The Yield Trap Investors Keep Falling For

A high dividend yield can look like a ticket to lasting retirement income, until the cut arrives. Before rushing into a high-yield name, ask yourself three questions.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

When you’re looking for income to provide ballast in your long-term portfolio, so-called “blue chips” might look attractive.

For example, you might consider Verizon (VZ) a “good” stock, right, even though it’s being kicked out of the Dow?

After all, the company raised its dividend for 19 years in a row. That’s what’s called “dividend achievers” territory, which includes companies that boosted their shareholder payouts for at least 10 consecutive years.

In September 2025, Verizon’s board increased the quarterly dividend to 69 cents a share. The stock’s yield is currently 6.14%. For plenty of income-focused investors, Verizon’s combination of a long dividend history, familiar name and big dividend check makes it a portfolio staple, Dow or no Dow.

But yield and safety are not the same thing. Confusing them is one of the most common ways to wake up one morning with a lower dividend and a stock that’s already priced in bad news.

What’s the Story With Verizon?

I’m not saying Verizon, which is among S&P 500 stocks with the highest yields, is the worst example of this I’ve seen. It’s not.

Behind that decline lurk potential red flags like heavy debt and increased competition in the wireless space.

But this isn’t a deep dive into Verizon; the point is to understand whether or not a stock’s yield may signal danger.

How the Trap Works

Yield is just the annual payout divided by the current share price. Which means that as a stock’s price falls, its yield automatically rises. Pretty simple.

So a stock that’s under selling pressure looks increasingly attractive based on just its yield, even as fundamentals like earnings and sales growth are weakening. As the share price falls, investors chasing income are still buying. That might cause the share price to stabilize briefly, but then a dividend cut arrives, and both the yield and the price fall together.

When a dividend stock’s yield is exceptionally high, be aware: There’s usually some sort of cause for concern.

If the dividend were considered safe, investors would be buying up the stock, pushing the price up and the yield back down.

Now, back to Verizon for a hot second: I doubt the company will slash its dividend any time soon, given the company’s long history of increasing its payment to shareowners.

But it does follow the pattern of a falling stock price, which is often more alarming in other stocks.

REIT Case Study

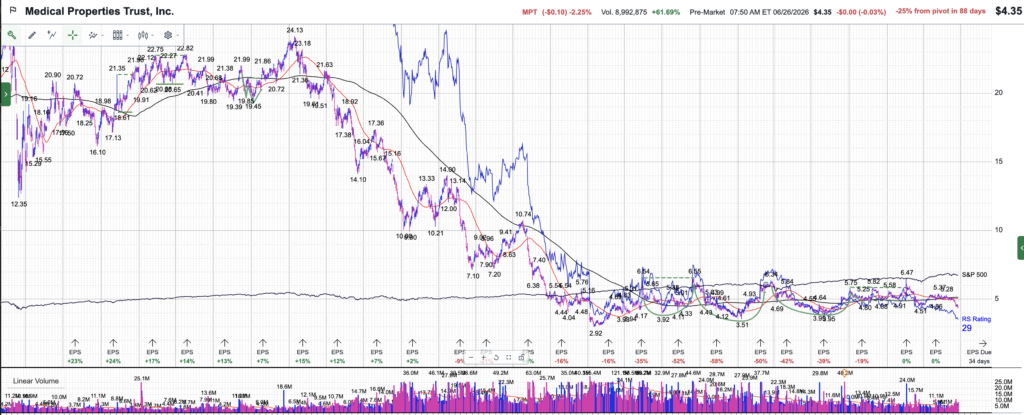

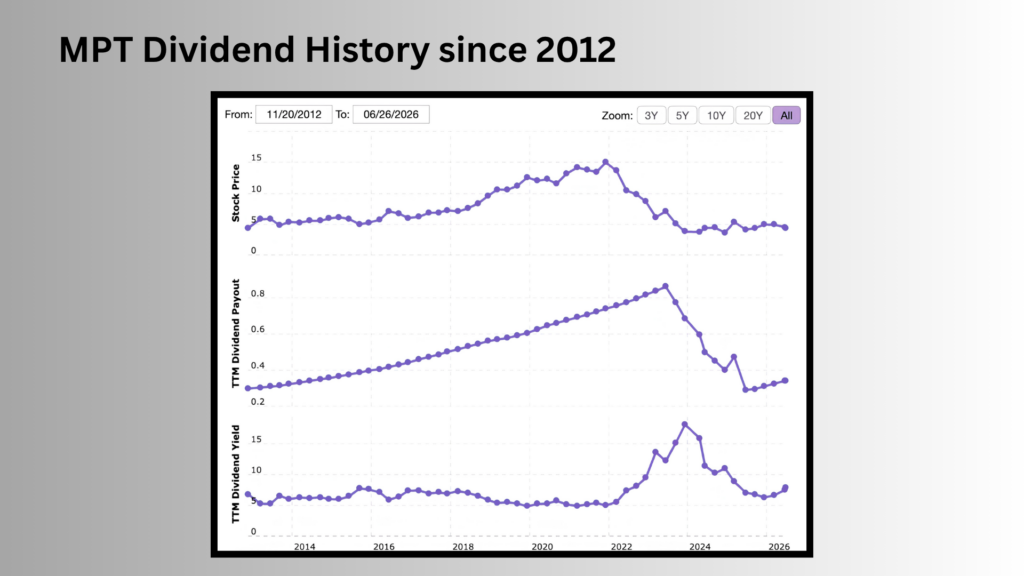

The real estate investment trust Medical Properties Trust (MPT) offers a clear recent example.

