Wall Street Keeps Saying ‘1999’—But the Market’s Internals Tell a Different Story

Three strategists see a blow-off setup, but tops form slowly. Breadth isn’t expanding, the Dow is bleeding, and key sectors aren’t confirming.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I was struck by something quite curious on Monday. Not one, not two, but three different strategist types discussed how similar today’s market feels to 1999.

One said he thought we should expect a little choppiness, but in the end, it would be okay because earnings are rising. Another said he saw some issues—he highlighted the banks and industrials, where have you heard that before???!—and that they were worth monitoring, but overall he was still bullish. And the last person raised his S&P target on Monday, noting that often interest rates and stocks rise into a blow off as we had in 1999, and heck, he even cited Tokyo in 1989 too.

So I suppose all three believe they will be able to spot the exact top of the blowoff, or at least close to it. To that, I say, I applaud you. Blow off bottoms are easier to spot than blow off tops because blow off bottoms tend to be panicky, and we’ve seen plenty of them in our careers. But a blow off top? I don’t think they are as easy to spot, and they tend to show up more specifically and not in the market overall.

Notice the third fellow only had two citations for a blow off: the US in 1999 and Japan in 1989. Sure, we’ve seen a blow off in gold. We saw one in silver too. We saw one in SPACs five years ago. But those are specific, not general.

Let me quote from a Special Report titled The Philosophy of Tops, written by my mentor, Justin Mamis, in July of 1987, a month before the peak of the market and two months before the Crash of 87:

Tops are not made in a day. Unlike bottoms, which often can abruptly materialize on a climactic panic, with many stocks making their lows at the same time, tops form over a much longer period of time.

He finishes the report with this line:

The one eternal aspect of every market top is that it occurs before we’re ready for it.

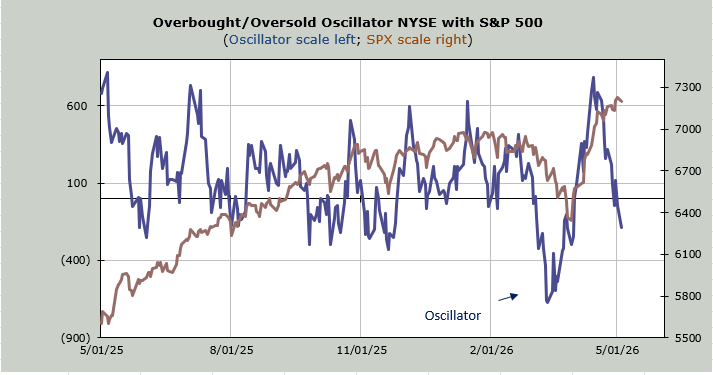

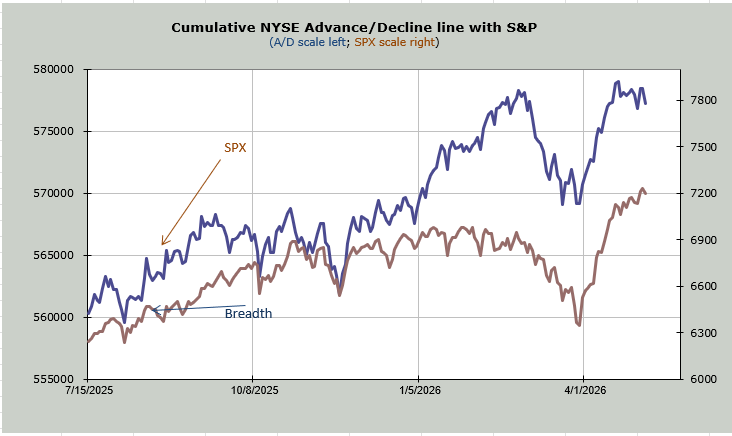

I do not know if this upcoming intermediate term overbought condition will mark the top. I will only know in hindsight. What I do know is that the number of stocks making new highs is not expanding and hasn’t been. I know that the Dow has been red for seven of the last eight trading days. I know that there are several Dow stocks on the new low list or pretty close to getting there. I know that breadth, while not screamingly divergent, is certainly acting differently than the S&P these last two weeks, which is a change from the last year.

I also know the Banks and Industrials continue to sag. I know the Transports have collapsed, giving back almost the entire run they had. And I know on Monday the chatter about the bonds picked up, as I assumed it would. I won’t rehash my view on bonds (discussed in full here yesterday), but I will note that the Daily Sentiment Index (DSI) is down to 21. So it won’t take much to get that reading to the teens.

In the meantime, you can also see the narrowness of the rally in the Oscillator charts. Oscillators that are based on breadth don’t plunge like that if breadth is good.