Weekly Roundup: A Big Week for the Market, But Caution Lights Are Flashing

Even as TheStreet Pro Portfolio benefits and outperforms, market gains have key indicators flirting with overbought levels.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

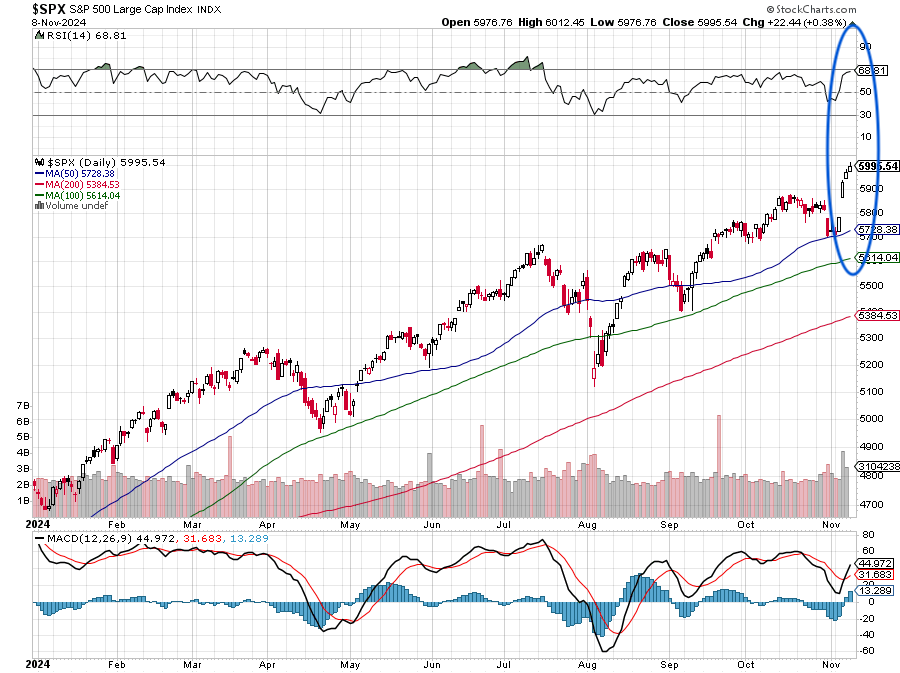

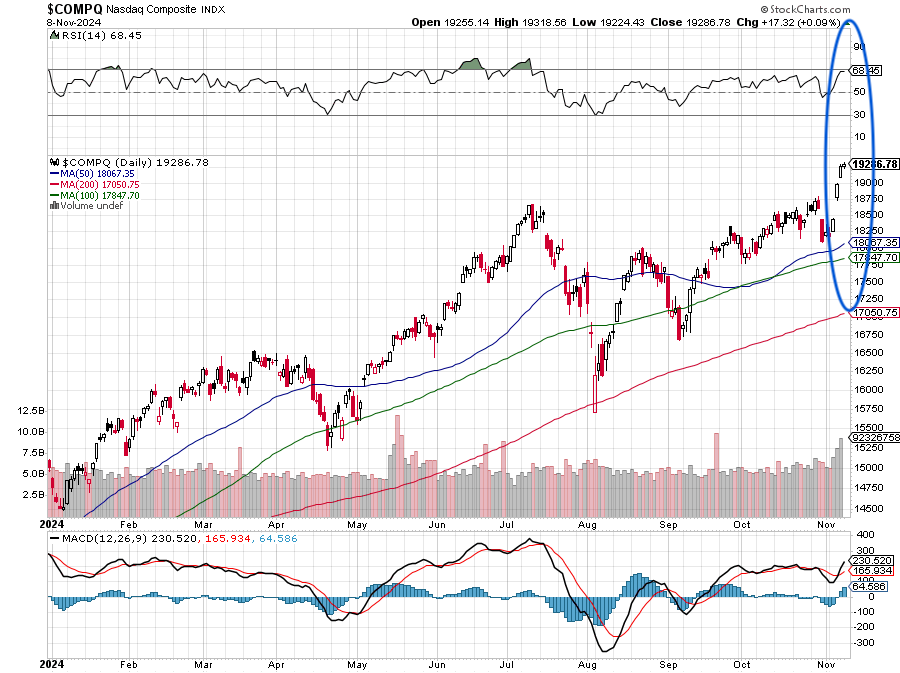

The stock market had a very enthusiastic response to the outcome of the 2024 presidential election and the Fed delivered another 25-basis point rate cut on Thursday. That combination led to significant moves higher across all the major market indexes, with the S&P 500 gaining 4.7%, and the Nasdaq Composite 5.7%. However, the big winner was small-cap stocks with a more than 8.6% rise in the Russell 2000.

