Weekly Roundup: Powell and Inflation Toss Cold Water on the Post-Election Rally

These are the support levels we’re watching for the market entering next week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In last week’s Roundup, we discussed the many moves we made to lock in big gains, which also served to boost the portfolio's cash position. The reason for those actions was the pronounced post-election rally in the market and the even sharper ones in those holdings. We also recognized the market’s technical position and the likelihood this week’s October inflation numbers could lead to more sobering rate-cut comments from Fed Chair Powell and other Fed heads.

The potential for that scenario kept us on the sidelines this week ahead of the October CPI and PPI reports, which confirmed inflation remains sticky, and in the case of core CPI remains quite a distance from the Fed’s 2% inflation target. That combination, as well as other recent economic data, led Powell to say Thursday afternoon that the Fed is in no hurry to cut interest rates, especially with the economy signaling it doesn’t need to rush into action.

Powell's comments, along with Friday’s updated GDPNow model from the Atlanta Fed that still puts current quarter GDP at 2.5% on a rolling basis, weighed on rate-cut expectations for the December FOMC meeting. The yield on the 10-year Treasury rebounded on those developments, closing out the week at its highest level since early July. The same was true with the dollar.

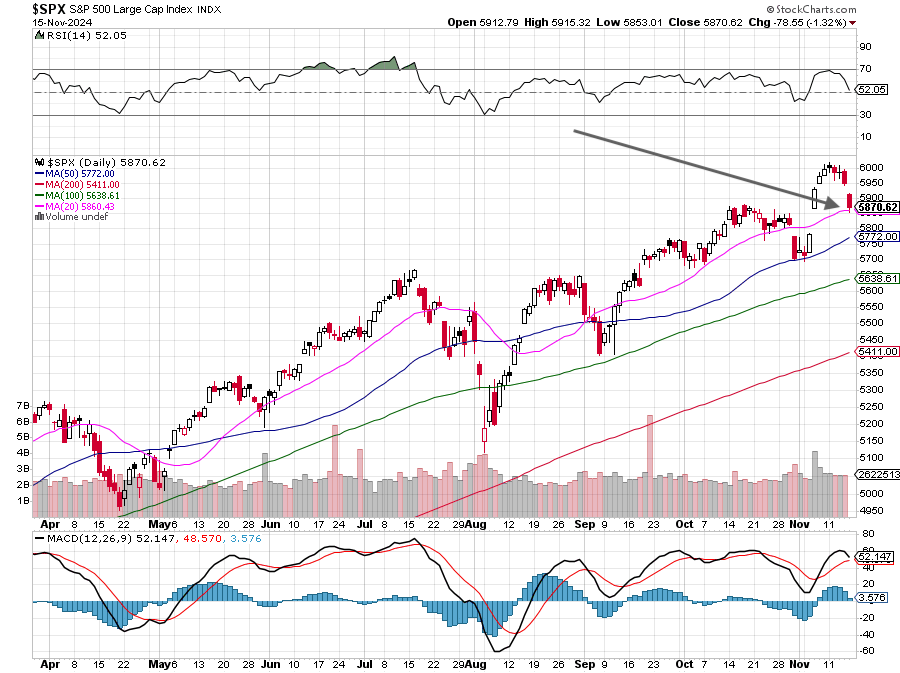

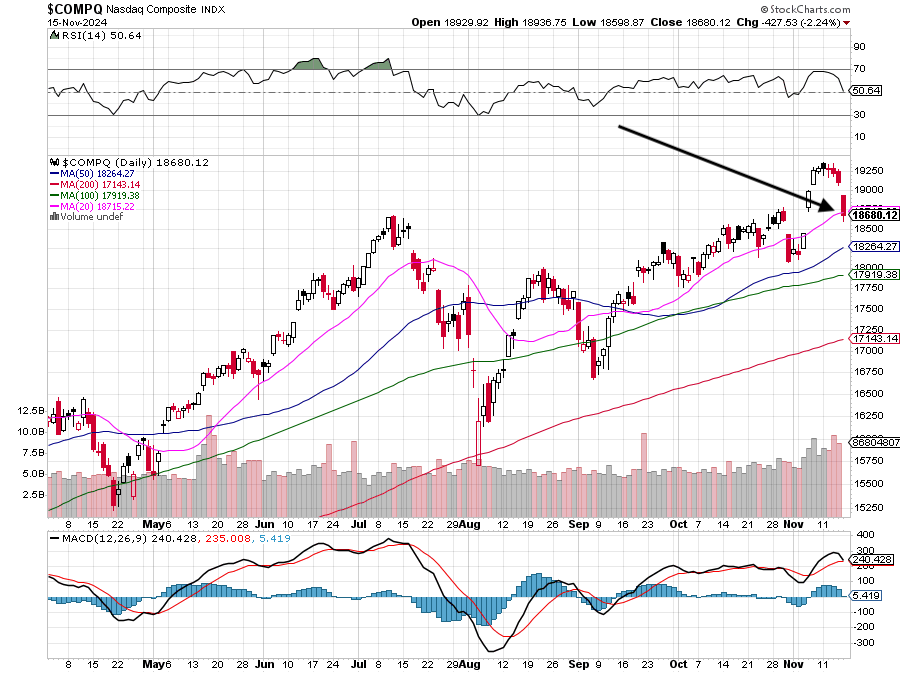

During the week, the relative strength index (RSI) levels for both the S&P 500 and Nasdaq Composite approached overbought levels and the combination of the events described above resulted in the market’s late Thursday and Friday selloff. That erased some, but not all of the post-election move in those two market barometers. As we can see in the chart below, that left the S&P 500 flirting with its 20-day moving average near 5861. The Nasdaq Composite closed below its 20-day moving average at 18,715.

When trading begins next week, we will be watching those major market indexes closely, especially with their technical support levels. While there are gaps evident in both charts, the next level of key support for both is their respective 50-day moving averages. For the S&P 500 that is roughly 1.7% lower from Friday’s close and for the Nasdaq Composite it's more like 2.2%.

That means we will likely start next week off in “wait and see” mode, but as we discuss below there are several holdings on our shopping list we will be keeping close tabs on. We may have opportunities to put some cash to work next week, but we won’t force any action just to say we did something.

Be sure to keep your eyes peeled for our next edition of portfolio signals that will be published on Saturday morning. And for a bit of weekend fun make sure you catch the next edition of Sunday Soup.

Catching Up on the Portfolio This Week

