Weekly Roundup: Profiting From the Rally, But Not Letting Our Guard Down

We locked in big gains this week, added to two holdings, upgraded a rating, and lifted price targets on three positions.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It was another positive week for the market, bringing the tally of successive week-over-week gains that much higher. The gain for the S&P 500 pushed that market index further into a double-digit move on a quarter-to-date basis and pulled its year-to-date one that much closer to 10%. The Cboe Volatility Index retreated to its lowest level since late January, as market watchers continued to hope for a peaceful settlement between the U.S. and Iran.

Late in the week, indications were the U.S. and Iran still had key differences between them on the topics of enriched uranium and tolls for the Strait of Hormuz. On Friday, U.S. Secretary of State Marco Rubio said there was “slight progress” during talks with Iran amid uncertainty about whether a deal will be reached or war will resume. In our view, things could go either way, and for that reason we will continue to keep the Portfolio’s inverse ETF positions in play.

Should we see a clear path to peace emerge, we would consider unwinding those inverse ETF positions. We would also have to consider whether that path clearing could be a “buy the rumor, sell the news” event following the market’s double-digit move over the last several weeks, as well as the time to re-open the strait and get oil and other petrochemicals flowing. Based on this week’s Flash May PMI report from S&P Global, the probability is high we’ll see May inflation data move up compared to March and April.

That makes Friday comments from Federal Reserve Governor Christopher Waller that he’s concerned higher energy prices will leave a lasting imprint on inflation a notable one. Waller added that it is “unclear” how long the conflict in the Middle East will impact constrained supplies, high gas prices and goods.

Those renewed inflation tailwinds were captured in comments from retailers this week, including Walmart (WMT), and Friday’s preliminary May reading of consumer sentiment. That index fell for the third straight month as gas prices continued to rise. The index reading is now just below the previous historical trough seen in June 2022.

Inflation expectations over the year ahead rose to 4.8% from 4.7% last month, and well above the 3.4% reading seen in February, before the war began. This adds to the thinking consumers will be mindful in their spending, supporting the comment I made about investors potentially using certain retailers and consumer-facing companies as a source of funds for the upcoming wave of IPOs.

We will continue to follow the signals we collect each week and stick to following where capital is being spent by companies, consumers, and other entities. Next week that means paying attention to the modicum of corporate earnings reports and management comments as we trade the earnings season for investor conferences. On that front, next week brings several events to tune into, including:

Jefferies Software, Internet, and AI Conference

Bank of America Power Utilities and Cleantech Conference

Bank of America Power Utilities and Cleantech Conference

TD Cowen 54th Annual Technology, Media & Telecom Conference

Deutsche Bank Global Financial Services Conference

Bernstein 42nd Annual Strategic Decisions Conference

With U.S. equity markets closed on Monday, we’ll wish you a wonderful holiday weekend, and see you bright and early back here on Tuesday. For your weekend reading pleasure, be sure to catch our latest patch of Portfolio Signals.

Catching Up on the Portfolio This Week

We closed out another positive week for the market and for the Pro Portfolio. Quarter to date, our collection of individual positions and the EPS All-Stars basket is up more than 15%. Week over week we narrowed the gap between the Portfolio’s year-to-date return and that for the S&P 500. Helping us to that were the strong moves in Marvell (MRVL), Arista Networks (ANET), TJX (TJX), SuRo Capital (SSSS), Morgan Stanley (MS), and the First Trust Nasdaq Cybersecurity ETF (CIBR).

The EPS All-Stars basket continued to power ahead, adding several percentage points to its QTD return. Double-digit gains this week in Bloom Energy (BE) and Credo Technology (CRDO) were the primary drivers as was the mid-single-digit climb in Micron (MU). QTD, the basket is up about 55% compared to 14.5% for the S&P 500.

Those weekly gains were offset by a decline in Nvidia (NVDA), Alphabet (GOOGL), Eaton (ETN) and United Rentals (URI), as well as our market-hedging positions. Above, we discussed our plan for the inverse ETFs we hold in the Portfolio, and we suspected the market’s reaction to Nvidia’s Wednesday night earnings report would turn out this way. We explained our thoughts on that report and guidance, laying out why we remain bullish and the reasons behind our new $280 target. In that same note, we increased our Marvell price target to $210.

