Are You Investing or Simply Gambling?

Playing these three stocks is no better than betting on horse races or the NBA or NHL playoffs.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Many people fool themselves into thinking they are prudently investing.

Many high-volume stocks, though, are nothing more than the equivalent of risky sports betting, where quick results can prove very profitable or end up as 100% losses of principal.

Look back at these three formerly high-flying stocks to get proof of what I am speaking about.

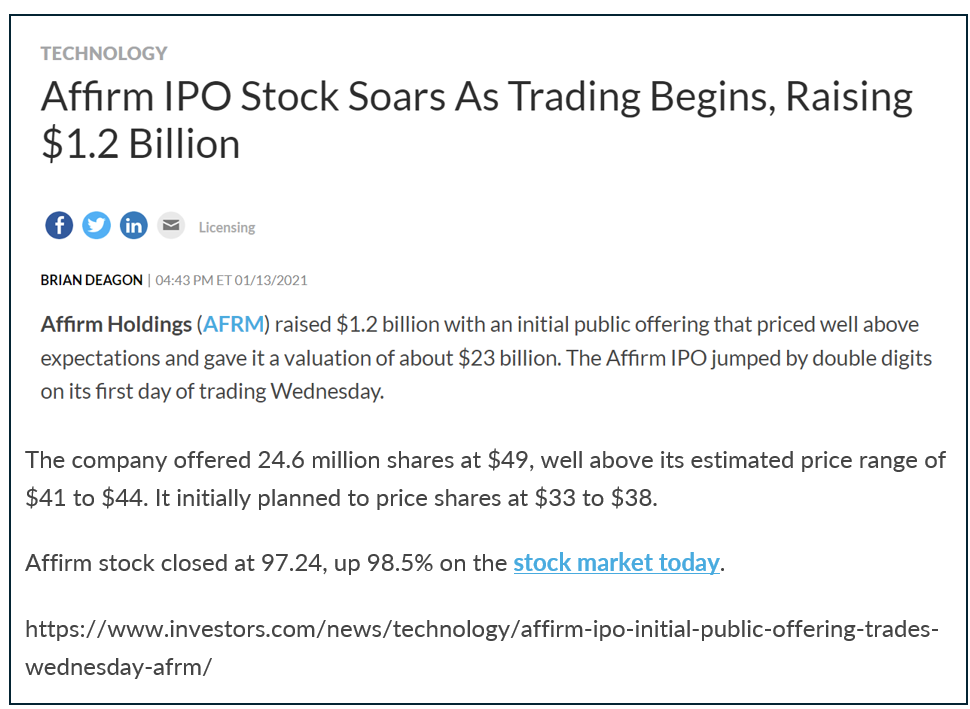

Affirm Holdings AFRM came public in January 2021 priced at $49 per share. It ended that day up 98.5% from its IPO level.

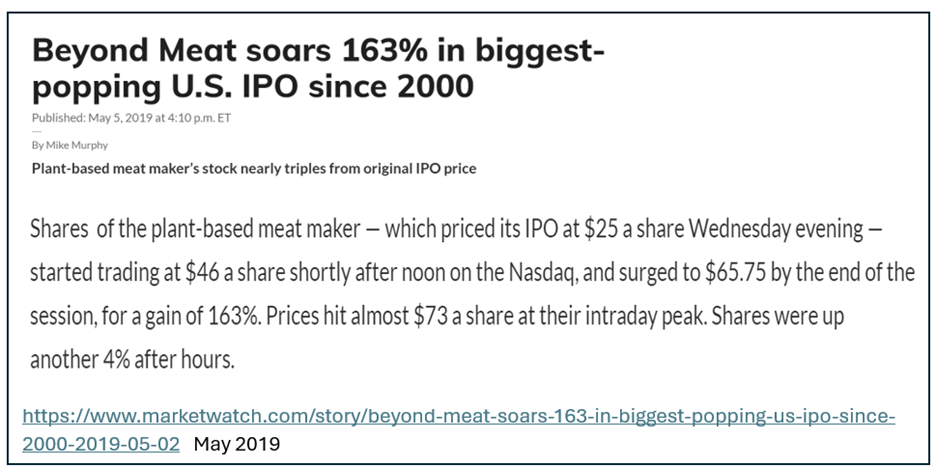

Beyond Meat BYND outdid AFRM. Its IPO came at $25. By 4 p.m. that day it settled 163% higher, at $65.75, while still down from almost $75 intraday.

