Michael Burry Vs. My Panic Points; Ferocious Foxconn Sales; Bad Jobs Data

Why I’m sticking to plan on memory stocks; also, let’s brace for the week ahead, check the markets’ charts, and interpret those jobs numbers.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Morning, gang. What to with, or do about, the results of last week’s price discovery process? That’s a difficult question. How about certain positions? That’s an even tougher question. The headline-level indexes were indeed tested, but for the most part, passed those tests, at least technically. That said, the final two trading sessions of the four-day holiday impacted workweek sported a ferocious beatdown that rotated capital out of semiconductor stocks and other “AI-type” stocks. The memory / storage basket stocks, which have been a big “Sarge” trade, were especially impacted.

The Philadelphia Semiconductor Index, on Friday, relied upon its 50-day simple moving average for support. All while those memory / storage stocks, namely, Micron Technology (MU), SanDisk (SNDK), Western Digital (WDC) and Seagate Technology (STX) all gave up at least 20% individually, for the four-day period. So, did I reduce the size of my basket due to the magnitude of that selloff? To be totally honest, yes, but only because I had used my long position in WDC as a day trading vehicle last week.

I have not cut back on my exposure to the heavyweights in that basket, SanDisk or Micron, even with the pressure applied by the news that Michael Burry was not a fan. I have panic points for a reason, and trade/invest in a disciplined manner for a reason. Concerning Micron, where Burry actually disclosed a short position, I wrote to you wonderful folks last week to tell you that my panic point was the 50-day simple moving average. Well, Micron has not come anywhere close to actually making contact with that line.

Concerning SanDisk, I wrote that my panic point was the 21-day EMA, which currently stands at $1,933. The shares closed on Thursday at $1,745. True, the line was pierced. Not true that the lien was lost. Though the trading range for this stock for any single day can be immense, remember what I have taught you. For a level to be lost, contact with said level must be lost. The simple piercing of any given line is irrelevant in that regard.

Hence, even if the shares surge back on Monday, if they fail to reach that line in the sand, contact may be lost and I may have to act. The shares are trading around $1,825 overnight as I write this. Fortunately, should I have to act, I do have enough shares in inventory to give this name a haircut with exiting the name completely.

On That Note…

Overnight, Foxconn reported June sales that were up 52.1% year over year and second-quarter sales that also beat expectations. For the third quarter, Foxconn, formally known in Asia as Hon Hai Precision, projected that AI rack shipments would maintain their growth trajectory. Foxconn is a major supplier to both Apple (AAPL) and Nvidia (NVDA). Hence, if the tech space is going to catch some bids in what could be a rotational rebound, this news could act as a tailwind, for at least Monday’s regular trading session.

Last Week

The week is over and so are the holidays. At least until Labor Day. Position traders and commission brokers rejoice. The pressure to have to out-earn your daily average on a per-week or per-month basis is off, at least until early September. Market holidays are never truly welcome events for those working without a safety net (base salary).

The short week kicked off with optimism over the U.S. and Iran calling a halt to what had been rekindled hostilities as the two nations decided to get back to the table and try to reopen the Strait of Hormuz. Recent days do show that maritime vessels are traversing through that passage unmolested. This has resulted in a continued slide in crude oil prices.

Toward the end of the week, in addition to the AI-trade beat-down, the national macroeconomic condition became an issue as the BLS June employment report disappointed badly. As far as non-farm payrolls are concerned, the BLS Establishment Survey showed job creation of just 57,000 positions for June. In addition, new May jobs were revised down to 129,000 jobs from 172,000 and April jobs were revised down to 148,000 from 179,000. Still decent months, but those numbers leave June’s net job creation compared to expectations, at -17,000.

Even worse, the BLS Household Survey sported a June print of -507,000 employed persons as 720,000 people dropped out of the labor force. This took participation down to 61.5% from 61.8%, which is a horrific drop for one month’s time. Hence, both the unemployment and underemployment rates deceptively moved lower. That does not reflect increased demand for labor, kids.