We made some trades with the Pro Portfolio this week, including adding to two positions and bowing to our discipline to lock in massive gains on another. Ahead of TJX’s (TJX) quarterly earnings report on Wednesday, we picked up more shares on Monday at $150.47, a nice spot given the favorable post-earnings reaction. Following that report, we boosted our TJX target to $185 from $180.

Following after the continued runup in GOOGL that led it to become an outsized position, we trimmed back the Portfolio’s holdings on Tuesday near $390. It was a very, very profitable move for the Portfolio. Following the trade, we still have a sizable position in Alphabet. We continue to see Google as being well positioned as it continues to monetize Search and YouTube, and benefit from continued AI adoption and usage, a nice combo for Google Cloud.

Thursday, we picked up more shares of American Express (AXP) very close to $310, and upgraded our rating to One from Two. Consumer spending has been better than expected of late, but as the cumulative effects of renewed inflation pressures are felt, Amex’s card fee driven profits and its more affluent consumer base should shine through.

On the dividend front, this week we collected our latest quarterly payment from Welltower (WELL). That leaves ones from United Rentals (URI) and Eaton (ETN) before we close out May next week. Another eight holdings will pay quarterly dividends in June, and among them will be Nvidia’s upsized dividend of $0.25 per quarter.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings during the week:

Monday: Morgan Stanley boosted its Nvidia target to $285 from $260, while KeyBanc took its target to $300. JP Morgan added $1 to its TJX target putting it at $174, and Truist initiated coverage with a fresh Buy rating and a $175 target. Amazon (AMZN) shares were added to the Jefferies’ Franchise Picks list. Melius upped its Marvell target to $220 from $140, and UBS upped its Broadcom (AVGO) target to $490.

Tuesday: Evercore reset its Broadcom target at $582 from $490 and took its Marvell target to $155. HSBC increased its Nvidia target to $325 from $295, Oppenheimer lifted its Costco target to $1,160 and Argus added $80 to its Applied Materials (AMAT) target, landing it at an even $500.

Wednesday: UBS reset its Costco target at $1,275. Oppenheimer did the same with its Marvell target, placing it at $200 from $170 as did Wells Fargo, which now sits at $195 from $135.

Thursday: Scotiabank’s Welltower target was upped to $248 from $236. Multiple price target increases for TJX to $175-$197 from $168-$175 at Telsey Advisory, Truist, UBS, Barclays, and others. Nvidia shares also saw numerous price target increases, clustering between $300-$350 but we saw some aggressive outliers, including Baird’s new $500 target and Evercore ISI’s $430 one. Citi took its Marvell target to $215 from $118 (where have they been on this stock?).

Friday: Loop Capital started American Express with a Buy rating, a $389 price target, and named the shares as its top Financials pick. Marvell’s price target was raised to $210 from $140 at Stifel.

Key Global Economic Readings

After spending time reviewing the existing data tracked in the Weekly’s macro-economic table, we find it needs an overhaul after so many years. We’re revamping the layout to make it easier to read, but also making some adjustments to the data tracked and presented.

We’ll aim to unveil this table in the forthcoming May Monthly Roundup.