We felt the market's retreat this week in the portfolio, which gave back some of the big moves we saw following the 2024 presidential election. While our cash position and the week-over-week outperformance relative to the S&P 500 in Apple AAPL, Bank of America BAC, Morgan Stanley MS, Dutch Bros BROS, Mastercard MA, and ServiceNow NOW helped temper things, moves lower in our tech and more interest rate-sensitive/construction holdings weighed on the overall portfolio.

We made no trades in the portfolio during the week, which kept us at 26 holdings as we move into the second half of the current quarter. However, we did make a few price target adjustments starting with Thursday’s increase for ServiceNow to $1,100 from $1,000 and resetting Eaton's ETN to $400 from $380. On Friday, we nudged up our Mastercard price target to $540 from $535 and lifted our panic point to $450. Following our review of the October Retail Sales report Friday morning we increased our price target for Costco COST to $975 from $950.

It wasn’t all price target increases, though. On Friday we dialed back our price target for Applied Materials AMAT to $210 from $220, which reflects a more conservative near-term ramp in semi-cap spending. As various chip reshoring programs award funding, the longer-term outlook for semi-cap equipment remains bright.

We are watching the technical levels for the market as we contemplate the next steps for our shopping list of stocks. Thursday we shared our thinking on Universal Display OLED and in our Friday comments for Costco and Applied Materials we outlined levels that would make for attractive pickup points. We’ll also be revisiting Qualcomm QCOM following favorable smartphone guidance from Skyworks Solutions SWKS this week and Qualcomm’s 2024 Investor Day on November 19.

Over the weekend, we’ll revisit such points for all our holdings and share them along with an updated table of consensus EPS forecasts on Monday.

Now let's turn to comments made across Wall Street concerning our holdings:

We weren’t the only ones to dial back our price target for Applied Materials. Raymond James cut its target to $225 from $245 as did Needham. Wells Fargo and Mizuho trimmed their targets to $220 from $235 and $235, respectively.

MoffettNathanson had an interesting take on Alphabet GOOGL and Meta Platforms META this week, sharing its view that both stocks are undervalued after stripping out Meta’s Reality Labs unit and Alphabet’s "other bets" business. While both of those businesses are generating meaningful operating losses for their parents and are a drag on Meta’s and Alphabet’s bottom lines, we have to assess the entire company when valuing it, not just the money-making parts.

Dutch Bros caught a price target increase from Stifel to $53 from $42. This follows our target boost to $50 from $39. Our decision to lock in a slice of gains amid a short squeeze in BROS shares looks like a smart one given where the shares closed this week.

In addition to our price target boost, BofA Global Research lifted its Eaton price target to $410 from $350 this week. UBS made a more aggressive move, resetting its target at $431 from $330.

