The Stock Tip Nobody Wants: It Doesn’t Matter

The data show the real edge is never picking winners; it’s something far less exciting.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It happens fairly regularly, but much less than it used to. Somebody will ask me, “What do you think about such-and-such stock?”

I get it. I’ve been around the investing world for a long time, and the trading world before that.

But I don’t have stock tips anymore. And the reason may shock you: They don’t matter.

Here’s the tip nobody wants: The stock doesn’t matter. What matters is something hella less exciting, but more important.

Yeah, I’m Talking About Asset Allocation

“Nearly half of Russell 1000 stocks have suffered a catastrophic loss (50%+ decline) over the past decade, and many never fully recover.”

Concentrated Stock Solutions by Morgan Stanley

“Strengthening Your Portfolio With Diversification”

The 2025 Morgan Stanley report that features the quote above also found that 60% of stocks that outperformed over five years became underperformers in the subsequent five years. For stocks in the Russell 1000 since 2014, the average volatility measured 37%, versus just 15% for the index itself.

That illustrates how broad diversification smooths returns, making a basket of stocks a more predictable investment when a specific return is needed, such as for retirement.

But volatility and catastrophic loss are only half the story. Investors also have to ask where the stock market’s return actually comes from, or which stocks are actually worth owning.

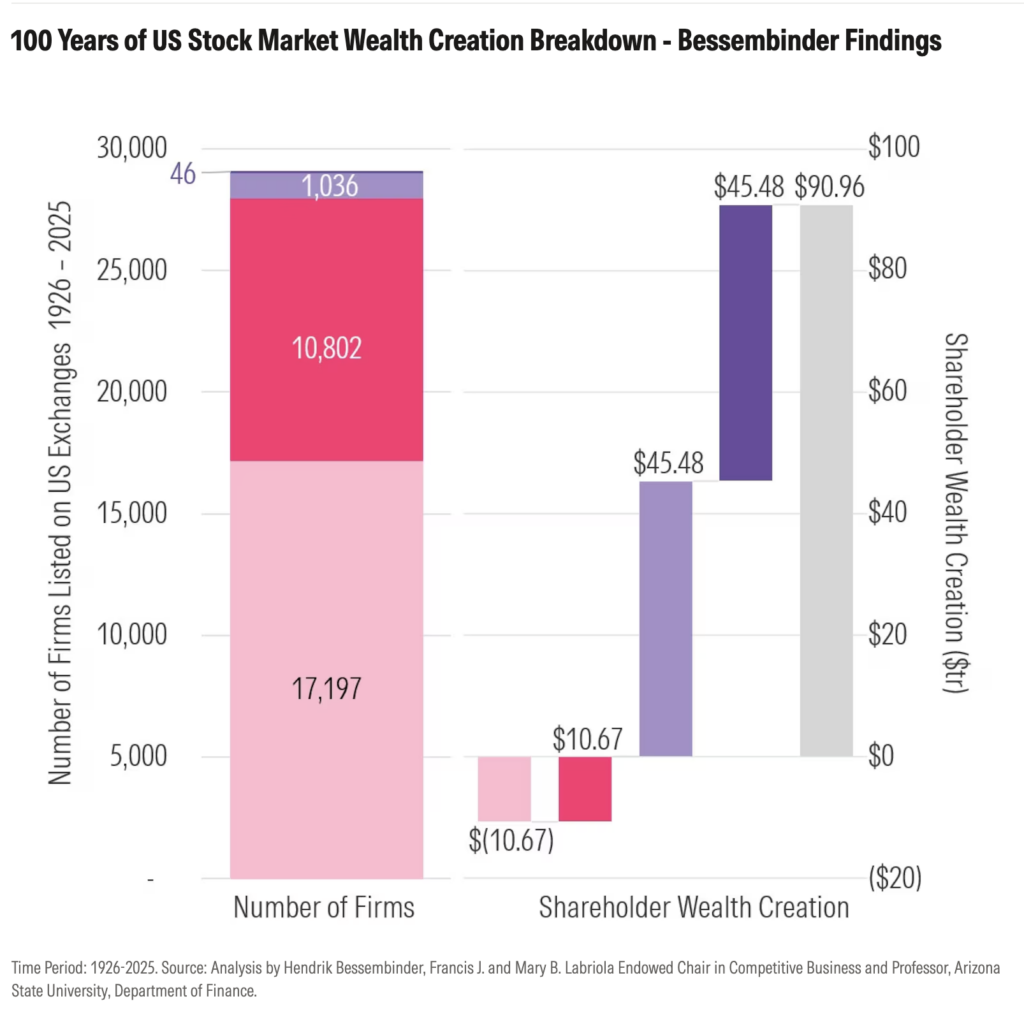

Hendrik Bessembinder, a finance professor at Arizona State University, recently updated his research using a full century of data from the performance of almost 30,000 U.S. stocks between 1926 and 2025.

The chart below, derived from Bessembinder’s research shows that over that 100-year period, U.S. stocks created $91 trillion in wealth, but 17,197 stocks, or more than half, actually destroyed value. Just 46 companies produced half of all the gains.