The question now, kids, is this: Do weaker labor markets increase the prospects for short-term rate cuts or at least decrease the probability for a rate increase? The answer is “yes.” That would be good for our marketplace. One would think. Unless investors and traders start to price in a recession. That would be bad. Very, very bad.

Week Ahead

A full week lies to our direct front. This will be the final week of the market’s “off-season” as Q2 reporting season will kick off with the big U.S. banks next week. The week will be quiet in some ways. Not so light in others. Let us explain…

- The Geopolitical:

It would appear that while tensions in the Middle East could be cooling, it won’t take much for tempers to reflare in that corner of the world. In other news, OPEC and OPEC allied nations have decided to increase output again, and Russia has launched a heavy attack on Kyiv, Ukraine on the eve of the NATO summit in Turkey.

- Macro:

This will be a fairly thin week for U.S. macroeconomic events. This morning, the Institute for Supply Management will release the results for their June service sector PMI survey. On Thursday morning, the National Association of Realtors will release June existing home sales, which is the largest slice of the national housing pie. In addition, the U.S. Treasury will auction off $39 billion worth of new 10-year paper on Wednesday afternoon and $22 billion in new 30-year bonds on Thursday afternoon.

- The Federal Reserve…

The Fed will be back in action, publicly, after for the most part, taking last week off. The central bank will release the Minutes from the June meeting on Wednesday afternoon. In addition, we’ll hear from a number of speakers, including Fed Gov. Christopher Waller on Monday morning. Waller is influential. We’ll also hear from NY Fed Pres. John Williams and Dallas Fed Pres. Lorie Logan on Thursday. They both hold policy voting rights for 2026.

- Earnings:

Second-quarter earnings season will not begin in earnest for another week. This week, we will hear from a few firms, but no real headliners. Readers can consider this week the second quarter reporting “pre-season.” On Wednesday afternoon, Levi Strauss (LEVI) will go to the tape with their numbers. They will be followed by PepsiCo (PEP) on Thursday morning and Delta Air Lines (DAL) on Friday morning.

- Events:

1) The quiet period for those underwriters that participated in the SpaceX (SPCX) initial public offering expires this Tuesday. That means that investment banks can legally release research reports and ratings for that stock at that time. Yes, the algorithms that run price discovery in 2026 will be ready.

2) The Allen & Company Sun Valley Conference will kick off in Sun Valley, Idaho on Tuesday and run through Sunday, though participants will likely leave in droves by Friday. This is not an agenda-driven event but is heavily attended by executives from major corporations. The event (often called summer camp for billionaires), this year will be attended by representatives of Apple, Amazon (AMZN), Meta Platforms (META), Alphabet (GOOGL), OpenAI, Netflix (NFLX), and Disney (DIS).

3) The RAISE Summit is a global AI leadership conference that will take place this week from Tuesday to Thursday from Paris. This year, we expect to hear from representatives of Alphabet, Advanced Micro Devices (AMD), Broadcom (AVGO), Anthropic and OpenAI.

The Week That Was…

The S&P 500 posted a third winning week in four last week, as did the Nasdaq Composite. That said, the four-day period was quite messy. This is how it went…

- The S&P 500 closed almost flat on Friday and 1.71% for the week.

- The Nasdaq Composite gave up 0.8% on Friday but gained 1.87% for the week.

- The Nasdaq 100 surrendered 1.61% on Friday and 0.38% for the week.

- The Russell 2000 lost 0.55% on Friday and 0.39% on the week.

- The S&P Small Cap 600 gave back 0.71% on Friday but added 0.08% for the week.

- The S&P Midcap 400 lost 0.44% on Friday and 0.51% for the week.

- The Dow Transports gained 0.25% on Friday and 0.38% for the week.

- The Philly Semis were pummeled for 5.44% on Friday and for 9.43% for the week.

- The KBW Bank Index gave up 0.24% on Friday and 0.29% for the week.

On Friday, eight of the eleven S&P sector SPDR ETFs closed out the session in the green. The defensive sectors out-performed for the day as health care (XLV) led the defensives. Technology (XLK) finished out the day in a very distant last place.