As we alluded to in our Mastercard note this week, those shares saw several price target changes this week following its investor day. TD Cowen boosted its target to $567 from $533, Mizuho went to $570 from $532, and Piper Sandler refreshed its target to $575 from $565. The biggest increase we saw was the one at UBS, which set a $610 target. When we adjusted our MA price target this week, we explained how many of those targets equate to paying more for a slower rate of earnings growth ahead. That realization was a factor in our more moderate adjustment.

Wells Fargo made a sizable move with its Morgan Stanley price target, pushing it to $142 from $107. That move reflects the improving outlook for M&A deals under the incoming Trump administration. We see a better IPO market in 2025 spurring investment banking activity and fees higher year over year. However, rather than be head faked, we’ll revisit our MS target as the activity for both starts to perk up. The same goes for Bank of America shares in the portfolio.

Morgan Stanley upped its price target on Nvidia NVDA to $160 from $150, while Piper Sandler named the shares as its top large-cap pick as it raised its target to $175 from $150. There were multiple positive data points for Nvidia as well as Marvell Technology MRVL this week, including Taiwan Semi’s TSM October revenue report, Foxconn’s bullish AI server outlook, and Cisco’s CSCO comments that confirmed we are still in the early innings of AI adoption. Loop Capital initiated coverage of MRVL shares with a $95 target. We’ll get much more on AI next week when Nvidia and Elastic ESTC report earnings.

we were joined this week in our price target increase for ServiceNow by Wells Fargo which raised its target for NOW to $1,150 from $1,050.

Lastley, UBS made an eye-popping adjustment to its United Rentals URI target, moving it to $910 from $665.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, November 11: Our Roadmap for This Inflation Data Week

