AM ET)

ISM Non-Manufacturing PMI – April (10:00 AM ET)

JOLTs Job Openings & Quits – March (10:00 AM ET)

New Home Sales – March (10:00 AM ET)

Wednesday, May 6

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

ADP Employment Change Report – April (8:15 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, May 7

Challenger Job Cuts Report – April (7:30 AM ET)

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Productivity & Unit Labor Cost – Q1 2026 (8:30 AM ET)

Construction Spending – February, March (10:00 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Consumer Inflation Expectations – April (11 AM ET)

Consumer Credit – March (3 PM ET)

Friday, May 8

Employment Report – April (8:30 AM ET)

University of Michigan Consumer Sentiment Index (Prelim) – May (10:00 AM ET)

Wholesale Inventories – March (10:00 AM ET)

International

Monday, May 4

Eurozone: S&P Global Manufacturing PMI – April

Eurozone: ECB Survey of Monetary Analysts, Annual Report

Tuesday, May 5

UK: New Car Sales - April

Wednesday, May 6

China: RatingDog Services PMI – April

Eurozone: S&P Global Services PMI – April

UK: S&P Global Services PMI – April

Thursday, May 7

Eurozone: Retail Sales – March

We have another busy week of earnings, with five Portfolio holdings reporting. Following the upsized 2026 hyperscaler capital spending figures this week, what we hear from Arista Networks (ANET) and Eaton (ETN) should be very positive. Based on what we hear and see in their respective backlog figures, we will revisit our price targets for both holdings. Also on deck are Palantir (PLTR) , SuRo Capital (SSSS) , and Axon Enterprise (AXON) . In the EPS Diplomats basket, Lumentum (LITE) will also report next week.

Per data from Nasdaq, as of April 15, there were ~3.1 million shares short Axon, which equates to just over two days to cover. We think the market has incorrectly hit AXON shares with the “SaaSpocalypse” brush, while also ignoring signals that point to AI adoption in the public safety sector, in addition to adoption of body cameras, drones, and other hardware in that market and others.

We will continue to collect data points and updated guidance from the likes of Advanced Micro Devices (AMD) , Duke Energy (DUK) , GlobalFoundries (GFS) , and others, connecting them back to our holdings as well as those we are eyeballing for consideration.

Monday, May 4

Open: Norwegian Cruise Line (NCLH), Tyson Foods (TSN)

Close: Advanced Energy (AEIS), Boise Cascade (BCC), Diamondback Energy (FANG), onsemi (ON), Palantir (PLTR), Paramount Skydance (PSKY), Sonos (SONO)

Tuesday, May 5

Open: ADM (ADM), AGCO (AGCO), Anheuser Busch InBev (BUD), Cummins (CMI), Duke Energy (DUK), DuPont (DD), Eaton (ETN), GlobalFoundries (GFS), Idexx Labs (IDXX), KKR (KKR), PayPal (PYPL), Pfizer (PFE), Rockwell Automation (ROK), TopBuild (BLD)

Close: AMD (AMD), Arista Networks (ANET), Dentsply Sirona (XRAY), Emerson (EMR), Interparfums (IPAR), International Flavors (IFF), Lumentum (LITE), Navitas Semiconductor (NVTS), Qorvo (QRVO), Skyworks (SWKS), Super Micro Computer (SMCI), SuRo Capital (SSSS), Veeco Instruments (VECO)

Wednesday, May 6

Open: Bloomin’ Brands (BLMN), Clear Secure (YOU), CVS Health (CVS), Dine Brands (DIN), Edgewell Personal Care (EPC), Elanco Animal Health (ELAN), Insulet (PODD), Kraft Heinz (KHC), Marriott (MAR), New York Times (NYT), Restaurant Brands (QSR), Uber (UBER), Utz Brands (UTZ), Walt Disney (DIS)

Close: American States Water (AWR), Axon (AXON), CF Industries (CF), DoorDash (DASH), Fastly (FSLY), Kratos Defense & Security (KTOS), Kulicke & Soffa (KLIC), LegalZoom (LZ), Realty Income (O), Snap (SNAP), Sunrun (RUN), Whirlpool (WHR)

Thursday, May 7

Open: Canada Goose (GOOS), Datadog (DDOG), GATX (GATX), Grainger (GWW), Installed Building Products (IBP), Lamar Advertising (LAMR), McDonald’s (MCD), Papa John’s (PZZA), Peloton (PTON), Radware (RDWR), Shake Shack (SHAK), Tapestry (TPR), Trex (TREX)

Close: Airbnb (ABNB), AMN Healthcare (AMN), Block (XYZ), Cloudflare (NET), CoreWeave (CRWV), Gilead (GILD), GoodRx (GDRX), Lyft (LYFT), Motorola Solutions (MSI), Post (POST), Sony (SONY), Synaptics (SYNA), Toast (TOST), Warner Music (WMG)

Friday, May 8

Open: AMC Networks (AMCX), Construction Partners (ROAD), Fluor (FLR), Wendy’s (WEN)

Portfolio Investor Resource Guide

Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company's Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

Stocks & Markets Podcast Links

Some helpful links if you prefer to catch the podcast on the go, in the car, or wherever. Be sure to give it a like or thumbs up and leave a review if you’re so inclined. We’d appreciate it.