Weekly Roundup: Portfolio Maintains Lead as Select Holdings Do the Heavy Lifting

We added to three holdings and started a new position during a roller-coaster week for the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market moved a bit like a roller coaster this week. It started with a continuation of last week’s decline, only to rebound sharply following Thursday’s comments that a deal between the U.S. and Iran was largely done. That helped the market bounce, although there were still some questions about potential mixed messages.

Leaked terms of a proposed memorandum to end the war in the Gulf outlined by Western, Pakistani and Iranian sources on Friday appeared to favor Iran, drawing criticism from President Trump, who called the reports inaccurate. Subsequently, Iranian Foreign Minister Seyed Abbas Araghchi said that a deal has “never been closer.” Araghchi went on to say that the details of a memorandum of understanding with the U.S. will be shared publicly “in due course.”

Those developments, along with the initial trading of SpaceX (SPCX) shares, helped the stock market regain the ground it lost last week. As we’ll discuss below, TheStreet Pro Portfolio did the same this week, keeping its quarter-to-date and year-to-date leads over the S&P 500.

The silver lining in the market’s pullback early in the week is that even after its bounce back Thursday and Friday, based on their relative strength index (RSI) levels, neither the S&P 500 nor the Nasdaq Composite are in an overbought condition. As we write this week’s Roundup those RSI levels are hovering around 50 for both indexes, and that tells us the market is on neutral footing. The Fear & Greed Index, meanwhile, was still flashing “Fear” as we put the trading week to bed.

While we are optimistic about for a U.S.-Iran deal, our view is the details of any final deal is what we and other investors should focus on. Whether that is what is shared in the coming days or just a memorandum of understanding with further talks to ensue will be made clear in the coming days. Chatter is we may could see a formal announcement this weekend, ahead of the upcoming G-7 summit that will run from June 15-17. Time will tell how much there is in what’s announced.

Next week brings Kevin Warsh’s initial outing as Fed Chair, including his first post policy decision press conference. Coming off this week’s May inflation data that climbed another ladder rung higher, we are waiting to see Warsh’s comments about renewed inflation pressures and the path forward for monetary policy under his leadership. With a hat tip to Pro Portfolio friend J.D. Durkin, we would remind you that FOMC stands for Federal Open Market Committee, not Federal Open Market Chair.

Current market expectations captured in the CME FedWatch Tool do not foresee a rate cut this year or next and we’d note the odds of a 25-basis point rate hike by the Fed’s December 2026 meeting are on the rise. This gives us more reason to parse Warsh’s words next week very carefully, cross-referencing them with the updated Set of Economic Projections the Fed will publish as well. If both remove that rate-hike probability, it will give the market a reason to move higher.

Once again, we are heading into the weekend keeping our eye on the ball, and that means we’ll be sharing any Saturday or Sunday developments with you early Monday morning.

Enjoy your weekend, Saturday’s Signals alert, and catch a Word Cup match or two if you can.

Catching Up on the Portfolio This Week

The Pro Portfolio inched ahead this week, maintaining its lead over the S&P 500. Double-digit gains in Applied Materials (AMAT) and strong week-to-week performance in Arista Networks (ANET), American Express (AXP), Bank of America (BAC), Marvell Technology (MRVL), TJX Companies (TJX), and Welltower (WELL) offset declines in Apple (AAPL), Axon Enterprise (AXON), and several others holdings.

Apple’s WWDC 2026 unveiling of the revamped Apple Intelligence and Siri AI unveiling left us underwhelmed. However, we also recognize that as Apple releases the first public beta of its newest software platforms, which include the overhauled Apple Intelligence and Siri AI across iOS, iPadOS, macOS, and its other platforms, that will tell us whether these new offerings are winning over users or are falling flat. Those public betas are expected to be released “next month,” which likely means before Apple reports its June-quarter results.

In Saturday’s batch of Portfolio Signals, we discussed several that speak not only to rising body camera adoption in the public safety market but AI adoption as well. We have our $425 pick-up point for AXON shares, and we are watching it closely along with those for other existing positions.