Wednesday, November 13: Thematic Investing 101 Webinar

Thursday, November 14: Foxconn Forecast Is Big for Nvidia and This Other Holding

Friday, November 15: How the Latest Retail Sales Data Supports This Holding

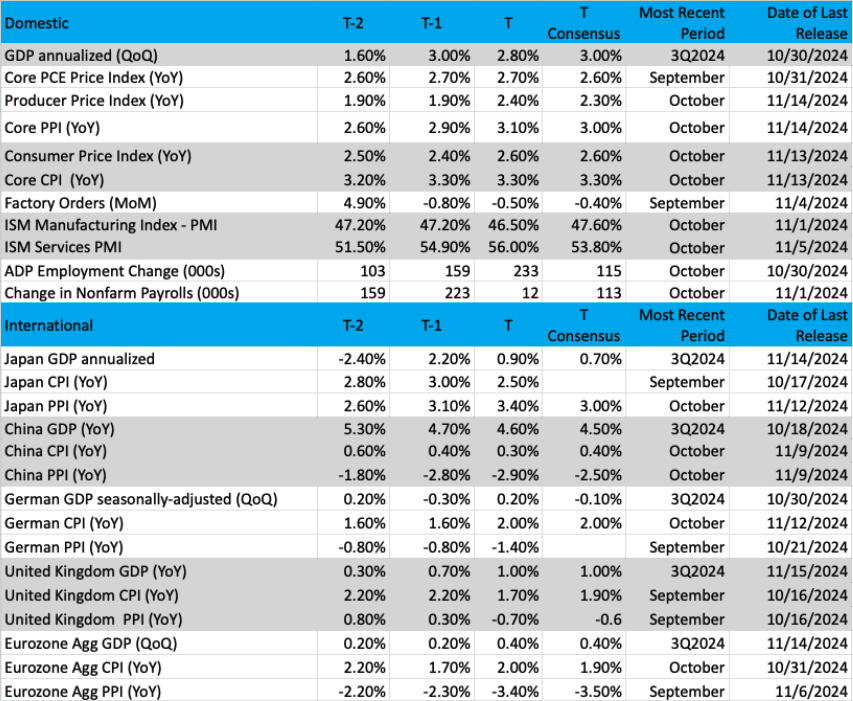

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

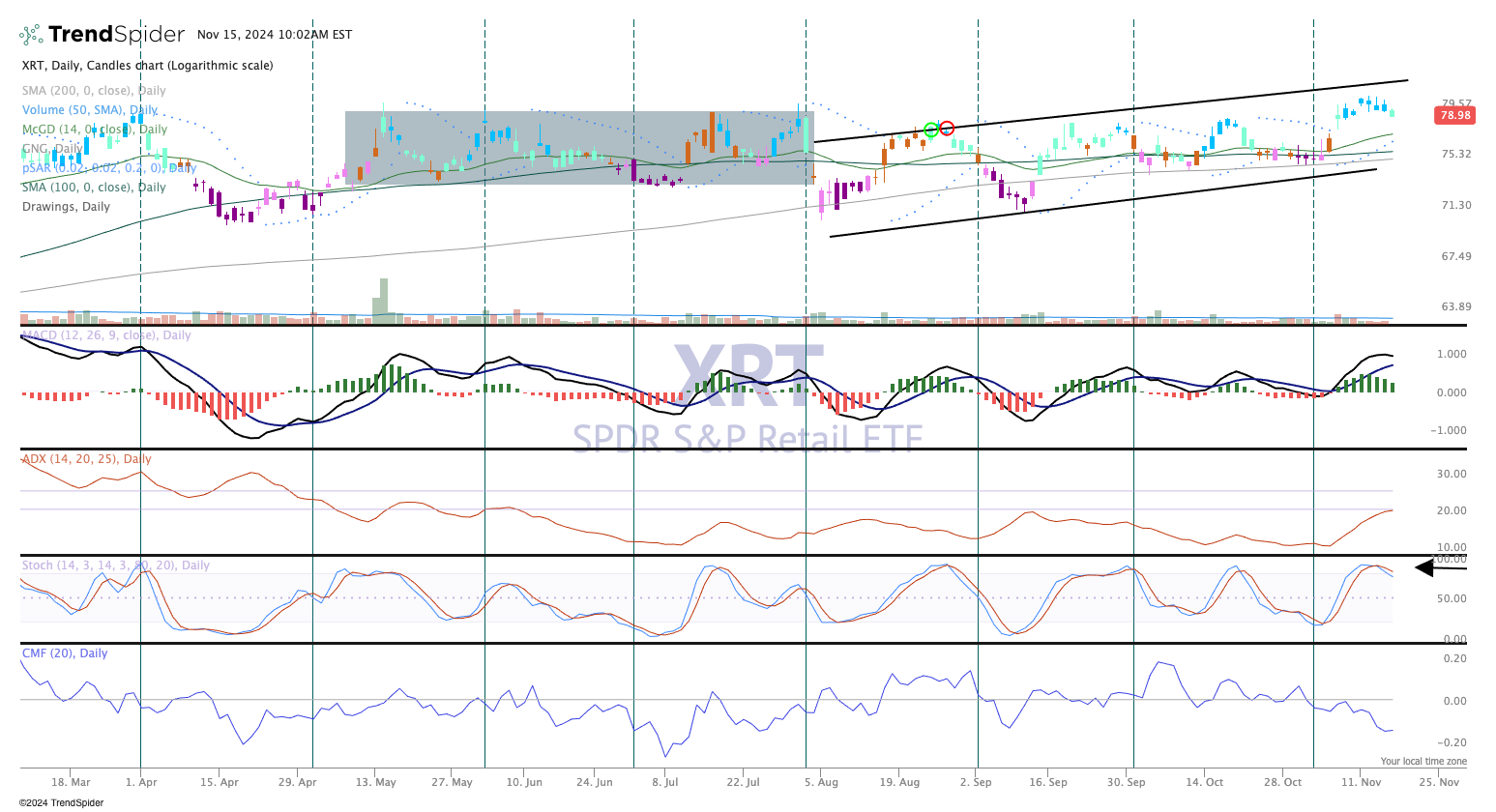

Chart of the Week: SPDR S&P Retail ETF (XRT)

Don’t look now, but a slew of retail earnings will be coming in the next couple of weeks. In addition, the holiday shopping season will commence, with the unofficial start on the day after Thanksgiving or "Black Friday." It is called that because that was the day retailers would be "in the black" for the year, the idea that sales were so big that would put them over the top.

This past week, though, we heard from a few big-box retailers such as Home Depot (HD). They flagged, yet again, some caution with consumer spending, but showed some optimism in their forecast for the next twelve months. Again, not a surprise. But next week we hear from the likes of Walmart (WMT), Target (TGT), Williams-Sonoma (WSM), and others. Some stocks have done well recently, with their charts reflecting the optimism of a positive holiday season.

The XRT, a chart we like to examine from time to time, is the SPDR S&P Retail ETF, which contains some names that are in or related to those in the Pro Portfolio. Amazon AMZN is a big name but a small holding in this ETF. By contrast, Amazon is much larger percentage of the VanEck Retail ETF RTH and thus has a much bigger influence on that ETF. We like to compare these two, but the XRT gives us a much more conclusive view of how the entire group is faring.