In August 2023, the dividend was cut from $0.29 to $0.15. A year later, in August 2024, the board cut it again, this time to $0.08 per share, a total decrease of more than 70% from where it started.

The first chart below shows the stock price plunging. The second is the dividend history.

So what happened?

This was a story whose sad ending was attributable to the REIT structure itself. And REITs often attract investors looking for reliable yield.

REITs are required to distribute most of their taxable income. But real estate depreciates on the books, which means net income can look healthy even when cash is thin.

But because depreciation isn’t something you see deducted from a company’s cash, net income alone can hide whether the company truly has the ability to keep funding a hefty dividend. The REIT structure can magnify that problem.

When MPT’s largest tenant, Steward Health, stopped paying rent, the dividend obligation stayed on the income statement long after the revenue was dropping. Payout ratios looked hunky dory. Except that they weren’t.

Three Questions

Before rushing into a high-yield for income, ask yourself three questions.

- Is the dividend covered by free cash flow, not just earnings?

Net income can look good due to one-time items and it can hide problems like depreciation in a REIT portfolio, but cash flow is harder to disguise. For REITs, review the company’s funds from operations.

Other companies can have cash flow problems, of course. The formerly public company Walgreens is a case in point: Facing declining earnings and negative free cash flow, it slashed its quarterly dividend from $0.48 to $0.25 in January 2024. That didn’t stop a freefall in the share price, though.

But the yield had looked attractive for months before the cut.

- Has dividend growth been slowing?

A 10-year track record of dividend payouts means less if the company’s growth rate has been decelerating.

This is why increasing dividends are a pretty significant indication of a company’s health. Pay attention when you see that.

- Is the debt load rising?

Rising debt can crowd out future dividend capacity even when today’s payout appears to be covered.

For example, its acquisition of Frontier pushed Verizon’s net leverage to about 2.5 times EBITDA in early 2026. That contributed to a share price decline and to the company’s being booted out of the Dow.

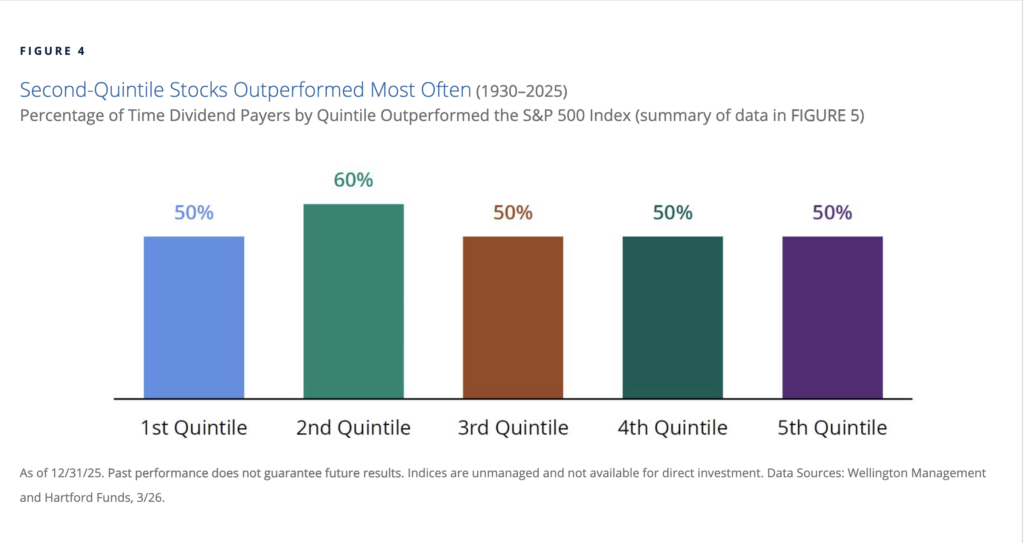

High Yield Can Be Deceptive

Research from Hartford Funds and Wellington Management, covering S&P 500 data from 1930 through 2025, found that stocks in the highest quintile of dividend yields have historically underperformed those in the second quintile.

Sounds a little counterintuitive, but it illustrates the point about higher dividends not always being as safe as they same.

This image from Hartford Funds illustrates that phenomenon.

In this study, researchers showed that the highest yielders aren’t the best performers; they’re often stocks the market has already marked down for a reason.

Cash flow quality matters more than the yield number in isolation.

For example, a 9% yield backed by reliable free cash flow is a different animal than a 9% yield because the share price has fallen 40% and the board hasn’t chopped the dividend yet.