Several components of the EPS All-Stars basket also outperformed the S&P 500 this week, but where that the really model shined was with Credo Technology (CRDO) and Micron (MU), and their double-digit week-over-week gains.

We made some trades this week that increased the Portfolio’s position sizes, with two buys in Broadcom (AVGO), one on Tuesday and the other on Thursday. We also picked up more shares of Netflix (NFLX) on June 9 and Eaton on June 11 following Eaton’s combination of its mobility solutions segment with Dana, retaining 50.1% of the combined company. Thursday afternoon, we started a new position in heavy and medium-duty truck company Paccar (PCAR) with a Two rating and a $135 price target.

Following those moves, the Portfolio’s cash position stood at ~8.2% of its assets. We should see those cash levels drift higher over the final June trading days as we have several dividend payments coming our way from Google (GOOGL, Waste Management (WM), Meta (META), Bank of America (BAC), Nvidia (NVDA), and Broadcom (AVGO).

We continue to keep a close watch on recent Bullpen additions. As we contemplate our next moves, we’ll consider the upcoming EPS All-Stars reconstitution, which will start on June 30 and conclude on July 1. With that reconstitution, we intend to increase the starting position size for the strategy to 6.0% of the Portfolio’s assets. We will consider topping out the model’s position size at 8% with the September 30-October 1 reconstitution.

Now let’s see what others on Wall Street had to say about the Portfolio’s holdings this week:

Monday: BofA raised its price target for Arista Networks (ANET) to $200 from $185.

Tuesday: Morgan Stanley raised its Apple (AAPL) price target to $360 from $330; TD Cowen raised to $350 from $335; Maxim raised to $350 from $310. TD Cowen raised its Google (GOOGL) price target to $475 from $450.

Wednesday: UBS raised its price target for Applied Materials (AMAT to $570 from $515, while Cantor Fitzgerald took its AMAT target to $650 from $575. Raymond James raised its price target on the shares of United Rentals (URI) to $1,275 from $1,100.

Thursday: Barclays raised its Applied Materials target to $590 from $500.

Friday: Morgan Stanley upped its Arista Networks target to $190 from $180, while JPMorgan increased its Morgan Stanley (MS) target to $187 from $179. B. Riley raised its Marvell (MRVL) target to $345 from $240.