Retail stocks have been strong the past few months, which is notable in the chart of the XRT. After some sideways action in late spring (box) we now have a nice series of higher highs and higher lows in place. In fact, the recent action (past week) has the XRT just barely eclipsing the double-top highs in May and July, not an easy feat. Momentum is still strong though pulling back some; Moving Average Convergence Divergence (MACD) is still on a buy signal here.

The price chart is bullish and looks constructive, though we could see a pullback to the shorter-term 20-day moving average coming into play, which would be to the $77 area, just a couple of dollars lower from here. If that holds firm there is a good chance for the XRT to make another leg higher, certainly helped by a positive response to earnings.

Other charts we shared with you this week were:

Monday, November 11: S&P 500 - It's Hard to Argue With This Strength

Monday, November 11: Applied Materials (AMAT) - Applied Materials Looks Shaky Before Earnings

Tuesday, November 12: Bank of America (BAC) - This Holding's Chart Says Better Times Are Ahead

Wednesday, November 13: Universal Display (OLED) - This Tech Position Is Showing Better Entry Points

Thursday, November 14: Apple (AAPL) - Apple Is Starting to Sweeten

The Week Ahead

As we move into the second half of November, next week brings us the latest housing data in the form of October Housing Starts and Existing Home Sales. While it won’t be captured in those reports, Redfin’s (RDFN) Homebuyer Demand Index, a measure of tours and other buying services from Redfin agents, jumped more than 15% this past weekend to its highest level in nearly a year and a half. Other data from Redfin and Ipsos found that nearly a quarter of soon-to-be first-time homebuyers were waiting until after the election before buying a home.

With that in mind, we’ll look forward to the November Purchase Index details from the Mortgage Bankers Association in the coming weeks to gauge the accuracy of those survey findings. Should we see a pick-up in activity that would be a positive sign for the housing market and a few of our holdings.

Following Fed Chair Powell’s comments Thursday, another piece of data we’ll be interested in digging into next week will be the November Flash PMI data from S&P Global. The Flash PMI data will bring the first hard look at the manufacturing and service sectors in November, including new orders, hiring, and inflation findings. Falling new orders for the manufacturing sector in October suggest we’re likely to see that part of the economy remaining sluggish in November, with the overall economy continuing to be carried by the Services sector. New order activity for that part of the economy continued to rise in October per S&P Global’s findings, which suggests it continued to hum in November.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, November 18

· NAHB Housing Market Index – November (10:00 AM ET)

Tuesday, November 19

· Housing Starts & Building Permits – October (8:30 AM ET)

Wednesday, November 20

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, November 21

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Existing Home Sales – October (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, November 22

· S&P Global Flash Manufacturing & Services PMI – November (9:45 AM ET)

· University of Michigan Consumer Sentiment Index (Final)- November (10:00 AM ET)

International

Monday, November 18

· China: Foreign Direct Investment - October

Tuesday, November 19

· Eurozone: Inflation Rate (Final) - October

Wednesday, November 20

· Germany: Producer Price Index – October

· UK: Inflation Rate - October

Thursday, November 21

· Eurozone: New Car Registrations - October

Friday, November 22

· Japan: Inflation Rate – October

· Japan: Jibun Bank Flash Manufacturing & Services PMI – November

· Eurozone: HCOB Flash Manufacturing & Services PMI – November

· UK: S&P Global Flash Manufacturing & Services PMI - November

While two of our tech holdings, Nvidia and Elastic, report quarterly earnings next week and Qualcomm will hold its investor day, the bulk of next week’s earnings reports will be retail-facing. Friday’s October Retail Sales report contains trailing three-month line-item data that will serve as a yardstick for those reports, but we will be more focused on how they see the all-important holiday shopping season shaping up. That includes their thoughts on overall consumer spending as well as pockets of spending strength. As we tally their results and guidance, we’ll be thinking about what it says about Mastercard’s December-quarter revenue prospects.

One other thing that we’ll be paying close attention to given our comments in Friday’s video about the dollar and PepsiCo PEP is what multinational companies like Deere (DE) are saying about currency headwinds in their guidance.

Here's a closer look at the earnings reports coming at us next week:

Tuesday, November 19

· Open: Lowe’s (LOW), Medtronic (MDT), Walmart (WMT)

· Close: Dolby Labs (DLB),

Wednesday, November 20

· Open: Dycom (DY), Target (TGT), TJX (TJX)

· Close: Jack in the Box (JACK), Nvidia (NVDA), Palo Alto Networks (PANW)

Thursday, November 21

· Open: Baidu (BIDU), BJ’s Wholesale (BJ), Deere (DE)

· Close: Elastic (ESTC), Gap (GPS), Ross Stores (ROST)

Friday, November 22

· Open: Buckle (BKE).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.