Would You Buy an Investment That Guarantees No Profit for at Least 10 Years?

If someone tries to sell you an annuity ask them to explain 'why?'

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Would you buy an investment where it takes around 10 to 17 years to recoup what you originally put in?

Amazingly, millions of people are doing that every single year.

They do that via purchase of annuities, which are often pushed hard by financial planners as a good way to "avoid outliving your money."

Owning annuities does, indeed, insure that you will always have a monthly income. Unfortunately, that promise comes at a huge cost to the purchaser. It also comes with an outsized commission to the selling agent and his company.

A typical percentage commission on an annuity runs 6% of the principal amount committed. On a $1 million annuity purchase that equals $60,000. That is a huge incentive for people selling annuities, regardless of the facts I will detail next.

That explains why you may be receiving so many invitations for educational seminars offering free meals to attendees. The cost of those tasty dinners is usually sitting through pitches on why you should consider buying annuities.

America's Social Security department provided the following life expectancies for men and women who have already reached age 65.

The average 65-year-old man will live to just over 84 years of age. Women, at 65, can expect to live until age 86.6. I'll be referring back to those numbers shortly.

Annuities are typically marketed as giving owners "Higher than CD rate income." That is usually true but fails to mention the major differences between FDIC-insured CDs and annuities.

Certificates of deposit merely pay interest on your amount invested. After the predetermined time, you will have collected all interest due plus get a 100% return of your principal assuming you did not exceed the $250,000 FDIC limit per person, per bank.

A 5% CD, then, would deliver back $105,000 after one year (ignoring any compounding effect), on $100,000.

Annuities are not FDIC insured. They are merely obligations of the issuing entity, an insurance company.

Once you buy an annuity you have forfeited your principal to the insurance company. Your original deposit amount is no longer "yours." All you have in return is the promise of a set monthly income for life.

If you fail to add (expensive) riders to protect against inflation or to guarantee at least a minimum number of years of payment...

- Your principle is gone from your estate.

- You may have received well below the initial amount paid.