Meanwhile, TheStreet Pro Portfolio benefited from the market’s move and post-earnings short squeezes, which catapulted shares of Dutch Bros BROS higher, and led us to lock in a 144% gain on our remaining position in Axon Enterprise AXON. This all resulted in the portfolio extending its year-to-date lead on the S&P 500.

As we explained in Friday’s video, while we are pleased the strategies we employ and the moves that we’ve made over preceding quarters are playing out, we recognize the road ahead remains long. We also know from experience the market is an evolving one, which means we need to remain vigilant.

With that in mind, while we enjoyed the market’s move this week, as you can see in the charts below, the net effect has the relative strength indexes for the S&P 500 and the Nasdaq Composite bumping up against overbought levels — not surprising given the sharp moves both market indicators put in this week. You’ll also notice the pronounced gaps in both charts, and as we know, typically, over time, gaps tend to get filled.

We’re exiting this week with higher cash levels, and if the market moves deeper into overbought territory, as prudent investors we may want to raise some additional cash. When it comes to putting that cash to work, some patience may be warranted as we look for suitable candidates that meet our investment criteria — well-positioned companies growing their earnings faster than the S&P 500 and with a favorable risk-to-reward entry point in their shares.

Catching Up on the Portfolio This Week

As we discussed in Friday’s video, the portfolio turned in a very nice week, building on October's outperformance. While we benefited handsomely from the 24% move in Axon Enterprise AXON this week when we closed the position, other outsized movers included Dutch Bros BROS and its 40% jump, as well as double-digit gains with Morgan Stanley MS, Eaton ETN, and Marvell MRVL. Even shares of Builders FirstSource BLDR and The Trade Desk TTD, which gave back some of their early-in-the-week gains, still finished in the green. The only real laggards for the week were PepsiCo PEP, Universal Display OLED, and Apple AAPL.

We made several moves with the portfolio, which began with picking up more shares of Builder FirstSource, Lockheed Martin LMT, and Waste Management WM on Wednesday. Following the market’s post-election pop, we took advantage of the notable move in Bank of America, Marvell, and Morgan Stanley, and performed some prudent portfolio management while locking in big gains for the portfolio. As we booked those gains, we scooped up some additional shares of Meta META following the news it will allow its AI models to be used by government agencies and national security applications.

Later that day, we recognized the short squeeze that was popping shares of Dutch Bros, which opened a window to book some very large profits as we boosted our price target to $50 and downgraded the shares to a Two rating. On Friday, we took advantage of another short squeeze, this time in Axon shares, which led us to close out the position with a 144% gain on that last slug of shares given our $193.56 cost basis.

While we didn’t top-tick the shares on Friday, the return we booked isn’t anything to sneeze at. We continue to like Axon’s expanding role in public safety and the favorable margin shift underway, but it would have been irresponsible of us not to take advantage of Friday’s explosive move. To keep tabs on the shares and to see if a favorable risk-to-reward re-entry point emerges, we placed AXON in the Bullpen.

With the S&P 500’s RSI quickly approaching overbought levels near 70 and the Nasdaq Composite there as well, we will proceed carefully as the September-quarter earnings season continues and we digest the coming October data that could influence the Fed’s next policy decision coming on December 18. When we return on Monday, we will share an updated portfolio table containing the latest consensus EPS expectations for our holdings, and any panic point adjustments we need to make following what we saw this week.

Now let’s turn to what Wall Street had to say about our portfolio holdings this week:

Loop Capital raised its Alphabet GOOGL price target to $185 from $170 and also upsized its target on Meta to $655 from $575.

Citi upgraded its rating on Bank of America to Buy from Neutral and boosted its price target to $54 from $46.

TD Cowen increased its Dutch Bros price target to $53 from $47, while BofA reset its target at $51 from $49.