For the week, seven of the 11 S&P sector SPDR ETFs finished in the green. Performance for the week was well-spread among defensive, cyclical and growth sectors. But health care still led and tech still had to rise in the caboose.

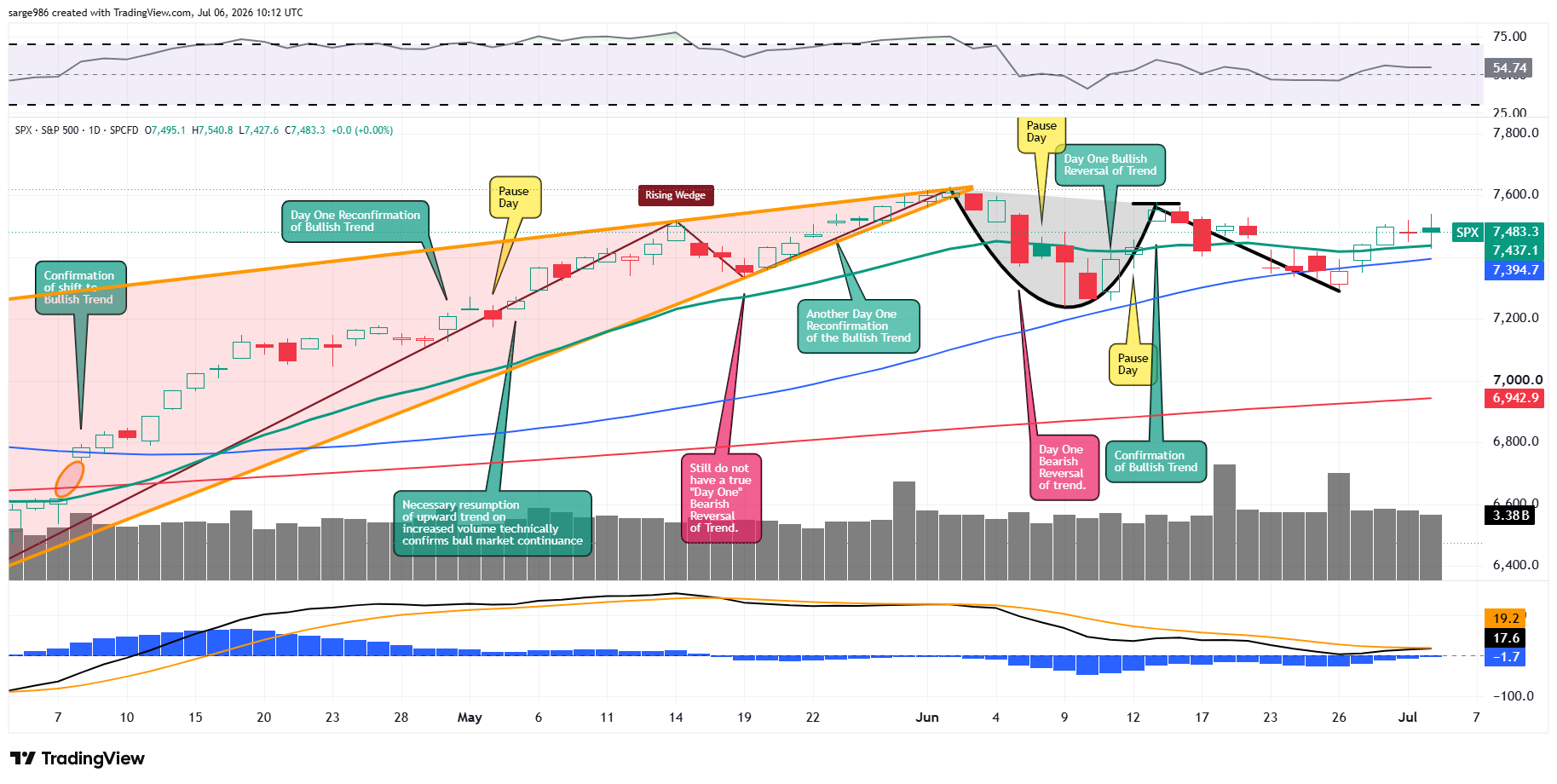

The Charts

Readers will see that the S&P 500 regained both its 50-day simple moving average and 21-day exponential moving average last week, ultimately finding swing trader support at that 21-day line three days in a row.

