Is the Recent Rise in Gold a Trap?

Wealth advisors (and regular investors) should include precious metals in their portfolios. Read on to learn why. Plus what’s going on with gold and silver and whether pullbacks are buying opportunities.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It’s easy for a fundamental analyst to despise gold.

My money manager friends can't stand die-hard gold bugs. These fundamentally-driven managers say, ‘I don’t invest in gold because it doesn’t generate cash flows, the price swings are too volatile, and it’s not a great inflation hedge.’

I usually agree with the gold-dodgers. I’ve always preferred to focus capital on stocks and real estate, which have the potential for better returns than precious metals. The drawbacks of storage costs and limited industrial use make me hesitate. To top it off, central banks tend to distort the supply and demand.

But I can't ignore history. When conditions are right, investors are well-served by owning precious metals.

When I first got into the investment business, my mentor taught me about gold market price cycles. I started accumulating precious metals during the COVID sell-off and the Biden/Trump election because gold often surges during times of currency issues, political unrest, and high inflation – even stagflation.

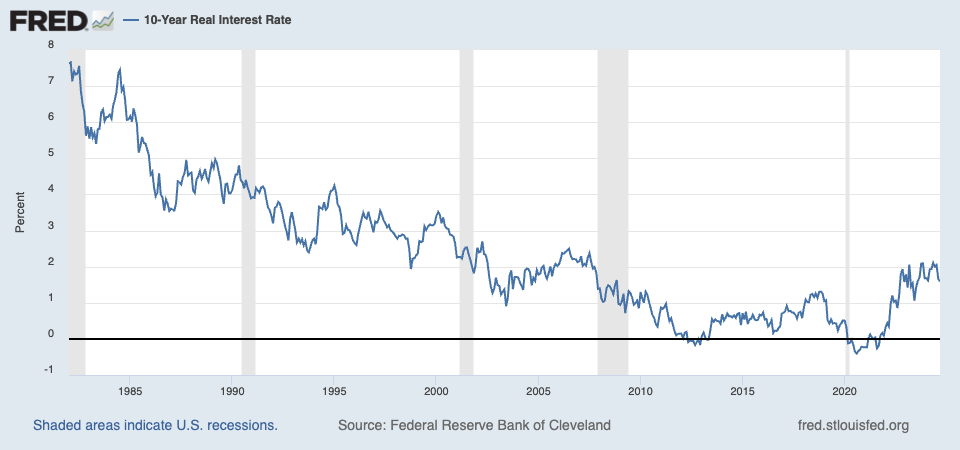

Low real rates are a buy signal for gold and silver

The 10-year real interest rate has a negative correlation with gold prices. This chart gives a forward-looking view of the inflation-adjusted 10-year Treasury yield by combining the nominal 10-year Treasury Constant Maturity Rate with the 10-year breakeven inflation rate to calculate the real rate. Since both the nominal rate and expected inflation cover the same time frame, this is a more accurate measure of the real interest rate. It’s a key indicator for timing investments in precious metals.

Real interest rates hovered around 7.62% in 1982, but as of September, they're just 1.58%—historically low! When central banks are too loose with monetary policy, gold can significantly outperform stocks.

Is worrying about political risks a waste of time?

Predicting political risks is tough, but gold is a great hedge against them. Plus, if you can lower portfolio volatility without sacrificing returns, shouldn't you?

Risks I’ve heard include:

- Domestic terrorism in the U.S. could rise with politically motivated violence.

- Middle East and Russia/Ukraine conflicts could escalate.

- Unregulated AI could destroy jobs and lengthen unemployment lines.

- Massive federal deficits will be unbearable without drastic tax changes or more money printing.

- More violent protests resulting from a widening income gap.

- Democracy is at risk, according to both political parties.

Political risks are higher than usual right now. That alone justifies an allocation to precious metals.