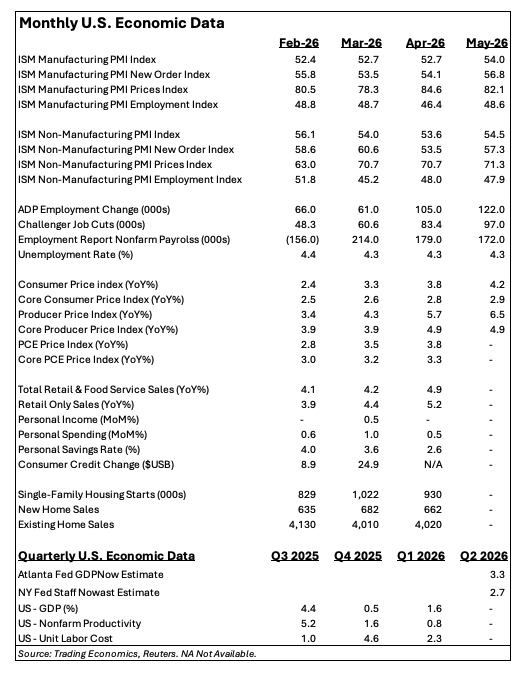

Key Global Economic Readings

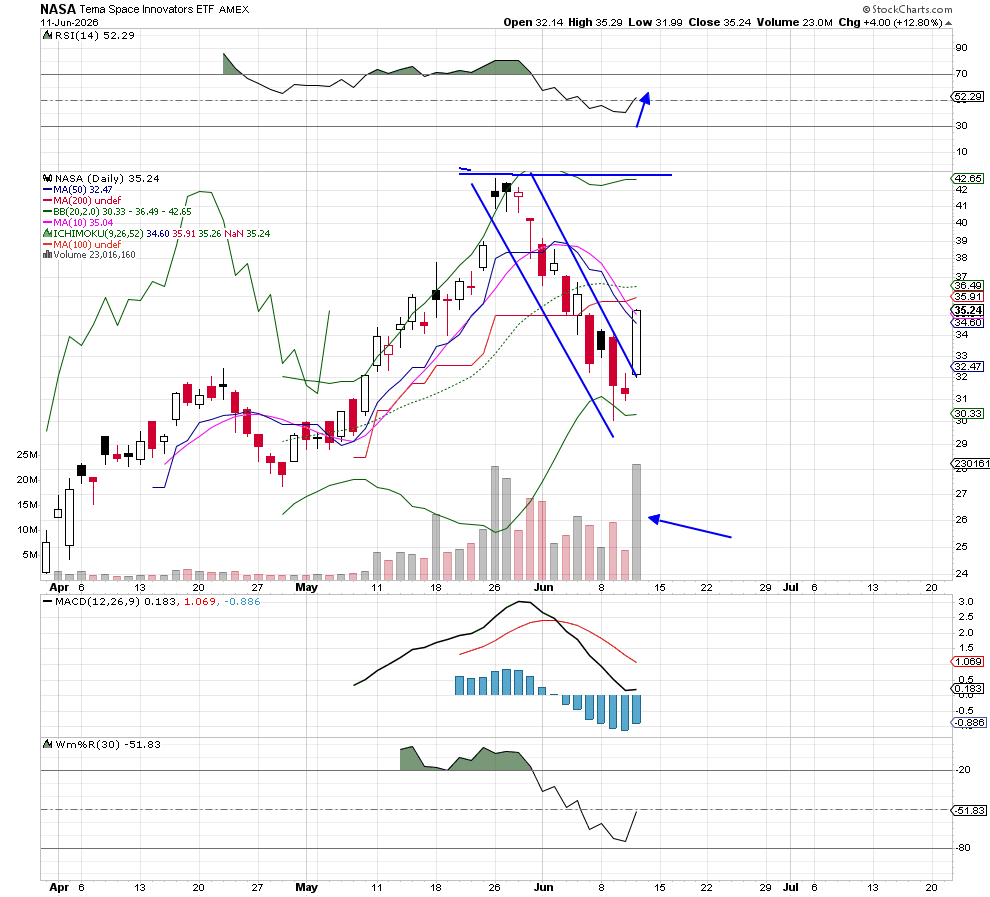

Chart of the Week: Tema Space Innovators ETF (NASA)

With today’s release of SpaceX (SPCX) IPO into the public market Bob thought it would be fun to chart/discuss one of the newer space-related ETFs, the Tema Space Innovators ETF (NASA). This ETF has only been trading since early April and boasts some very surprising names in the fund. This is not a very large market cap ETF, only about $2.6 billion, but it is the first pure-play ETF with exposure to one certain stock!

Some of the most obvious space names are in NASA, including Rocket Lab (RKLB), Intuitive Machines (LUNR), AST SpaceMobile (ASTS) and Planet Labs (PL). But did you know SpaceX was also a member, even before the IPO on June 12? Yes, this fund bought shares through a special purpose vehicle (SPV) that actually has a valuation of the shares that trade on the secondary market.

The exposure in the NASA ETF from SpaceX is rather wide, as low as 6% but as high at 10% (at the moment). No question when the shares are released and the excitement is fulfilled NASA will eventually have a much bigger weighting than 6-10% of SpaceX.

Other names in the ETF are likely to get some flows as well, some pin action from the biggest IPO ever. As for the chart, the NASA recently came off a low base and had a nice surge on June 11 with very strong volume. The ETF is volatile and will likely be running hard to move back toward old highs in the low $40’s. MACD is negative but the RSI is starting to turn upward, so a couple more up sessions for NASA could turn this ETF bullish.

If you found yourself empty handed from the SpaceX IPO with no shares or just very few of them, you might consider NASA as a good proxy for buying the new stock at a better price, knowing the ETF will be picking up many thousands of shares.

Other charts we shared with you this week were:

Monday, June 8: S&P 500 – Bears Take a Vicious Swipe

Monday, June 8: Apple (AAPL) – Is Apple a Port in a Storm?

