Skipping the Light Fandango

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

And a little (divine) exit music:

Position: None

BY Doug Kass · Jul 8, 2026, 4:45 PM EDT

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

And a little (divine) exit music:

Position: None

BY Doug Kass · Jul 8, 2026, 4:45 PM EDT

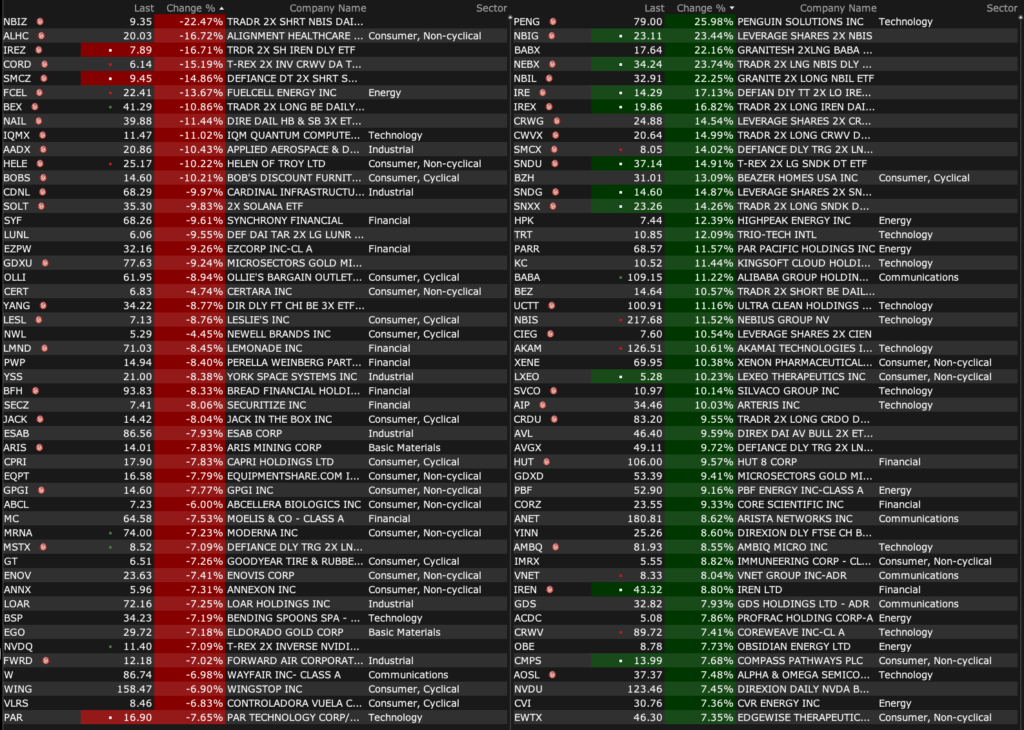

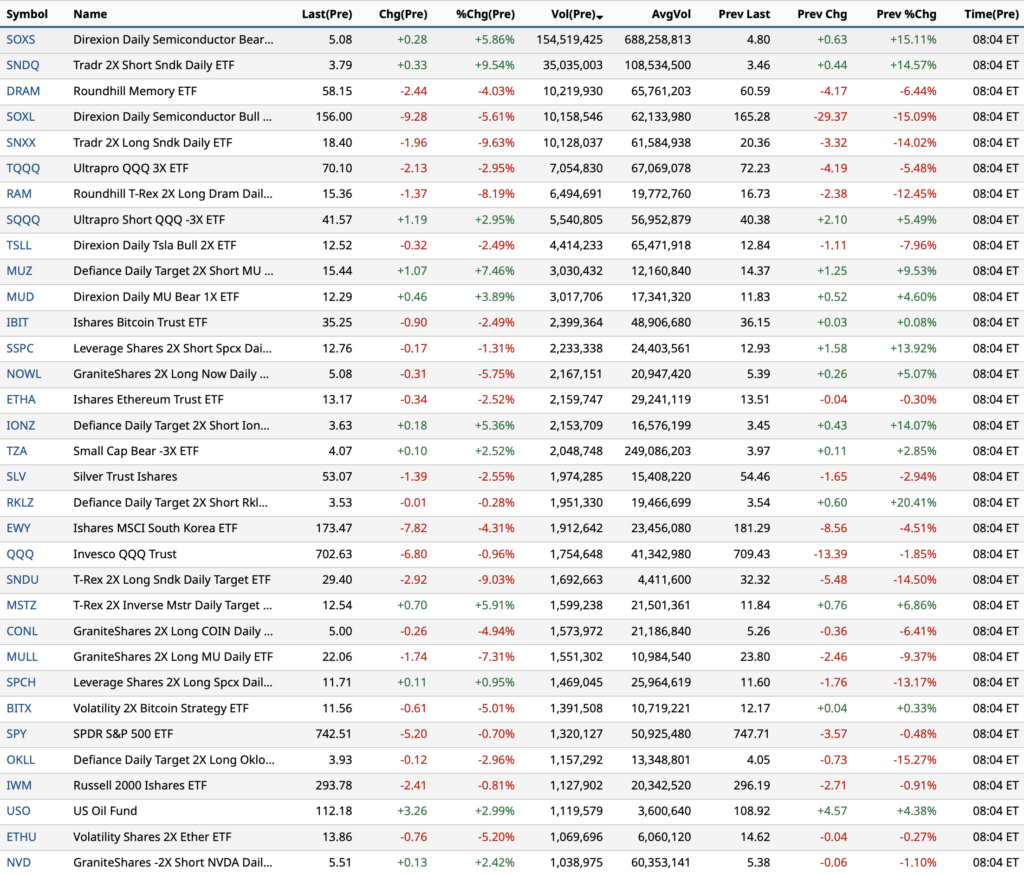

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jul 8, 2026, 4:35 PM EDT

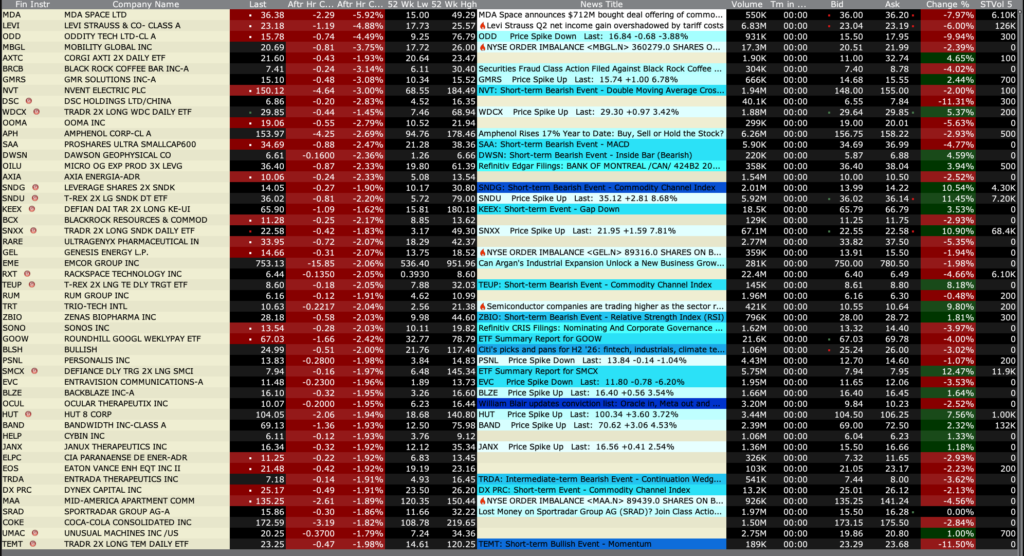

Closing Volume

– NYSE volume 13% below its one-month average

– NASDAQ volume 30% below its one-month average;

