Beneath the Headline, the June Jobs Report Is Fed-Friendly

With the market once again overbought, a potential for a wrinkle in next week’s reports means prepping our shopping list.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* The market should like the June Employment Report as it sends Treasury yields lower.

* Slower private job creation, slower wage gains, and the rise in the Unemployment Rate are all Fed-friendly.

* With the S&P 500 and Nasdaq back in overbought territory, we will be revisiting our shopping list ahead of next week's CPI, PPI, and earnings reports.

* The June Employment Report supports our view on three building stocks.

We may be in for another low-volume Friday sandwiched between the Independence Day holiday and the weekend, but the June Employment report is sending Treasury yields lower, pointing to a favorable end to the week.

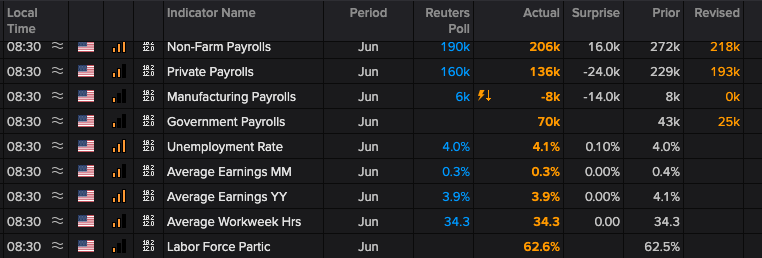

A few things are leading those yields to fall, including the June Unemployment Rate hitting 4.1%, which is above the Fed’s 4.0% June dot-plot forecast. Wage gains, as expected, ticked lower, compared to May’s 4.1% figure. And while headline June job creation of 206,000 was ahead of the 190,000 consensus forecast, private payrolls showed a far greater decline to 136,000 from the revised May figure of 193,000 than the market expected. We’d also note the report showed 111,000 fewer jobs were added during April and May.

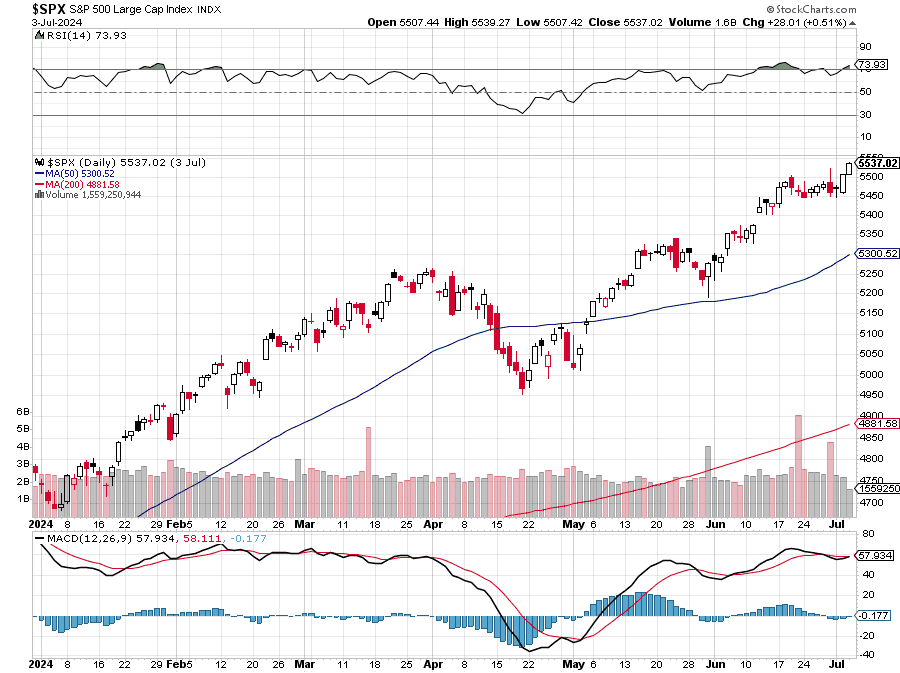

All told, the report supports the Fed eventually starting to cut interest rates and that should help the market move higher even after setting new records earlier this week and moving back into overbought territory.

As of this morning, the S&P 500’s relative strength index (RSI) is 73.93, while the RSI for the Nasdaq Composite is 73.25. Based on this week’s June PMI reports, next week’s June CPI and PPI reports should show continued progress for inflation.

Because the market is overbought, a wrinkle in either of those reports or with the start of the June-quarter earnings season next week could lead some traders to take profits following the double-digit move in the S&P 500 since mid-April. Recognizing this potential, we’ll be revisiting our shopping list ahead of that action late next week.

One other positive we would call out today was the continued growth in construction jobs, which added another 27,000 during June with continued gains in both non-residential and residential construction. That builds on the number added in May, confirming the seasonal pick-up in activity. That bodes well for our holdings in United Rentals URI, Vulcan Materials VMC, and Builders FirstSource BLDR. To that we can add the drop in the construction unemployment rate, which fell to 3.3% in June from 3.6% the month before.

More Pro Portfolio:

- Locking in Big Gains on This High-Flying Stock

- Weekly Roundup: Looking to the Second Half

- How the Latest Signals Are Impacting Our Portfolio Holdings

At the time of publication, TheStreet Pro Portfolio was long URI, VMC and BLDR.