Bernstein initiated coverage on Eaton shares with an Outperform rating and a $382 target.

Macquarie and Piper Sandler lifted their The Trade Desk price targets to $133 and $140 from $130 and $110, respectively, while Susquehanna and UBS upped theirs to $150.

Shares of Vulcan Materials VMC received a new Buy rating from UBS with a $349 price target. UBS joins our thinking that Vulcan should benefit from an improving non-residential construction market in the second half of 2025 and 2026.

Oppenheimer increased its target on Waste Management shares to $231.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, November 4: Our Road Map for This Election and Fed-Filled Week

Tuesday, November 5: Palantir’s Comments Bring Support for These Holdings

Wednesday, November 6: Trump-Driven Change at FTC Can Boost This Big Tech Holding

Thursday, November 7: Powell's Policy Admission Keeps Us Bullish on These Holdings

Friday, November 8: Let's Discuss the Portfolio's Recent Trades and the Road Ahead

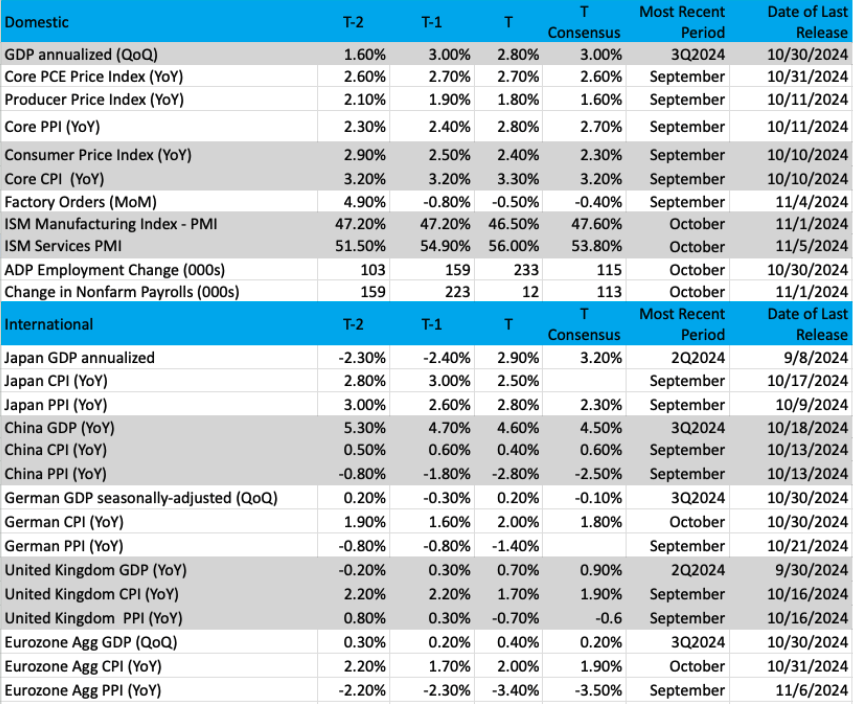

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

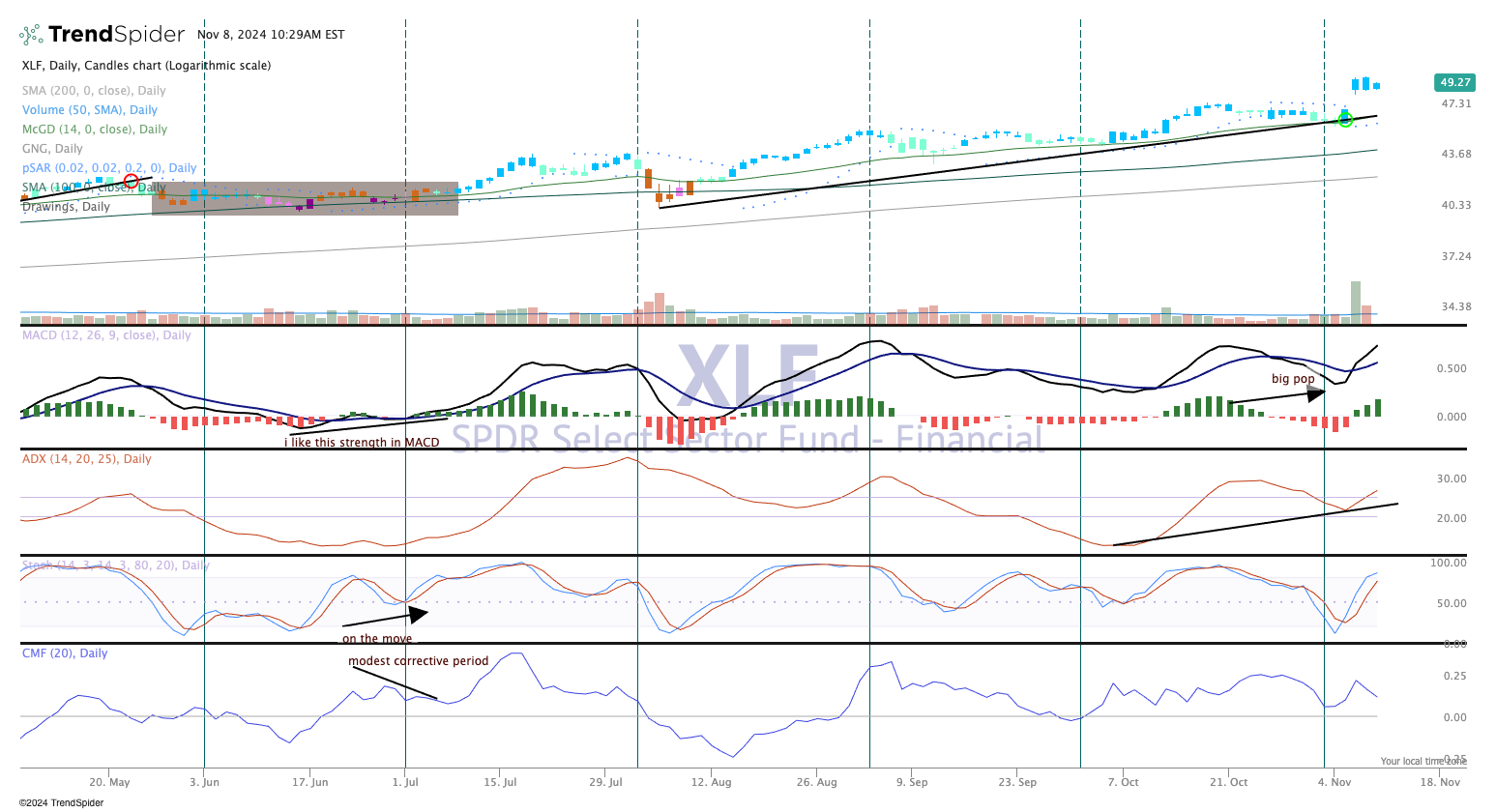

Chart of the Week: Financial Select Sector SPDR Fund (XLF)

Now that the election is behind us and a new administration will be in place in a couple of months, it is time to figure out who the winners will be over the next four years. That is a tough task, of course, with so many variables out there that may derail a particular thesis. But there are very strong groups that performed well over the last four years and may thrive even more over the next period.

One group that has our focus is financials, banks, and brokerages. This sector responded well after the pandemic started, and while the group initially fell sharply there was plenty of time for the banks to shine. Just recently, names like JPMorgan Chase JPM, Goldman Sachs (GS), and Morgan Stanley MS hit all-time highs on strong volume. That is very telling, as big institutions are actively buying these names.

But was it just the election results that suddenly made the banks look attractive? Not at all, but frankly once the election was behind us money started flowing, looking for the best areas to get a nice return. Banks have always been the reliable and steady place for that.

Today we’ll look at the Financial Select Sector SPDR Fund XLF for some clues about future direction. The chart looks very strong. The last few days were spectacular with strong turnover. The Moving Average Convergence Divergence (MACD) crossed for a bullish signal and the ADX (pane 3) is moving higher — this indicator is bullish. Stochastics (pane 4) shows good, solid momentum building in the financials.

TheStreet Pro Portfolio holds Bank of America BAC and Morgan Stanley, high-quality issues that should thrive with the other big banks. In the coming new year, we see good things happening.

Other charts we shared with you this week were:

Monday, November 4: S&P 500 – Are You Ready?