– VIX index: up 4.09% to 16.79

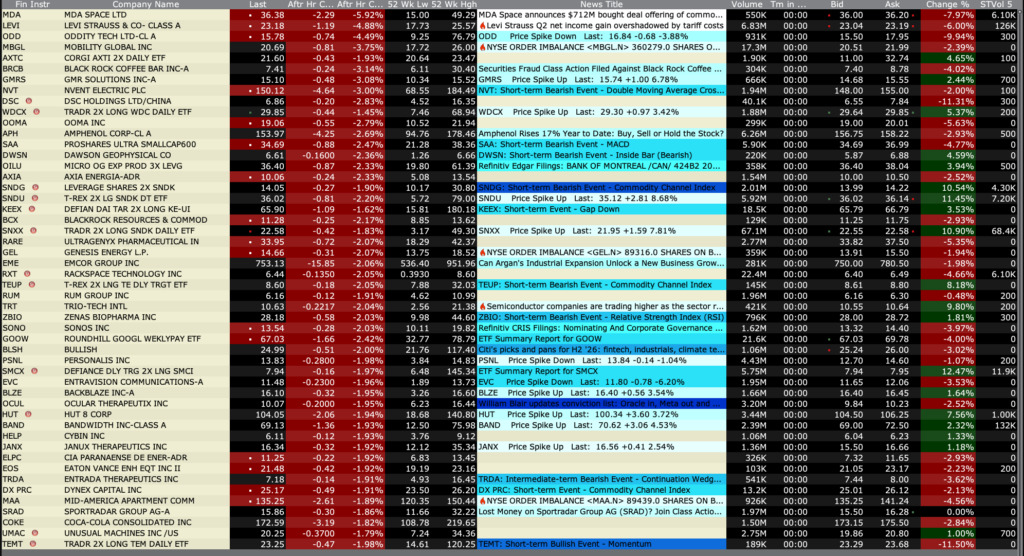

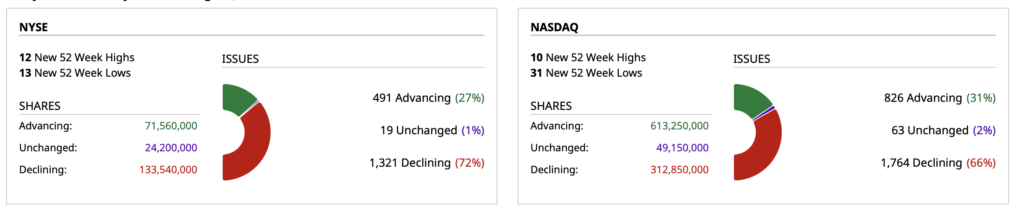

Breadth

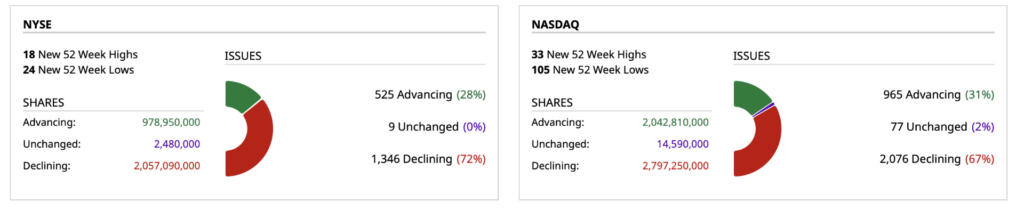

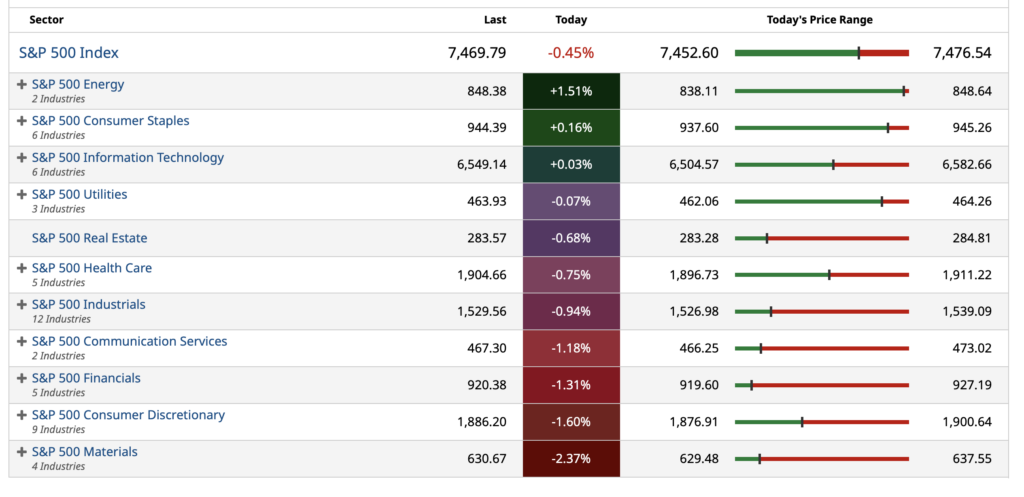

S&P 500 Sectors

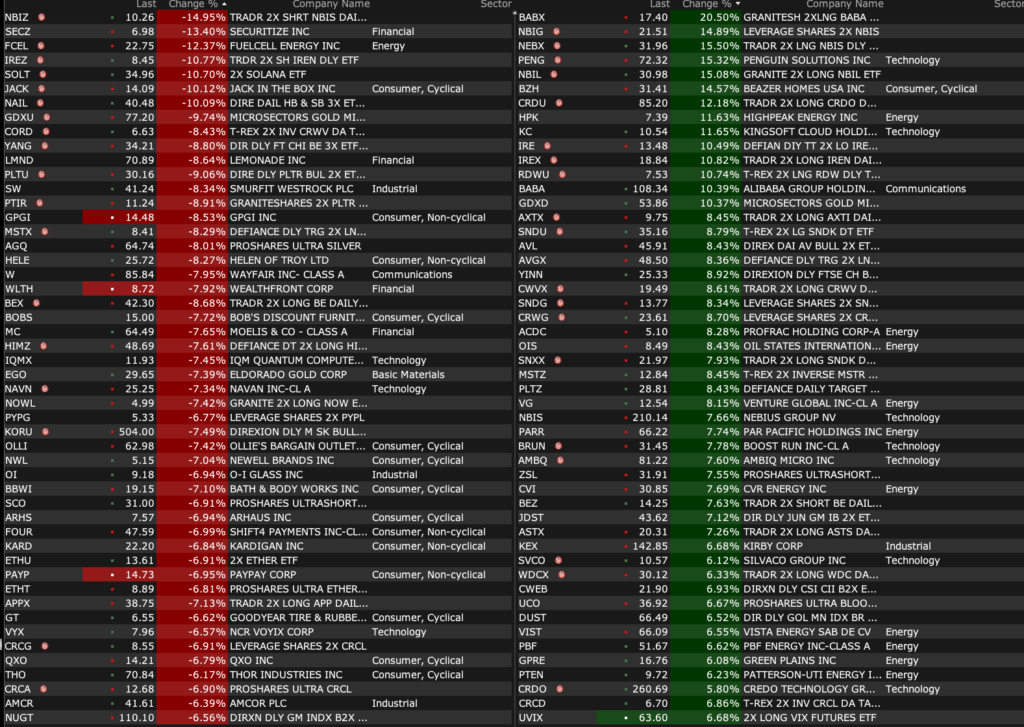

% Movers

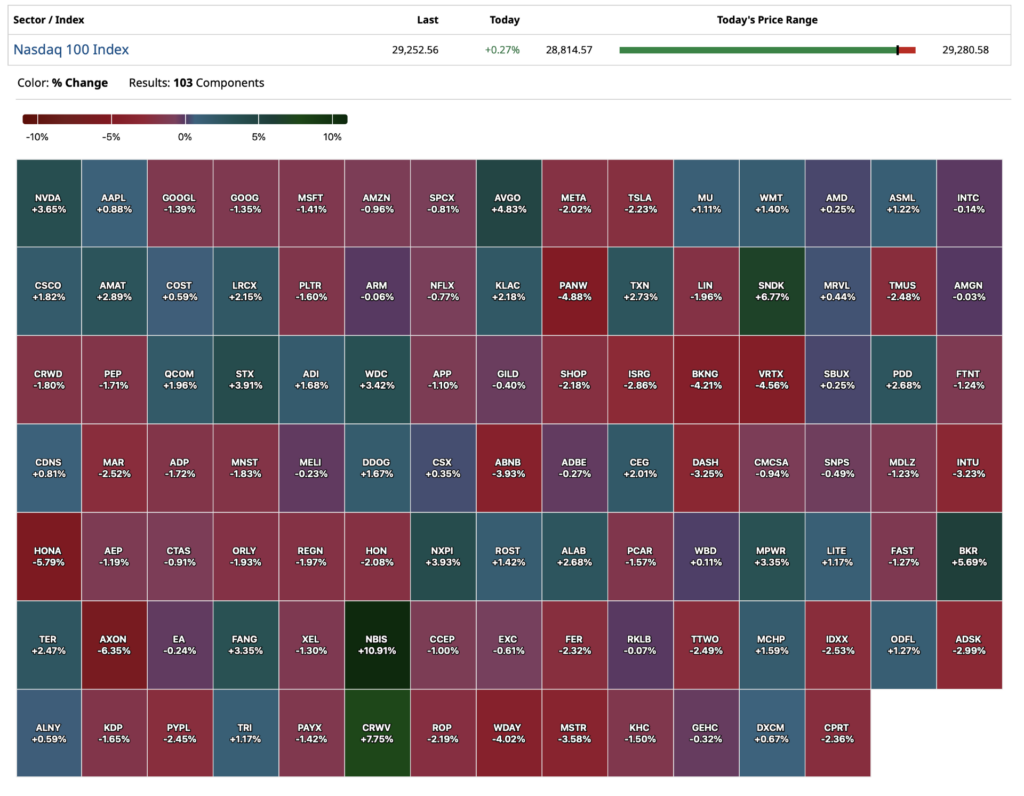

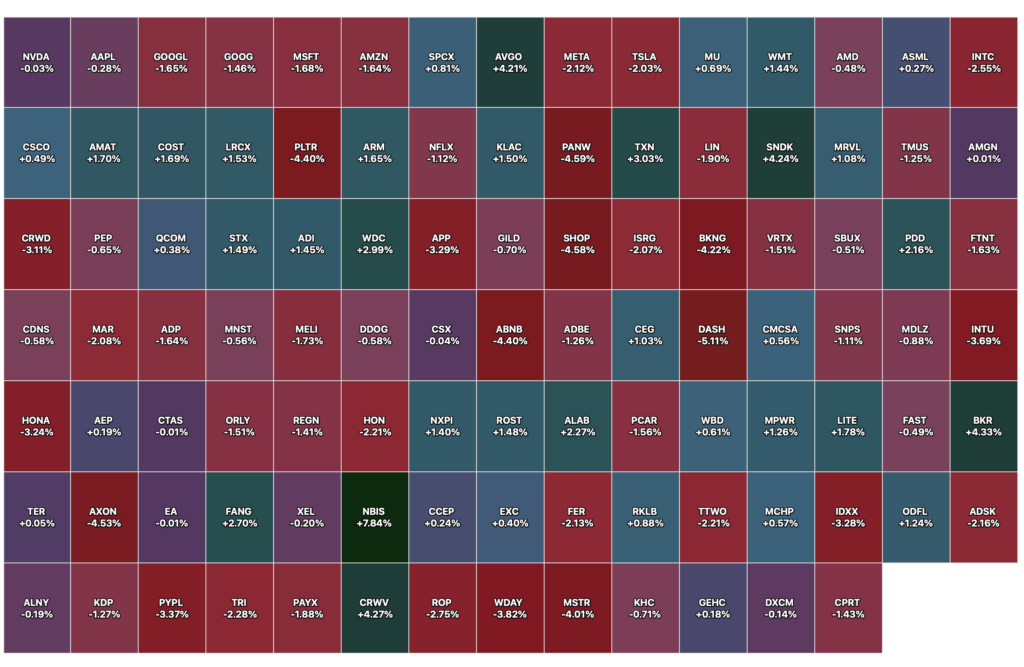

Nasdaq 100 Heat Map

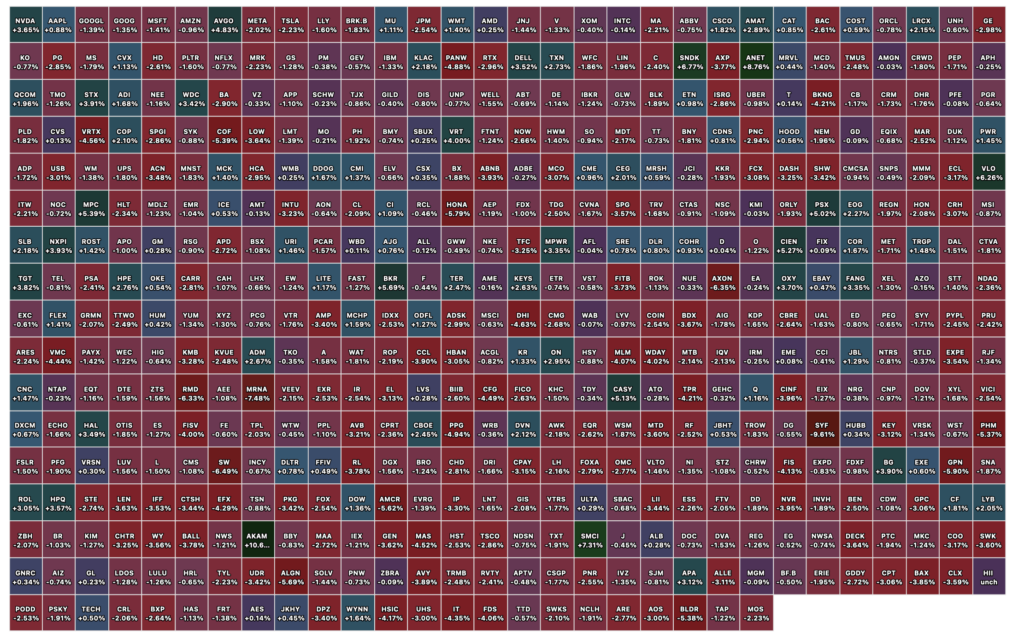

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jul 8, 2026, 4:26 PM EDT

Randy

Position: None

BY Doug Kass · Jul 8, 2026, 3:30 PM EDT

Position: None

BY Doug Kass · Jul 8, 2026, 3:20 PM EDT

From Peter Boockvar:

No more ‘forward guidance’ but still plenty of opinions

I know there is a rethink going on about the use of ‘forward guidance’ but we are still getting a form of it in terms of hearing what Fed members are thinking and the minutes certainly gave us plenty of their thoughts. My bottom line is this, there was a lot of commentary on the inflation picture and clearly a main focus of theirs again. So, we’ll have to see if they hike rates, as the market is currently pricing in a 100% chance of one hike and a 48% chance of a second by year end, but for now there is no chance they are thinking about a cut.

Yields are little changed in response.

I’ll give a bunch of quotes here but try to focus mostly on those that mention ‘several’ or ‘many’ or ‘majority’ when referring to a particular opinion/point.

