Weekly Roundup: Reasons to Be Cautious

The new quarter started on a positive note for the portfolio, but here's why we want to tread carefully as we enter second-quarter earnings season.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The start of the new quarter was a positive one overall for the market, with gains in the S&P 500 and the Nasdaq Composite while the equal-weighted S&P 500, Dow, and Russell 2000 trailed. As indicated by the moves higher in the S&P 500 and Nasdaq, it’s fair to say the June PMI reports this week from ISM returned the notion that bad news is good news for stocks. Bad news because those reports found both the manufacturing and services economies contracting, but good news in that favorable inflation comments support the Fed being that much closer to rate cuts.

When he spoke on Tuesday, Fed Chair Powell shared the Fed is facing the two-sided policy risk of loosening Fed policy too late and doing it too early. Easing too early runs the risk of re-igniting inflation while easing too late from what the Fed already considers restrictive policy could threaten the economy. This week’s data from ISM suggests that restrictive policy is impacting the economy as did the drop in private sector payrolls seen and the higher June Unemployment Rate found in Friday’s June Employment Report.

In our view, that supports the case for rate cuts to start later this year, and it will take more data of that ilk to solidify thoughts of more than one rate cut in 2024. Should July, August, and September ISM PMI data reaffirm the picture laid out in the June findings we could see market excitement return for multiple rate cuts. Whether such thoughts will be warranted or are only hopium-filled will be determined by the data.

Since the Fed isn’t likely to cut rates anytime soon, the onus will be on corporate earnings to further the market rally that has led the S&P 500 more than 12% higher since mid-April. We’ve participated significantly in this move, but it also means we will be busy the next few weeks with the June-quarter earnings season. In addition to assessing customer, competitor, and supplier comments for our holdings, as well as their own earnings reports, we’ll be taking stock of second-half 2024 consensus EPS expectations for the S&P 500.

Because the index's current P/E ratio is bumping up against its 2021-2022 highs, H2 2024 EPS expectations for the S&P 500 basket of companies will need to be higher than the 11.5%-12.5% compared to H1 2024 and H2 2023 forecasted by the market in order to drive meaningful upside from current levels. Should guidance from the first few dozen companies to report not support such an outlook, we could see the market give back some of its pronounced gains since mid-April.

In the past when we’ve seen the market in overbought territory, it has often been priced to perfection. Those are Wall Street words for saying even the smallest wrinkle in the market could be disruptive. Add in the market being technically overbought, and it means we will want to tread carefully as we enter June-quarter earnings season that begins late next week.

Catching Up on the Portfolio This Week

The start of the new quarter was a positive one for the portfolio. Gains were led by our positions in Apple AAPL, Amazon AMZN, Costco COST Alphabet GOOGL, Universal Display OLED and several others that outperformed the S&P 500 this week. Those gains were partly offset by the decline in Builders FirstSource BLDR and Elevance Health ELV. We will remain patient with BLDR shares, which because our multi-quarter thesis and current position size remain on our shopping list. Shares of Elevance Health were knocked lower by poor reviews of the company’s digital pharmacy, and our take is management will address this given the potential cost savings to be had.

Actions taken by the portfolio this week included Monday’s pick up of more Marvell MRVL shares, a move that expanded our exposure to this digital infrastructure company. In Friday’s video, we noted MRVL shares have moved higher since that buy, but still offer newer members a nice entry point. That same day we lifted our price targets for Bank of America BAC and Morgan Stanley MS following post-Fed stress test dividend announcements.

On Wednesday, the significant rise in Universal Display shares pushed the portfolio’s position size well past the 4.5% level, which led us to do some prudent register ringing. We continue to see a bright future for the company and our shares, and we will revisit our current $225 price target once we have digested the June revenue report from Taiwan Semiconductor (TSM).

Monday’s May Construction Spending report and Friday’s June Employment Report contained positive data points for the portfolio’s positions in construction-related United Rentals URI, Vulcan Materials VMC, and Builders FirstSource.