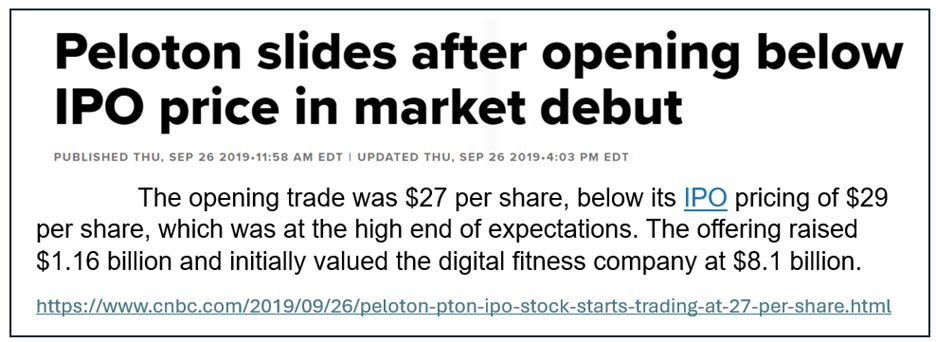

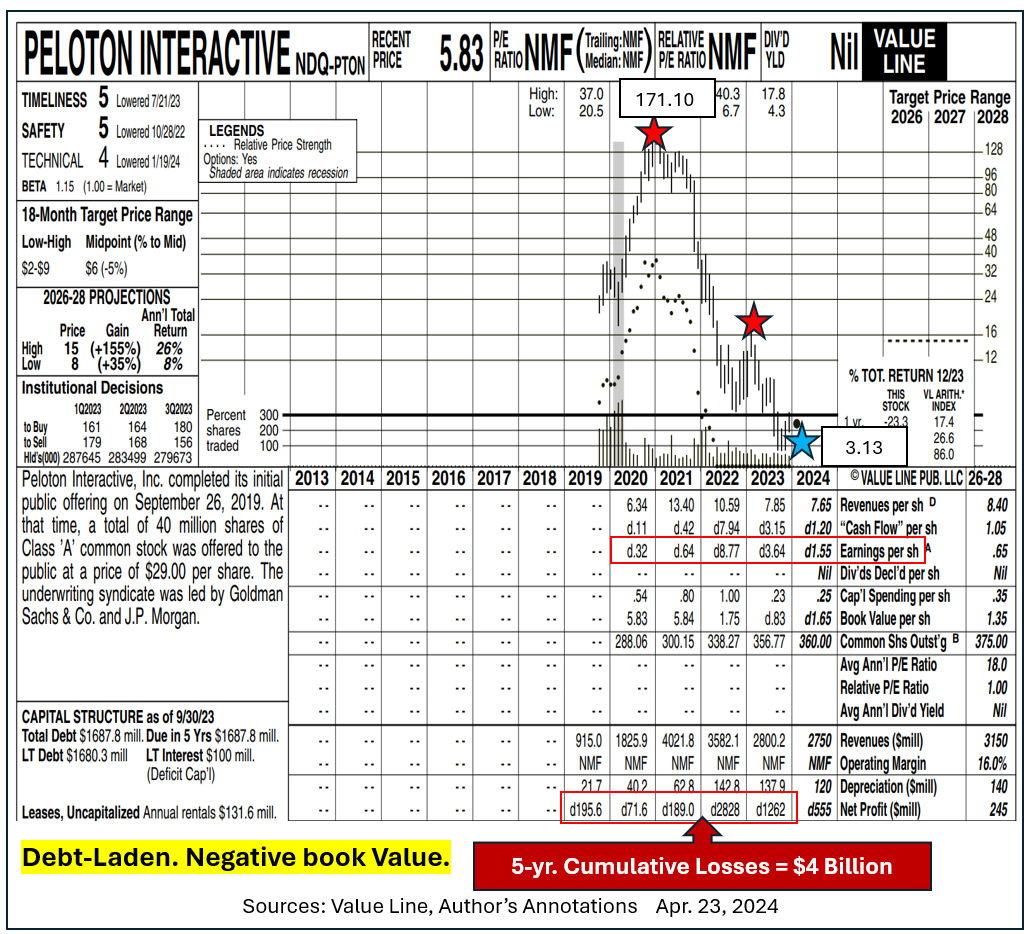

Exercise equipment maker Peloton PTON priced its IPO at $29 during September of 2019. It slid back on its first day of trading but rebounded quickly, hitting $37 before year-end.

