June Services PMI: The Return of Bad News Is Good News?

The surprising sharp slowdown will weigh on June-quarter GDP forecasts and could bolster the case for the Fed to cut rates more than once in 2024.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* While the S&P’s June Services PMI was positive, ISM’s found an unexpected contraction in that part of the economy.

* Both reports showed further inflation progress during the month.

* ISM’s report and impact on GDP forecasts are boosting the odds of more than one rate cut this year.

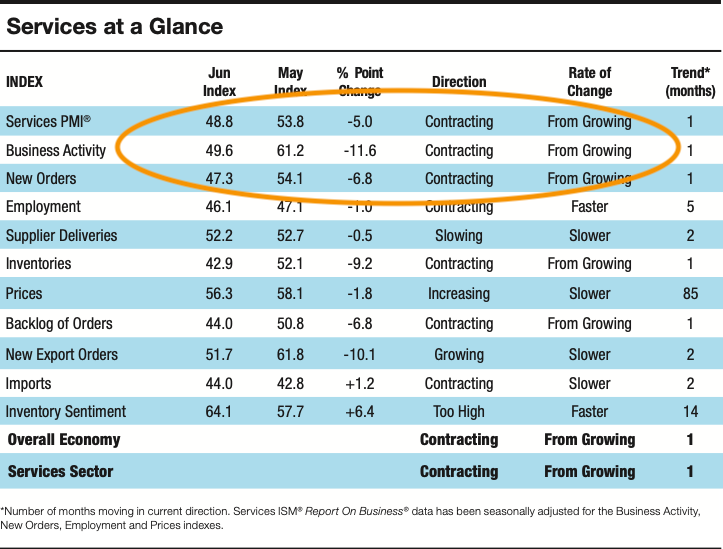

We are once again presented with mixed views on the economy, this time in the June Services PMI reports from S&P Global and ISM. While S&P’s findings showed a solid end to the quarter with its Services PMI rising to 55.3 from 54.8 in May with new orders expanding and a solid rise in workforce numbers, ISM’s painted a different picture — a surprising slowdown in what’s been driving the overall economy.

This isn’t the first time PMI reports from these firms have presented conflicting views, but just the way ISM’s June Manufacturing report weighed on Q2 2024 GDP forecasts so too will its June Services PMI data. That means there is a high probability we see the rolling GDP forecast from the Atlanta Fed, better known as its GDPNow model, revised lower yet again. That model fell to 1.7% for the June quarter from 2.2%, after ISM’s June Manufacturing PMI report, and following the May PCE and Personal Income & Spending Report.

Normally, such a miss in ISM’s data would sound alarm bells. Following Fed Chair Powell’s comments yesterday that the Fed is closely watching the speed of the economy because it doesn’t want to risk sabotaging it, the June ISM Services bad news is potentially good news for rate cuts. At the same time, the inflation commentary found in both S&P’s and ISM’s June Service PMI data showed further sequential progress for input and output prices. We see that supporting further improvement in next week’s June CPI and PPI reports — and the market seems to agree given today’s decline in the 10-year Treasury yield.

Arguably, the June ISM reports bolster the case for the Fed to cut rates more than the single rate cut telegraphed in its June set of economic projections. Indeed, the market is thinking that and those thoughts have tipped the odds of a September rate cut to more than 66%, up from 56% a week ago, per the CME FedWatch Tool. Not to parrot Powell, but we’re thinking the Fed will want to see more data to ensure it isn’t head faked, especially given the surprising slowdown depicted in the June ISM Services report.

Should upcoming data reaffirm ISM’s findings, we will likely see those rate-cut odds rise further. That potential shift should lift our tech plays and support our more interest-rate sensitive ones, including United Rentals URI, Vulcan Materials VMC, and Builders FirstSource BLDR.

More Pro Portfolio:

- Amazon's Spending Plans Prompt Us to Buy More Shares of This Position

- Weekly Roundup: Looking to the Second Half

- How the Latest Signals Are Impacting Our Portfolio Holdings

At the time of publication, TheStreet Pro Portfolio was long URI, VMC and BLDR.