The World’s Biggest Investor Says You’re Doing It All Wrong

BlackRock says your portfolio strategy is outdated. Here’s what to actually do about it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Wall Street has a new message for people approaching retirement: Everything you thought you knew about building a portfolio is wrong.

BlackRock (BLK) is the world’s largest asset manager, with a mere $14 trillion or so under management. The company made the case that it’s time to review portfolio construction in its weekly market commentary on June 8, titled, “The Need for a New Portfolio Approach.”

The firm argues that macro anchors, like expectations for stable inflation, are gone, and that AI and other forces are reshaping markets faster than traditional portfolio frameworks can handle.

The solution, according to BlackRock, is a fundamentally new approach to portfolio construction.

But what would that mean, exactly?

And is “a fundamentally new approach” even a thing?

Beyond Reading the Labels

BlackRock’s core argument is that investors need to shift away from familiar labels like “stocks” and “bonds” and toward the underlying drivers of risk and return. They’re saying your portfolio categories are too simple for today’s markets, and you need a more sophisticated framework.

According to the BlackRock update, “All asset allocation decisions are active calls in today’s investment environment. This requires portfolios to be built around exposures and convictions, and looking beyond asset class labels.”

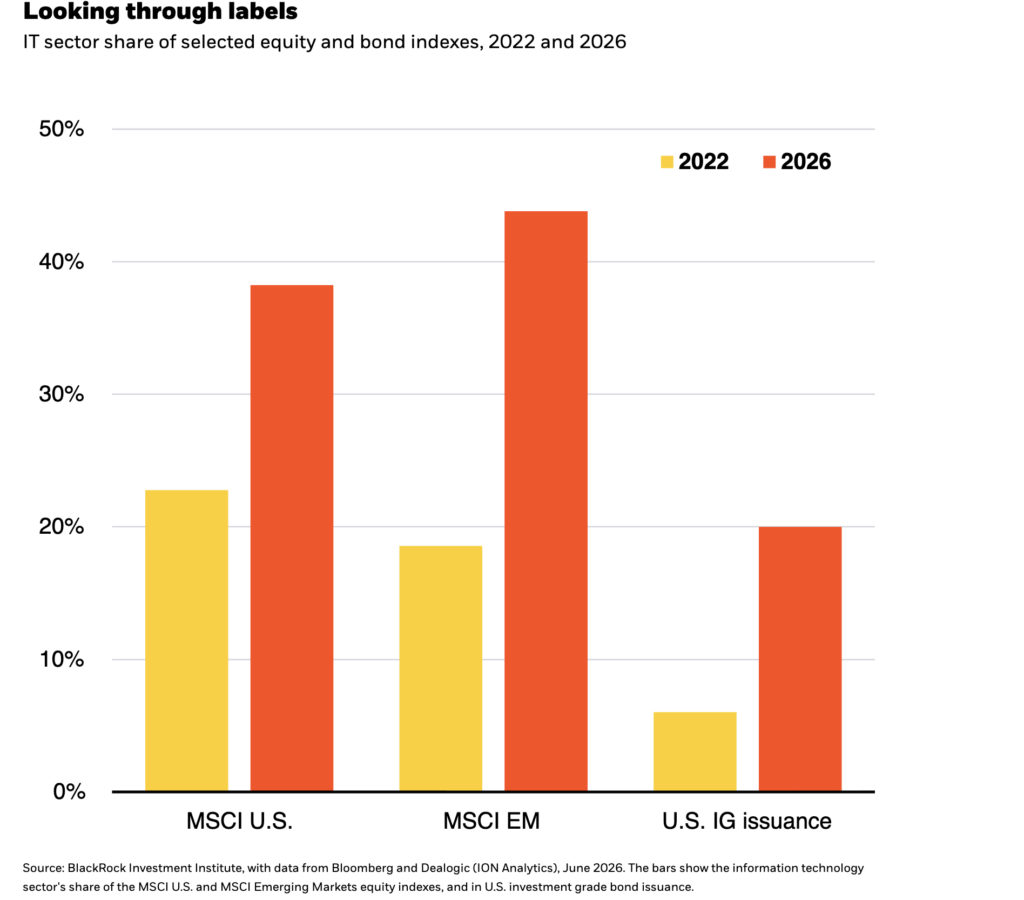

Fair enough. Below is BlackRock’s chart illustrating how much the tech sector’s footprint has grown across major indexes worldwide between 2022 and 2026.