Check out the fundamentals on those firms to see why no true investor should have wanted to own them.

Affirm focuses on a horrible business. They lend small amounts to buyers of retail goods as buy now, pay later loans. If customers make all installment payments on time there will be no interest accrued.

Miss any deadlines, though, and high interest kicks in immediately. What was sold as “interest-free” loans can morph into higher costs than many credit-card rates.

If those loans go bad Affirm will end up eating many write-offs as the expenses involved in collection of small dollar debts is prohibitive.

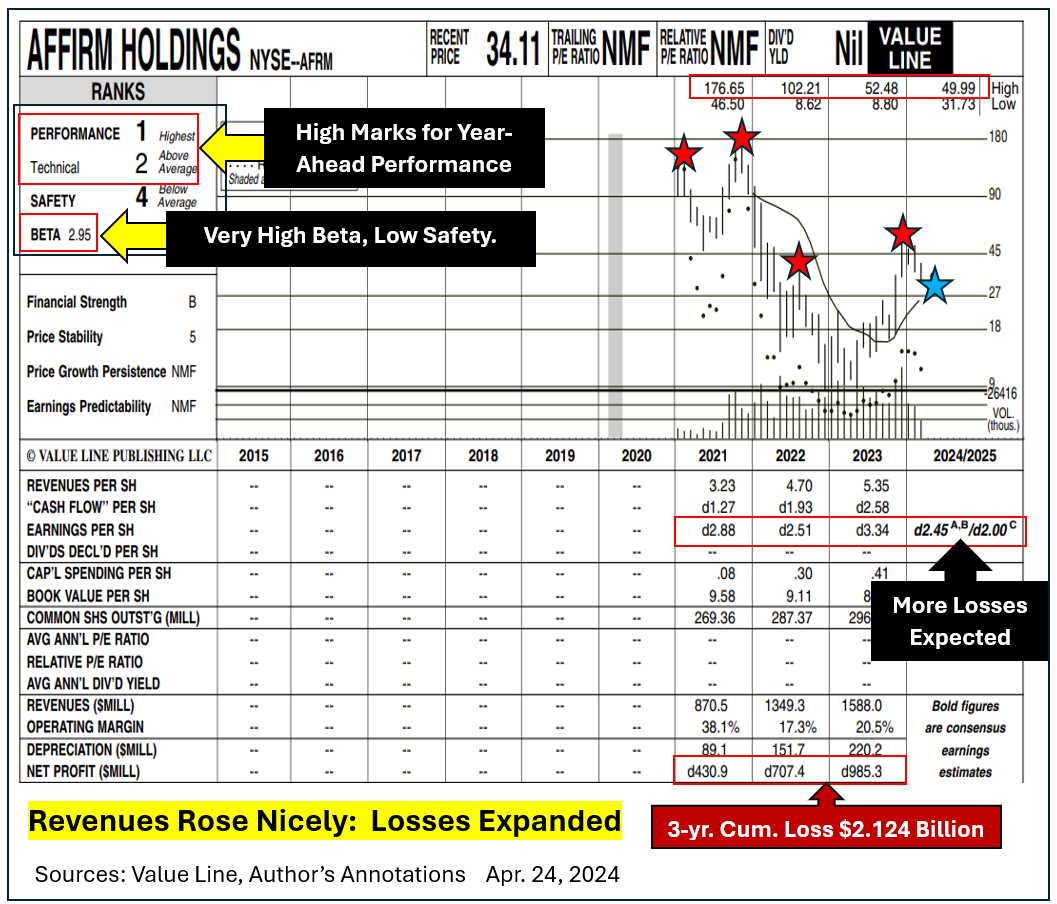

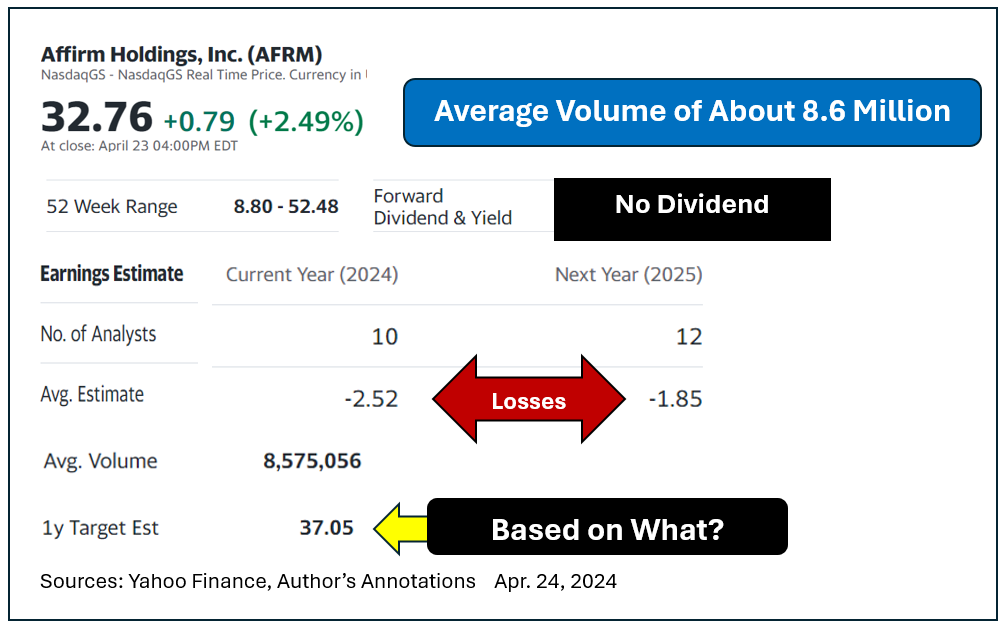

From its first three years as a public company Affirm lost about $2.12 billion cumulatively. Analysts see further large losses for both 2024 and 2025.

Amazingly, Value Line’s timeliness ranking for Affirm labels its shares a “best buy” for year-ahead performance. Its technical ranking for AFRM is above average as well. Why? They do not say.

The business model appears flawed. Revenues advanced dramatically since 2021 yet no economies of scale have kicked in. Net losses grew larger during each of the past two years.

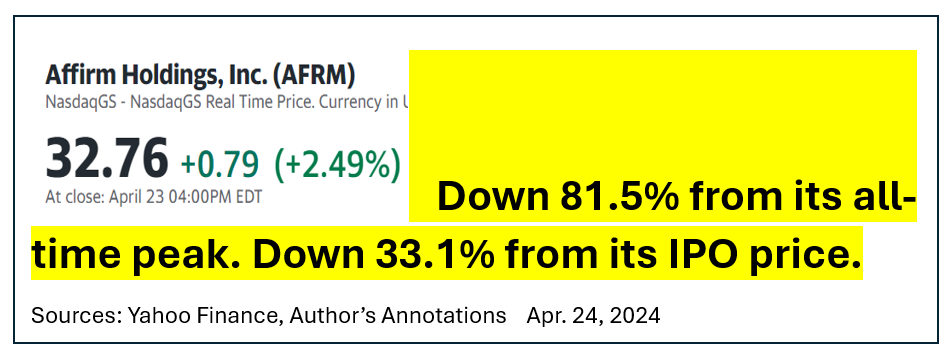

Affirm surged in price to north of $176 late in 2021. As of Apr. 23, 2024 the stock fetched $32.76.

Despite those horrendously bad numbers AFRM has average daily trading volume of almost 8.6 million. Yahoo Finance carries a year-ahead target price for AFRM of $37.05. They make no attempt to justify that number, which seems fanciful to me.

Anyone playing these shares is gambling on short-term fluctuations which have absolutely no connection to any calculable fundamental value. If somebody offered to gift you the entire company for free, on the condition that you could not sell any shares or borrow against them, you would be hard pressed to say yes.

Affirm carried greater than $6 billion in debt as of Dec. 31, 2023. Who could afford to absorb those huge losses on the hope that maybe someday AFRM will turn profitable?

How About Peloton?

Peloton had the good luck to benefit from the Covid-era lockdowns of commercial gyms. What could be better than selling home-based exercise equipment when people were prevented from going out?

Revenues more than doubled from 2019 through 2020. Peloton’s losses doubled, too, As with Affirm the company did not capitalize on economies of scale. Product recalls and the end of lockdowns then combined to decimate Peloton’s results.

Losses expanded and debt ballooned. Book value is now negative. Interest on over $1.68 billion in debt is not being earned. PTON never deserved its run-up and is now a serious bankruptcy candidate, in my view.