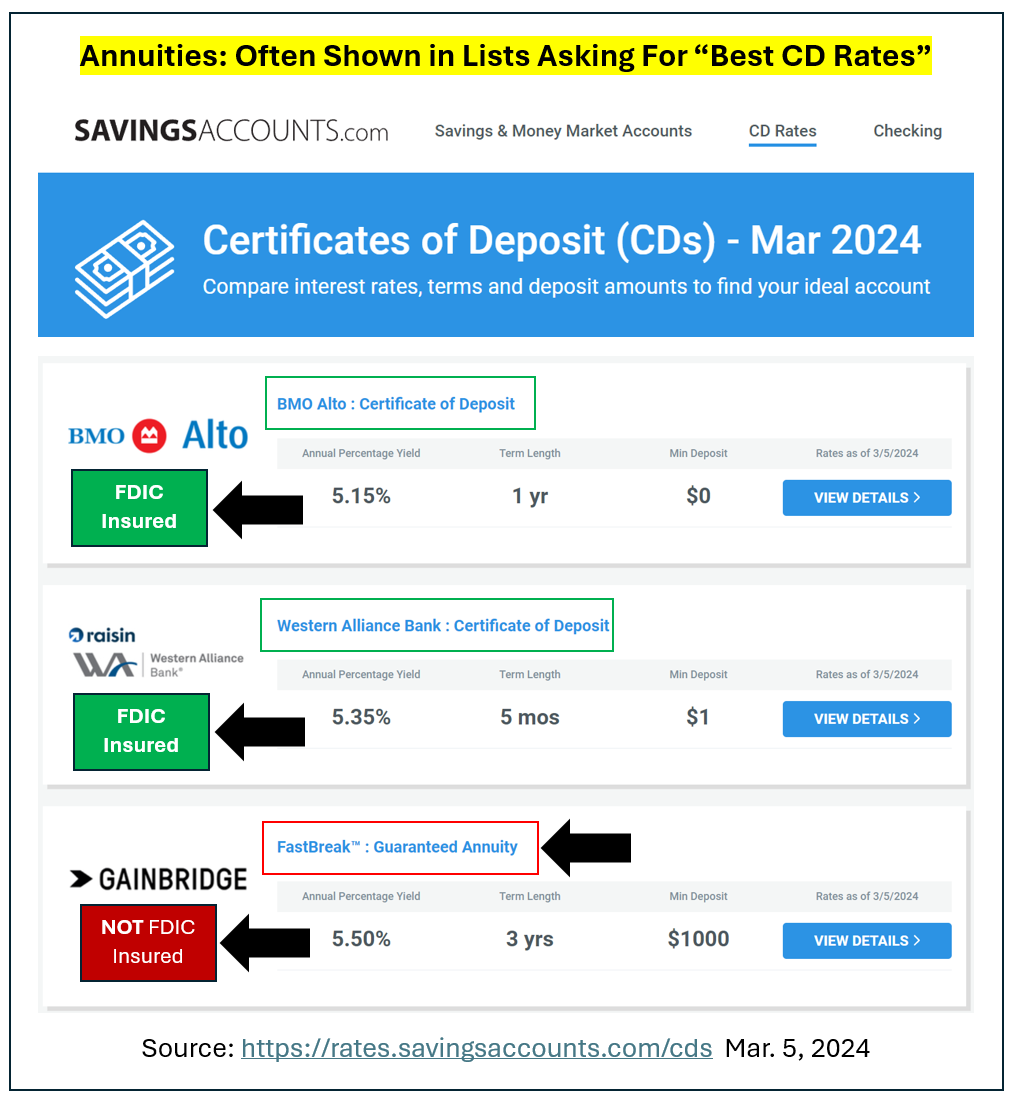

Selling agents, and even online search engines like the one shown below, often lump annuity rates of payment alongside bank CD rates. Uninformed investors, who fail to know the differences between the two instruments, could easily think the annuity is the better buy.

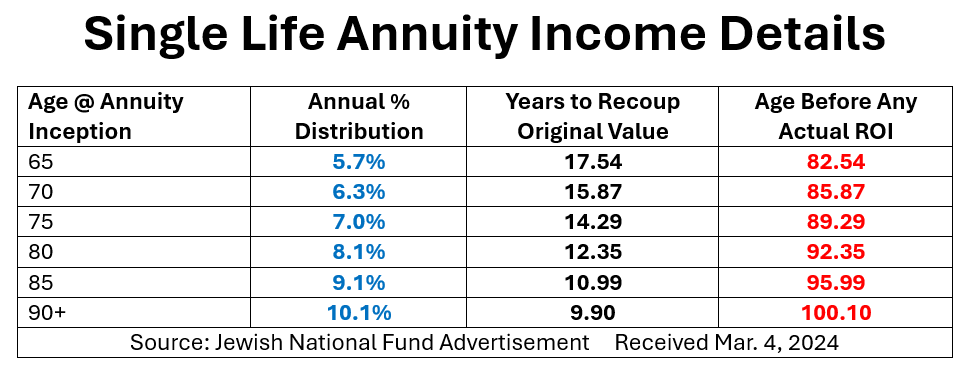

I got a postcard-based ad recently offering the following Single-Life Annuity.

Benefits listed included:

- Provides dependable, guaranteed income for life.

- Supplements your retirement.

- Get started with as little as $5,000.

Let's simply decode the propositions being offered, depending on the age of the annuitant.

Now that you know how annuities function, we can determine how long it will take to simply recoup what you paid up front to buy them.

According to the terms in the advertisement, it would take 17.54 years for a 65-year-old to get back what they paid. If the purchaser was a man he would be more than 82.5 years old before seeing the first penny of actual profit.

Social Security says that more than half of those men would already have died before even getting back their original purchase price. What a great deal.

Older people of both sexes would have to live to past their average life expectancies before seeing any return on investment.

Giving up your hard-earned lifetime savings to, perhaps, start earning something only after 82.5 to 100.1-years of age is a statistically insane bet to make. You could have locked in almost the same income initially via owning bank CDs without any waiting period and without giving up your principal.

In the end annuities almost always pay less out than comparable non-annuity choices while hurting your own and your descendants' financial security.

All those so-called government consumer advocacy agencies have caved in to insurance industry lobbyists in now allowing them to be bought inside tax-sheltered accounts. One of the most basic principles in sound financial planning has always been "never put tax-sheltered investments inside already tax-sheltered accounts like IRAs, 401ks, and Keogh plans."

If someone tries to sell you an annuity ask them to explain "why?"

Caveat emptor.

Paul Price was insurance licensed years ago when he was employed as a broker. He never sold annuities.