Three indexes are shown:

- MSCI U.S.: Technology share grew from about 23% to approximately 38%

- MSCI EM: Tech grew from around 19% to around 44%

- U.S. IG issuance: Tech allocation grew from about 6% to about 20%

The point this chart is making is that “stocks” and “bonds” are increasingly the same bet.

A broad equity index, an emerging markets fund, and an investment-grade bond portfolio all now carry significant tech sector concentration, and that concentration has essentially doubled in four years.

The label on the wrapper tells you less and less about what’s actually inside.

Where They’re Not Wrong

Give BlackRock credit where the data support it; the company isn’t wrong about tech’s dominance, although that’s far from a new story.

If you own a broad index fund and assume you’re well-diversified, look at your top-10 holdings. You may be more exposed to a handful of tech companies than you think, and that’s worth knowing. As long as those assets perform well, there’s no fund manager “magic” happening.

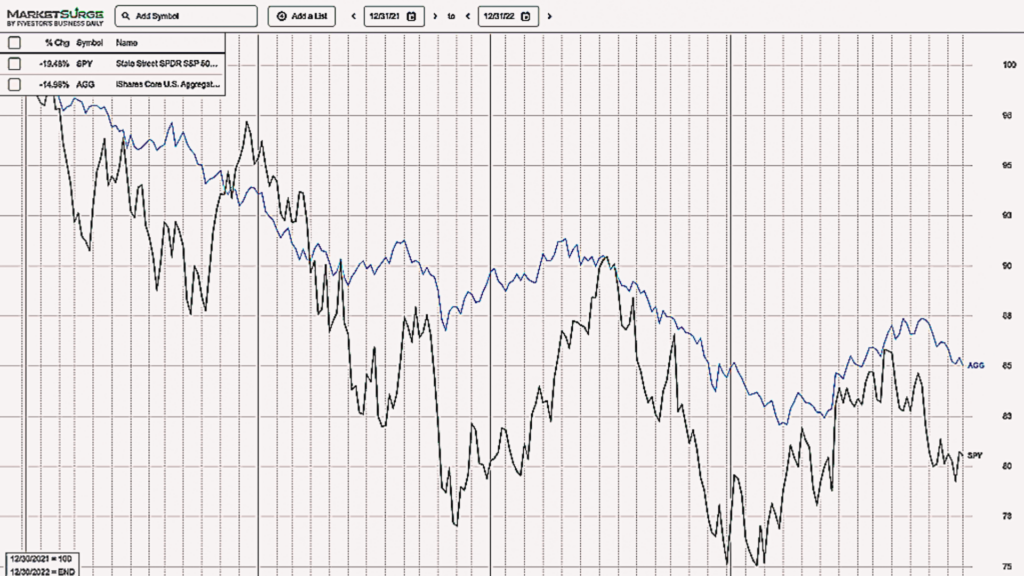

The 60/40 portfolio did have a rough few years. In 2022, stocks and bonds fell simultaneously, something that hadn’t happened in decades. This chart compares the performance of the SPDR S&P 500 ETF Trust (SPY) versus the iShares Core U.S. Aggregate Bond ETF (AGG).

BlackRock has pointed to this as a “diversification mirage,” noting that bonds haven’t been reliably cushioning portfolios against risk asset selloffs. That’s true, and is a legitimate concern, especially for someone five to 10 years from retirement.

These are real issues. They just don’t necessarily require BlackRock’s solution.

What BlackRock’s Solution Actually Costs

Here’s where the savvy consumer angle comes in. The “new approach” firms like BlackRock are selling involve active management, thematic funds, factor strategies, whole-portfolio frameworks and buffered ETFs, all of which come with fees. And fees compound against your returns.

