What’s Our Game Plan for Palantir?

Let’s discuss PLTR’s oversold condition, increased earnings expectations, and notable valuation.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The calls by folks to discuss the Pro Portfolio’s position in Palantir (PLTR) have not gone unnoticed, and after clearing our desk of this morning’s comments and the May Durable Goods report, let’s get into it.

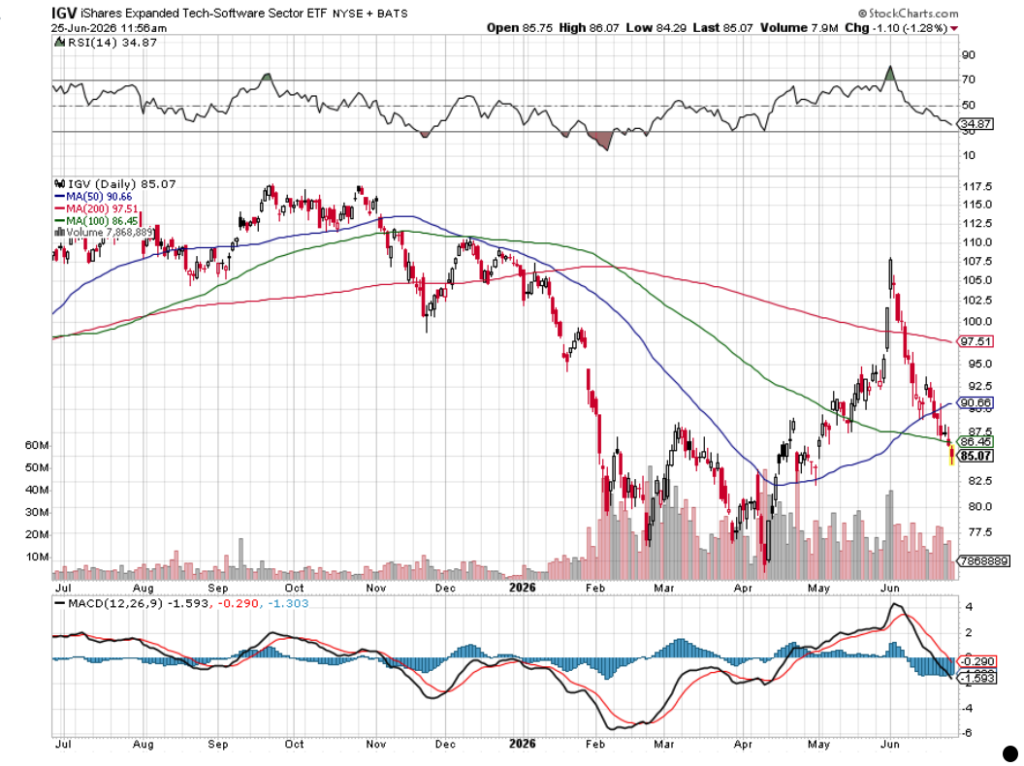

As we do, let’s first set the backdrop for the conversation, and that is PLTR shares and their move lower joined by many others in the software space. We see that firsthand with the drop in the iShares Expanded Tech-Software Sector ETF (IGV), which is down more than 20% from its recent peak. The difference in the beta figures for IGV at 1.12 and Palantir’s 1.51 helps explain the larger dop in PLTR and their oversold condition.

