Port Deal and Robust Jobs Report Lift the Market and Portfolio

Growing support for a 'no-landing' economic scenario will raise questions over Fed rate-cut prospects.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market received positive news for the economy Friday, with a tentative deal ending the port strike that started on Tuesday and the September Employment Report handily trouncing market expectations. While we are enjoying the rebound effect that it is having on stocks closing out the week because two concerns have been removed, we have to also consider it will keep the market’s valuation stretched on multiple fronts. Meanwhile, tension associated with the Israel-Iran conflict remains elevated following further attacks and the 2024 U.S. presidential race remains tight.

We will remain disciplined investors, letting Friday’s market move wash over our holdings but noting which positions are extended and potentially ripe for some profit-taking early next week.

September Jobs Report and the Tentative Port Deal

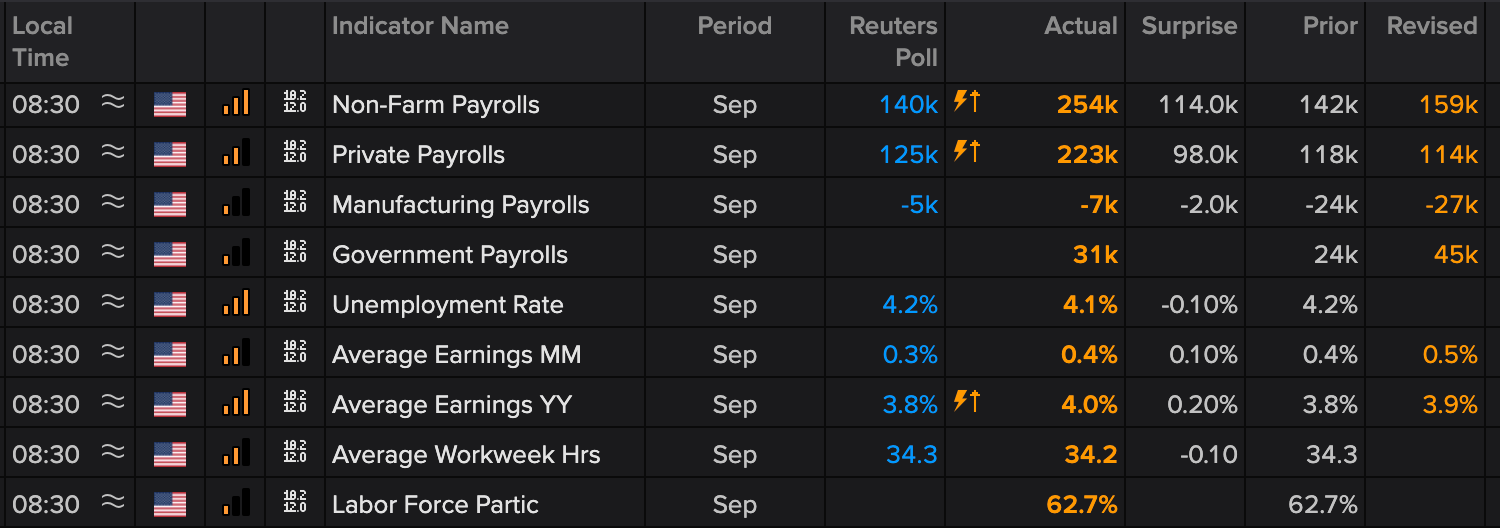

On Thursday, we discussed the potential for an upside surprise in the Employment Report but the 254,000 non-farm jobs added during the month were far stronger than we expected and significantly higher than the market forecast of 140,000 jobs. Adding to that upside surprise, revisions for July and August show 72,000 more jobs than previously estimated, and average hourly earnings in September rose 4.0% year over year, a tad higher than in recent months.

The port deal, which should keep goods flowing through at least early January, should keep the economy humming, remove near-term inflation worries, and leave only a modest disruption risk for the holiday shopping season.

Both of these remove layers of concern that have been weighing on the market.

Support for No-Landing Narrative Grows

Combining Thursday’s stronger-than-expected September ISM Services PMI with the data found in the September Employment Report supports something closer to a no-landing scenario for the economy than a soft landing and should be giving folks fearing a hard landing some comfort. When the Atlanta Fed GDPNow model is updated next Tuesday, October 8, we should see a very nice upward revision from its recent downgrade to 2.5% for the current quarter.

When it comes to more people working and their earnings growing, we view that as a positive for the economy and consumer spending as well as our positions in Amazon AMZN and Costco COST. It also means that we may need to revisit our current price target on shares of Mastercard MA.

Rate-Cut Expectations Will Be Dialed Back, but That’s OK

The jobs numbers and the spike in the September ISM Services PMI price sub-index supports our thinking the market will need to re-adjust its Fed rate-cut expectations for the balance of this year — to two cuts or maybe even one from the three 25-basis points found in the CME FedWatch Tool. There are two Fed speakers Friday and another slew of them ahead of next week’s September CPI and PPI data and once again the market is likely to hang on their words.

The good news is the economy continues to perform well even though monetary policy is still relatively tight. The next indicators to watch for the pace of Fed rate cuts will be next week’s September CPI and PPI data. Based on the September ISM, we may not see as much improvement in that data as some expect. That could be another factor in the market having to center its thoughts between one and two rate cuts between now and year-end.

Should that come to pass, it could pressure some of our more interest rate-sensitive positions, such as Builders FirstSource BLDR and United Rentals URI, which were strong performers for us in Q3 2024. We’ll keep a close eye on those shares and depending on the degree of any price retrenchment, we’ll share potential entry points for new members.

We would note that both those stocks as well as Waste Management WM and Vulcan Materials VMC may see some near-term disruption given the fallout of Hurricane Helene but all four stand to benefit from the eventual rebuilding. Knowing that we’ll continue to favor a longer-term view of those stocks.

More from TheStreet Pro

- Weekly Roundup: Bucking Trend, September Is Lifting the Portfolio Higher

- Is the Recent Rise in Gold a Trap?

- The Global Economy Is a Stephen King Movie

At the time of publication, TheStreet Pro Portfolio was long AMZN, COST, MA, BLDR, URI, VMC and WM.