On Friday, we shared that both the S&P 500 and the Nasdaq Composite have returned to overbought status. Recognizing this, we will tread carefully ahead of next week’s inflation data and the start of the June-quarter earnings season. Should wrinkles appear in any of those reports, we would see the market give back some of its recent gains, which have been pronounced, especially since mid-February.

Our game plan will be to revisit our shopping list, which as mentioned, includes Builders FirstSource, ServiceNow NOW, and Labcorp LH. We’ll also be seeing if any positions are over-extended and warrant some trimming, moves that should they come about would help rebuild the portfolio’s cash position.

This Week's Portfolio Videos and Podcasts

We cover a lot of ground during the week in our Daily Rundowns and the Portfolio Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, July 1: Let's Talk About Our Latest Trade, Cash Levels and Important Data

Tuesday, July 2: Our Reaction to Powell’s Policy Comments

Friday, July 5: Our Holdings Are Getting a Boost From AI

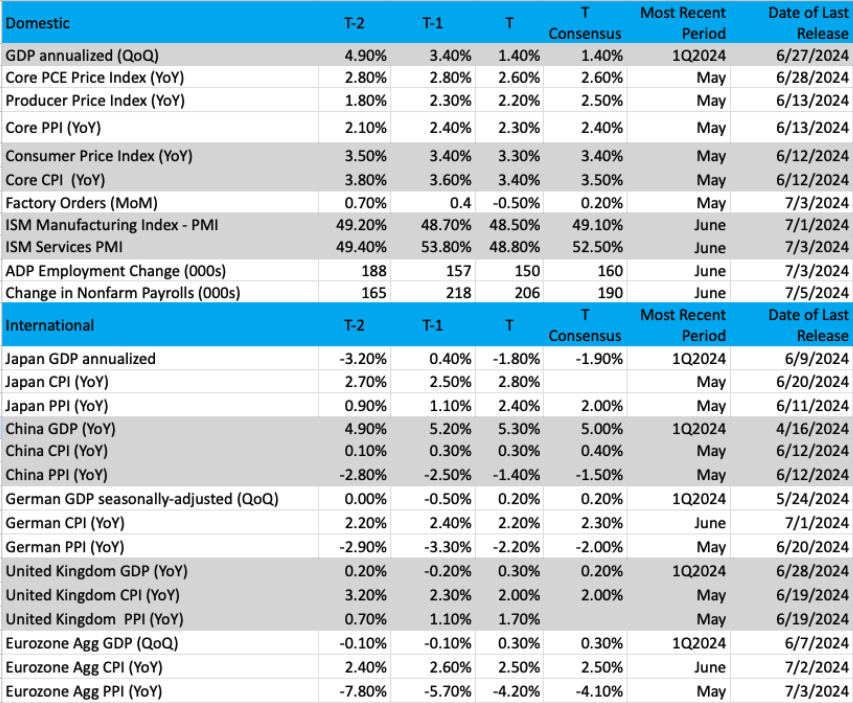

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: Financial Select Sector SPDR Fund (XLF)

Banks and financials have been leading markets higher over the past couple of months. Certainly, with names such as JPMorgan Chase (JPM), Bank of America, and Goldman Sachs (GS) with a head of steam that is enough to push the entire group forward.

Banks/financials are considered an important group in the markets, some say even more important than technology. Why is that?

Banks are the lifeblood of the economy, lending capital to businesses, and homeowners. Also, workers need to build their credit to help raise their social and economic status. Banks provide that outlet. Banks have always helped us gauge the health of the economy and the consumer. With all the noise about a faltering economy (and consumer) in 2024, they both have fared well and so have bank stocks. When they do poorly, like during the Great Financial Crisis (GFC) from 2008/09, everyone suffers.

With earnings season on the near-term horizon, we have these big banks stepping up to the plate first. Will they hit a home run or strike out swinging? The charts/technical conditions may offer us some clues. We suspect the positive charts of the banks, including the Financial Select Sector SPDR Fund (XLF), are telling us the earnings will be strong.