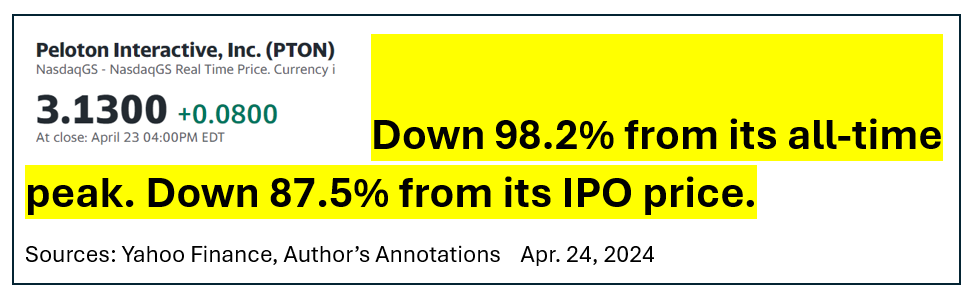

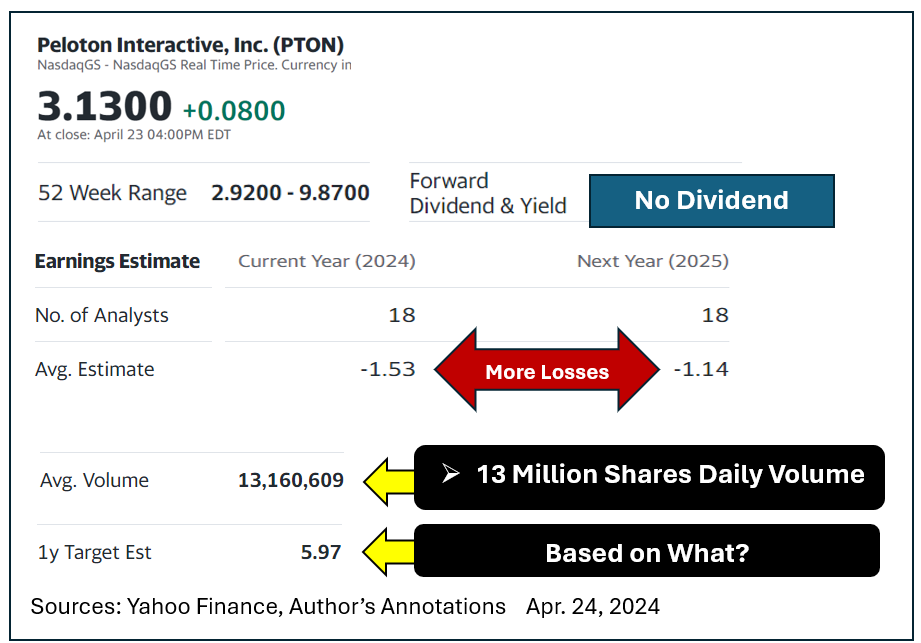

Peloton stock closed at $3.13 on April 23, 2024. True investors should have no reason to own PTON shares. Gamblers, though, love its high volatility enough to trade over 13 million shares daily.

Yahoo Finance sees nothing but bad fundamental news on the horizon. They forecast a near doubling of PTON shares by this time next year while giving no reasoning whatsoever for that goal.

More From Paul Price:

Remember When Plant-Based 'Meat” Was a Hot Idea?

