This Is the Single Most Important Factor in How Wealthy You'll Be at Retirement

Everybody's long-term investment time horizon is really the same. Here are my guiding principles from 46 years of successful investing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Financial planners typically ask people what their investment time period is.

Unless they have a distinct plan to spend a substantial amount, at a predetermined time, the actual answer should be, "It's the rest of my life."

Each of us must decide every day whether to be in stocks, bonds, bank CDs or equivalent short-term Treasuries, corporate bonds, real estate, or gold. Today's world also includes ownership of cryptocurrencies and commodities.

Determining your asset mix is the single most important factor in how wealthy you are likely to end up when retirement rolls around.

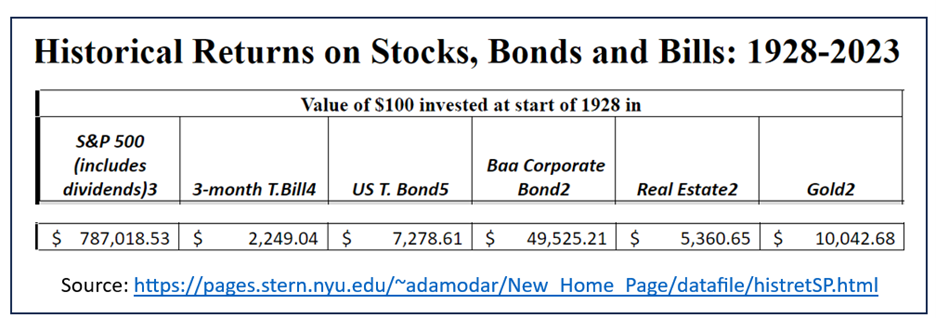

New York University is nice enough to tabulate historical results from the start of 1928 right through all subsequent full years.

They compare total return results for the S&P 500, 3-month T-Bills, 10-year T-Notes, investment-grade corporate paper, real estate, and gold (noted below).

Final values for $1,000 compounded through 2023 confirm that equity investing was far superior to all other choices.

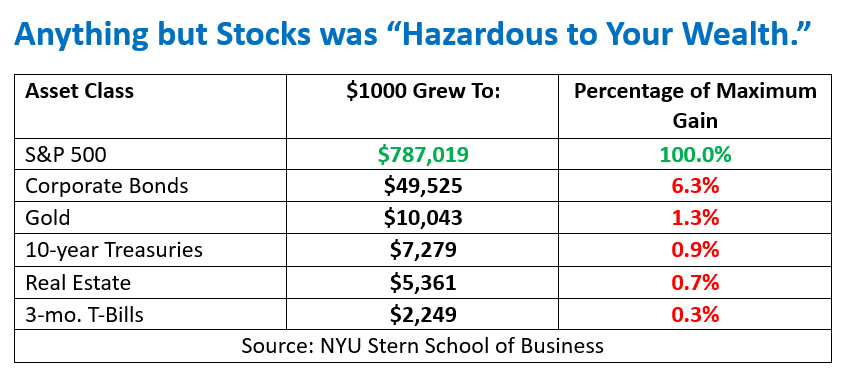

Knowing the facts above makes financial planners' recommendations for holding a fixed percentage of various asset classes look quite silly.

The table below shows how far below "pure equities" each of the other five major asset classes weighed in over the full 95 years.

The second-best asset choice (corporate bonds) returned only 6.3% as much as the top choice. Gold, often touted as a fine inflation hedge, returned only 1.3% as much as being 100% in stocks. Intermediate-term and short-term government paper sandwiched real estate since 1928. All three of those asset classes lagged pure equities by greater than 99%.

Equity returns are typically more volatile than the rest. That is why planners like to diversify. It makes them less likely to be fired by clients angry after years when stocks did poorly.

Making maximum long-term gains requires putting up with inevitable, but scary, selloffs along the road to financial security.

Legendary sales trainer/motivation speaker Brain Tracy said it best decades ago:

"The price for success must always be paid in full, and in advance."

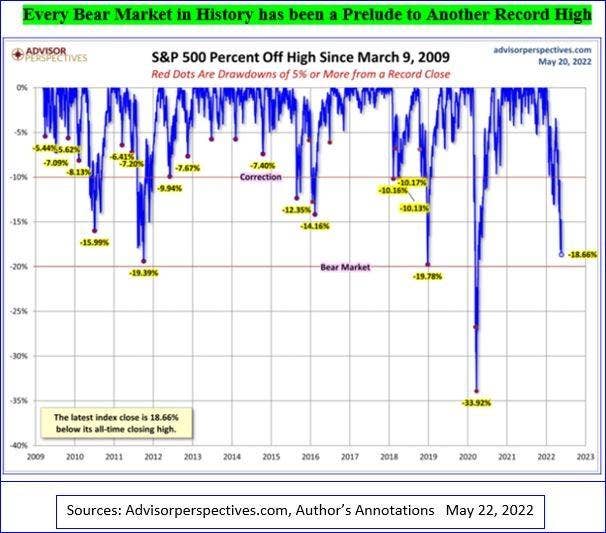

Why fear stock price volatility, though, when every bear market in the history of America has proven to be just a prelude to another all-time high?

The chart below illustrates that point beautifully. It detailed every 5% or greater decline from each previous record from 2009 through May of 2022.

What happened to the S&P 500 index after that? It took a while but, once again, we saw new all-time highs for the broader market in the week ended Jan. 26, 2024.

I have been investing my own money for 46 years (since 1978).

I funded an IRA account as soon as I became eligible in the early 1980s with $2,000 per year, the maximum allowed back then. Since the very beginning, and continuing to the present, I have remained 100% invested in stocks through good markets and bad.

Between appreciation, dividends, and covered call premiums my IRA accounts (traditional and Roth) have grown exponentially over the decades.

There were plenty of bad times along the way and many losing stock picks. None of that prevented both my IRAs from achieving new record highs last week along with the broader market.

Following the same advice I have been offering here on Real Money Pro since 2010 has taken me to financial nirvana.

My portfolios threw off more than enough income to let me live a fine lifestyle while continuing to grow my personal net worth dramatically over time.

That would never have been possible if I had not committed to a 100% equity asset allocation back in the 1970s, and stayed the course through the many ups and downs along the way.

My guiding principles have been these:

1. Invest, rather than "trade."

2. Buy only clearly undervalued shares.

3. Allow enough time for "the market" to change its opinion (typically at least 12-24 months).

4. Be a seller, not a buyer, of options.

5. Never be afraid to buy low if a company's fundamentals remain healthy.

6. Averaging down is often a great way to make outsized gains.

7. Do not hold on to losers "hoping to get even" if fundamentals deteriorate badly.

8. Avoid fixed income altogether. After inflation and taxes they almost never produce good results.

9. Keep enough liquid cash in reserve to pay bills and taxes for at least a year. That prevents panic selling at bad prices when markets get tough.

I remain fully invested in stocks in retirement accounts other than for short periods between selling and putting money back to work. I own only individual stocks, not index funds or ETFs. I rarely buy options except as closing transactions.