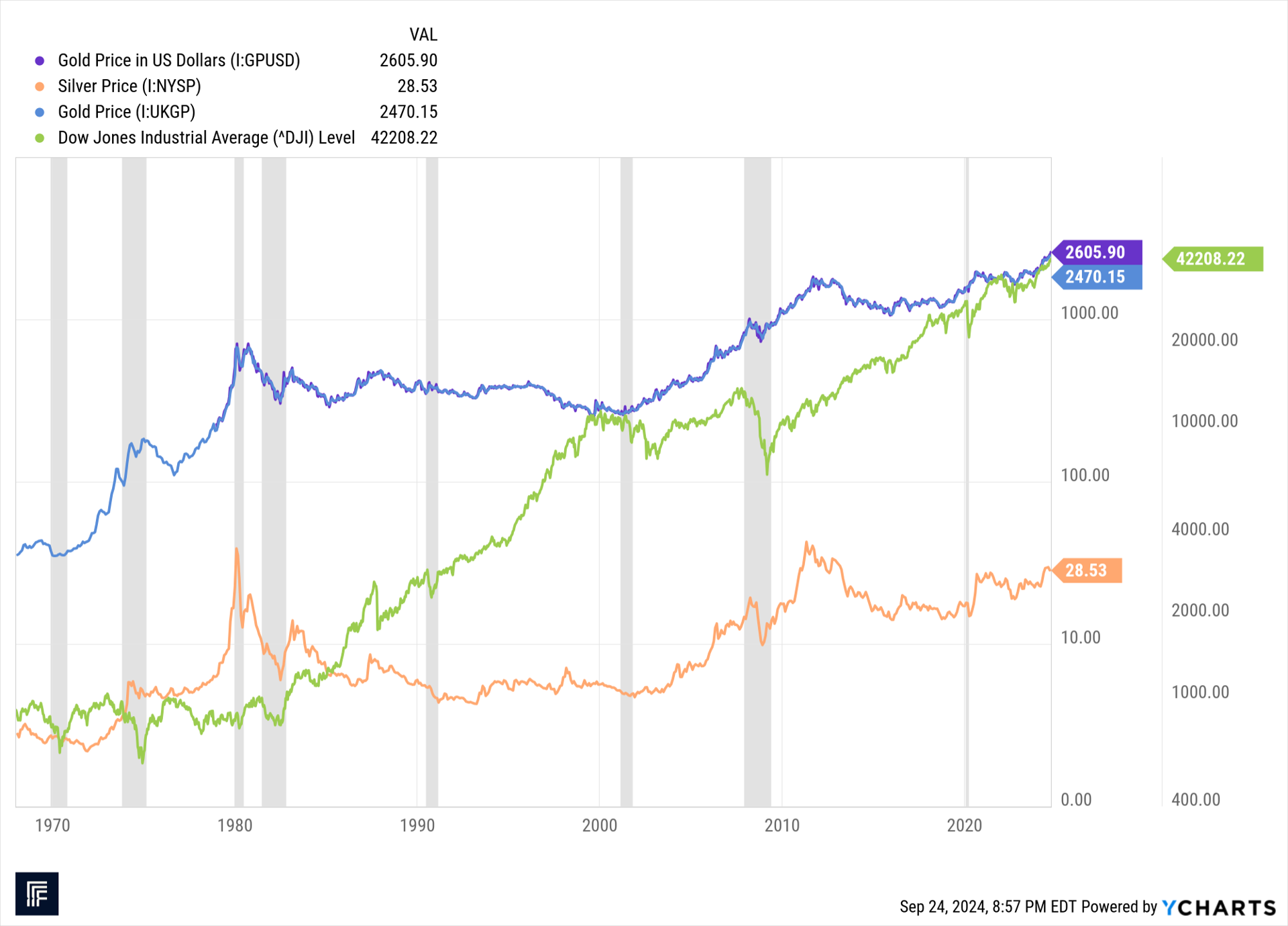

Gold might rally to over $4600, but buy on pullbacks

If you adjust the price of gold for headline inflation, it does not seem extended. In fact, we could be witnessing a long-term base before a huge catch-up rally! A move like this began in 1971 when gold was at $37 and the rally lasted 9 years, hitting $677 in 1980. If we see a similar move from this recent cycle, gold will reach $4632 an ounce!

But gold can be choppy, so I like to enter on pullbacks. And Gold has been known to peak at the start of a recession. For example, gold and silver prices fell when two quick recessions stunned economists in 1980 and then again in 1981. We also saw similar market action during the financial crisis and the COVID recessions.

Don’t wait for an official recession announcement!

The National Bureau of Economic Research (NBER) announces a recession an average of 8 months after it starts, so you have to anticipate. Precious metals prices typically become more volatile giving traders an opening to buy a dip. I take an initial position just in case prices run up right away, and then I try to add to it.