“Several participants commented that price pressures had become more broad based, with a large share of goods and services—including transportation, airfares, petrochemical products, and agricultural inputs—experiencing substantial increases. Several participants remarked that services price inflation excluding housing had declined little and remained high.”

“The majority of participants commented that most measures of medium- and longer-term inflation expectations remained at levels consistent with the Committee’s 2 percent objective.”

“Participants anticipated that inflation would remain elevated in the near term and then begin to decline as the effects of tariffs and energy price increases wane and other supply disruptions related to the closure of the Strait of Hormuz diminish. Participants judged that the risks to the inflation outlook were still tilted to the upside.”

“Many participants noted that elevated commodity prices and supply disruptions could persist longer than currently anticipated. Several participants reported that their business contacts were facing notable cost pressures.”

“Several participants noted, however, that firms in their Districts reported that they had been cautious about increasing prices, citing concerns that higher prices could reduce demand or their market shares. Many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity. Most participants remarked that growth in economic activity that exceeded that of potential output, owing in part to strong AI business investment, could contribute to more persistent inflationary pressures.”

“The majority of participants highlighted the possibility that, after several years of inflation above 2 percent, continued elevated inflation rates could begin to affect inflation expectations and wage- and price-setting decisions.”

On the labor market, “Several participants observed that other labor market indicators, such as job openings, initial unemployment insurance claims, and layoffs had remained stable in recent months and that such data pointed to a balanced labor market. Several participants noted, however, that declines in the job-finding rate and certain survey measures of job availability reflected a labor market with relatively low dynamism. Many participants remarked that the labor market was not currently a source of inflationary pressures, or that nominal wage growth remained consistent with inflation moving toward 2 percent.”

And, “several participants noted that the solid payroll employment data in recent months could signal increased labor market momentum. Several participants cited, however, the possibility that uncertainty related to geopolitical developments or the broader economic outlook could lead firms to reduce hiring or begin implementing layoffs.”

The Fed’s bottom line on the economy, “Participants generally expected solid real GDP growth to continue throughout the remainder of the year and pointed to several factors likely to support continued expansion, including ongoing AI-related investment, household spending, and fiscal policy.”

Position: None

BY Doug Kass · Jul 8, 2026, 3:10 PM EDT

BY Doug Kass · Jul 8, 2026, 2:45 PM EDT

* And fading it…

I don’t own and am currently short (and have been recently short C, JPM, GS, MS, UBER, NFLX, homebuilders, etc.) some of the most consensus sectors.

I am long some of the most non-consensus sectors.

Consensus Longs:

* Memory: SanDisk (SNDK), Micron (MU), Intel (INTC), AMD (AMD), Applied Materials (AMAT) (“it’s different this time”)

* Value Tech: Adobe (ADBE), Oracle (ORCL), ServiceNow (NOW) and Nvidia (NVDA)

* Tech With Biggest Moat: Apple (AAPL)

* Value Industrial: Caterpillar (CAT)

* Best Overall Value: Homebuilders

* Streaming: Netflix (NFLX)

* Autonomous: Uber (UBER)

* Entertainment: Disney (DIS)

* Financials: JPMorgan (JPM), Citigroup (C), Goldman Sachs (GS), Morgan Stanley (MS)

* Frontier Exposure “For The Long Haul”: SpaceX (SPCX)

Non-Consensus Longs:

* Cannabis: MSOS, VRNOD, TRLV, GTBIF, GLAS

* Private Equity: Apollo (APO), Blackstone (BX), KKR (KKR)

* Consumer Staples: Kimberly-Clark (KMB), PepsiCo (PEP), Procter & Gamble (PG)

Positions:

Long MSOS (L), VRNOD (S), TRLV (S), GTIBF (S), GLAS (S), APO (S), BX (S), KKR (S), KMB (S), PEP (S), PG (S)

Short SPCX (VS), SNDK (VS), MU (VS), INTC (VS), AMAT (VS), AMD (VS), CAT (VS)

BY Doug Kass · Jul 8, 2026, 2:30 PM EDT

From Peter Boockvar:

Very good 10 yr note auction

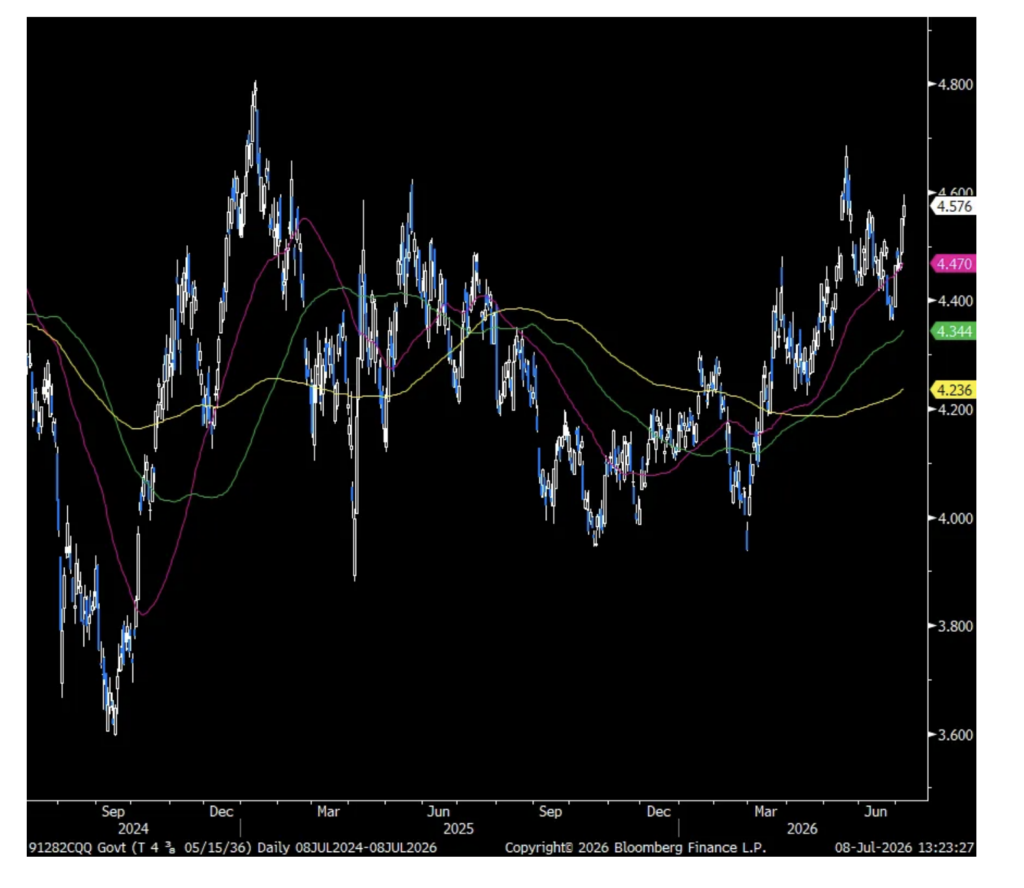

The 10 yr note auction was very good. The yield of 4.580% was just below the when issued pricing of 4.586%. The bid to cover of 2.59 was above the previous one year average of 2.49 and the best since last September. Also of note, dealers got stuck with the least amount of a 10 year auction since January with direct and indirect bidders taking the most since then.

Bottom line, while auction results really only have an impact on the market the day of the issuance, it’s very likely that buyers took advantage of a 10 yr yield that is nearing its Middle East conflict high and not far from the highest since January 2025.