Go Ahead, Buy That Stock

Look, I’m not telling you to completely give up buying any individual stocks. That would be kind of Scrooge-like.

A small position in a company you like is a fun hobby, and I get the thrill of winning. Personally, I enjoy researching stocks and companies to understand what are the driving trends in society, and where big investors are putting their money.

But the trick is to keep it small and keep it separate from your retirement income plan. There’s a difference between playing with stocks and planning a retirement around them.

As Bessembinder’s research shows, the market’s long-term return doesn’t come from individual stocks, plural. It comes from a handful you would have to identify well in advance, sitting inside a much larger pile that just sat there, like a bunch of couch potatoes.

Professionals Aren’t Finding Them Either

But c’mon, a sharp stock picker can find the winners, right?

Well, that’s exactly what active fund managers are paid to do. And paid well.

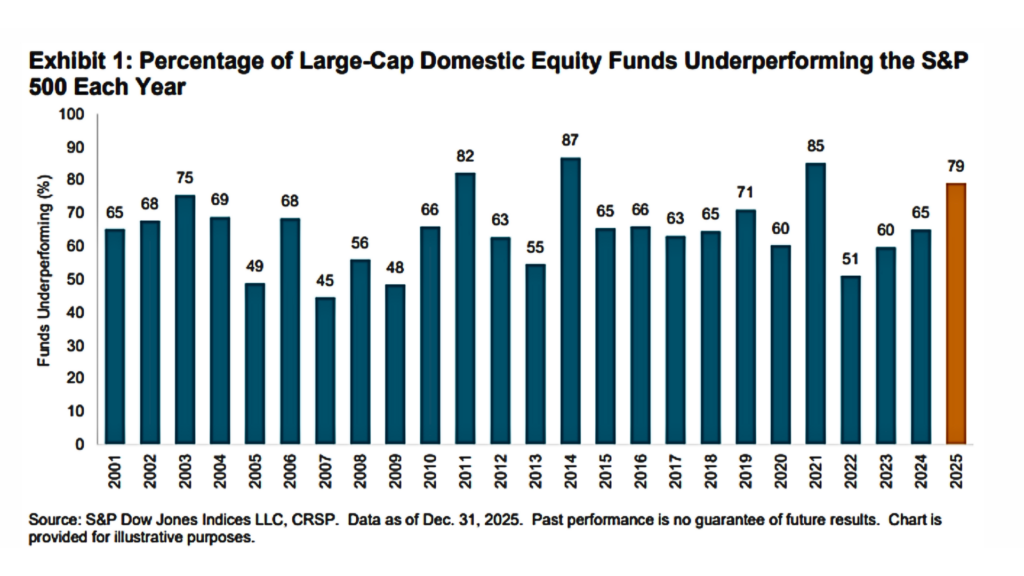

But cue the sad trombone: According to S&P Dow Jones Indices’ SPIVA U.S. Year-End 2025 Scorecard, 79% of active large-cap U.S. equity managers underperformed the S&P 500 last year. That performance is worse than 2024’s 65% of underperformers, and the fourth-worst year for large-cap managers in the scorecard’s 25-year history. International, global, and bond managers didn’t do much better.

If professionals whose full-time job is picking stocks can’t consistently beat a simple index, the odds aren’t in your favor either.

Bessembender nailed it with this comment from his research paper:

“Lists of top performing stocks are of inherent interest, but identifying such stocks in advance is a formidable challenge, to say the least.”

Why You Can’t Manage the Risk

You can’t properly measure risk and return on a portfolio built around individual picks the way you can with a diversified, asset-class-based one.

A single stock is a bet on one industry, one product cycle, one CEO; there’s no clean statistical grounding the way there is for an asset class with decades of return data behind it. You can build a model to try and forecast its return, but that model only holds up if that one company’s story goes the way you assumed.

An asset class doesn’t carry that kind of single-point-of-failure risk. Its expected return is anchored to a century of data across hundreds of companies, not a bet on any one of them. In other words, you’re spreading the risk, not concentrating it.

What to Own Instead

Here’s your tip, and I think it’s a good one. But as Bessembender said, it’s probably not as exciting as some hot takes on whatever ticker is in the news today.

These are my approximate ratios for categories of portfolios. As always, your mileage may vary.

- Conservative: 30% to 40% broad U.S. stocks, 10% to 15% international stocks, the rest in short-term, high-quality bonds

- Moderate: 50% to 60% total stock market exposure, with the balance in bonds

- Growth-tilted: Equities past 70%. Go crazy.

The Real Tip

Yeah, I don’t have one. Not a ticker, not a sector. I think the eBay (EBAY) chart looks pretty good right now, with the stock close to breaking out of a base. Same for Targa Resources (TRGP). No hate if you’re eyeing those on a watch list; I get it!

(To be clear, those are not recommendations, just observations.)

It turns out that the investing edge was never about picking the right stock. It’s owning the market broadly enough that you don’t have to guess which 46 companies out of 30,000 matter (good luck with that!), and then building a portfolio you can plan a retirement around.

Buy the stock if you want to. Just don’t plan your retirement around it.