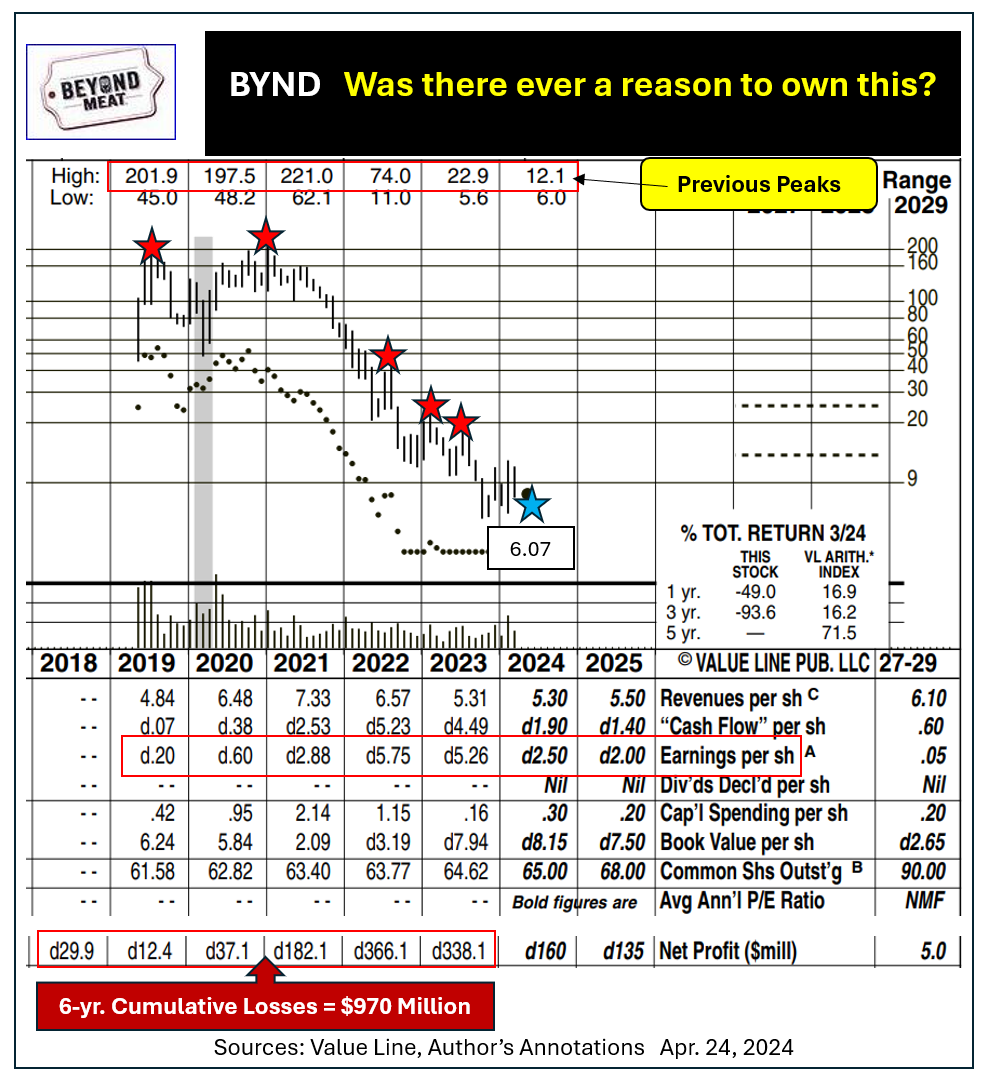

Beyond Meat benefited from that concept following its IPO. The shares reached $221 in January 2021 on hopes that the public would flock to both Whole Foods market and fast-food outlets in search of healthier sounding products.

That has not proved accurate enough to allow for profitability. From 2019 through 2021 sales surged. Amazingly, losses expanded even faster. Since 2021, revenues declined significantly as consumers went back to real meat. Six-year cumulative losses through 2023 approached the billion mark.

No profits appear on tap for years to come. With greater than $1.1 billion in debt and negative cash flow a future bankruptcy is possible.

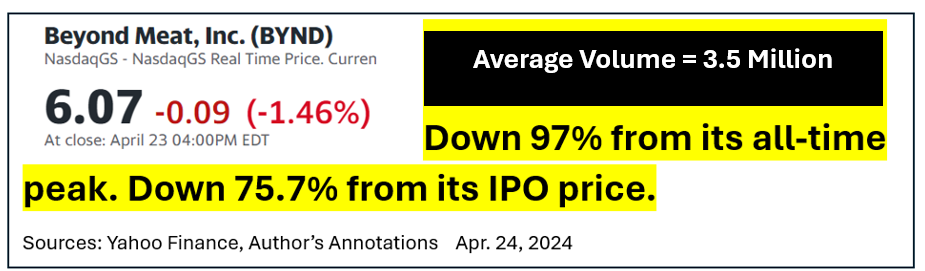

True investors in Beyond Meat should be nowhere in sight. Despite that assessment BYND has average daily volume of nearly 3.5 million shares.

Playing BYND, AFRM, or PTON is no better than betting on horse races or the NBA or NHL playoffs. The only difference might be the fact that realized losses on stocks like these can be used to offset gains made elsewhere.

If entertainment is your goal go for it. Just be aware that you are gambling, not investing. Over the long-term the house always wins.

At the time of publication, Price had no positions in any stocks mentioned.