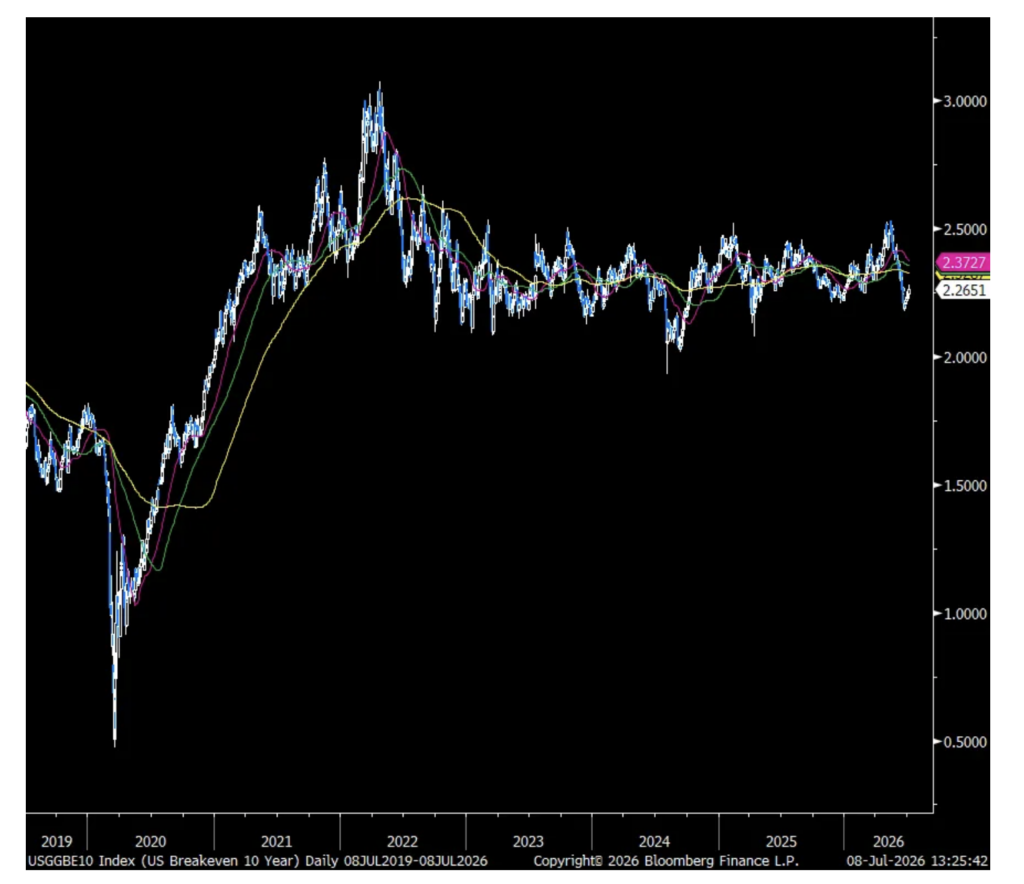

With respect to the reaction in the TIPS market to today’s rise in oil prices, the 10 yr inflation breakeven is unchanged at 2.26% and the 5 yr is flat as well at 2.32%. It’s the shorter end that is responding more with the 2 yr breakeven up 6 bps to 2.10%

10 yr Yield

10 yr Inflation Breakeven

Position: None

BY Doug Kass · Jul 8, 2026, 1:55 PM EDT

Position: None

BY Doug Kass · Jul 8, 2026, 1:40 PM EDT

* On Apple’s margins and Micron’s average price realizations… you can’t have it both ways!

Wait, the same panelists who own Micron (MU) because “it’s different this time” are now arguing that the pressure from Micron’s high memory prices will be fleeting (so Apple’s (AAPL) margins will mean revert higher as memory prices “normalize”)?

That doesn’t compute and the arguments are not consistent.

Position: Short MU (VS)

BY Doug Kass · Jul 8, 2026, 12:45 PM EDT

Wolf Street howls about the ECB.

Position: None

BY Doug Kass · Jul 8, 2026, 12:35 PM EDT

See this tweet:

But, more importantly, the subtweet under it:

I think that is the leading indicator. Although I would modify the subtweet a bit.

This also means the revenue growth is flattening. The spike we had that really kicked off this last rally was artificial. It was unsustainable tokenmaxxing (and apparently Anthropic also had a big 1x pull in of revenue in Q3, if I remember correctly). The consumer quickly found out they were doing the opposite of gaining productivity, they were costing themselves more money than the humans they had.

So it has been stopped. Then the biz also started shifting to China/Open Source as well. A double whammy.

No wonder SpaceX (SPCX) and Meta (META) are selling excess capacity all of the sudden… and why Blackstone (BX) is rumored to be stopping data center projects, for example.

Position: Long BX (S); Short SPCX (VS)

BY Doug Kass · Jul 8, 2026, 12:15 PM EDT

BY Doug Kass · Jul 8, 2026, 11:59 AM EDT

I have covered much of my GRNY at $27.30 and JOET at $45.01 shorts now.

I plan to reshort on strength.

Position: Short GRNY (VS) JOET (VS)

BY Doug Kass · Jul 8, 2026, 11:47 AM EDT

– NYSE volume 22% below its one-month average;

– Nasdaq volume 38% below its one-month average;

– VIX index: up 10.73% to 17.86

Positions: None

BY Doug Kass · Jul 8, 2026, 11:30 AM EDT

FWIW This sort of daily action suggests a “market structure event” might be closer at hand.

Integer like movements in a casino backdrop usually doesn’t result in a benign outcome.

Positions: none.

BY Doug Kass · Jul 8, 2026, 11:20 AM EDT

BY Doug Kass · Jul 8, 2026, 11:10 AM EDT

* From my good pal and fellow employee at Putnam (in the 1970s!) …

Although history doesn’t repeat and doesn’t always even rhyme, this nevertheless evoked the memory of when, at the height of the Nifty Fifty growth stock era in 1972-73 John Neff, one of the greatest value investors aver, came within one quarter of being fired because of his poor performance:

Terry Smith of Fundsmith revealed plans to incorporate momentum factors into the investment strategy and reduce buying quality companies during temporary setbacks. The letter highlights recent sales such as Intuit and potential interest in high-momentum stocks like GE Vernova.

Positions: None

BY Doug Kass · Jul 8, 2026, 11:00 AM EDT

Chart from 9:34 a.m. ET

Positions: None.

BY Doug Kass · Jul 8, 2026, 10:45 AM EDT

Positions: None.

BY Doug Kass · Jul 8, 2026, 10:35 AM EDT

I bought an odd lot of MSOX (MSOX) (not my favorite ETF, as leveraged!) at $2.66.

The message of the small buy is that the reward vs. risk in cannabis has grown more compelling over the last few days.

This is a trading rental (all levered ETFs are) and I could be out at any time.

Positions: MSOX VS MSOS L Indiivudal Cannabis Equities

BY Doug Kass · Jul 8, 2026, 10:10 AM EDT

BY Doug Kass · Jul 8, 2026, 10:10 AM EDT

I have covered my C (C) $138.88 (-$2) and JPM (JPM) $333.95 (-$5) shorts for a small profit this morning.

I plan to reshort on any strength.

Positions: None.

BY Doug Kass · Jul 8, 2026, 10:07 AM EDT

From Peter Boockvar:

Oil prices are doing what’s expected in response to the news while global bond yields continue higher even with oil prices well off their war highs and a price I mentioned Monday I found most interesting. The US 10 yr yield is now just 10 bps from the May high while the price of oil is still down about 25% from its close high (intraday was about $120).