Portfolio Videos

Monday, May 18 – How to Prepare for Nvidia Earnings

Wednesday, May 20 – What AI Means for Productivity as Nvidia Reports

hursday, May 21 – Rising AI Adoption Keeps Us Bullish on Nvidia

Friday, May 22 – What We Learned From the SpaceX IPO Filing

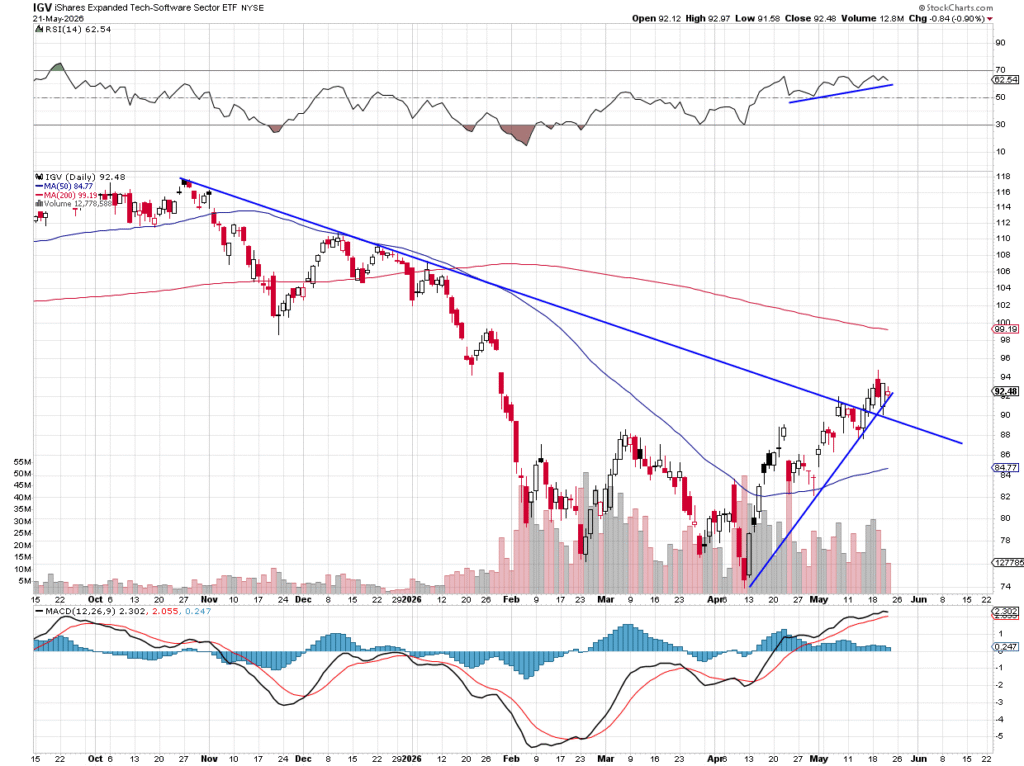

Chart of the Week: iShares Expanded Tech-Software Sector ETF

Remember the “old days” (sarcasm) when the markets shunned software names? Heck, it was only six weeks ago when this entire group was quickly forgotten, “software is dead, long live software.” Well, as we know, markets move in cycles as do specific sectors. With this group it has been such a long time (if ever) that a large adverse move stung so badly.

We can have a long discussion on how AI is going to destroy businesses and jobs in the future, but that is just speculation. Even Jensen Huang, the CEO of Nvidia (NVDA), claims this sector is being wrongly sold off, that software as a service (SAAS) is vital to the success of future AI initiatives and other new developments.

The IGV (iShares Expanded Tech-Software Sector ETF) has been on everyone’s radar. The chart below shows this ETF likely bottomed in early April and since then the IGV has been in a nice uptrend. Higher highs and higher lows are our textbook definition of an uptrend, and testing a bottom (from late February) makes us feel a bit more comfortable calling this a rally.

But let’s not get too excited here, the IGV is well below the 200-day moving average and sits in a “no man’s land” area between the 50-day and 200-day moving average. Resistance is right about $99 on the ETF. The positive here is the IGV is not going down much and continues to build on its momentum. Money flow is strong; volume is showing positive trends; and the MACD is firmly on a buy signal. The IGV has crossed above a downtrend line this week, which is bullish.

We pay close attention to the software group as it helps to drive better performance in the Nasdaq and technology stocks in general. Dip buyers have been active in adding the IGV, perhaps the next dip could be your opportunity as well.

Other charts we shared with you this week were:

Monday, May 18: S&P 500 – Weekly Candle Has Bearish Implications

Monday, May 18: Meta (META) – Meta Fails to Impress

Tuesday, May 19: Morgan Stanley (MS) – Morgan Stanley Stands Tall

Wednesday, May 20: Marvell (MRVL) – Despite Volatility, Marvell Remains Attractive

Thursday, May 21: Suro Capital (SSSS) – SuRo Is Looking Bullish as IPO Buzz Builds

The Week Ahead

We’ll have a compressed trading week following the Memorial Day holiday that will see U.S. equity markets closed on Monday. We wish you a fun time as you recharge your batteries before we barrel through economic data, some key earnings reports, and weekend developments on the U.S.-Iran front.

Upcoming economic data include the April PCE Price Index and a more detailed look at consumer spending in April. Given the comments we collected in S&P Global’s Flash May PMI and the hot April CPI and PPI readings, we’re already looking through the April PCE data, but even the Cleveland Fed’s Inflation Nowcasting models sees a step up to over 3.8% on a year-over year basis for the headline PCE figure.

If that’s the figure we get, it will build on the sharp increase found in the March figure of 3.5% from February’s 2.8% print. Coming off the latest Fed meeting minutes released this week that showed the topic of a rate hikes percolating, we’ll want to assess comments from Fed officials once the PCE price index data is published Thursday morning.