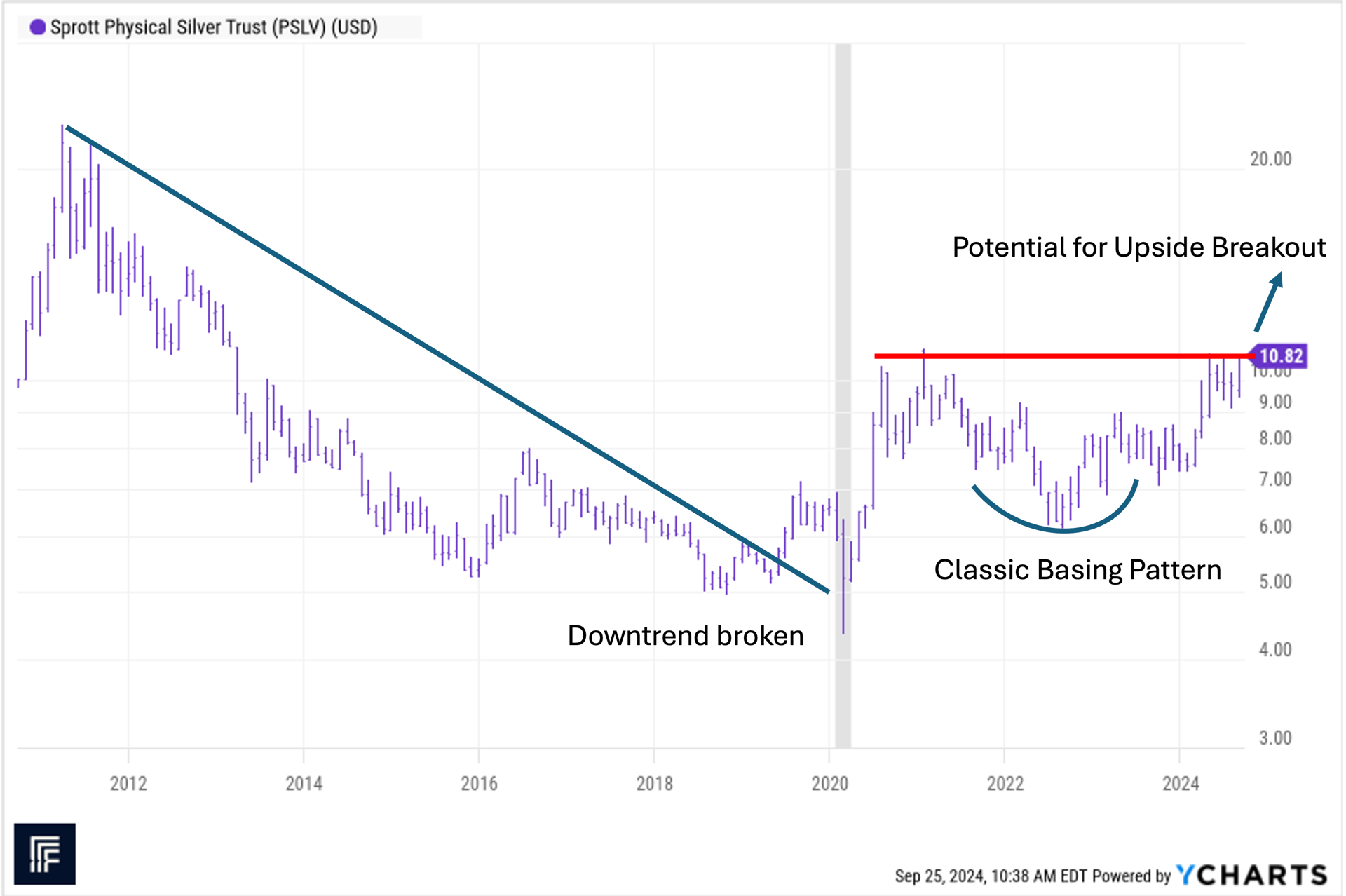

Silver could outperform gold

Silver looks better than gold to me, both technically and fundamentally. When gold rallies, silver can really outperform. The silver-to-gold ratio is low and signals that silver is cheap compared to gold.

Silver could see increased demand from EV batteries, solar panels, and silver nanotechnology in medical sensors.

Technically, silver hasn’t broken out like gold has, which leaves more room for a big move. Based on a traditional measured move from the base to the peak, the upside target is $68 per ounce!