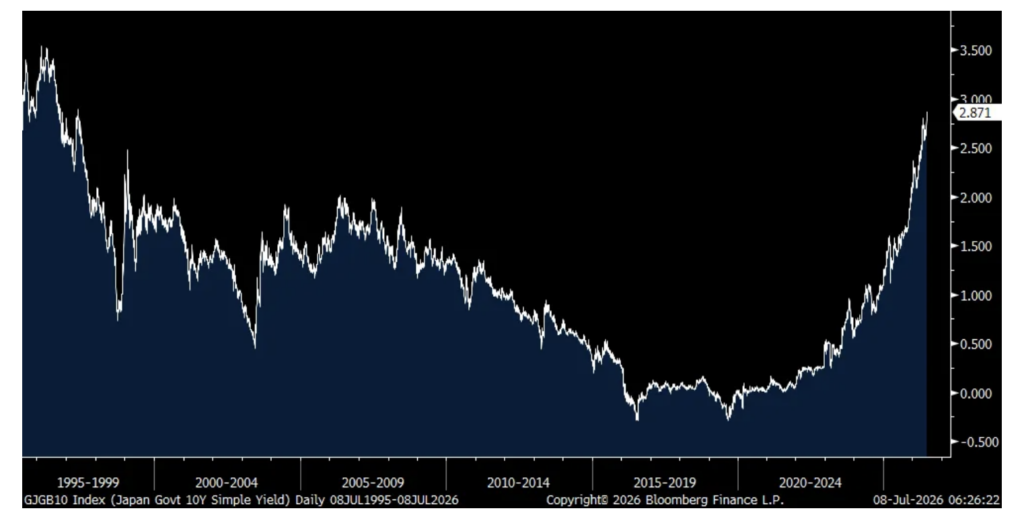

I’ll emphasize again that the move up in developed market bond yields continues to be global as debts and deficits now matter. The bond bear market continues on. The 10 yr JGB yield closed at a fresh 29 year high at 2.87%. The 10 yr French oat yield has broken out to a 17 yr high at 3.90% up 11 bps today. The 10 yr UK gilt yield is up 10 bps to 4.95% but below its May peak of 5.17%. The German 10 yr yield is up 8 bps to 3.07% though about 12 bps from a 15 yr high.

Oil in orange, US 10 yr yield in white

JGB 10 yr yield

French 10 yr yield

One of my bull cases for commodities has been the expected stock piling I expect to see of a variety of things. A story I read on Bloomberg this morning, “The US Department of Defense is buying lithium for its strategic stockpiles as the nation ramps up efforts to reduce supply risks for critical minerals. The Defense Logistics Agency is seeking offers for almost 36 million pounds, about 16,000 tons, of battery grade lithium carbonate over the next five years in a contract worth as much as $300 million, according to a tender document published on a US government website dated July 2.”

Yesterday, I read this on Reuters, “Germany’s Economy Ministry is drawing up plans for a state-owned strategic gas reserve to be used in emergencies…The reserve would hold around 24 terawatt-hours (TWh) of gas, equivalent to just under 10% of Germany’s total gas storage capacity, and would be financed through a levy on gas consumers, the ministry said. The reserve is intended to protect against extreme situation, such as sabotage of critical energy infrastructure or a severe global gas storage.”

I expect to hear a lot more of these type stories in the months to come.

In the June NY Fed Consumer Expectations Survey seen yesterday, one yr inflation expectations rose to 3.7% from 3.5% even as expectations for gasoline prices fell to the lowest since 2022. Higher expectations for health care costs and rents offset the gas decline, along with a lower outlook for food and college tuition costs.

Otherwise from the NY Fed, “Labor market expectations improved, with job-finding expectations increasing and job-loss expectations and expectations about the unemployment rate declining. Spending growth expectations were unchanged. Respondents were more optimistic about their future household financial situations, while expectations about future credit availability deteriorated slightly.”

Of note, and another example of how stock market sentiment follows price, “The mean perceived probability that U.S. stock prices will be higher 12 months from now increased by 2.9 percentage points to 40.9%, the highest level of the series since April 2021.”