The chart of the XLF is one we follow closely, in part because two of the portfolio’s holdings – Bank of America and Morgan Stanley – are good-sized positions inside this ETF. The

XLF shows very strong indicators, the MACD (moving average convergence/divergence) remains bullish, and stochastics (pane 4) indicate strong momentum. While the top pane of the price chart (candles) shows a flat move, there is a higher high, higher low pattern present – the textbook definition of an uptrend.

Other charts we shared with you this week were:

Monday, July 1: S&P 500 - Large-Caps Were the Story in the First Half of 2024

Monday, July 1: Universal Display (OLED) - Step Aside Nvidia and Apple, Universal Display's Lighting Up

Tuesday, July 1: Amazon (AMZN) – Amazon Muscles Its Way to New Highs

Wednesday, July 3: Meta Platforms (META) – Keep Your Eyes on Meta

The Coming Week

The last three weeks were relatively calm ones given the June and July holidays and the closing of the June quarter. However, next week means we are back in business with June inflation data and the start of the June-quarter earnings season. Reverberations from Friday’s ABC News interview with President Joe Biden could be a factor in how we begin next week as investors start to focus on the upcoming presidential election.

Midweek, the Atlanta Fed will issue its next update for its rolling Q2 2024 GDP forecast better known as its GDPNow model. Following this week’s June PMI reports, that model slumped to 1.5% from 3.0% in late June, but its next update on July 10 will factor in Friday’s June Employment Report.

Learnings from the June CPI and PPI reports on Thursday and Friday will give the central bank further fuel to revisit that GDP forecast. Based on what we saw in the June PMI reports, we are likely to see further improvement in both of those inflation indicators. That confirmation will be another step in moving the Fed closer to eventual rate cuts.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, July 8

· Consumer Inflation Expectations – June (11:00 AM ET)

· Consumer Credit – May (3 PM ET)

Tuesday, July 9

· NFIB Small Business Optimism Index – June (6:00 AM ET)

· Fed Chair Powell Testimony (11 AM ET)

Wednesday, July 10

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Wholesale Inventories – May (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, July 11

· Jobless Claims, Initial and Continuing – Weekly (8:30 AM ET)

· Consumer Price Index – June (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Treasury Budget – June (2 PM ET)

Friday, July 12

· Producer Price Index – June (8:30 AM ET)

· The University of Michigan Consumer Sentiment Index (Prelim) – July (10 AM ET)

International

Wednesday, July 10

· China: Producer Price Index, Vehicle Sales - June

Thursday, July 11

· Japan: Machine Tool Orders - June

Friday, July 12

· China: New Yan Loans - June

Late next week, June-quarter earnings season will kick off in earnest with quarterly results from PepsiCo PEP, and the first swath of reports from big banks, which will set the tone for results from Bank of America and Morgan Stanley on July 16. With PepsiCo, we’ll be looking for confirmation that its seasonally stronger second half is poised to repeat, and we’ll compare that against comments from frozen food company ConAgra (CAG).

With regard to the big banks, including JPMorgan, it will be their comments on the economy, loan activity, trading volumes, and asset gains as well as investment banking activity. We’ll also be interested in what Helen of Troy (HELE) says about its beauty business even though the market will likely focus on its Home & Outdoor and Health & Wellness segments. While it’s a modest player in Beauty, should that segment be a strong performer, it would be a nice data point for Coty COTY.

Here's a closer look at the earnings reports coming at us next week:

Monday, July 8

· Open: Greenbrier (GBX)

Tuesday, July 9

· Open: Helen of Troy (HELE)

Wednesday, July 10

· Close: PriceSmart (PSMT), WD-40 (WDFC).

Thursday, July 11

· Open: Delta Air Lines (DAL), PepsiCo (PEP)

· Close: Cintas (CTAS), ConAgra (CAG), Progressive (PGR)

Friday, July 12

· Open: BNY Mellon (BK), Citigroup (C), Ericsson (ERIC), Fastenal (FAST), JPMorgan Chase (JPM), Wells Fargo (WFC).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.