Scaling your buys improves risk-adjusted returns

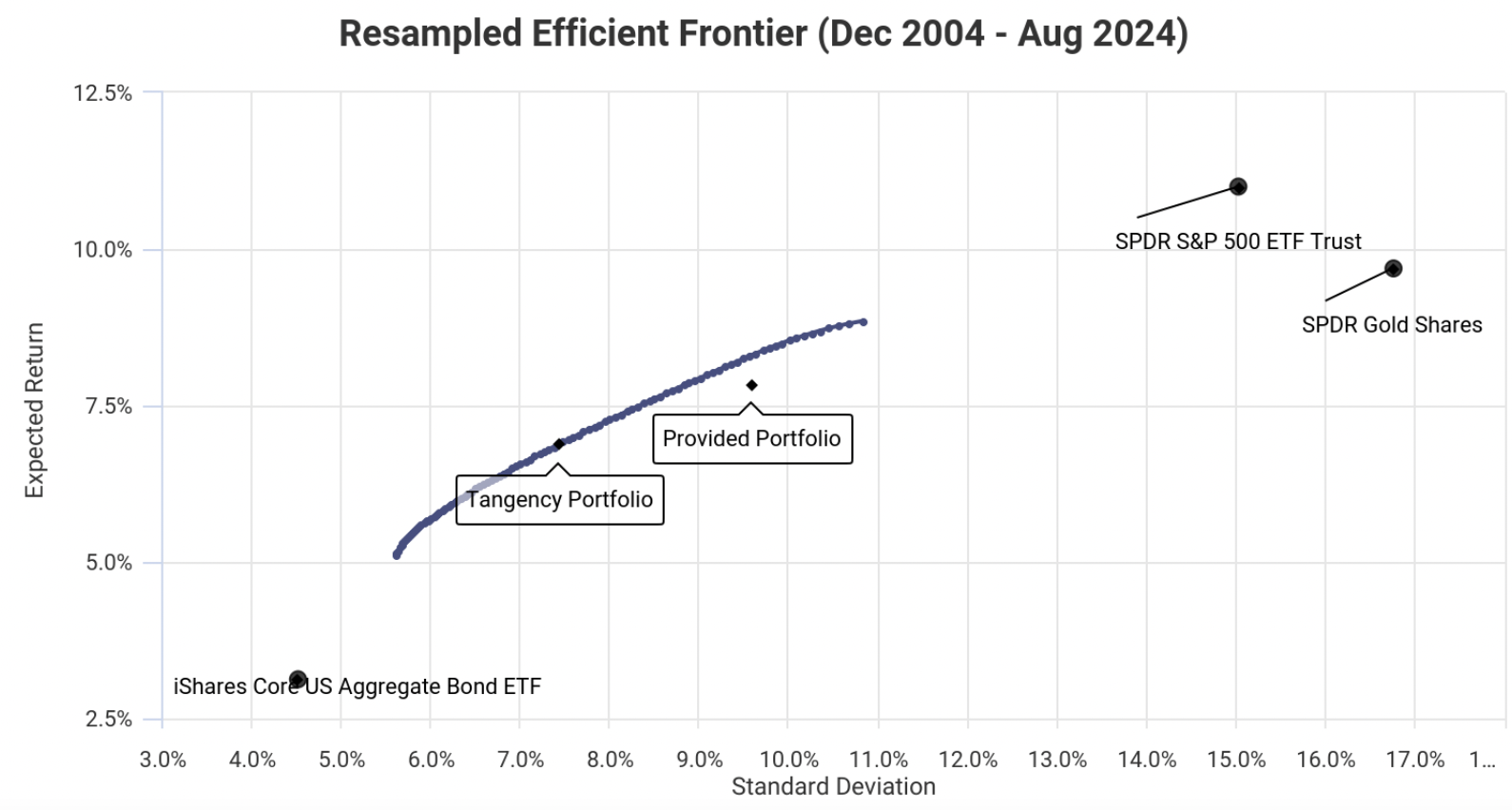

An investor with a 60% stock and 40% bond portfolio could improve their risk-adjusted returns by adding just 5% in precious metals. This simple move helps lower volatility without significantly sacrificing returns.

From December 2004 to August 2024, the correlation between the S&P 500 and gold was only 0.09. During that period, the S&P grew at 10.32% annually, and gold at 8.83%. Both offered similar standard deviations—15.02% for the S&P and 16.75% for gold.

A particularly attractive feature of gold is that its correlation with stocks decreases when stock market volatility rises and prices fall. That's exactly the kind of dynamic I look for when building portfolios.

Should I sell stocks or bonds to buy precious metals?

The easy answer might be to take money out on a prorated basis from both, but the data says that’s not quite right. I'll explain.

Both gold prices and bond returns are correlated with real interest rates, so it makes more sense to shift from bonds. Bonds have lower expected returns, and since gold isn’t as closely tied to stocks, reallocating mostly from bonds should give you better results.

The results of a portfolio optimization clearly show that as gold allocation increases, bonds are reduced more than stocks.

A reasonable case to buy precious metals

Although inflation has been moderating, deficit spending, political risks, and easing of monetary policy seem imminent. A fall in precious metals would be normal, but this is a buy signal for investors that do not yet have an allocation. The long-term outlook is favorable for this asset class too, so taking an initial position is warranted for many investors.

What are your thoughts about precious metals?

Do you think stocks and bonds will outperform gold or silver in the next 3 – 5 years?

Do you think gold and silver will fall if we head into recession?