Tuesday, June 9: Netflix (NFLX) – Netflix Continues to ‘Stream’ Lower

Wednesday, June 10: SuRo Capital (SSSS) – IPOs Are Exciting if You Already Own a Piece

Thursday, June 11: Arista Networks (ANET) – Arista Networks Is Trying to Catch a Break

The Week Ahead

Next week, we move into the home stretch for the current quarter, but we also have a U.S. market holiday on Friday, June 19.

Given our new position in Paccar (PCAR), we’ll be digging into the May Industrial Production report on Monday but following what we saw in the May Manufacturing PMI data, it should confirm a pickup in manufacturing activity. While we have no position in the homebuilding sector, we’ll continue to chew through the data and what it has to say for the single-family housing market in May. We’ll be looking to see if the downward trend that started earlier this year continued.

Wednesday brings the May Retail Sales report, one that will serve as a barometer for our shares of Costco (COST) and the 8.7% adjusted comp sales it reported for May. Later the same day, the Fed brings its latest policy decision, and based on the inflation picture, our thinking is that the commentary will skew more hawkish compared to the last meeting.

We’ll check that thinking against what we see in the updated Set of Economic Projections. The corresponding presser will be the first under new Fed Chair Kevin Warsh, and it’s fair to say the investment community will be reviewing his comments, word choice, and tone with a microscope to determine how he intends to put his thumbprint on monetary policy.

Here’s a closer look at the economic data coming at us next week:

U.S.

Monday, June 15

Empire State Manufacturing – June (8:30 AM ET)

Industrial Production & Capacity Utilization – May (9:15 AM ET)

NAHB Housing Market Index – June (10:00 AM ET)

Tuesday, June 16

ADP Employment Change Report – Weekly (8:15 AM ET)

Housing Starts & Building Permits – May (8:30 AM ET)

Import/Export Prices – May (8:30 AM ET)

Wednesday, June 17

MBA Mortgage Applications Index – Weekly (7:00 AM ET)

Retail Sales – May (8:30 AM ET)

Pending Home Sales – May (10:00 AM ET)

EIA Crude Oil Inventories – Weekly (10:30 AM ET)

FOMC Policy Decision, Fed Set of Economic Projections (2 PM ET)

Thursday, June 18

Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

Philadelphia Fed Index – June (8:30 AM ET)

EIA Natural Gas Inventories – Weekly (10:30 AM ET)

International

Monday, June 15

Eurozone: Industrial Production – April

Tuesday, June 16

China: Industrial Production, Retail Sales, Fixed Asset Investment – May

Eurozone: ZEW Economic Sentiment Index – June

Eurozone: Wage Growth, Labor Cost Index – Q1 2026

Wednesday, June 17

Japan: Machinery Orders – April

China: Foreign Direct Investment – May

Eurozone: Consumer Price Index – May

Friday, June 19

Japan: Inflation Rate – May

We have a modicum of earnings reports coming our way next week. While none of them will be market-moving, we will be interested in comments from Accenture (ACN) about AI adoption and usage, and what Kroger (KR) has to say about inflationary pressures and how that is affecting its customers.

Here’s a closer look at the earnings reports coming at us next week:

Monday, June 15

Close: Dave & Buster’s (PLAY)

Tuesday, June 16

Close: La-Z-Boy (LZB)

Wednesday, June 17

Open: CarMax (KMX), Jabil (JBL),

Close: Smith & Wesson (SWBI).

Thursday, June 18

Open: Accenture (CAN), Kroger (KR)

Portfolio Investor Resource Guide

Economic Data: Here’s a List of Links to the Key Economic Data We Closely Watch

Investing Terminology: 16 Key Terms Club Members Should Know

10-Ks: Want to Know About a Stock? Read the Company’s Reports

10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

Income Statement: Our Cheat Sheet to Understanding This Financial Document

Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

Valuation Metrics: Everyone Wants a Value. Here’s How Investors Can Find

Thematic Investing 101 Webinar

Like the Benefits of ETFs? Let’s Talk About Models

The Portfolio Ratings System

1 – Buy Now (BN): Stocks that look compelling to buy right now.

2 – Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 – Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 – Sell (S): Positions we intend to exit.