Monday, November 4: Qualcomm QCOM – Qualcomm Tests Support Again

Tuesday, November 5: Marvell MRVL - This Tech Position Just Continues to Flex Its Muscles

Wednesday, November 6: Dutch Bros BROS – Dutch Bros is Ready to Heat Up

Thursday, November 7: The Trade Desk TTD - A Tech Position Trends Higher Ahead of Earnings

The Week Ahead

Coming off such a jam-packed week like we just had, we will be back next week to the usual mix of economic data and earnings reports that we see this time of year. Now that we’ve passed the Fed’s November policy meeting, we’ll see a return of Fed speakers in the mix. As of now, there are a dozen such appearances sceduled next week, including one by Fed Chair Powell on the afternoon of Thursday, November 14.

What’s interesting about that timing is it falls after Wednesday’s October CPI report and Thursday’s October PPI. During Powell’s policy press conference this week, he noted some stickiness in the core PCE price index data, which remained unchanged at 2.7% in July, August, and September. In Thursday’s video we discussed that Powell’s press conference comment that the Fed has yet to figure out its path to a neutral policy level and why that means we and the Fed will be tracking data had before the Fed’s December policy meeting closely. Because Powell’s appearance follows the October CPI data, we’ll be interested in any comments from the Fed chair or other Fed speakers that follow that report.

Friday brings the October Retail Sales report, which could be a messy one to interpret given Hurricanes Helene and Milton as well as Amazon’s AMZN Prime Big Deal Days event and competing events from other retailers. As we read that report, we’ll be tracking non-store retail sales to gauge this quarter’s guidance Amazon shared for its North American retail business that included “a strong Prime Big Deals Days.” The Retail Sales report will also bring some context for Costco’s COST October sales report, which revealed U.S. adjusted comp sales growth of 5.8% and e-commerce sales that rose 19.3%.

Also out on Friday is the October Industrial Production report, which will bring another perspective on the domestic manufacturing economy. Once all of the week’s data are published, we’ll be eyeing the next update of the Atlanta Fed’s GDPNow model for where that rolling forecast pegs the current quarter’s economic growth. Exiting this week, that figure stood at 2.5%.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, November 11

· Bond market closed for the Veteran’s Day holiday

Tuesday, November 12

· NFIB Business Optimism Index – October (7:00 AM ET)

· Treasury Budget – October (2 PM ET)

Wednesday, November 13

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Consumer Price Index – October (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, November 14

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Producer Price Index – October (8:30 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, November 15

· Retail Sales – October (8:30 AM ET)

· Import/Export Prices – October (8:30 AM ET)

· Industrial Production & Capacity Utilization – October (9:15 AM ET)

· Business Inventories – September (10:00 AM ET)

International

Monday, November 11

· Japan: Eco Watchers Survey - October

Tuesday, November 12

· Germany: Inflation Rate – October

· Eurozone: ZEW Economic Sentiment - November

Wednesday, November 13

· Japan: Producer Price Index, Machine Tool Orders – October

· Eurozone: Industrial Production - September

Thursday, November 14

· UK: GDP – 3Q 2024

· UK: GDP, Industrial Production – September· Eurozone – GDP (2nd estimate) – 3Q 2024

Friday, November 15

· China: Retail Sales, Industrial Production - October

Following two heavy weeks of corporate earnings, including just over half of the portfolio’s holdings, things settle down rather nicely. The only portfolio holding reporting next week is Applied Materials AMAT, but we will continue to mine other reports, such as Beazer Homes (BZH), CyberArk (CYBR), Cisco (CSCO), and Skyworks (SWKS) for fresh insights.

Here's a closer look at the earnings reports coming at us next week:

Monday, November 11

· Open: Monday.com (MNDY)

Tuesday, November 12

· Open: AstraZeneca (AZN), Home Depot (HD), IAC Inc. (IAC), Mosaic (MOS), Surgery Partners (SGRY), TreeHouse Foods (THS), Tyson Foods (TSN)

· Close: American Healthcare REIT (AHR), Rackspace Technology (RXT), Skyworks (SWKS)

Wednesday, November 13

· Open: CyberArk (CYBR)

· Close: Beazer Homes (BZH), Cisco (CSCO),

Thursday, November 14

· Open: Walt Disney (DIS)

· Close: Applied Materials (AMAT)

Friday, November 15

· Open: Alibaba (BABA), Buckle (BKE), Foot Locker (FL).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.