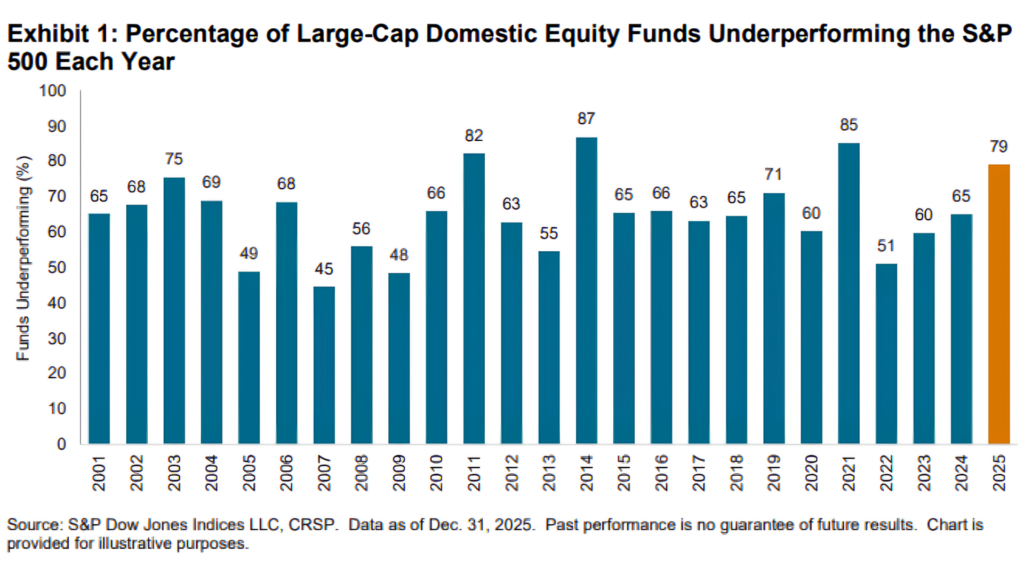

The numbers from S&P Global’s SPIVA U.S. Scorecard, the independent benchmark for active versus passive performance, are tough to ignore.

In 2025, 79% of actively managed large-cap U.S. equity funds underperformed the S&P 500.

Over a 20-year time frame, the picture is even clearer: Across all categories, underperformance rates rose as time horizons lengthened, and after 15 years there were no categories in which the majority of active managers outperformed.

BlackRock’s conclusion is that you need a more sophisticated portfolio. Two decades of SPIVA data suggest the more sophisticated portfolio usually loses to the boring one.

What You Actually Need to Do

This is the practical payoff, and it’s quite a bit easier than what BlackRock is selling.

- Check your concentration. Look at your actual top-10 holdings across all your funds. If five tech companies, or any large-caps really, represent 25% or more of your total portfolio, that’s a real and addressable risk. You don’t need a new framework to fix it. You need to rebalance.

- Think about sequence-of-returns risk. Yeah, this again. I harp on it because it’s really important. The decade before retirement is when a major downturn does the most damage, not because your portfolio loses value, but because you don’t have time to recover before you start drawing it down. That’s an argument for gradually shifting toward stability, not for complexity.

- Know exactly what you’re paying. Log into every account you own and look at the expense ratio on every fund. If anything is above 0.50%, ask why. The answer may justify the cost, as there are circumstances where a particular asset class costs more to hold, but you should know the number. Most people don’t.

The One Question Worth Asking

Whether it’s BlackRock’s weekly commentary, your 401(k)’s default options or a pitch from a financial advisor (particularly one of those who’s an insurance agent first and foremost), one question cuts through most of the noise: What does this cost me, and what’s the independent evidence that it’s right for me?

If the answer to either part is vague, you know what’s up.

BlackRock says portfolio decisions shouldn’t be driven by asset class labels. That’s fair enough. They just shouldn’t be driven by the firm selling the alternative, either.