Relative Strength has stabilized above the neutral line, while the daily moving average convergence divergence has improved to the point where the index could be a single day away from sending more bullish signals.

Readers will see that the Nasdaq Composite is in a very dangerous place entering the new week. The index closed in such a place that both the 21-day EMA and 50-day SMA could wind up standing as either support or resistance through the early days of the period.

The tech heavy Nasdaq 100, even with all of the troubles experienced by large cap Tech and AI stocks over recent days, still has not lost its 50-day SMA. For a second straight week, the Nasdaq 100 found support at that line. However, this index could use some help when it comes to my “go-to” indicators such as the Relative Strength Index and daily moving average convergence divergence.

Earnings

As of June 26, according to FactSet, for the second quarter, Wall Street now expects to see year-over- year earnings growth for the S&P 500 of 23.3%, up from 23.1% last week. Wall Street also sees revenue growth of 12.2%, down from 12.3% one week ago. For the second quarter, 48 S&P 500 companies have issued negative earnings guidance while 63 have issued positive guidance.

For the full year of 2026, the street now looks for earnings growth of 24.1%, up from 24% last week, and up from 14.7% more than two months ago. This would come on revenue growth of 10.8%, down from 11.2% last week but up from 7.7% a rough ten-plus weeks ago. The outlook for the third quarter is also very positive. Third quarter S&P 500 earnings growth is now estimated at 26.8%, year over year.

At the moment, the Energy and Technology sectors are projected to have grown Q2 earnings an absolutely jaw-dropping 122.1% and 63.3% respectively. Just one sector, Health Care (at -9.5%) is currently projected to have suffered a Q2 earnings contraction.

Interesting

According to this week’s “Earnings Insight” newsletter at FactSet, the Q2 bottoms-up EPS estimate for the S&P 500 increased by 3.4% to $81.54 from March 31st to June 30th. In a typical quarter, analysts, in aggregate, usually reduce earnings S&P 500 estimates as the quarter wears on. Over the past five years, the average reduction in consensus EPS estimates during the quarter has been an even 2%. Over the past ten years, the average decline has been 2.7%. Very interestingly, the second quarter marked the largest increase in the street consensus EPS estimate during a quarter since Q2 2021. Five years. Hmmm.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 20.4 times twelve months’ forward-looking earnings, up from 20.1 times last week but down from 21.6 times about ten weeks ago. This is still well above the five-year average of 19.9 times for the index as well as being well above its ten-year average of 19 times.

The S&P 500 also ended last week trading at 27.8 times trailing twelve months’ earnings, up from 27.3 times just one week ago, and also above levels that the index reached more than two months back. This also stands well above the five-year (24.5 times) and ten-year (23.4 times) averages for the index.

Only five of the eleven sectors are now trading above their five-year average valuations, led by the Industrials (26.0 times). Six sectors closed out last week undervalued relative to or even with their five-year norms, up from three sectors just last week.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 78% probability for no change to be made to the current target range (3.5% to 3.75) for the Fed Funds Rate at the culmination of the next FOMC policy meeting on July 29th. That’s up from 70% last week at this time. There is no chance for a rate cut being priced in, but there is now a 22% likelihood for a rate hike being accounted for.

There are no rate cuts fully priced in at any point in the future looking out towards year’s end 2027. That said, there is now a rate hike priced in for September 16th of this year (55% probability, down from 60%). That probability rises to 78% if given the rest of the calendar year 2026.

Economics (All Times Eastern)

09:45 – S&P Global Services PMI (June-F): Flashed 51.3.

10:00 – ISM Non-Manufacturing Index (June): Expecting 54.2, Last 54.5.

The Fed (All Times Eastern)

11:00 – Speaker: Reserve Board Gov. Christopher Waller.

Today’s Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long MU, SNDK, STX, WDC, AMD equity.