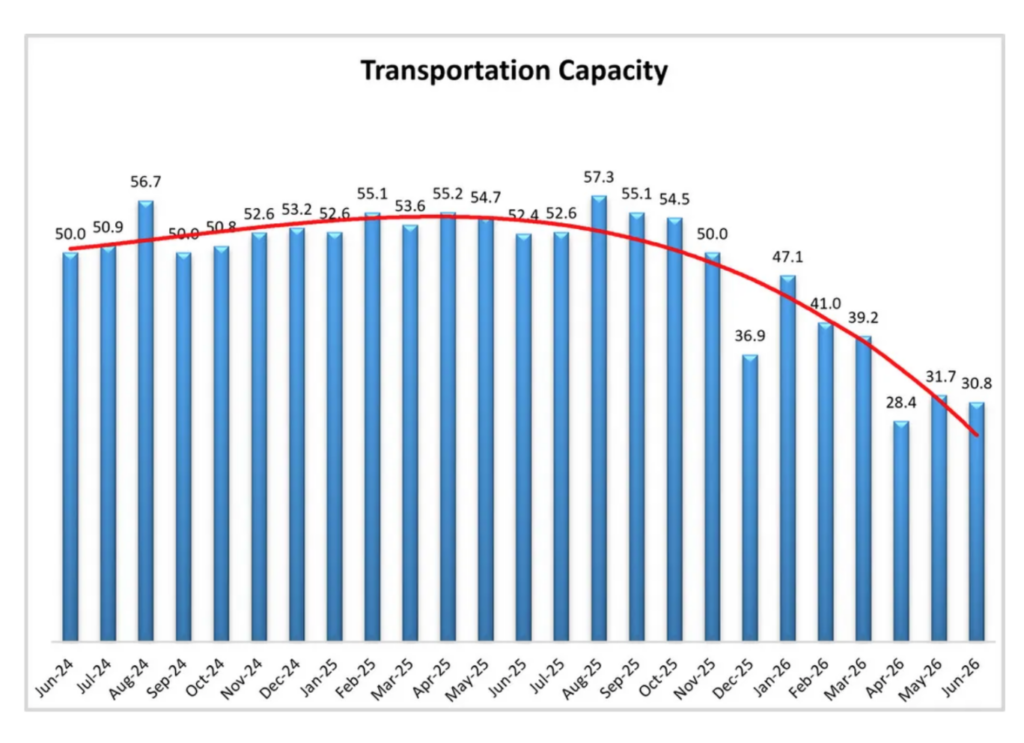

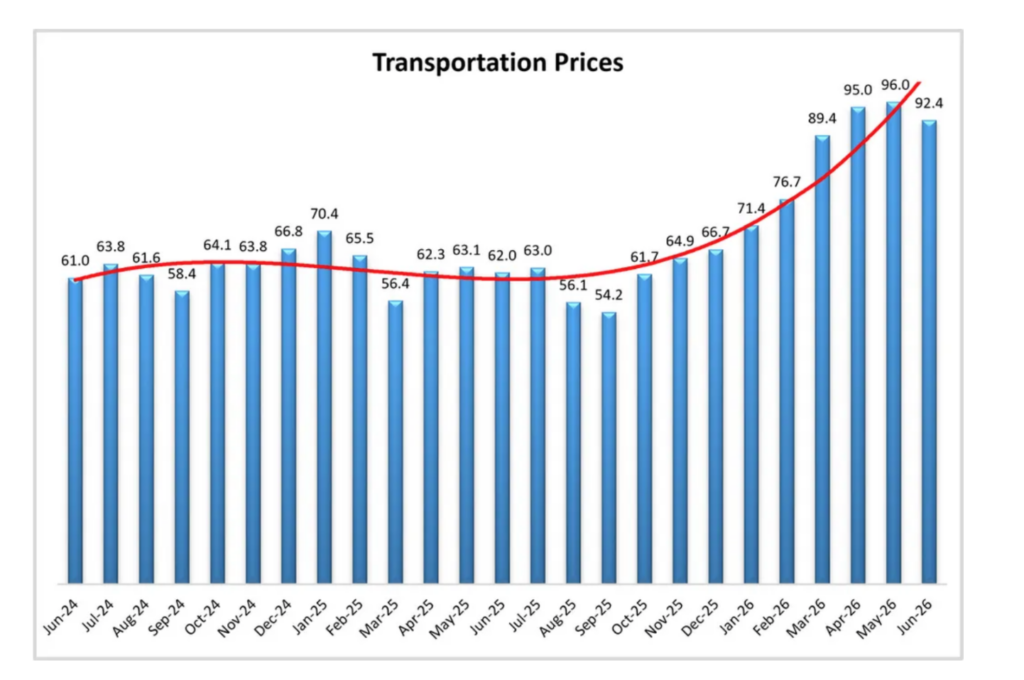

The June Logistics Managers’ Index came out yesterday and rose m/o/m driven by its inventory component. They said “This level of inventory expansion is a flip from what we have seen for most of 2026. The push from retailers is likely representative of two factors: 1)In spite of inflation, consumer spending has held through the first half of the year, giving retailers confidence in bringing forward goods for the second half of the year; 2)tariffs may increase in later July, so some of what we’re seeing is a pull-forward ahead of peak season.”

I think some of the pull forward is also due to companies that want to get ahead of any supply issues and/or other price increases.

Transportation prices did slip a touch after the May read, which was a record in this index as capacity continues to come out of the market.

Kura Sushi is trading lower pre market after they missed estimates, both top and bottom line, and slightly lowered their full year guidance. They said this of note;

Comps fell .4% y/o/y “with negative 5.1% of traffic, offset by positive 4.7% in price and mix. Effective pricing for the quarter was 4.5%.”

“We were certainly disappointed that traffic came in negatively…but we believe that this is largely due to elevated gas prices…As the gas prices have eased, we’re beginning to see a little bit of benefit as we’ve entered Q4, but those benefits are partially offset by how popular the World Cup is, and so the guidance that we’re providing for the revenue contemplates the Q3 and Q4 macro background as well as the construction delays” of new restaurants.

Influenced by the holiday, purchase applications fell .6% w/o/w and little changed over the past 3 weeks, ahead of what will be another rise in mortgage rates if the move in the US 10 yr yield holds. Refi’s were down by 4.1% w/o/w.

The Reserve Bank of New Zealand raised its cash rate to 2.50% as expected. New Zealand is a small country as we know with a modestly sized economy but it is fully developed and why I pay attention to what their central bank does. And, they hinted at further increases, “With inflation still above target and economic activity expected to strengthen, some further reduction in monetary stimulus is likely to be required.”

For perspective, before they started hiking in 2021, their cash rate was .25%. It went as high as 5.5% in 2023 and down to 2.25% early this year.

Positions: None.

BY Doug Kass · Jul 8, 2026, 9:50 AM EDT

BY Doug Kass · Jul 8, 2026, 9:20 AM EDT

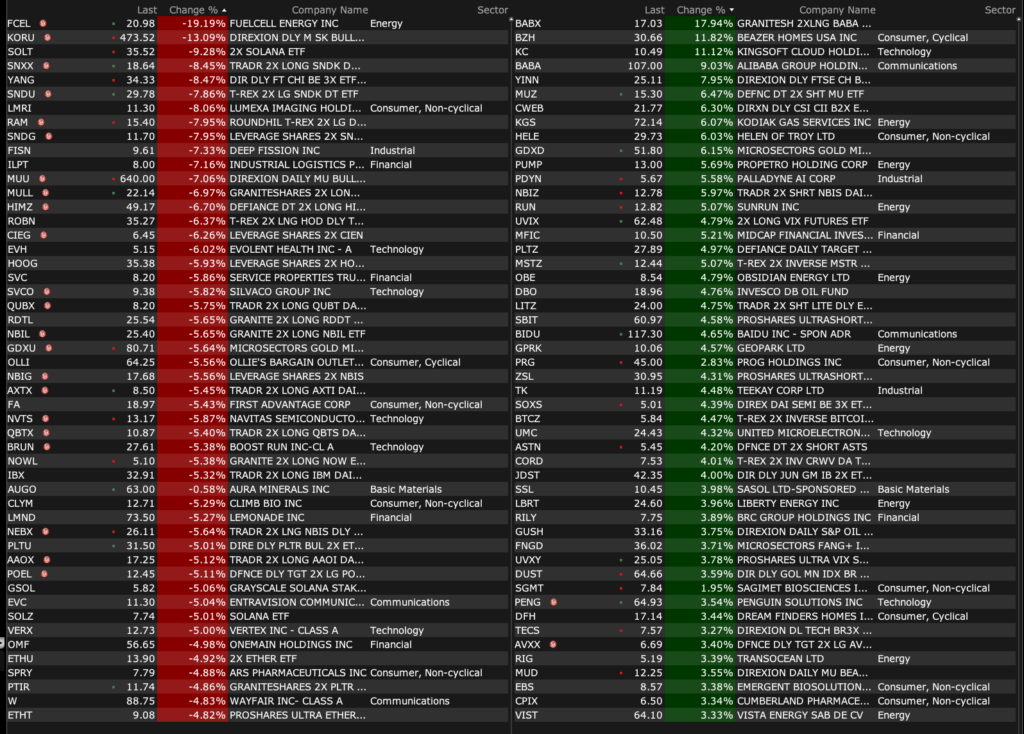

-BZH +12% (DFH raises Beazer acquisition proposal by ~24% to $32.00/shr cash)

-BABA +8.5% (reportedly Alibaba’s Q1 FY27 financial report previewed to investors showed that overall e-commerce business (China e-commerce + AIDC) profits have resumed growth)

-RUN +5.9% (launches distributed AI compute pilot program)

-PDYN +4.7% (prelim Q2 revenue, color)

-MTZ +3.2% (acquires electrical contractor The Superior Group for $1.65B in stock and cash)

-TGT +2.8% (bounce off prior week weakness)

-RKLB +2.1% (higher in sympathy with Blue Origin announcing it is raising outside capital for first time)

-FCEL -19% (prices upsized $225M (vs. $200M prior) public offering of 10.7M shares at $21.00/shr)

-LMND -4.9% (Morgan Stanley Cuts LMND to Equal Weight from Overweight, price target: $75)

-NVTS -4.9% (disputes Wolfspeed patent infringement complaint filed in Delaware)

-RIVN -4.8% (prices 75M-share offering at $15.50/shr for ~$1.2B gross proceeds)

-OLLI -4.5% (JPMorgan Chase and Co Cuts OLLI to Neutral from Overweight, price target: $70)

-SNDK -4.5% (downside momentum)

-BBWI -4.1% (Goldman Sachs Cuts BBWI to Sell from Neutral, price target: $19 from $23)

-MU -3.7% (downside momentum)

-AAL -2.6% (airline weakness following ramped up tensions with Iran, oil prices higher)

-UAL -2.2% (airline weakness following ramped up tensions with Iran, oil prices higher)

BY Doug Kass · Jul 8, 2026, 9:15 AM EDT

Cannabis equities, along with the more the speculative corners of the market, have fallen modestly in the last two weeks, despite a slew of positive reports on (the inevitability of) rescheduling.

My strategy has been to add to MSOS (MSOS) and to individual names daily.

Should the space continue to drop in value I could foresee taking my industry exposure to the highest level (in percentage terms) than at any time in the last five years – given my assessment of reward vs. risk.

Recognize that this is a speculative space and your risk appetite should govern your exposure.

Positions: Long MSOS et al

BY Doug Kass · Jul 8, 2026, 9:05 AM EDT

Positions: None.