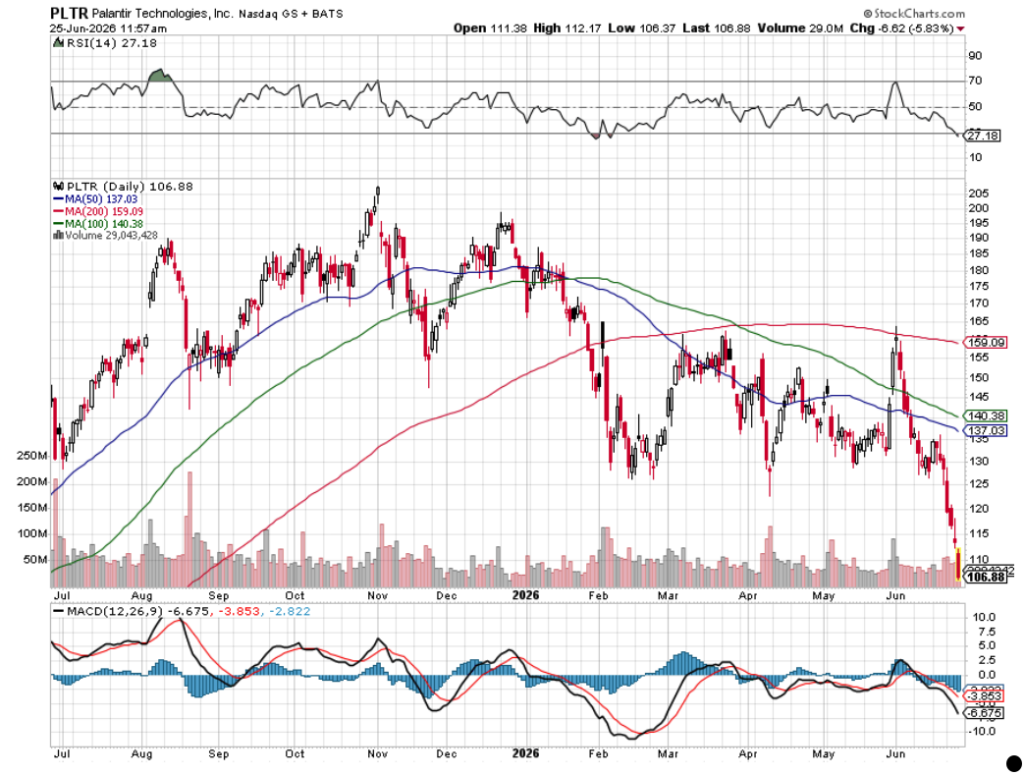

That oversold condition and the fact that PLTR shares are dancing around the Portfolio’s $109 checkpoint explain the, let’s call it, understandable interests from followers of the Portfolio.

We know software stocks have been facing some major headwinds over questions ranging from AI displacement to per-seat pricing. We also know, from our conversations about Axon (AXON), that companies can be painted with a wide brush by investors and most likely algorithms that focus on company classifications, even though they may not properly reflect a company’s business, what’s driving it or, more importantly, its operating profit. For example, per S&P Global, Amazon (AMZN) lands in the global industry classification standard (GICS) code of Consumer Discretionary, even though AWS accounts for nearly 60% of overall profits.

But I digress.

Those questions about software stocks that have weighed on companies from Salesforce (CRM), ServiceNow (NOW), and Elastic (ESTC), are pulling PLTR shares lower. Adding to that are the folks who have continued to use a P/E ratio to value PLTR. The fact that Elastic announced a 7% headcount reduction yesterday following layoff announcements at Salesforce, Oracle (ORCL), Intuit (INTU) and others refuels those questions.

At the same time, however, all the signals we collect point to not only accelerating AI adoption but expanding usage. Unlike the flat-to-down remaining performance obligations (RPOs) reported by Salesforce and ServiceNow, Palantir’s RPOs continued to step up in recent quarters. So did the company’s total customer count, as well as its commercial customer count. As their AI adoption rises and usage expands, that bodes well for Palantir’s billings and RPOs in the coming quarters. That helps explain the move up in consensus EPS expectations for Palantir for the current quarter in the last week, and also for the September quarter.

We’ll also note that Palantir’s consensus EPS figures for this year now sit at $1.47, up from $1.32 60 days ago, while for 2027 the consensus figure is now at $2.08 vs. $1.86 60 days ago. The math behind those revisions shows a tick higher in the implied EPS growth rate to just over 41% in 2027.

The multi-year outlook for AI adoption and expanding usage is one of the reasons we prefer to use a P/E-to-growth or PEG ratio to value PLTR, not a P/E ratio. Using 2025 as the base year and going out to 2028, using the $3.00 consensus EPS figure, the EPS compound annual growth rate over the 2025–2028-time frame is 60%. Based on 2027 EPS expectations, PLTR shares are trading at a PEG ratio of 0.85. And for those curious folks, on a 2026 basis, the current PEG ratio stands at 1.2. That suggests PLTR shares are the cheapest they have been in quite some time.

For that reason, the Pro Portfolio is not inclined to exit its PLTR position.

In fact, we are interested in picking up additional shares for the Portfolio, understanding of course that given market sentiment about “software” stocks, we will have a bit of an uphill battle. But we’ve faced them before, notably with Marvell (MRVL) last year. As we saw then, following the data tends to play out in the long run.

Given what we see with the MACD indicator in the Palantir stock chart above, any move in the very near-term would be on the smaller side. A larger bite would make more sense if we see the oversold condition joined by a flattening in the MACD indicator, like we saw back in February.

As we contemplate that move, it’s not lost on us that at last count ~69.2 million shares were short, which equates to roughly 1.8 days to cover. Given the oversold condition PLTR is in and the short interest in the stock, any unexpected, good news could trigger a wave of short-covering. That gives us a reason to pick up at least some additional PLTR shares sooner than later.

More Pro Portfolio:

- Locking in Big Gains on Two Positions

- Tracking 21 Signals Across 10 of Our Investing Themes

- Weekly Roundup: Peace Deal, Warsh Arrives, and the Portfolio Moves Ahead

At the time of publication, TheStreet Pro was long AMZN, MRVL, and PLTR.