Here’s a closer look at the economic data coming at us next week:

U.S.

Monday, May 25 — Memorial Day (US Markets Closed)

Tuesday, May 26

S&P Case-Shiller Home Price Index – March (9:00 AM ET)

FHFA House Price Index – March (9:00 AM ET)

Conference Board Consumer Confidence – May (10:00 AM ET)

Dallas Fed Manufacturing Activity Index – May (10:30 AM ET)

Wednesday, May 27

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

ADP Employment Change Report – Weekly (8:15 AM ET)

Richmond Fed Manufacturing Index – May (10:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, May 28

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

GDP – Q1 2026 (Second Estimate) (8:30 AM ET)

GDP Price Index – Q1 2026 (Second Estimate) (8:30 AM ET)

Personal Income & Spending – April (8:30 AM ET)

PCE Price Index – April (8:30 AM ET)

Durable Goods Orders – April (8:30 AM ET)

New Home Sales – April (10:00 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, May 29

Goods Trade Balance (Advance) – April (8:30 AM ET)

Retail & Wholesale Inventories (Advance) – April (8:30 AM ET)

Chicago PMI – May (9:45 AM ET)

International

Tuesday, May 26

Japan: Leading Economic Index – March

Wednesday, May 27

China: Industrial Profits – April

Thursday, May 28

Japan: Housing Starts, Construction Orders – April

Eurozone: Economic Sentiment Indicator – May

Eurozone: Consumer Confidence (Final) – May

Germany: CPI (Preliminary) – May

Friday, May 29

Japan: Tokyo CPI, Industrial Production (Preliminary), Retail Sales – April

From a Pro Portfolio perspective, we have earnings from Costco (COST) and Marvell (MRVL) on deck. This week we prepared you for Costco’s adjusted April-quarter comp sales, and how they are poised to top those figures reported by Target (TGT), Walmart (WMT), Home Depot (HD) and others. The “unknown” we’ll focus on in Costco’s earnings is its high-margin membership fee revenue stream. We say unknown as the figure will reflect Costco’s expanding warehouse footprint and corresponding new membership growth. In the current economic environment, we would be surprised if membership renewal rates for the quarter surprise to the downside.

Turning to Marvell, over the last few months its custom AI silicon customers have won a number of programs, the most recent including Anthropic using Microsoft’s chips. On Thursday, we issued the same note of caution heading into that report that we made for Nvidia’s quarterly results —that it is one of very high expectations following the 150% move since early March compared to a move near 10% for the S&P 500.

At the end of April, about 28.2 million MRVL shares were short per data from Nasdaq. We should get a mid-May update for that in the next few days, but we’d be surprised if it was meaningfully lower. Subject to Marvell’s guidance and the market reaction, should a negative overreaction ensue, we’ll keep an open mind and our eyes on key support levels.

Outside of those two reports, we’ll continue to track comp sales figures from other retailers as they post their quarterly results and guidance. With Dell (DELL), its comments on AI server demand will be one we track closely, and we’ll also be watching what Salesforce (CRM) has to say about AI adoption in the enterprise. Following Workday’s (WDAY) flat backlog, we’ll be scrutinizing Salesforce’s RPO figure and comparing it to the $72.4 billion figure reported on February 25.

Here’s a closer look at the earnings reports coming at us next week:

Tuesday, May 26

Open: AutoZone (AZO)

Close: Box (BOX), Zscaler (ZS)

Wednesday, May 27

Open: Abercrombie & Fitch (ANF), Capri Holdings (CPRI), Dick’s Sporting Goods (DKS), Dycom (DY)

Close: Agilent (A), HP (HPQ), Marvell (MRVL), Salesforce (CRM), Snowflake (SNOW)

Thursday, May 28

Open: Burlington Stores (BURL), Dollar Tree (DLTR), Hormel Foods (HRL), Kohl’s (KSS)

Close: American Eagle (AEO), Autodesk (ADSK), Costco (COST), Dell (DELL), Elastic (ESTC), Gap (GAP), NetApp (NTAP), Okta (OKTA), SentinelOne (S)

Friday, May 29

Open: Buckle (BKE)

Portfolio Investor Resource Guide

Economic Data: Here’s a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company’s Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here’s How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 – Buy Now (BN): Stocks that look compelling to buy right now.

2 – Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 – Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 – Sell (S): Positions we intend to exit.