BY Doug Kass · Jul 8, 2026, 8:55 AM EDT

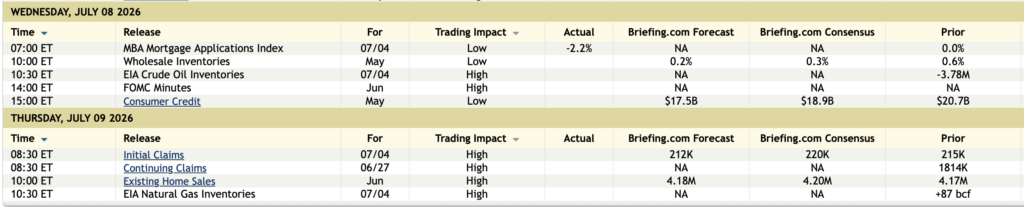

11:00 a.m.: Treasury hosts a $72B 17-Week Bill Auction;

11:00 a.m.: Treasury buyback announcement (liq support);

1:00 a.m.: Treasury hosts a $39B 10-Year Note Auction;

Positions: None.

BY Doug Kass · Jul 8, 2026, 8:35 AM EDT

S&P futures are now -40 handles (an improvement of +30 handles) and I have sold my trading long rentals for a quick and profitable trade:

* SPY (SPY) $743.47

* QQQ (QQQ) $704.23

From earlier:

Index Trading Long Rentals (720AM)

* SPY $740.96

* QQQ $700.16

Positions: None

BY Doug Kass · Jul 8, 2026, 8:22 AM EDT

Positions: None.

BY Doug Kass · Jul 8, 2026, 8:20 AM EDT

From Comments Section:

D

Dougie Kass

35m ago

Index Trading Long Rentals (720AM) * SPY $740.96 * QQQ $700.16

Positions: Long SPY VS QQQ VS

BY Doug Kass · Jul 8, 2026, 8:05 AM EDT

* What the hell happened to the Delta I used to know?

“Was it over when the Germans bombed Pearl Harbor?”

– Bluto, Animal House

In taking a trading long rental I am relying on the past statements of policy by President Trump.

It’s not over until he says it is over.

Where’s the guts? This could be greatest night of our lives.

Not me, I am not going to take this.

This could be just a futile and stupid trade, but we are the guys to do it.

Let’s do it.

Stay opportunistic and trade dispassionately.

Position: Long SPY (VS), QQQ (VS)

BY Doug Kass · Jul 8, 2026, 8:00 AM EDT

Dougie Kass just now

Trade the News reports: “Reportedly Pres. Trump did not repeat termination of interim deal with Iran during the NATO summit.”

Position: None

BY Doug Kass · Jul 8, 2026, 7:51 AM EDT

Position: Short MU (VS)

BY Doug Kass · Jul 8, 2026, 7:30 AM EDT

Yesterday CNBC’s Halftime show universally applauded Apple (AAPL). The cheerleaders were led by an uber confident (oops, another poor-performing investment recommendation (UBER)!) and assertive (and even sometimes yelling) panelist (Josh Brown), signaling that Apple’s shares are the premier investment in the Mag 7:

Josh Brown likes this ‘sleeping giant’ AI play and Magnificent 7 member

Here is a contrary view (something that is rarely considered in the business media that worships at the altar of price) — focused on the company’s valuation at 10.4x sales (the highest in history) and that, fundamentally, Apple’s sales have been roughly flat for five year:

Caveat emptor.

Position: None

BY Doug Kass · Jul 8, 2026, 7:15 AM EDT

From Michael Burry:

Position: None

BY Doug Kass · Jul 8, 2026, 6:50 AM EDT

From my pal George Noble:

Position: None

BY Doug Kass · Jul 8, 2026, 6:40 AM EDT

Position: None

BY Doug Kass · Jul 8, 2026, 6:30 AM EDT

Position: None

BY Doug Kass · Jul 8, 2026, 6:20 AM EDT

* Trading opportunistically and dispassionately…

Yesterday, among other activity, we added to shorts in GRNY, C and JPM.

I remain bearish.

Today’s ceasefire news will likely provide an opportunity to cover some shorts — something I like to do in a “newsy” backdrop.

I would anticipate reshorting the inevitable rallies than have followed a breakdown in negotitations with Iran.

Position: Short GRNY (L), C (M), JPM (M)

BY Doug Kass · Jul 8, 2026, 6:10 AM EDT

The S&P Short Range Oscillator remains overbought at 3.28% vs. 3.20%

Position: None

BY Doug Kass · Jul 8, 2026, 6:00 AM EDT

Break in!

President Trump’s ceasefire comments are taking futures lower (and crude prices higher) in the last hour:

Live updates: Trump says Iran ceasefire is ‘over’ after new attacks, but negotiations can continue

Position: None

BY Doug Kass · Jul 8, 2026, 5:52 AM EDT

Procol Harum’s Denmark performance of “A Whiter Shade of Pale” is regarded as one of the greatest live renditions of the song ever recorded. The band performed with a 72-piece orchestra and a 50- to 70-member choir. It has over 122 million views on YouTube.

World's Largest Data Center Campus On Verge Of Collapse After Blackstone Unexpectedly Pulls Out zerohedge.com/technology/wor…

A key witness for Smart Approaches to Marijuana (SAM), one of the nation’s leading anti-cannabis groups, acknowledged during the DEA’s ongoing marijuana rescheduling hearing that cannabis fits the legal definition of a Schedule III controlled substance. themarijuanaherald.com/2026/07/sam-wi…

BREAKING 🚨: Japan Japan's 10-Year Yield hits 2.87%, the highest level in 30 years 🤯 👀

Mkts are currently considering Trump's conundrum after his remarks this morning: "To TACO, or not to TACO, that is the question: Whether 'tis nobler in the mind to suffer The slings and arrows of outrageous fortune, Or to take arms against a sea of troubles"

I know we are only halfway through the year, but I feel it will be hard to top this comment from one of the obligatory buy recommendations on $SPCX issued by one of the underwriters this week. It is truly glorious.

The June FOMC minutes are interesting: they frame the committee's divide as a split over the outlook, not necessarily over tactics. Note the symmetry here: "Almost all" participants think higher rates will be needed if inflation pressures don't dissipate. "Almost all" also Show more

Losing money from a healthy correction feels so much better than from an unhealthy correction;) Please note not even oversold YET.

Fund Managers are now sitting on the lowest cash allocation in history 🚨

The CNBC Panelist Said What? (Issue #9) Halftime's Jim Lebenthal becomes the first repeater (Adobe $ADBE was his previous mistake) in my series (and this time, with two additional investment boners)... Consider Jim's long time recommendation of Oracle $ORCL and, most Show more

The CNBC Panelist Said What? (Issue #8) Halftime's Bryn Talkington seems to evaluate equities based solely on moving averages and by occassionally listening to company EPS calls (which I generally view as consensus and a shallow way of selecting portfolio candidates). As far as

"If you told me 3 months from now, all of a sudden Anthropic's revenue or OpenAI's revenue stopped or stopped growing, that would be a real problem." I don't get it, why are they confessing?

AI compute prices are completely collapsing. This is going to impact AI data center gross margins at the worst possible time. Keep in mind, even at peak pricing all of these AI providers were extremely unprofitable. The decline in private credit funding has forced them to

What are YOU thinking??? Seriously. Apple trades at 10.4x sales. The highest valuation in the company's history. Higher than 2000. Higher than 2007. Here's the part that should stop you: revenue has been roughly flat for five years. The stock kept climbing anyway. The entireShow more

What happens when a company becomes one of the 10 largest stocks in America? Dimensional studied every case from 1927 to 2020. Before joining the top 10, the average company beat the market by: – 24.2% per year in the 3 years before – 19.1% per year in the 5 years before –